Feeling Left Behind? 3 Dividend Stocks For A Worry-Free Retirement

Summary

- Retirement planning varies greatly depending on personal situations. Assess your expenses and create a plan tailored to your needs, considering risk and financial goals.

- For most investors, ETFs provide a simple and effective way to build wealth over time, offering diversification and stability without the need for constant stock-picking.

- Solid long-term investments can offer a mix of growth, income, and reliability. Focus on options that align with your retirement timeline and financial objectives.

yorkfoto

Introduction

I have to be honest. One of the hardest parts of my job is putting myself in other people's shoes.

When I make financial decisions, I obviously make them based on my personal situation. As I'm 29, my goals are very different from someone who's retired, close to retirement, or a freshman in college.

To make matters more complicated, age is just one of many variables. Some people have high-paying jobs and no mortgage. Others have to work additional jobs to have excess capital to invest. Then, there are health differences, different tax situations, family structure differences, and so much more.

I'm bringing this up because I just read a fascinating article from The Wall Street Journal titled "How to Plan for Retirement if You're Behind On Saving In Middle Age."

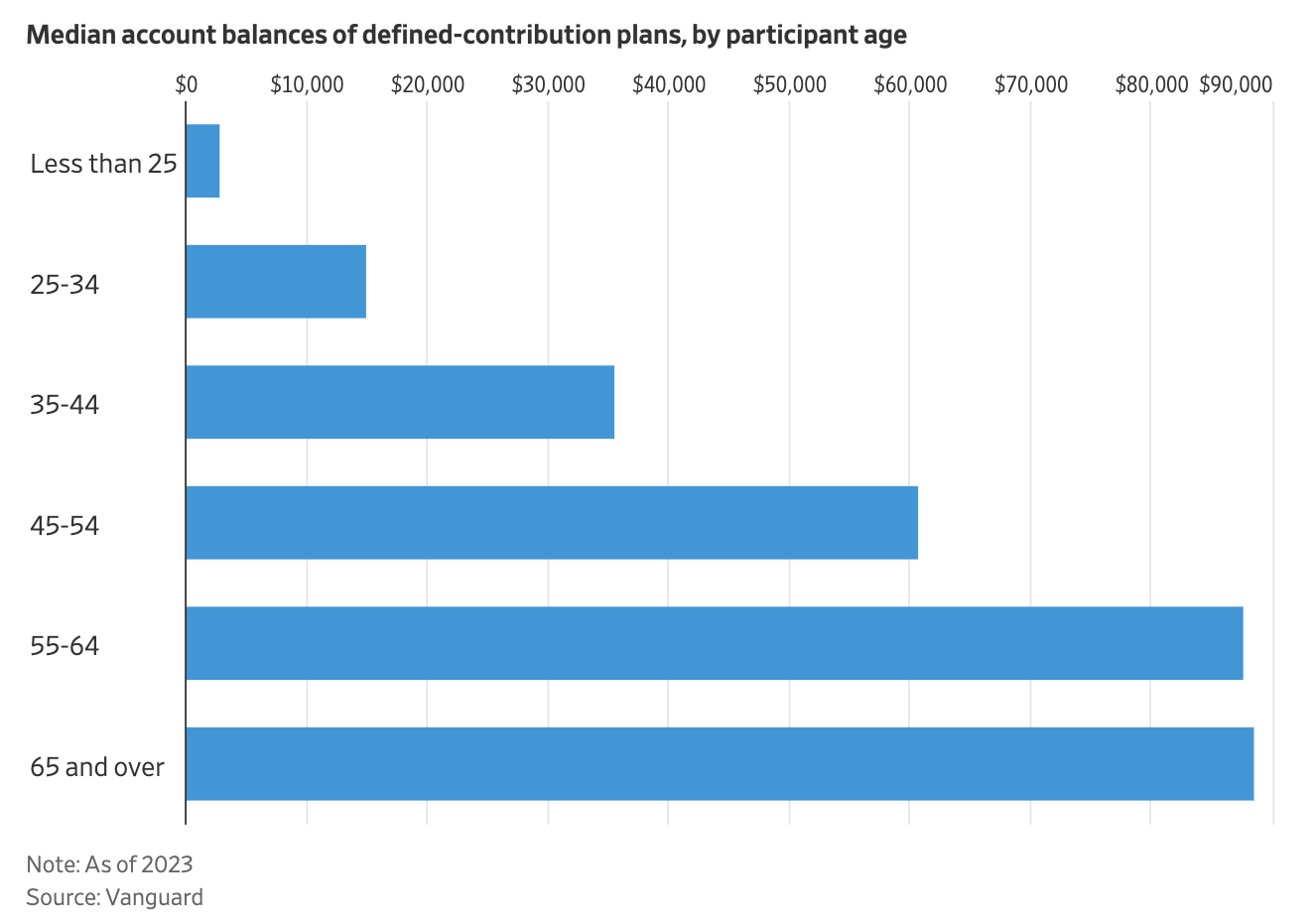

According to the article, workers between 45 and 54 years old had a median account balance of roughly $60,000 in employer-sponsored retirement plans, including 401k plans at Vanguard in 2023.

This is below the general target of having roughly six times one's annual salary saved for retirement by age 50. Again, it's a rule of thumb. Many cases are unique.

The Wall Street Journal

While many are way behind on their goals, there's hope.

In order to prepare, there are a few steps one can take.

- Assessing one's expenses. If you know how much you spend on average, you can cut unnecessary expenses and roughly estimate how much in (passive) income you may need to retire. That's where the first differences come in.

