The Time Has Come

Summary

- U.S. equity markets rallied this week while benchmark interest rates tumbled to the lows of the year after Fed Chair Powell stated that the "time has come" to cut rates.

- The dovish pivot, underscored by an emphasis on "cooling labor markets," was further supported by data from the BLS showing that job growth has been far weaker than initially reported.

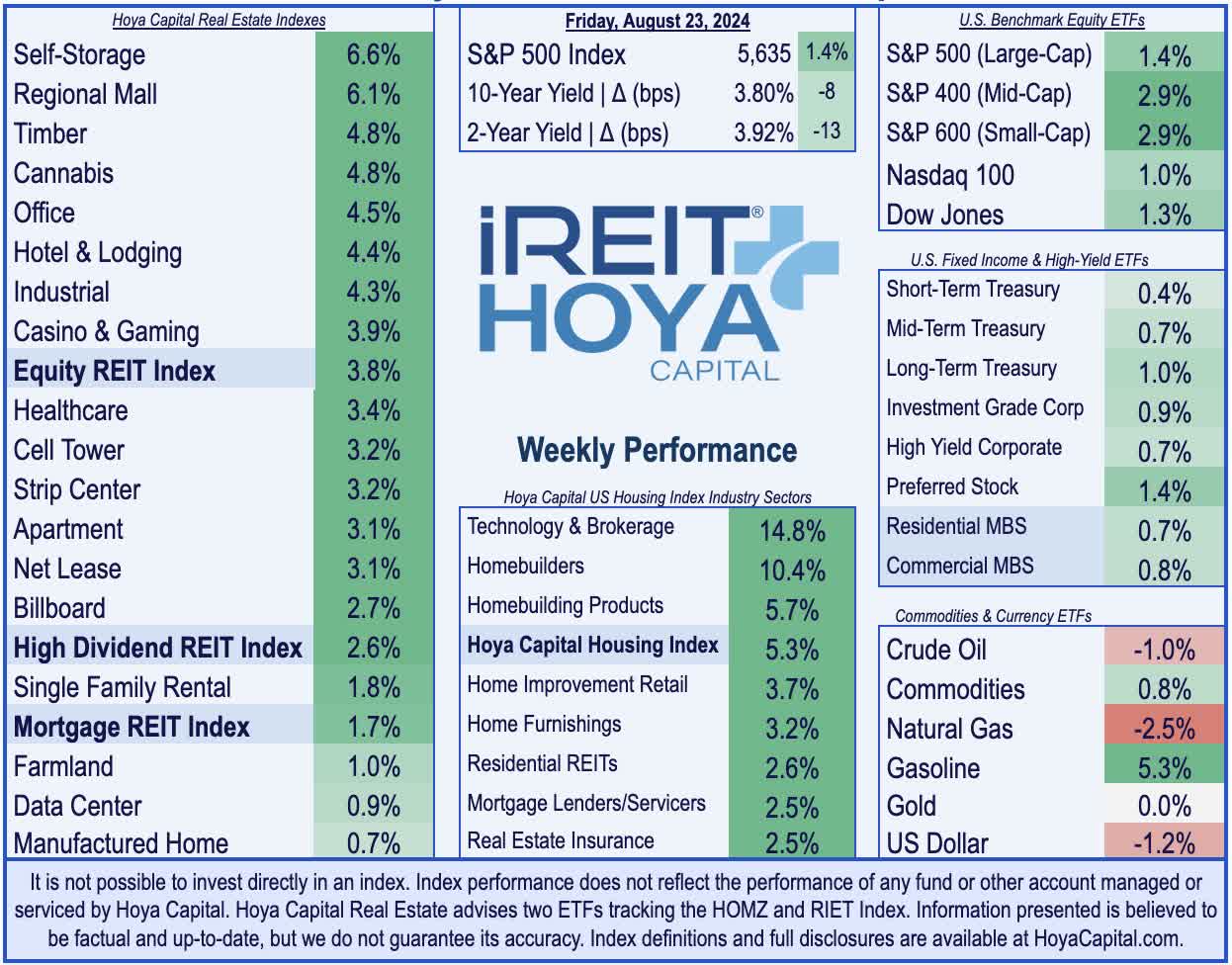

- The S&P 500 gained 1.4% this week, lifting the major benchmark to back within 0.5% of all-time record-highs. The Small-Cap 600 and Mid-Cap 400 each rallied nearly 3%.

