DNOW Inc.: A Diversified Approach Will Offset The Near-Term Sluggishness

Summary

- DNOW has a strong base with cash flow growth in 2024, strong liquidity, and reasonable valuation compared to peers.

- The company focuses on expanding revenue bases in traditional and non-traditional operations, with opportunities in various sectors and international markets.

- DNOW aims to strengthen market share through industrial offerings, with key strategies in actuated valves, PVF products, and digital initiatives.

bjdlzx/E+ via Getty Images

DNOW Has A Strong Base

I have discussed DNOW Inc. (NYSE:DNOW) in the past, and you can read the latest article here, published on November 8, 2023. In the near term, muted US drilling and completion activities following low natural gas prices and customers’ budget constraints will likely affect the company’s outlook. Although its operations in international markets are unlikely to recover, the company made headroom in electrical products. In non-traditional operations, I see traction in applications like soda ash mines, lithium extraction, and CCUS.

The cash flow growth in 2024 made a noticeable difference to the company’s financial strength. Its liquidity is strong, and it has recently extended its credit facility. The stock appears reasonably valued compared to its peers. I think the returns will improve in the medium-to-long term. So, I would suggest investors "hold" it.

Why Do I Keep My Call Unchanged?

In my previous article, I discussed how DNOW invested in supercenters and won large project awards in various sectors. Customer budget exhaustion and fewer business days affected its outlook, but cash flow growth improved its financial strength. So, I thought the stock was apt for a "hold." I wrote:

DNOW focused on expanding its revenue bases after it won large awards in gathering projects, midstream compressor stations, and centralized tank battery builds. It caters to the rising tide in workover rig programs and decarbonization projects. Lower iron and steel mills compared to a year ago should improve its operating margin. However, I see a lack of growth drivers in its international operations while the US energy market goes through an uncertain period.