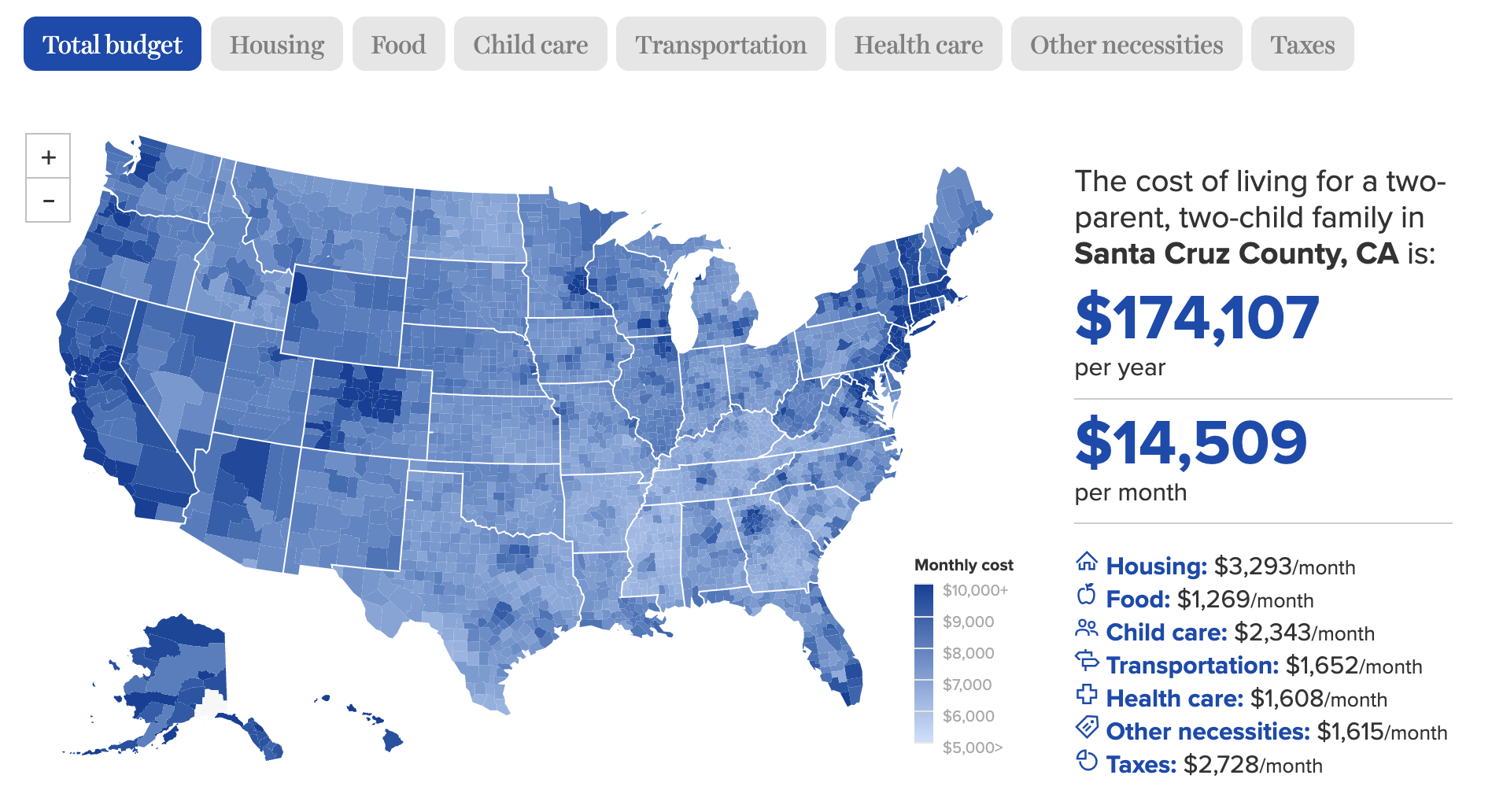

For example, a two-parent, two-child family in Santa Cruz (I went for an extreme here) needs at least $14,500 per month to cover basic expenses, including housing, food, child care, transportation, and other necessities.

Economic Policy Institute

If you live in Leslie County, Kentucky, that number is less than $7,000.

While retired people won't have to take care of children and have different costs, it's a good example of how different personal situations are. It's important to be aware of that. Some people can retire with much less than others.

In many cases, this step shows that people are better off than initially expected.

Historically, retirees have had a low probability of running out of money if they withdraw 4% of their retirement savings in their first year of retirement and then adjust that amount for inflation in subsequent years.

Some advisers say their clients often find themselves in a better spot than they originally thought after assessing their finances.

“A lot of people have just never really totaled everything up,” said Martin Schamis, head of wealth planning at Janney Montgomery Scott. - WSJ

- Creating a plan. Once you know what you need and how much you can invest, it's time to make a plan. This is where it gets tricky. If you're close to retirement with a million in cash, you will probably (this isn't advice) buy more bonds than stocks to lower downside risks and lock in some income. If you're 40 and far away from your retirement goal, you'll have to take on more risks. We can also make other decisions, including delaying retirement, working part-time in retirement, postponing taking Social Security, downsizing our homes, and so much more.

There are also many people who prefer to spend more when they are still "young," as the older we get, the less energy we have.

Richard and Lorena

Essentially, it's all about tradeoffs, being aware of what we want, and planning to get there with the resources at our disposal.

In most cases, this means making smart investment decisions, which is what I like to focus on.

Hence, in the second part of this article, I'll present three great investments that, I believe, make sense for people preparing for retirement. In this case, I am not focusing on a niche but presenting three investments that I expect to make sense for a wide range of investors, regardless of whether you're 20, 40, 60, or 80.

Schwab U.S. Dividend Equity ETF (SCHD) - Keeping It Simple

Seeking Alpha is a special place, as it is dominated by readers who all enjoy building their own portfolios. That's also why the comment sections are always a joy to read. Everyone has a different strategy, favorite stocks, and unique views on macroeconomics and politics.

That said, in general, I believe most investors are better off investing in ETFs. I often tell younger investors to not worry about stock picking. Some people spent hours (or even days) to figure out where to invest $1,000. These people are much better off buying ETFs, as it will allow them to invest their time and energy into their jobs to build a higher income.

Moreover, in general, I believe most people (excluding people on this website) lack the expertise to research stocks. There's nothing wrong with that. It just needs to be incorporated in one's financial plan.

That's where the Schwab dividend ETF comes in.

I believe this ETF is the gold standard of dividend investing.

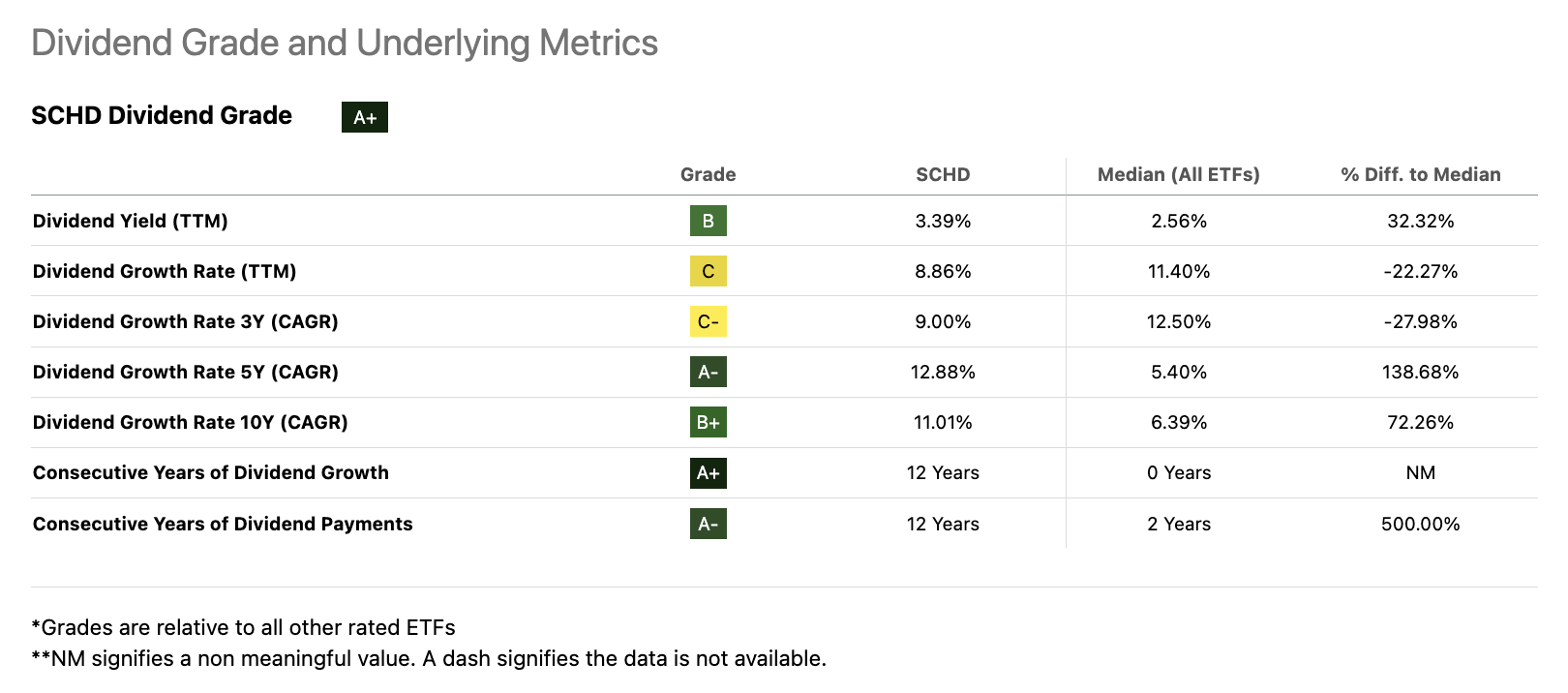

The SCHD ETF tracks the Dow Jones U.S. Dividend 100 Index. That's one of the reasons why its expense ratio is very low, at 0.06%. Currently, the ETF holds 103 individual stocks with a weighted average market cap of $131 billion, which shows the emphasis is clearly on a number of large dividend stocks.

Currently yielding 3.4%, the ten-year dividend CAGR is 11.0%. Although I do not expect that number to remain in double-digit territory in the current economic environment, I expect SCHD to maintain a fantastic mix of growth and income on a long-term basis.

