Equity Residential: Good Quality But Pricey

Summary

- Equity Residential focuses on niche markets in highly dynamic and desirable cities with high home price to income ratios.

- The company benefits from renters staying due to financial incentives to rent over buying, but faces potential challenges with renter fatigue.

- Despite high occupancy rates and historical dividend growth, the company's premium valuation may deter some investors, especially in uncertain economic times.

Volodymyr Kyrylyuk/iStock via Getty Images

Equity Residential (NYSE:EQR) is a residential REIT which focuses on what some people might consider a niche market within apartment sector. The company owns and manages a number of apartment buildings in cities that are considered "highly dynamic" and "highly desirable" by highly-educated younger population such as Boston, San Diego, Seattle and Denver.

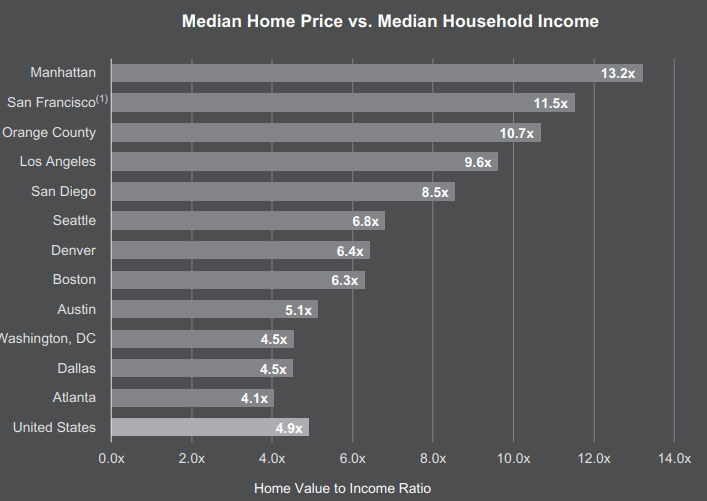

The company specifically invests in cities that fit its very specific criteria. The city has to have a high average income as compared to the US average, have a rising young population, be considered "hip" by highly educated younger people and most importantly have a high home price to household income ratio. Why is the last one important? Because if a city has high price to income ratio, it makes more sense for people to rent in those cities than buy. Since this company's main customer base tends to be renters with higher income, it always runs the risk that its renters might just decide to move out of their apartments and buy a house instead but if it makes little financial sense for them to buy a house over renting, it will keep them renting which is beneficial for the company. Below you can see that the average home price in the US is about 4.9x times the average household income whereas this number ranges from 4.1x to 13.2x in cities where this company owns apartments. Out of the 12 major the cities Equity Residential operates in, 8 have a price-to-income ratio of at least 6.3x which means people in those cities have little incentive to buy versus rent. This is even a bigger deal when interest rates are as high as they are right now because it increases cost of ownership even further.

Home Price to Income Ratios (Equity Residential )

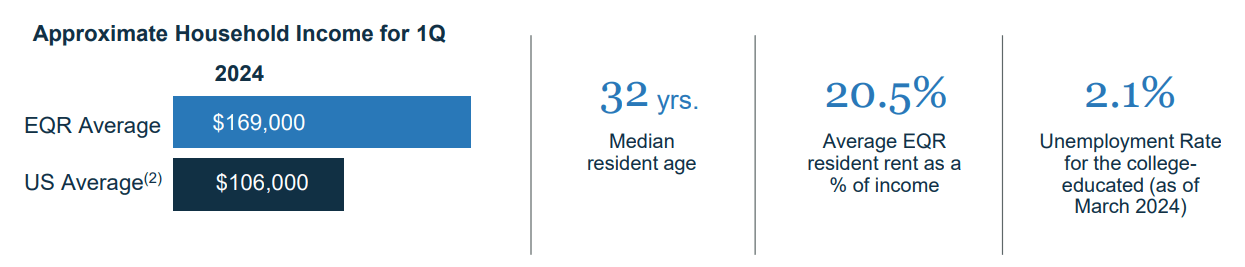

The company has every reason to want its renters to stay at its properties. When we look at the company's renter profile, we see that they have an average household income of $169k per year which is significantly above the US average of $106k. The average EQR renter spends only about 20.5% of their income on rent which means that not only will they have no trouble paying their rent but also they might be fine with handling some future rent increases. Considering that most of this company's renters are college-educated, it's noteworthy to add that the unemployment rate of college-educated Americans is only 2.1% as of March 2024 although this could easily change if the economy lost some of its strength in the coming months so there is room for caution while looking at this particular number.

Profile of EQR Renters (Equity Residential )

Between 2020 and 2023, we saw the inflation rage in the US (as well as the rest of the world for the most part) and apartment owners had little trouble passing on higher costs to their customers in shape of rent increases. On the other hand, they suffered from higher costs in property taxes, maintenance and repairs in terms of prices of both workmanship and materials. Now we are coming to a juncture where rent increases have come to a slowdown and customers started to shop around to find cheaper deals so in the future rent increases are likely to be smaller than what we saw between 2020 and 2023 especially if the economy sees further slowdowns or enters a recession.