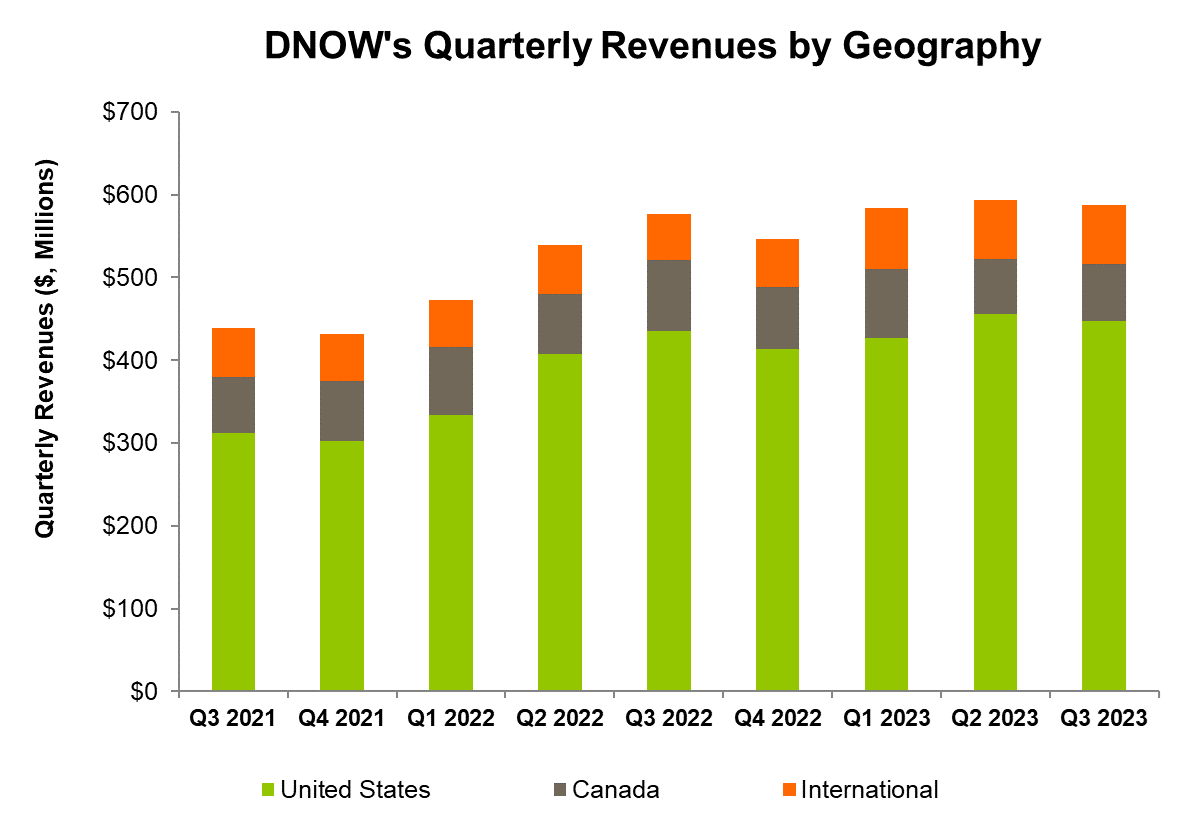

In Q2, DNOW strengthened its distribution in the municipal water market. In international operations, electrical products will lead the charge. In valve product, it secured new projects in Australia and Southeast Asia. Low steel prices should help expand its operating margin. However, US drilling and completion activity slowdown and energy operators’ capex conservativeness can keep its sales growth muted in the near term. So, I have kept my rating unchanged at a “hold.” Since my last publication in November 2023, the stock price appreciated by ~20%.

Strategy And Key Drivers

DNOW sees opportunities in both traditional and diversified operations. A higher demand for mobile horizontal trailer solutions (for water disposal and enhanced oil recovery applications) led to a higher Flex Flow H Pump rental utilization. The company aims to strengthen its market share through industrial air packages, mechanical seals, pump service, and repair offerings. With that objective, it added a new pump manufacturer distribution in the municipal water market. The company’s pump packages, mechanical seals, and field service have been used in multiple industries, including mining and chemical processing.

In international operations, DNOW expects electrical products to lead the charge, followed by PVF products. An FPSO project in Australia and an LNG project in Southeast Asia are notable projects where DNOW has offered its valve product. In addition, it has recently secured a supply agreement contract in Norway. In DigitalNOW initiatives, the company recently completed an e-commerce catalog project.

DNOW’s key strategies involve providing actuated valves to E&Ps and midstream companies. Its PVF products are tied to a natural gas gathering project in the Gulf Coast markets and used for LNG export. They include carbon capture and sequestration. The PVF products also upgrade existing infrastructure to eliminate greenhouse gas leaks. Another example of the use of pumps, pipe valves, and fittings products is in soda ash mines and the extraction of lithium to support growth in battery production. Another application is in offshore wind projects.