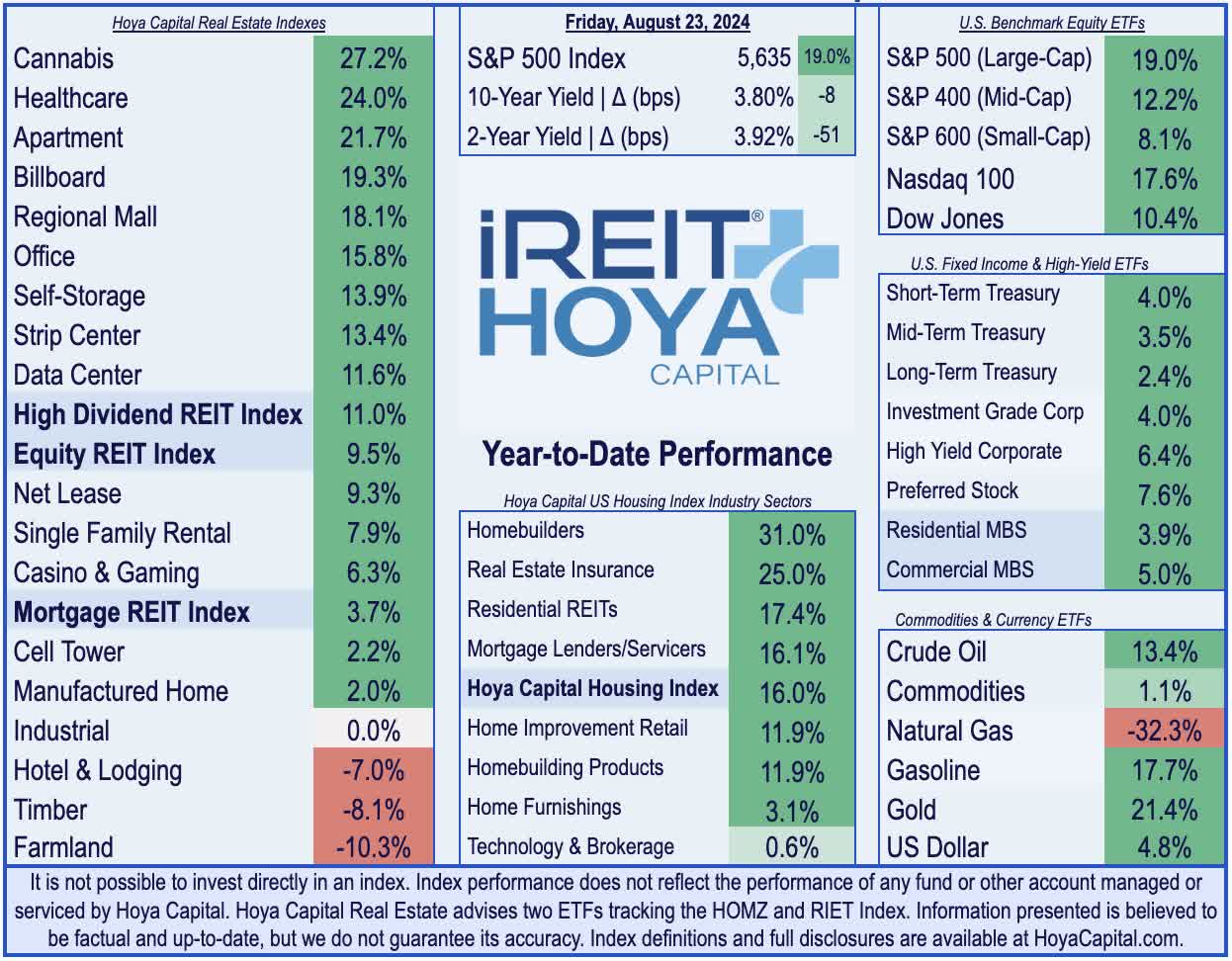

- Real estate equities - the most "Fed-sensitive" market segment and weakest-performing sector since March 2022 - ripped higher this week. The Equity REIT Index rallied 3.8% while Homebuilders soared 10%.