Seeking Alpha

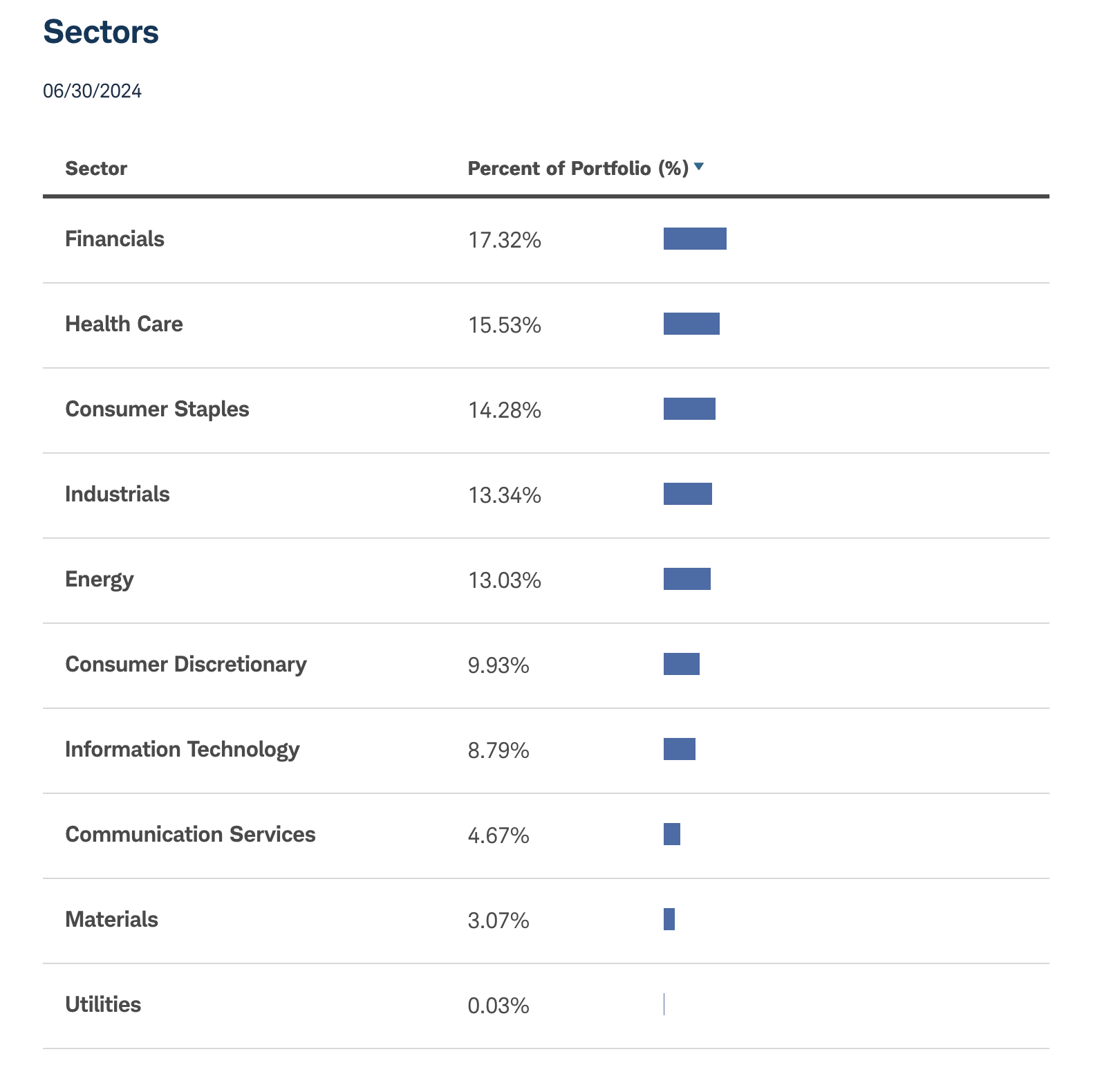

When zooming in a bit, we see the company has a well-diversified portfolio, with double-digit exposure to financials, healthcare, consumer staples, industrials, and energy. It also has significant exposure in consumer discretionary stocks, information technology, and communications services.

Schwab Asset Management

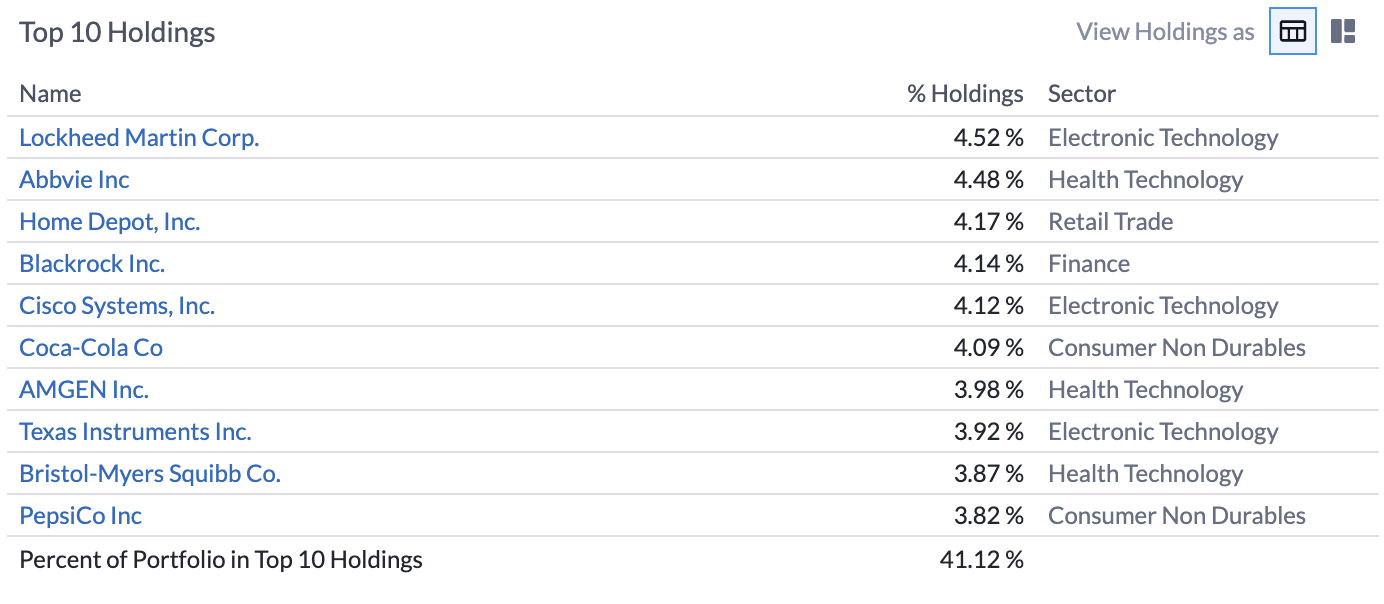

Its top ten holdings account for 41% of its total assets. This includes some of the best dividend stocks in the world (I think). I own four of the ten stocks listed below: Lockheed Martin (LMT), AbbVie (ABBV), Home Depot (HD), and PepsiCo (PEP).

FINVIZ

Although I cannot buy non-UCITS ETFs in the European Union, I have often said I would have 50% of my portfolio in SCHD if I had a different job and no time to research stocks all day.

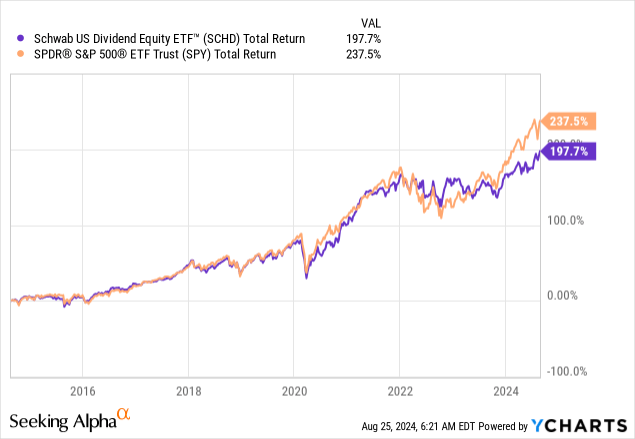

Moreover, over the past ten years, SCHD has returned close to 200%. Although this lags the S&P 500 by roughly 40 points, it's a fantastic return, as SCHD did not have the benefit of being top-heavy with tech stocks.