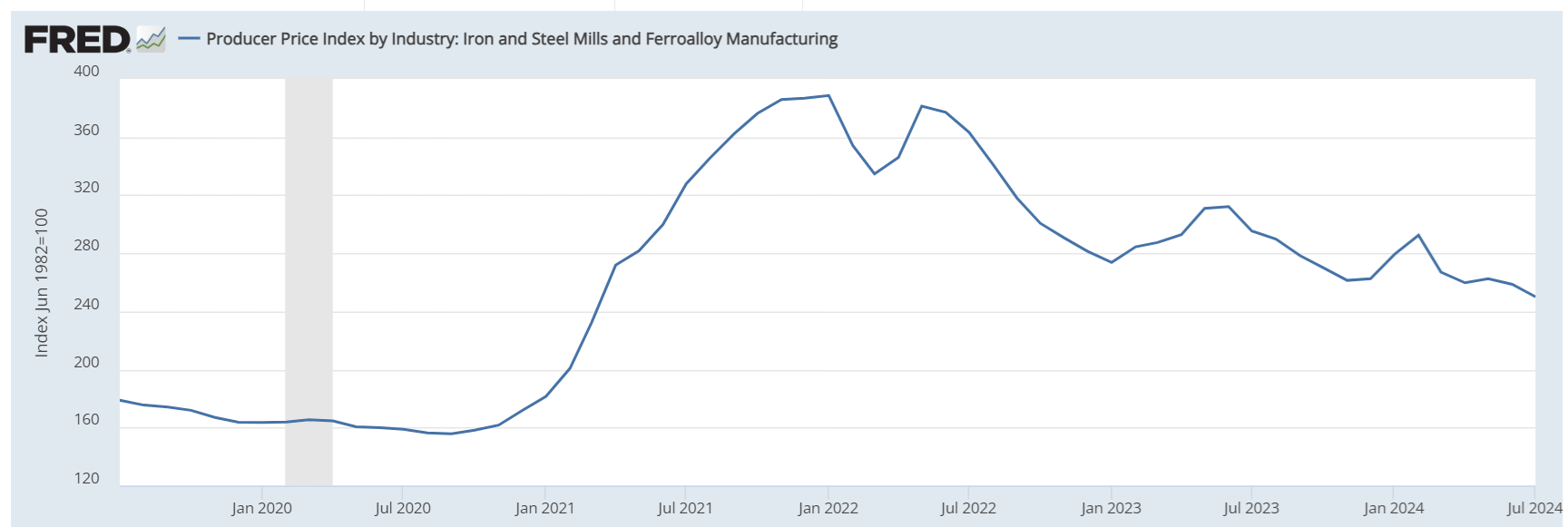

Steel Prices

FRED data

The PPI for iron and steel mills decreased by 15% in the past year until July, indicating a fall in input cost. Prices declined due to weaker industrial activity. The manufacturing PMI has recently fallen into the contractionary terrain (i.e., less than 50) following a decline in new orders. Lower iron & steel prices can ease DNOW’s margin. However, the decline rate has slowed down since March. Given the manufacturing sector's slowness, I do not see steel prices recovering anytime soon.

Outlook

Seeking Alpha

DNOW’s management expects the US drilling and completion activities to remain “muted” in Q3 compared to Q2 due to low natural gas prices and customers’ budget constraints. The political environment also does not appear suitable for new investments. Internationally, too, Q3 can turn out to be sluggish. In Canada, however, Q3 is the best quarter for energy activities.

Given these drivers, DNOW’s Q3 revenues can stay unchanged or decline by 5%. Its Q3 adjusted EBITDA margin can contract to 7% from 7.9% in Q2. In FY2024, its topline can increase by “low-to mid-single-digit” compared to FY2023, while its adjusted EBITDA margin can range from 7% to 7.5%. Also, it expects to generate $200 million in free cash flow in FY2024.

My Estimates

Over the past three years, the company’s adjusted EBITDA increased by 6.4%. I expect the US manufacturing index to remain steady, but may witness some downside in 2024. I also expect its international revenue and margin to continue to push higher. Given the company’s initiatives to improve its margin, its adjusted EBITDA should increase moderately, by 6% to 10%, in the next four quarters.