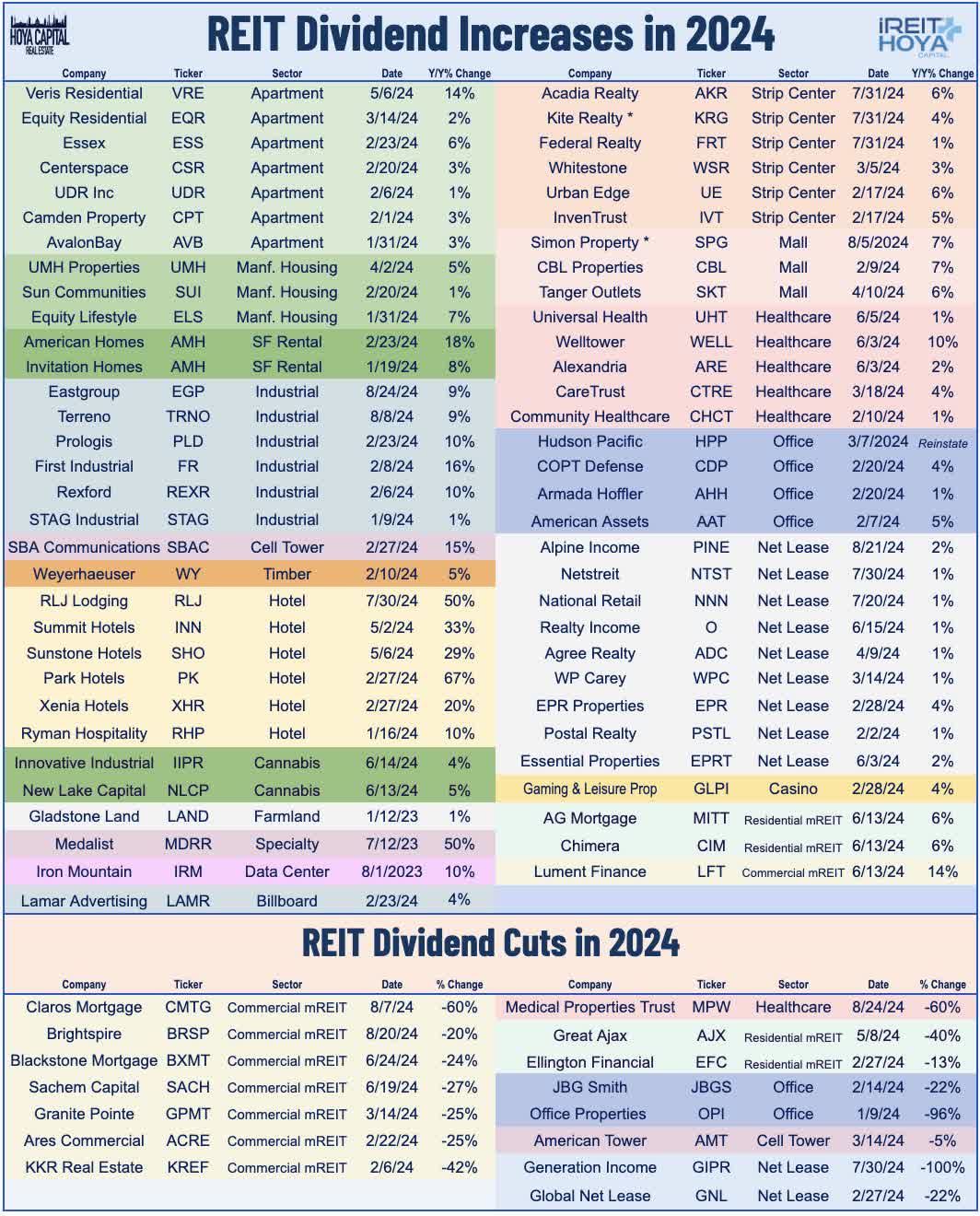

- It was also a relatively busy week of dividend news in the REIT space, with a pair of dividend increases - EastGroup and Alpine Income - along with one dividend reduction from Medical Properties. 61 REITs have raised their dividends this year, while 15 have reduced their payouts.