On a longer-term basis, I expect SCHD to beat the S&P 500, as it owns proven dividend growers with inflation protection, competitive business models, and often very healthy balance sheets. Especially if inflation remains elevated, I believe these dividend stocks are a great place to be.

Data by YCharts

Data by YCharts

The second pick of this article is one of SCHD's largest holdings.

Texas Instruments (TXN) - A Great Mix Of Growth And Value

Texas Instruments combines the best of many worlds, including growth, income, and secular tailwinds in the tech sector.

My most recent in-depth article on this company was written on July 14.

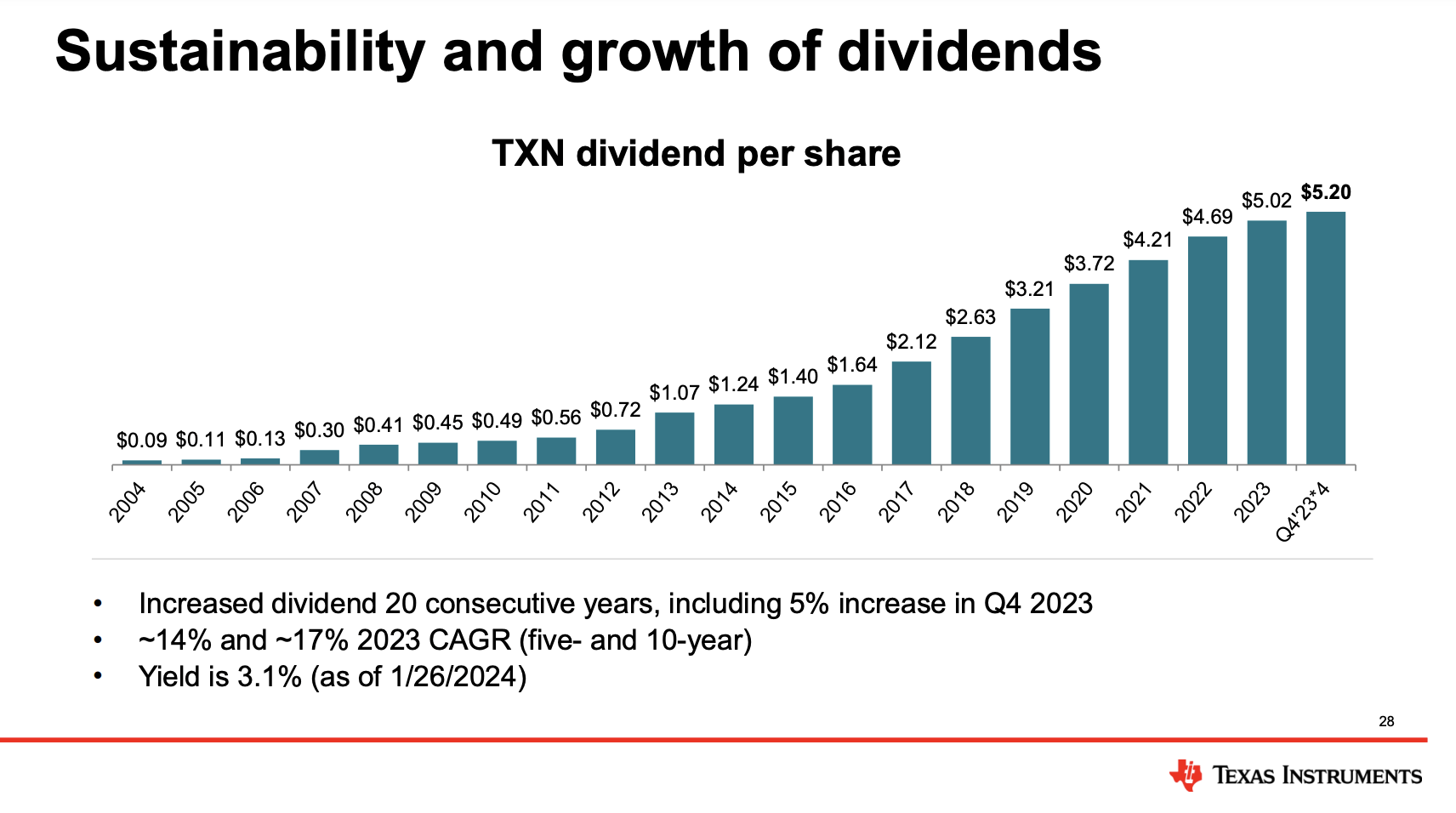

Back then, I used the chart below, which shows the company has hiked its dividend for 20 consecutive years, with a ten-year CAGR of 17%.

Texas Instruments

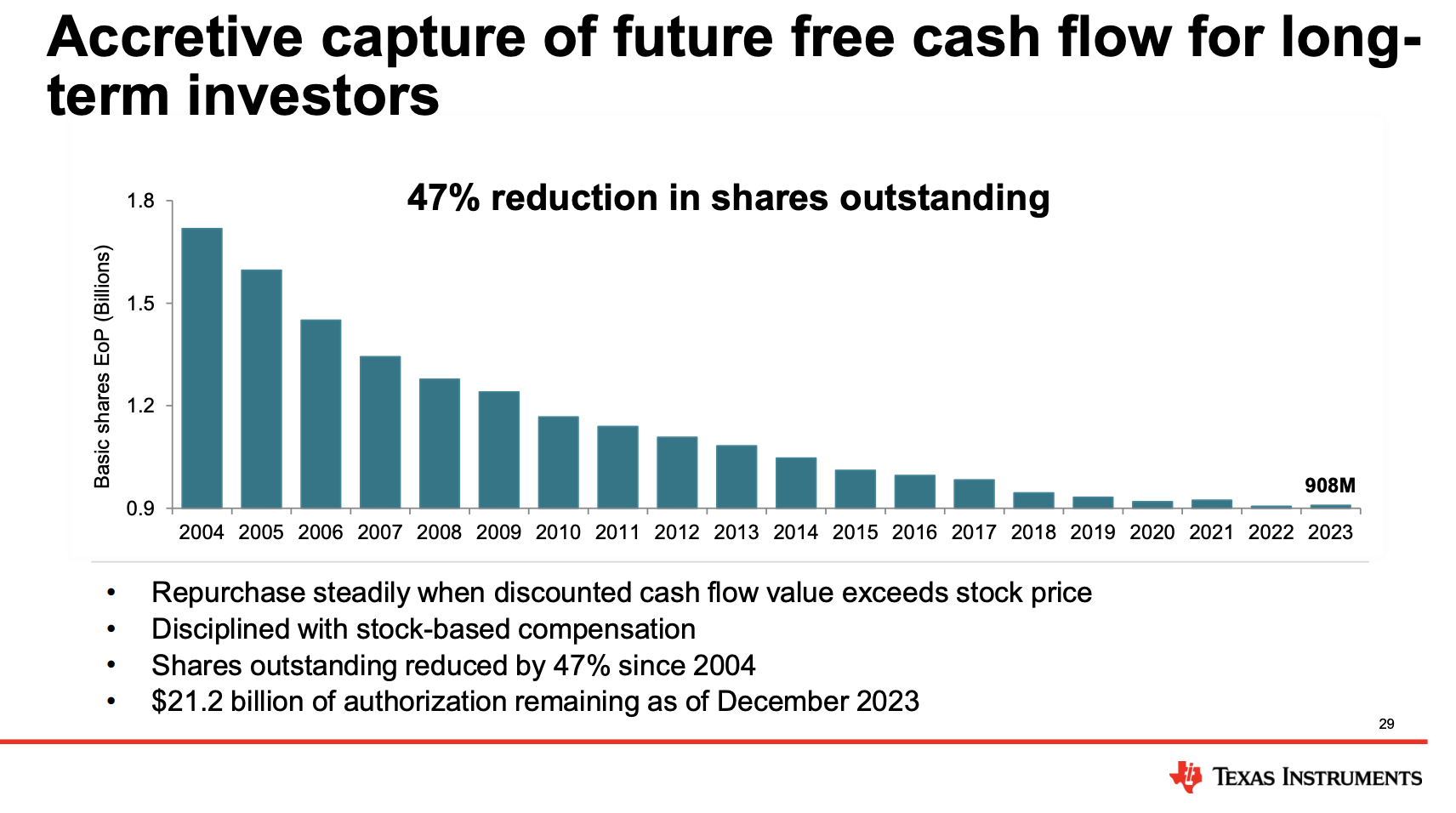

On top of that, it has bought back almost half of its shares since 2004. Going into this year, it had more than $20 billion in authorized buybacks, roughly 11% of its current market cap.