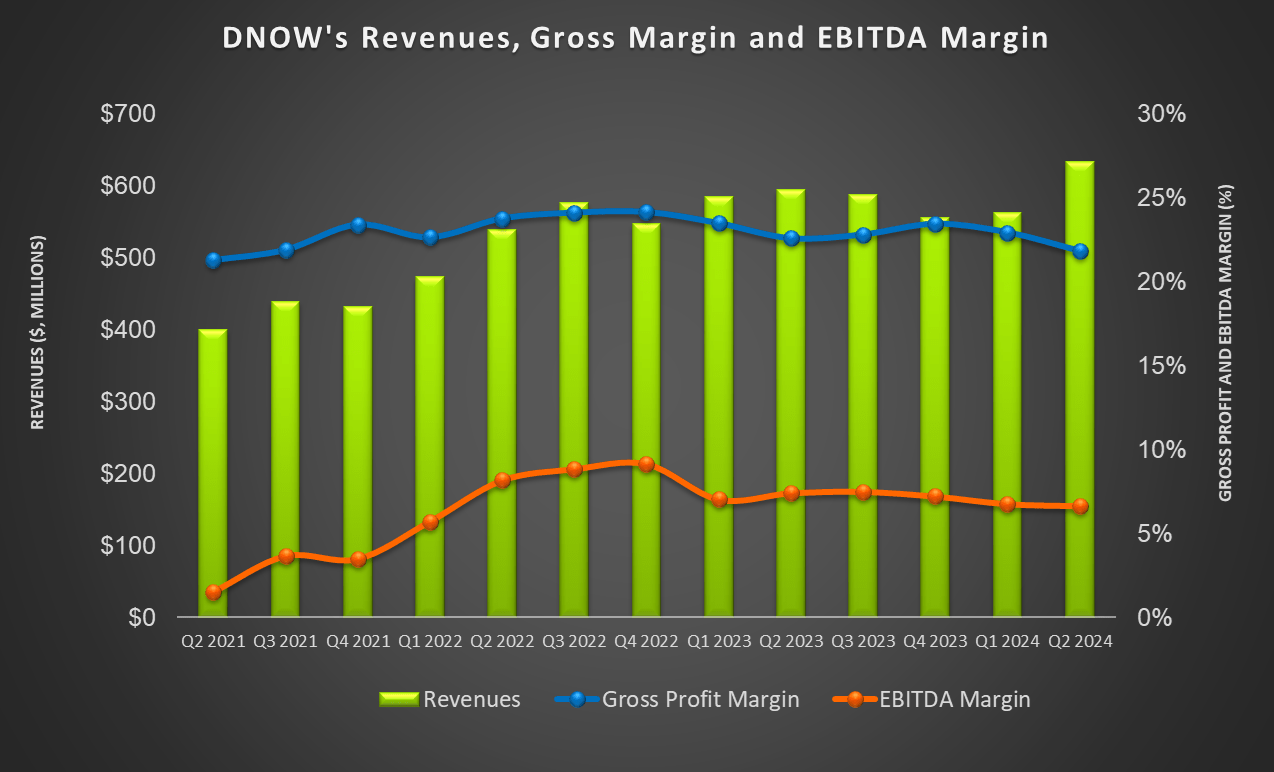

A Discussion On Q2 Drivers

DNOW's Filings

In Canada, DNOW's revenues decreased by 15% quarter-over-quarter in Q2 due primarily to the unfavorable impact of the seasonal breakup and lower gas prices. The company’s international business revenue increased by 5% in Q2. During this period, its revenues from the US increased by 18% because its US Energy Centers and Process Solutions businesses performed well. The Whitco Supply acquisition also boosted the US revenue. The result was remarkable, given the 3% drop in the US rig count and 4% drop in completion activities.

During Q2, DNOW undertook consolidation measures to improve customer service and enhance efficiencies, including consolidating third-party operating yards to a single centralized yard. In the Bakken, it aims to complete a refract program wells to improve production. It secured a supply contract in the Northeast to provide natural gas, LPG, electricity, and renewable energy solutions. It also diversified into adjacent markets, including the mining sector, municipal water, and chemicals markets.

Cash Flows And Balance Sheet

In 6M 2024, DNOW’s cash flow from operations (or CFO) increased by 29% compared to a year ago, due primarily to favorable changes in net working capital. However, its capital expenditure increased sharply, leading to negative free cash flow. However, excluding acquisition expenses related to Whitco Supply, its FCF was positive in 6H 2024.

DNOW's liquidity was $682 million as of June 30, 2024. It has a robust balance sheet with zero debt. Its revolving credit facility extends into December 2026, providing immediate access to capital.