Matteo Colombo

Real Estate Weekly Outlook

U.S. equity markets rallied to the cusp of record-highs this week while benchmark interest rates tumbled to the lows of the year after Fed Chair Powell stated that the "time has come" to begin cutting interest rates following a historically aggressive rate hiking cycle to counter pandemic-era inflation. The dovish pivot - underscored by an emphasis on a "cooling labor market" - was further supported by revised data from the BLS showing that job growth from mid-2023 to early 2024 was significantly weaker than initially reported.

iREIT®+HOYA Capital

Posting gains for a third week following a three-week skid in late July, the S&P 500 gained 1.4% this week, lifting the major benchmark to back within 0.5% of all-time record-highs. Gains were broad-based this week and led by strength from smaller-cap companies, which had substantially underperformed their larger-cap peers since the start of the Fed's tightening cycle in March 2022. The Small-Cap 600 and Mid-Cap 400 each rallied nearly 3% on the week, outpacing the tech-heavy Nasdaq 100, which gained 1.0%. Real estate equities - the most "Fed-sensitive" market segment and weakest-performing sector since March 2022 - ripped higher this week as the long-awaited pivot towards easier monetary policy is finally on the horizon. The Equity REIT Index rallied 3.8% this week, with all 18 property sectors in positive territory, while the Mortgage REIT Index gained 1.7%. Homebuilders and the broader Housing Index surged as mortgage rates dipped to 15-month lows, setting the stage for a long-awaited home sales recovery.