Texas Instruments

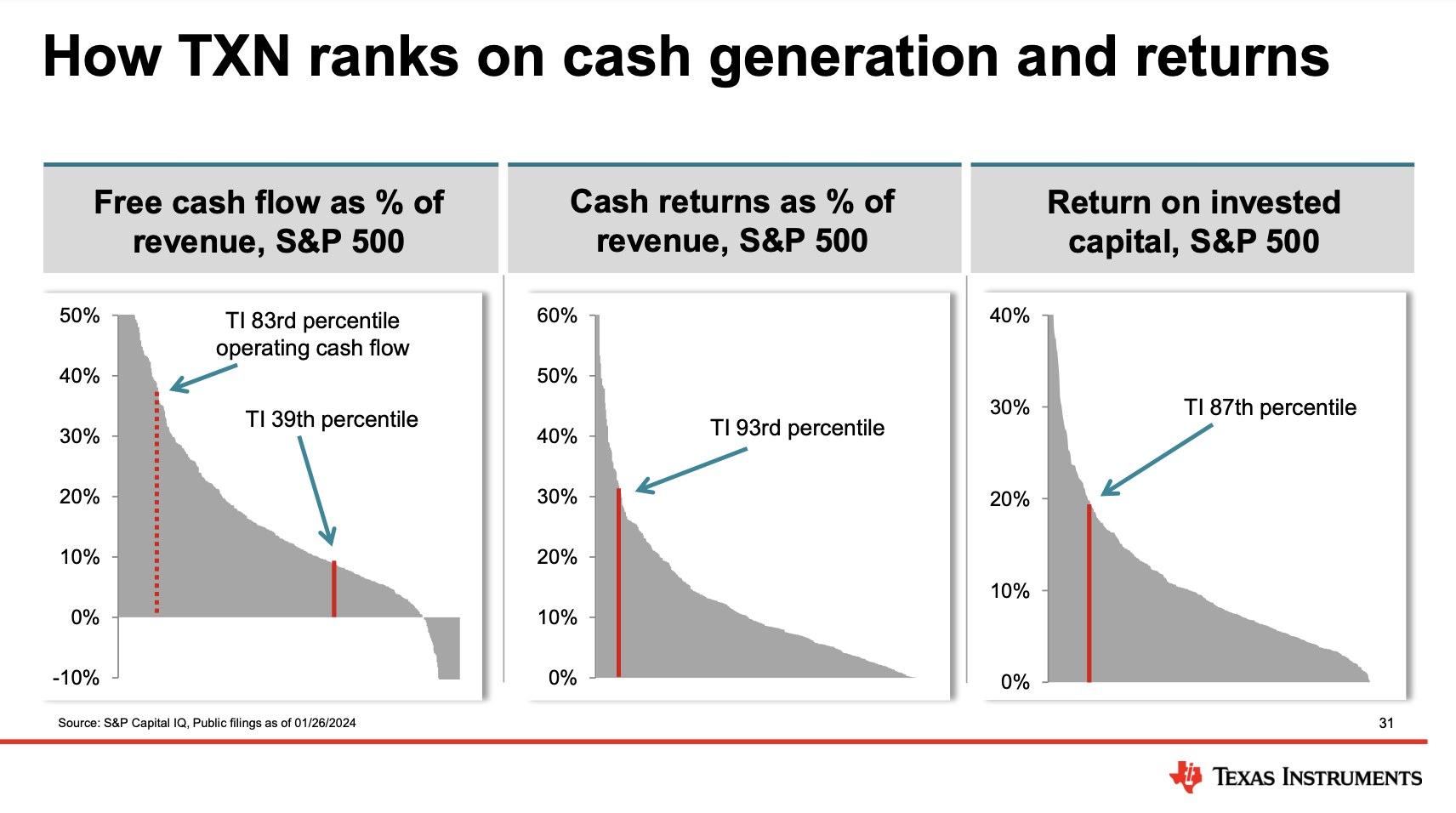

In fact, TXN is one of the most efficient companies in the S&P 500.

Texas Instruments

As a result, TXN has returned 472% over the past ten years. On top of that, it needs to be said it did not benefit from the AI and data center tailwinds that some of its peers benefitted from. TXN mainly produces chips for the automotive sector, which is cyclical.

Data by YCharts

Data by YCharts

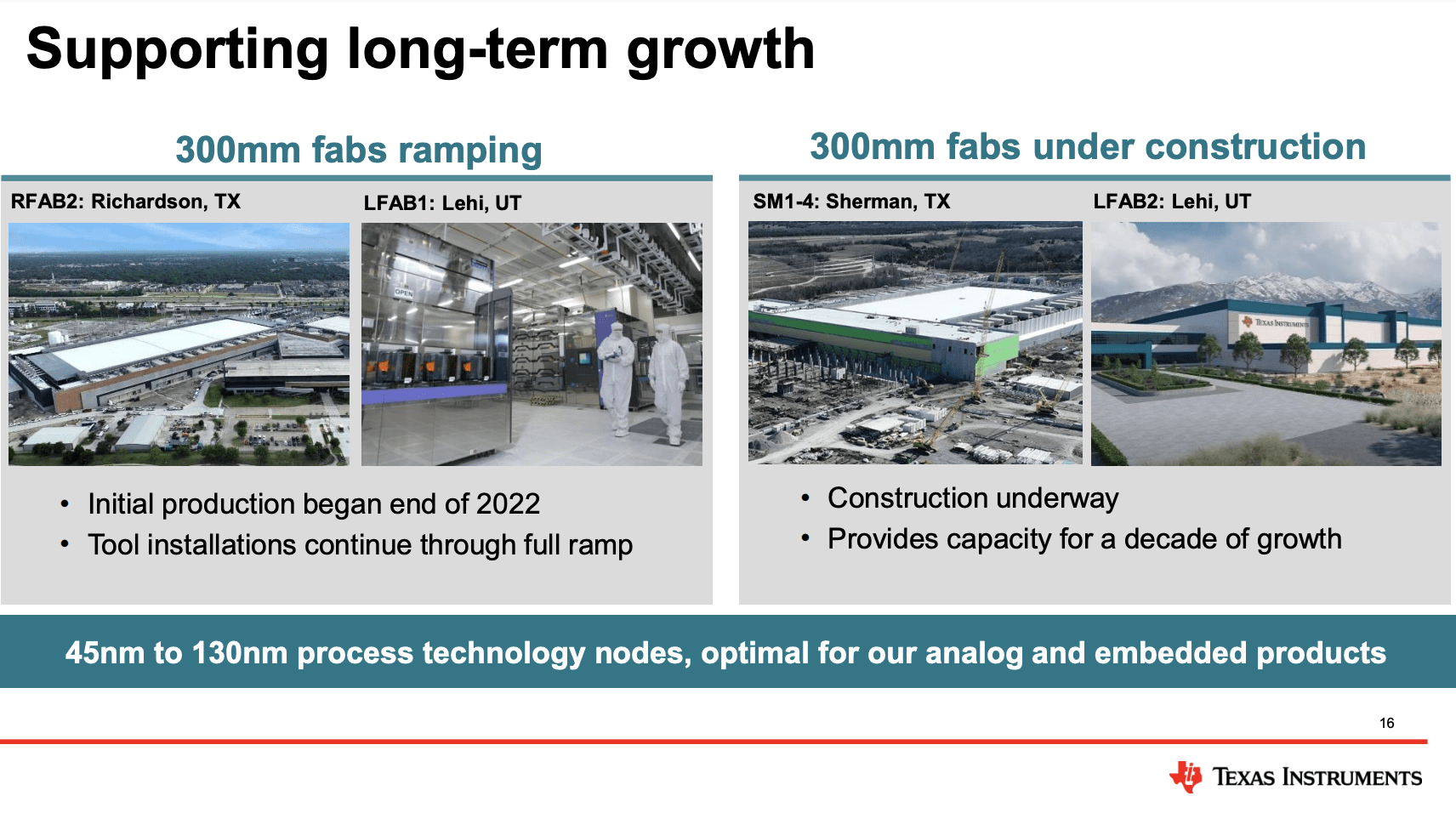

Right now, the company is aggressively investing in its production capacities in the United States. This is part of broader economic re-shoring and the de-risking of supply chains.