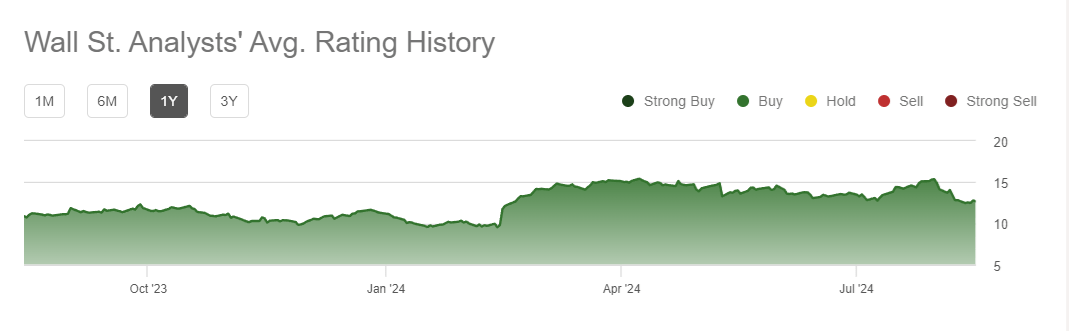

Analyst Rating

Seeking Alpha

Two sell-side analysts rated DNOW a "Strong Buy" in the past 90 days. None rated it a "sell," while one analyst rated it a "hold," The consensus target price is $15, suggesting a 15% upside at the current price. Given the value drivers discussed above, I think sell-side analysts are slightly more optimistic than reality warrants.

Relative Valuation And My Target Price

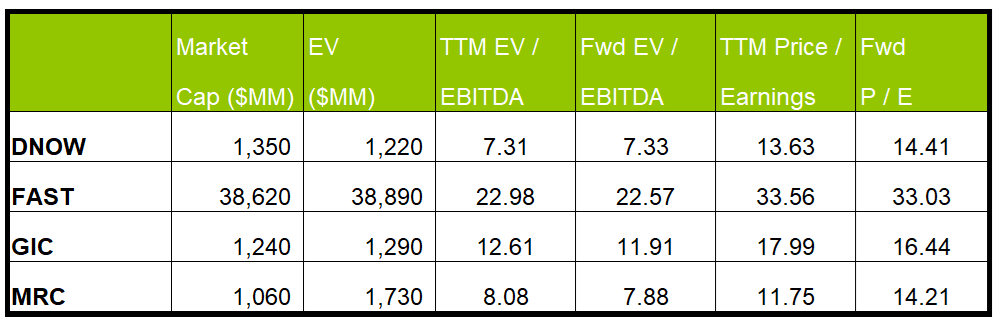

Author Created and Seeking Alpha

DNOW's current EV/EBITDA is expected to remain unchanged versus the forward EV/EBITDA multiple. For its peers, the multiple is expected to contract. This indicates that DNOW’s adjusted EBITDA can remain unchanged compared to a rise in EBITDA for its peers. This typically results in a lower EV/EBITDA multiple. The company's EV/EBITDA multiple (7.5x) is much lower than its peers' (FAST, GIC, and MRC) average (14.6x). So, the stock appears to be reasonably valued compared to its peers.

As I discussed earlier in the article, I expect a 6% to 10% adjusted EBITDA growth in the next four quarters. Feeding these values in the EV calculation and assuming the sell-side current EV/EBITDA multiple of 7.3x, I think the stock should trade between $13.8 and $14.3, implying a 6%-10% upside.