iREIT®+HOYA Capital

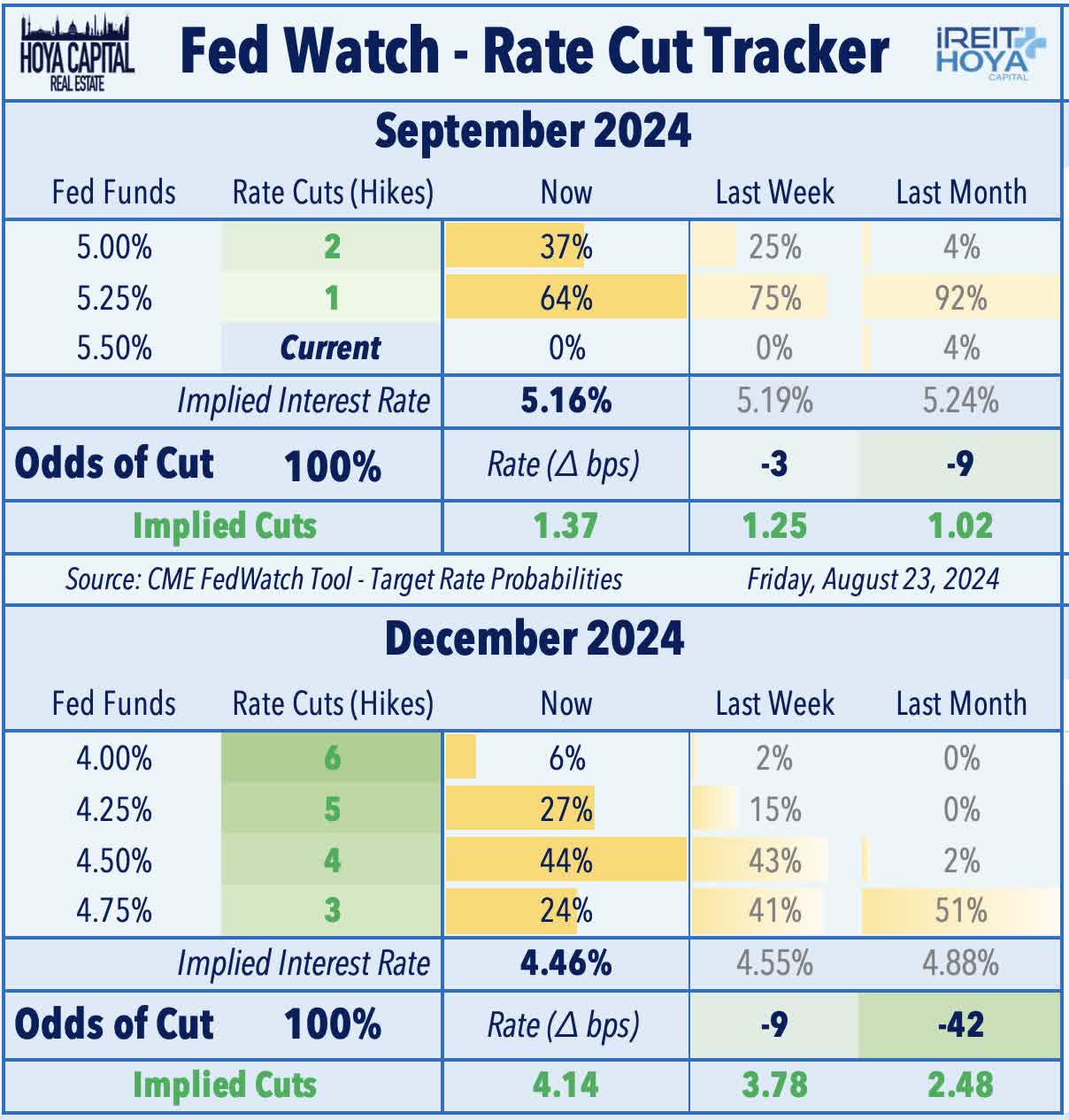

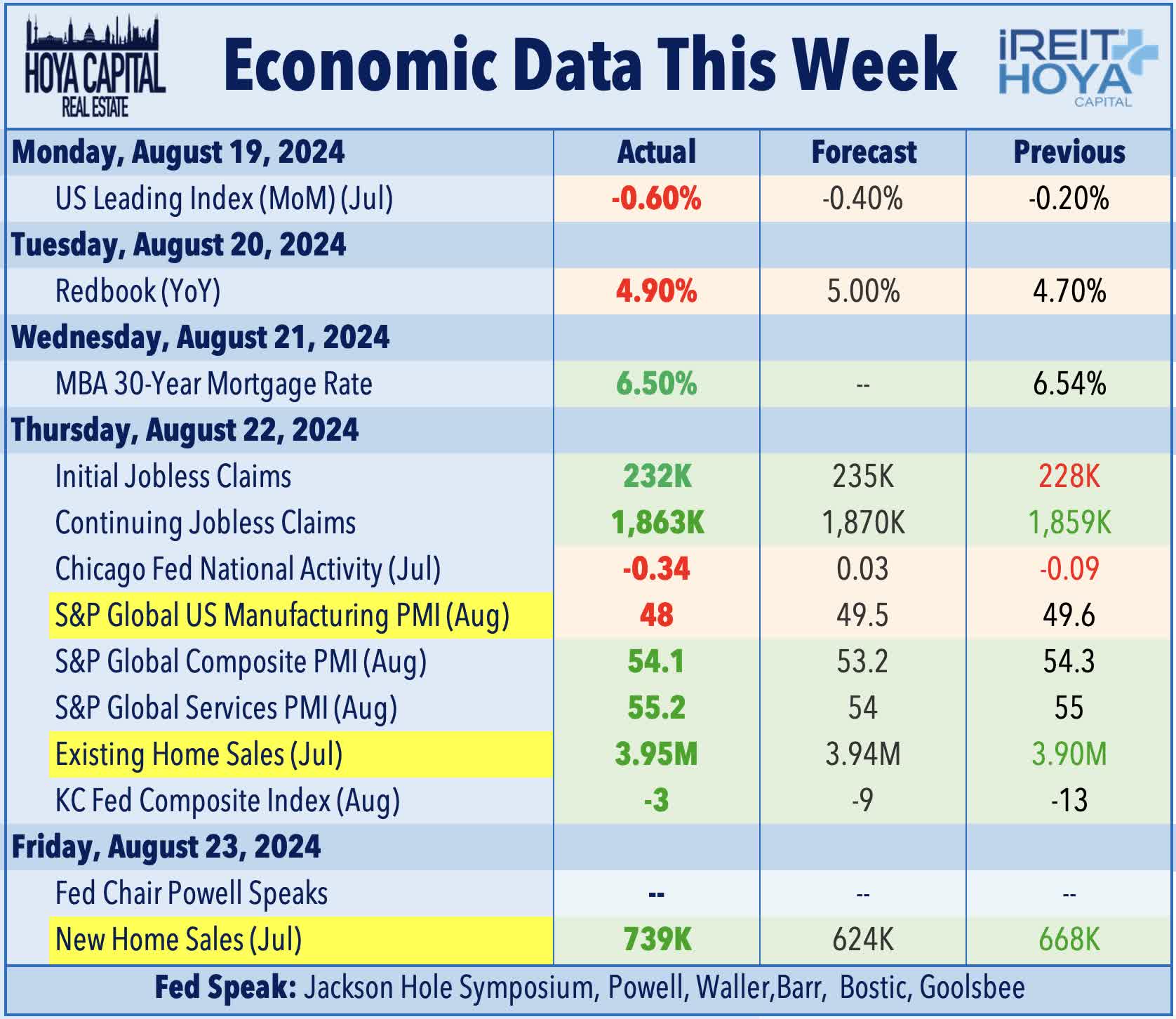

The Jackson Hole Symposium - the Federal Reserve's annual policy conference - was the focus this week with commentary from dozens of central bank officials. While there were a handful of notable "hawkish" remarks from several regional bank, traders interpreted comments from Fed Chair Powell as more "dovish" than anticipated, effectively confirming that rate cuts would begin next month. Prior to the conference, minutes from the July FOMC meeting released on Wednesday showed that several officials deliberated cutting rates at last month's meeting, but ultimately showed an emerging consensus to begin cutting rates in September. Bonds rallied across the yield and maturity curve this week as this relatively dovish "Fed Speak," combined with lukewarm economic data, suggested a more aggressive pace of cuts than previously thought. The 10-Year Treasury Yield dipped 8 basis point this week to close at 3.80% - barely above its 2024-lows seen in early-August of 3.78%. The policy-sensitive 2-Year Treasury Yield dipped 13 basis points to close at 3.92% - also narrowly above its early-August lows of 3.87%. Swaps markets now price-in 1.37 rate cuts in September (up from 1.25 last week) and 4.14 rate cuts by the end of the year (up from 3.78 implied last week). WTI Crude Oil fell another 1.0% this week to around $75/barrel, flirting with its lows of the year after climbing to nearly $90 in early April.