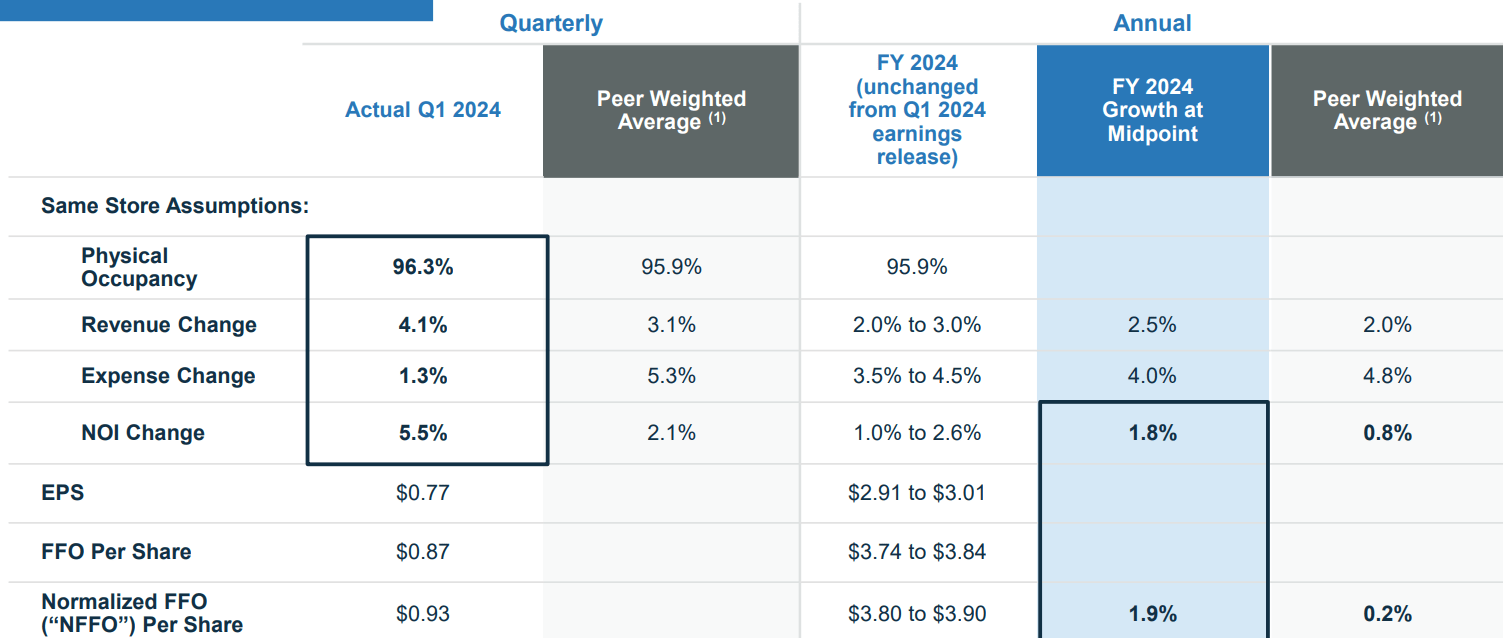

As a matter of fact, we might be already seeing some signs of renter fatigue in terms of price hikes. Earlier this year, the company reported a revenue increase of 4.1% for same locations. This came better than peer average of 3.1% but still much lower than what we saw a couple years ago. The company's guidance for the rest of the year calls for a revenue growth of only 2% to 3% while expenses are expected to grow from 3.5% to 4.5% so there are some signs showing that apartments can't just keep hiking their prices forever without any consequences.

Financial Results (Equity Residential )

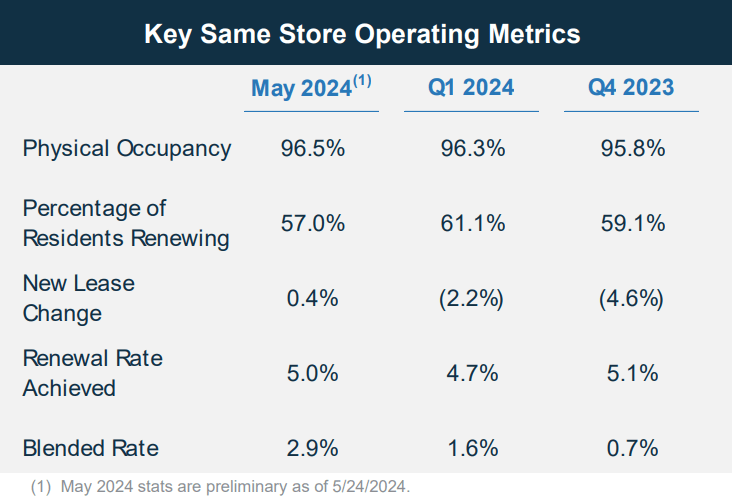

The company still enjoys a very high occupancy rate at 96.5% so it isn't having much trouble filling its apartment units. Meanwhile, percentage of existing residents renewing their contract is down slightly from 61% to 57%, indicating that people are now shopping around to find better deals instead of staying within their comfort zone and renewing their existing leases. It is also possible that a lot of renters are becoming first time home buyers but their number has to be small considering how both home prices and interest rates are very high right now.