Not only does the U.S. want to become less dependent on China, but chips for cars and industrial purposes are increasingly critical. As I wrote in my in-depth article, in a modern electric car, the company places up to $1,000 in chips.

In 2024 and 2025, the company is investing roughly $5 billion per year in projects like RFAB2 and LFAB1, two massive facilities in Texas and Utah.

Texas Instruments

These investments are supported by tax credits and have resulted in massive supply chain benefits.

By moving loadings from external suppliers like TSMC and UMC to its own facilities, TXN has managed to lower its variable wafer costs from roughly $2,500 to $200.

Additionally, the 25% Investment Tax Credit ("ITC") that applies to RFAB2 and LFAB1 until 2026 further supports the financial attractiveness of the company's investments and puts an emphasis on investing as much as possible before the credits expire. - July Article

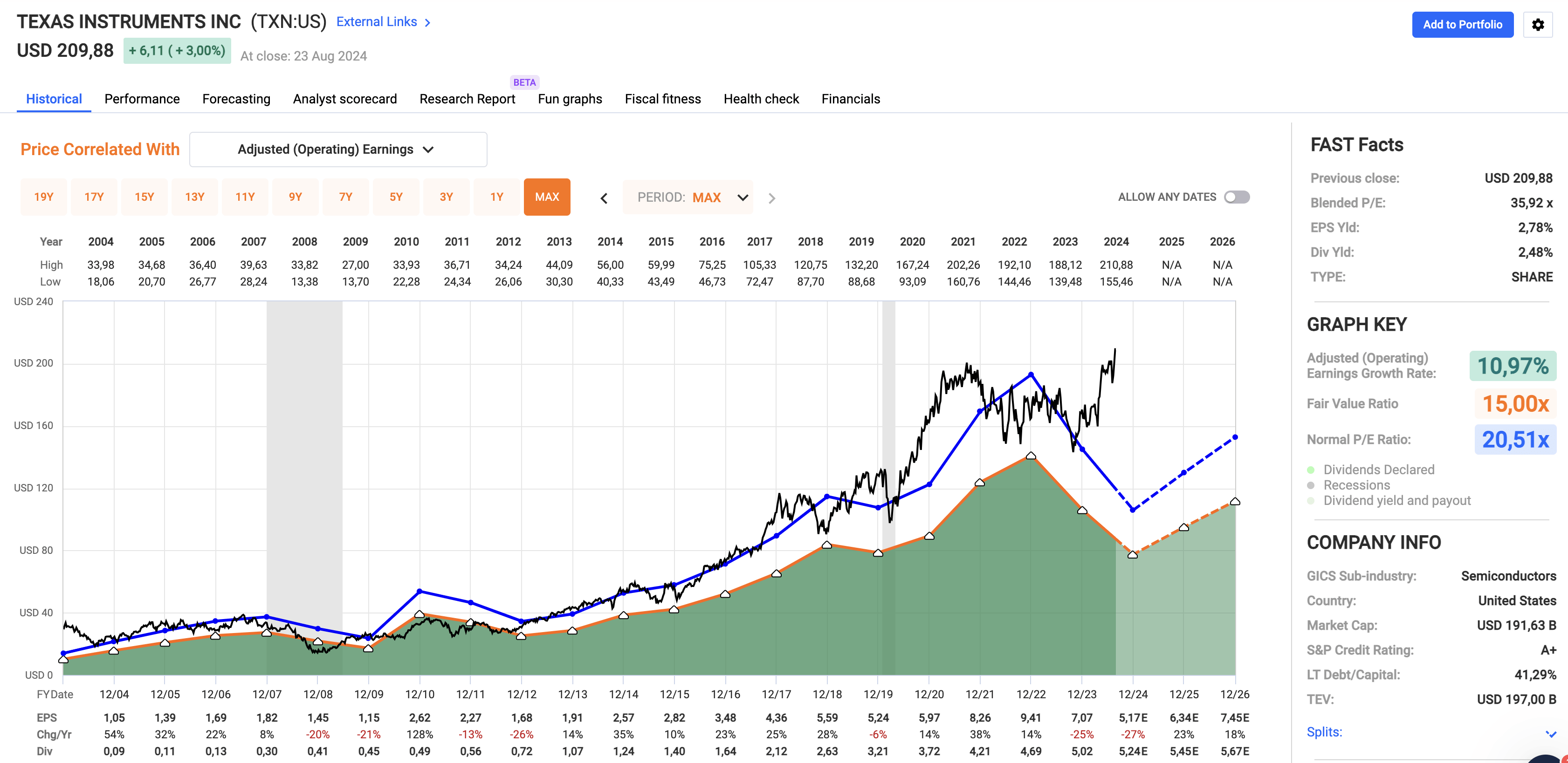

Valuation-wise, we're dealing with a company trading at a blended P/E ratio of 36x. Although this is elevated, it is the result of a 25% EPS contraction in 2023 and an expected EPS decline of 27% in 2024 - using the FactSet data in the chart below. This is due to economic weakness and automotive production being scaled back. However, in 2025 and 2026, EPS growth is expected to be 23% and 18%, respectively.

FAST Graphs

As such, the market has been looking past current weakness, with Citigroup giving the company a $235 price target on August 21, 12% above its current price.

While economic challenges could provide corrections in the TXN stock price, I believe the company is a great long-term investment to build income and wealth, just like the next stock.

Canadian National Railway (CNI) - Consistency With A Capital 'C'

Canadian National is Canada's largest Class I railroad. The only reason why I don't own this gem is that I already own three other railroads, including its peer Canadian Pacific Kansas City (CP).