iREIT®+HOYA Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

iREIT®+HOYA Capital

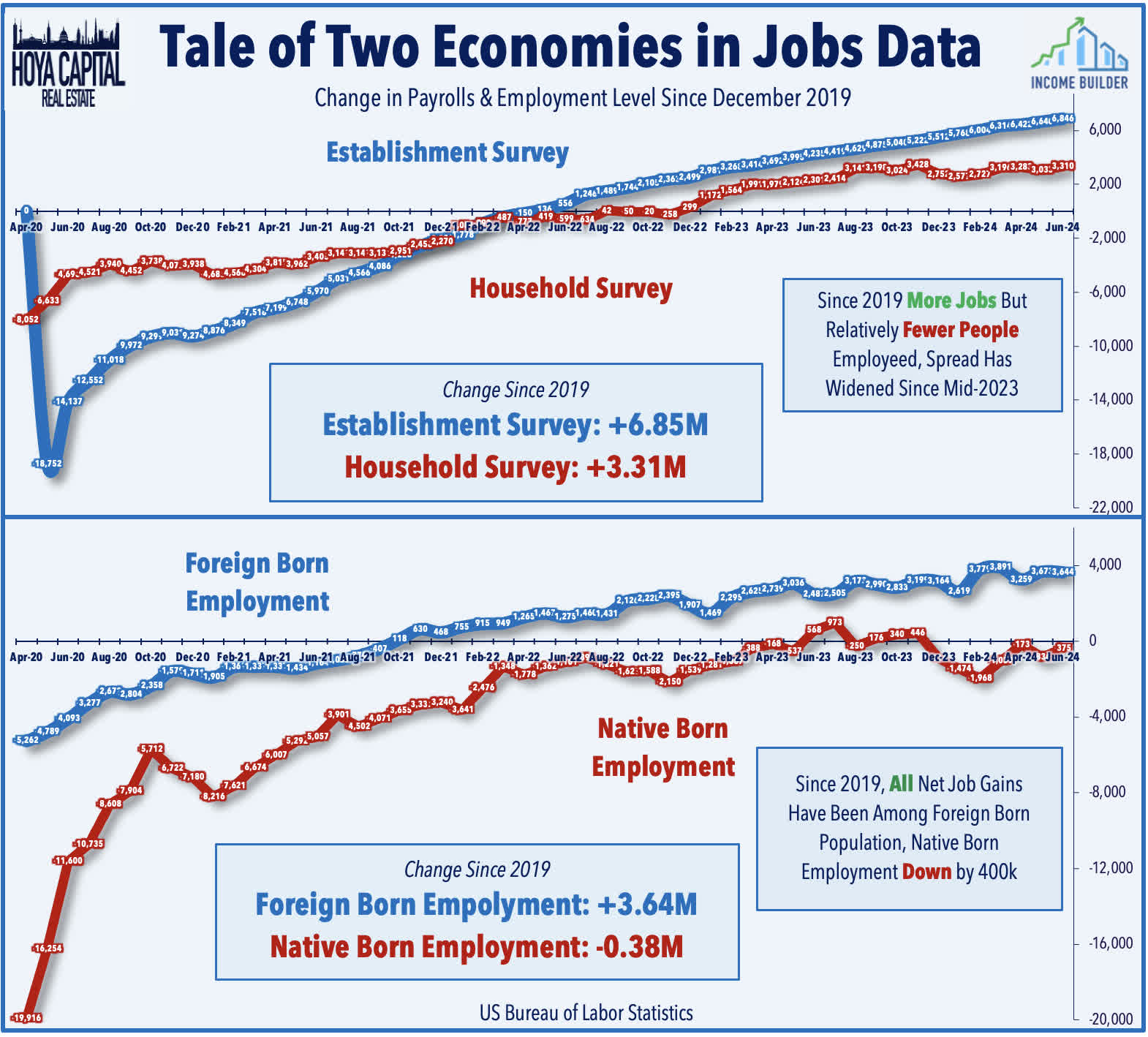

Behind the Curve? The Labor Department reported this week that the U.S. economy created 818k fewer jobs than originally reported during the 12-month period through March 2024, providing further support for multiple Federal Reserve rate cuts in the final three months of 2024. As part of its annual revisions to the nonfarm payroll numbers, the BLS reported that job growth was actually 30% less than initially reported. We've noted since mid-2023 that the BLS' Establishment Survey - which drives the "headline" job growth figures - had been showing far more upbeat (and questionable) hiring trends than the Household Survey. The revision to the total payroll level amounted to -0.5%, which was the largest revision since 2009. The revised numbers show that job growth actually averaged 174k during the period, considerably below the 242k that was initially reported. The biggest downward revision was seen in professional and business services (-358k less than initial estimates), leisure and hospitality (-150k), manufacturing (-115k), and trade/transportation (-104k). Government hiring and educational/healthcare were among the only categories that saw upward revisions.