Same Location Metrics (Equity Residential )

One thing is for sure, though. America still has a shortage of housing and this is not going to go away anytime soon. We are building far fewer homes than how fast our population is growing, and this creates an advantage for companies that own a lot of properties in a lot of desirable markets. Currently, American homebuilders are building about 1.5 million units per year, which is the same rate of homebuilding that happened in 1960 when the US population was half of today's population. Current high-interest rates are also making it very difficult for homebuilders to build more homes, not to mention we are running out of good quality land in desirable markets since that's one thing that can't make more of. This is definitely something to consider for residential REIT investors.

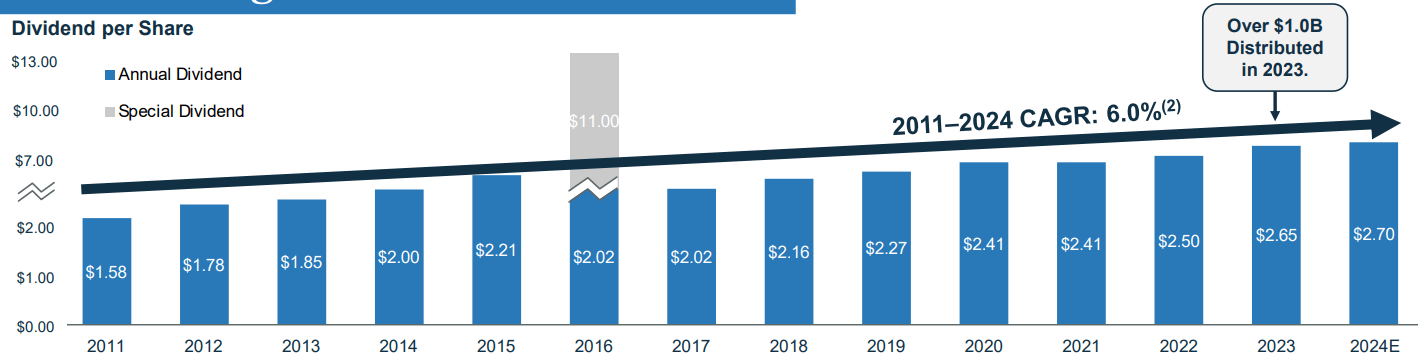

People invest in REITs mostly for income, and this company has a nice dividend yield of 3.72%. More importantly, it has a good history of dividend hikes. Between 2011 and 2024, the company has hiked its annual dividends from $1.58 per share to $2.70 per share, which is an annualized compounded growth of 6%. This means that investors saw their dividend income grow at a rate comfortably above the average inflation (below 2%) during this time. By now, people are used to the high inflation from the last few years, but they don't realize that inflation was actually very low until 2021 and US enjoyed a long period of low inflation which could make a comeback soon. Keep in mind that this company didn't hike dividends every single year, so it doesn't qualify as a dividend aristocrat. There are years where the dividend stayed flat, such as in 2021, but for the most part, the trend has been upwards in the long run, and we have little reason to believe this will change anytime soon.

Dividend History (Equity Residential )

One thing I must say about the company is that it is anything but cheap, though. Since this is a REIT we have to price it based on AFFO metrics and the company has a P/AFFO ratio of 20-23 depending on whether you are looking at trailing or forward metrics, which compares poorly to the sector median of 15-16 and offers a premium of 30-40%. Some could say that it is worth the premium because of its high quality, but this is something investors will have to decide themselves whether they want to pay a premium or not. If we learned anything from the stock market in the last 15 years, good quality rarely comes cheap (if ever) and investors will often pay a premium for it. But not all investors will feel comfortable paying a premium either, especially if it's as large as 30-40% versus sector median.

Valuations (Seeking Alpha)

The overall economy is showing signs of weakness or slowdown, and many investors are now expecting a recession. Historically, recessions have been incredibly difficult to predict and economists have a poor track record of predicting it ahead of time, so I don't know if we will actually have a recession or not especially when the government is posting multi-trillion deficits right now which acts as an invisible stimulus for the economy. Having said that, if the economy enters a recession, you might get an opportunity to buy this stock at a cheaper price. Then again, if the Fed cuts rates and the economy avoids recession, the premium on the stock could go even higher since other income vehicles will have lower yields as a result of the Fed's actions.

This stock basically becomes a bet on whether you believe in the US economy in the next few years or not. If you are bullish on the overall economy, this could be a good bet but if you are feeling bearish about the economy, you might want to wait for a better entry point.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.