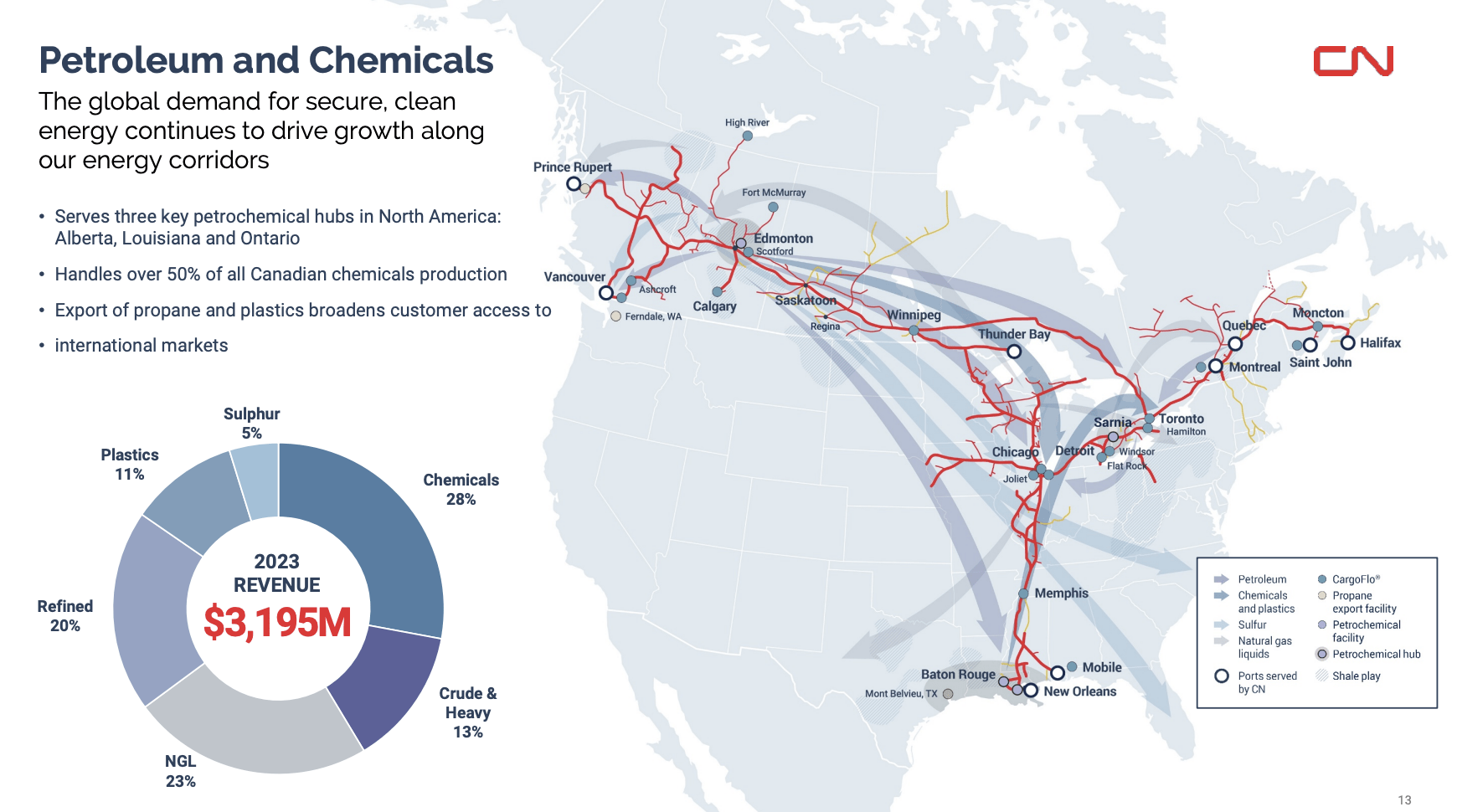

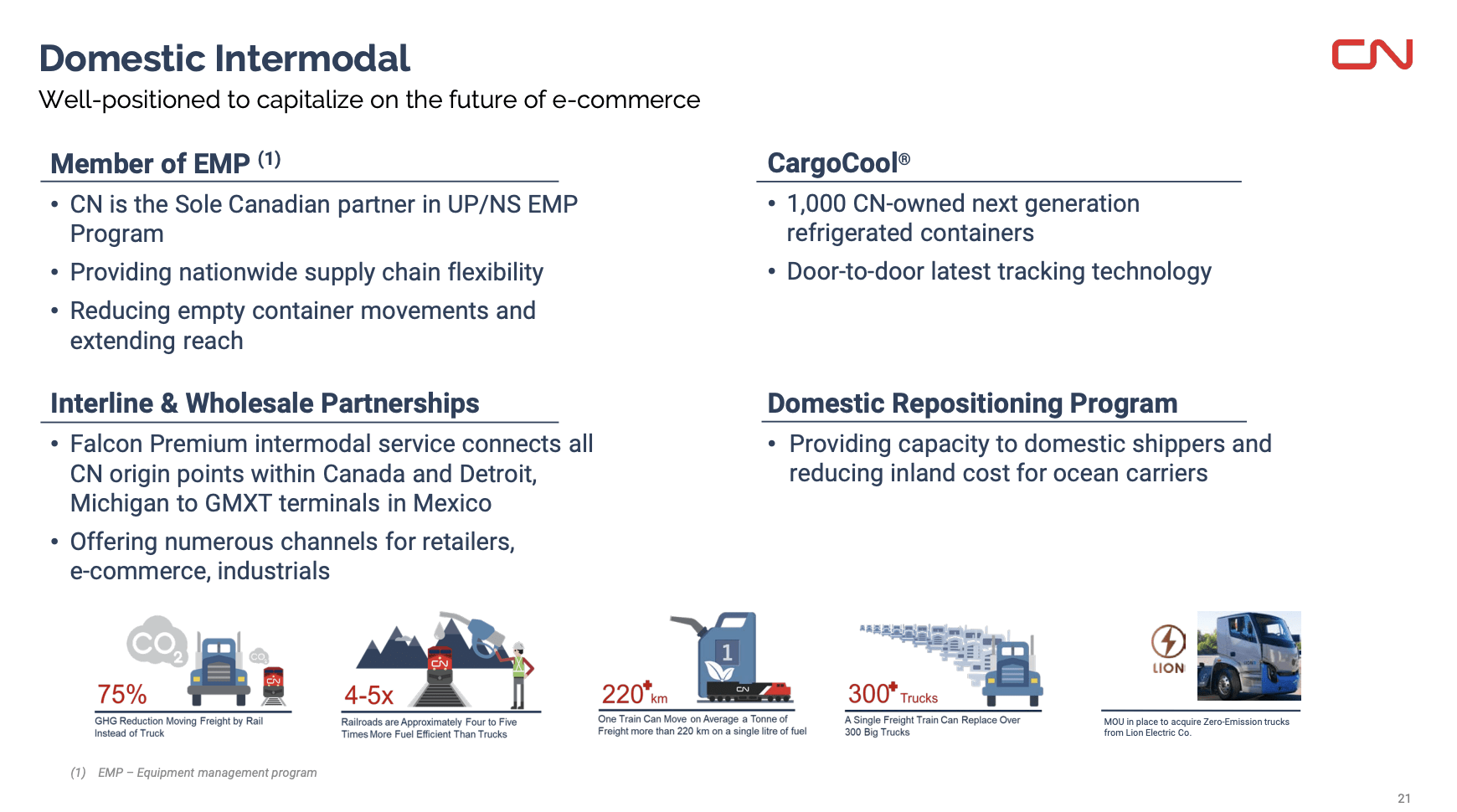

As we can see below, the company has one of the best networks in the industry, with a major footprint in domestic transportation, transborder trade, and domestic operations in the United States. This also includes a mix of high-margin goods like petroleum/chemicals, agriculture, metals, automotive, and coal - among others.

Canadian National Railway

For example, in its petroleum segment, the company handles more than half of Canada's chemical production. It also services the nation's massive energy market, shipping petroleum products to major export markets on the West Coast and Gulf Coast.

Canadian National Railway

The company is also increasingly competitive in the lower-margin intermodal business, where it competes with trucks. In this segment, it has agreements with other railroads, including Union Pacific (UNP) and Norfolk Southern (NSC) to increase the reach of its goods. This includes Falcon Premium, which adds a connection to Mexico.

It also has a sustainability benefit, as one freight train can replace 300 trucks. Although trucks have a cost-benefit when economic growth is weak (truck rates drop when demand is poor), stronger economic environments give railroads a competitive edge over the trucking industry.