Risk Factors

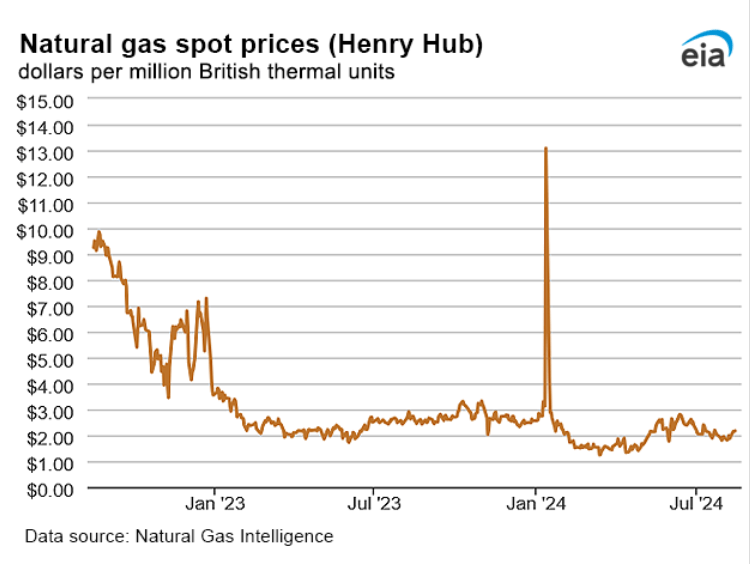

EIA

Depressed natural gas prices in the US kept DNOW’s revenues and margins depressed in 2024. From January to May, the price of U.S. natural gas imports declined by 71%, and it fell by 67% in 2023. Low natural gas prices and customers’ budget constraints also kept its Q3 outlook relatively dull. However, there is glimmer of hope because the EIA expects the Henry Hub futures price to increase in September through August 2025.

What's The Take On DNOW?

Seeking Alpha

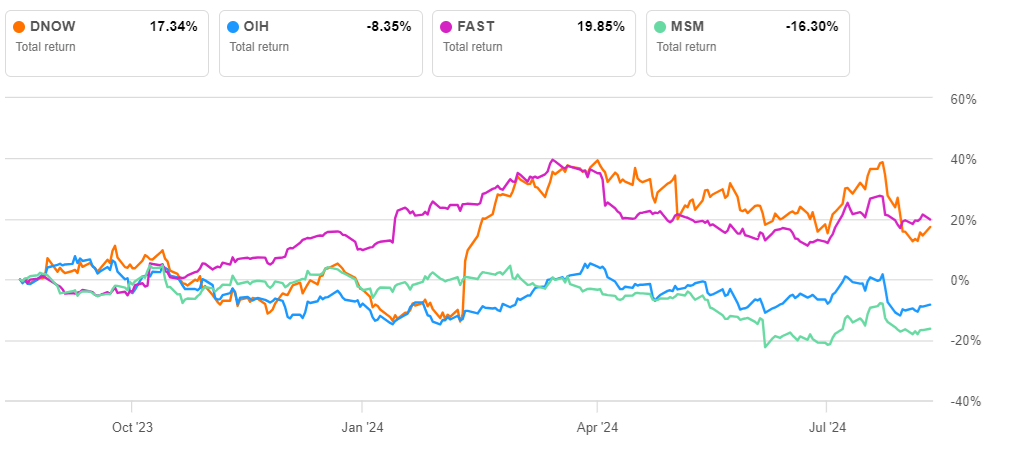

In energy and valves/pipes, a higher demand for mobile horizontal trailer solutions led to a higher Flex Flow H Pump rental utilization for DNOW in Q2. The company also aims to strengthen its market share through traditional offerings as the products find uses in multiple industries, including mining and chemical processing. In new energy fronts like CCUS, DNOW’s PVF products have been used to upgrade existing infrastructure. They have also been used in soda ash mines and lithium extraction. Internationally, the company received projects in Australia, Southeast Asia, and Norway. So, the stock underperformed the VanEck Vectors Oil Services ETF (OIH) in the past year.

However, due to low natural gas prices and customers’ budget constraints, I see growth impediments. Its operating margin can also contract in Q3, although I expect the momentum to pick up over the next four quarters as energy prices stabilize. The company has a robust balance sheet and positive cash flow. So, I reiterate my “hold” call.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.