Canadian National Railway

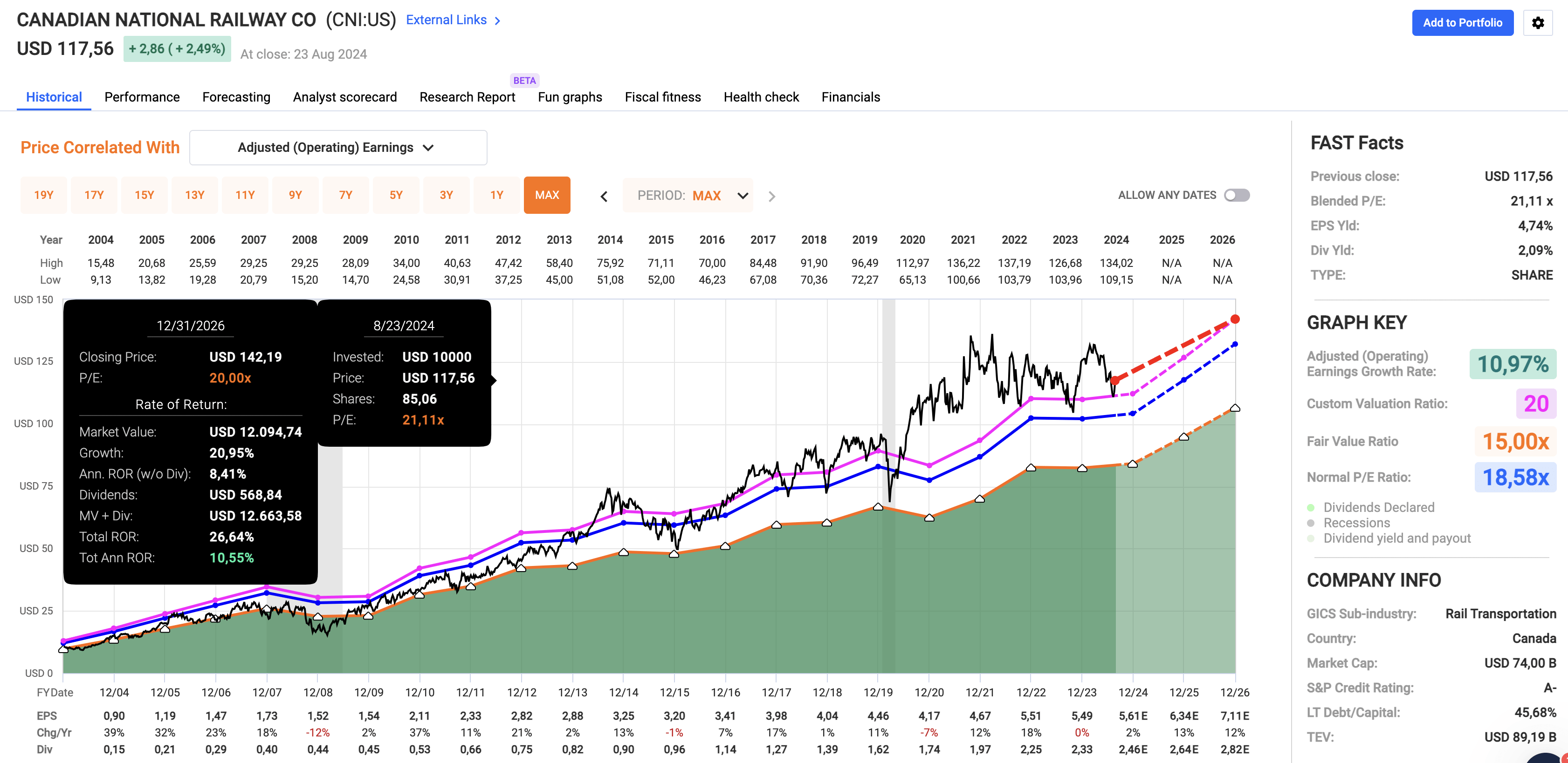

On top of that, the company has an A-rated balance sheet with leverage multiple close to 2x EBITDA and a track record that comes with an elevated return on invested capital ratio of roughly 15%.

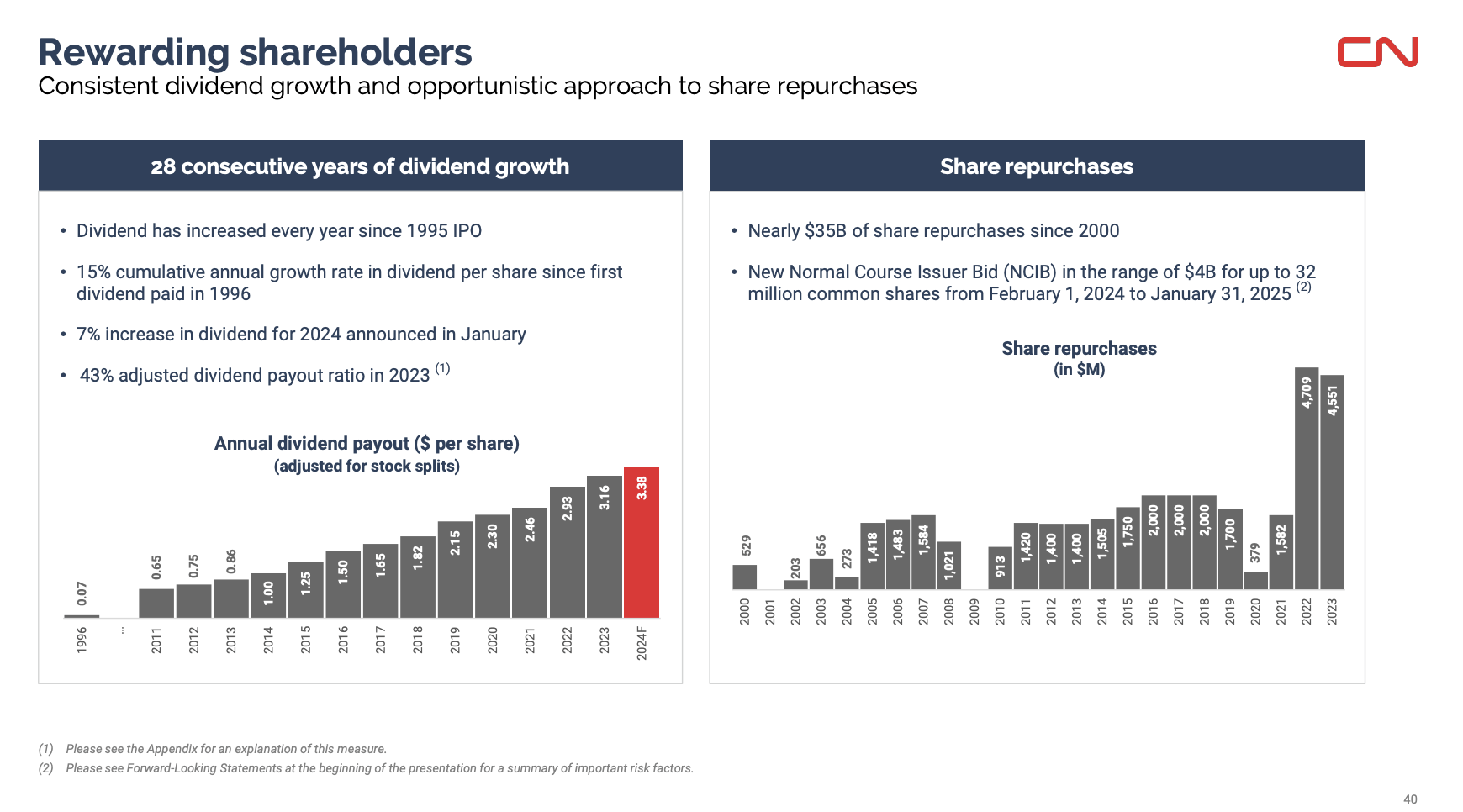

This has helped the company to reward shareholders. Since going public in 1995, the railroad has hiked its dividend every single year. Last year, it had a 43% payout ratio. Its current yield is 2.1% with a five-year CAGR of 10.0%.

Canadian National Railway

The company has also bought back 22% of its shares over the past ten years.

Since January 2004, New York-listed CNI shares have returned 13.3% per year.

Using the FactSet data in the FAST Graphs data below, currently trading at a blended P/E ratio of 21.1x, the company is expected to grow its EPS by 2% this year, which would be a great number in light of the weak manufacturing sector in North America. As we can see below, the leading ISM Manufacturing Index hints at a contraction in the industrial sector.

Data by YCharts

Data by YCharts

Next year, EPS is expected to rise by 13%, potentially followed by 12% growth in 2026.

FAST Graphs

Although I expect these numbers to be significantly higher if economic growth bottoms, the current implied annual return is 10-11% per year.

As such, I am convinced CNI (or Toronto-listed CNR) shares are a great investment for income and growth. While it's a cyclical company, it has helped many people retire, and I expect that to remain the case for younger generations.

Takeaway

When it comes to financial planning, there's no one-size-fits-all approach.

Our goals, income, jurisdictions, and even family dynamics play a huge role in shaping our retirement strategies.

Hence, It's key to assess our unique circumstances before making decisions.

With that said, for those behind on retirement savings, hope isn't lost!

By evaluating expenses, creating a solid plan, and making strategic investments, we can still work towards a comfortable retirement.

While some may benefit from the simplicity and stability of dividend ETFs like SCHD, others might find value in growth-oriented stocks like Texas Instruments or stable, long-term investments like Canadian National Railway.

Going forward, I will continue to focus on retirement issues, as it's one of the most important topics in the investment industry.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.