iREIT®+HOYA Capital

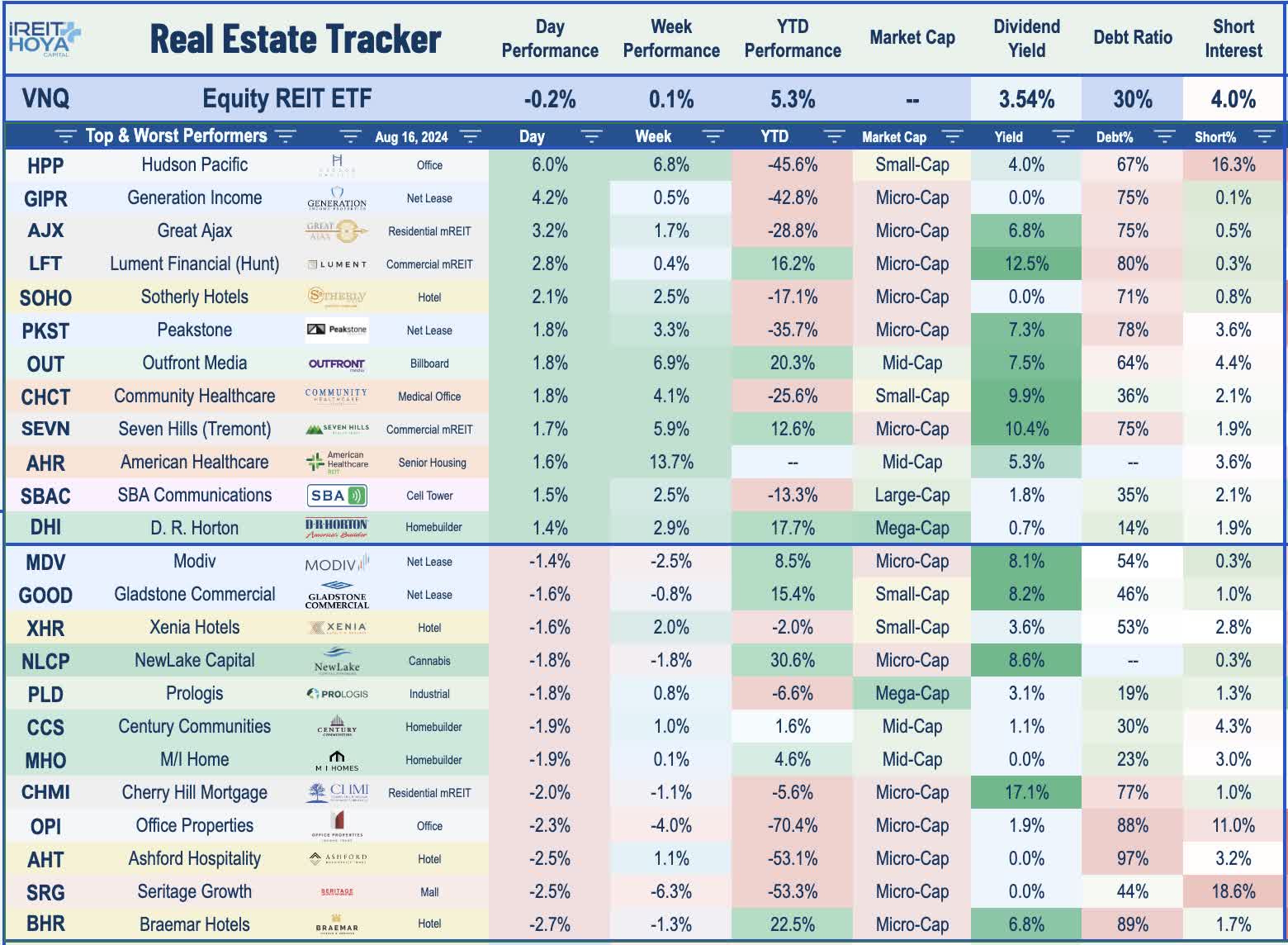

Equity REIT & Homebuilder Week In Review

Best & Worst Performance This Week Across the REIT Sector

iREIT®+HOYA Capital

Light at the End of the Tunnel? This week, we published Winners & Losers of REIT Earnings Season, which noted that two years of persistent rate-driven pressure on residential and commercial real estate markets appears to finally be abating, not a moment too soon. Amid an otherwise underwhelming earnings season across the broader equity market, real estate earnings results were notably better than expected, providing an added uplift to the rate-driven rebound. Of the 96 equity REITs that provide full-year FFO guidance, 57 (59%) raised their outlook, while 13 (14%) lowered - well above the historical second-quarter average "raise rate" of 40-45%. Upside surprises at the property-sector level included Retail, Sunbelt Apartment, NYC/Sunbelt Office, Senior Housing, and Industrial REITs. Ten REITs announced dividend increases this earnings season. There were few major "bombshells" this earnings season, but we did observe ongoing pockets of distress among some of the most highly levered REITs. Five REITs reduced their dividends. With recession fears ever-present, REITs are not entirely out of the woods yet. Losers included Self-Storage, Hotel, Farmland, and Mortgage REITs. The West Coast - particularly California - was a region of notable weakness. External growth has been limited, but there are signs that animal spirits are starting to come alive.

iREIT®+HOYA Capital

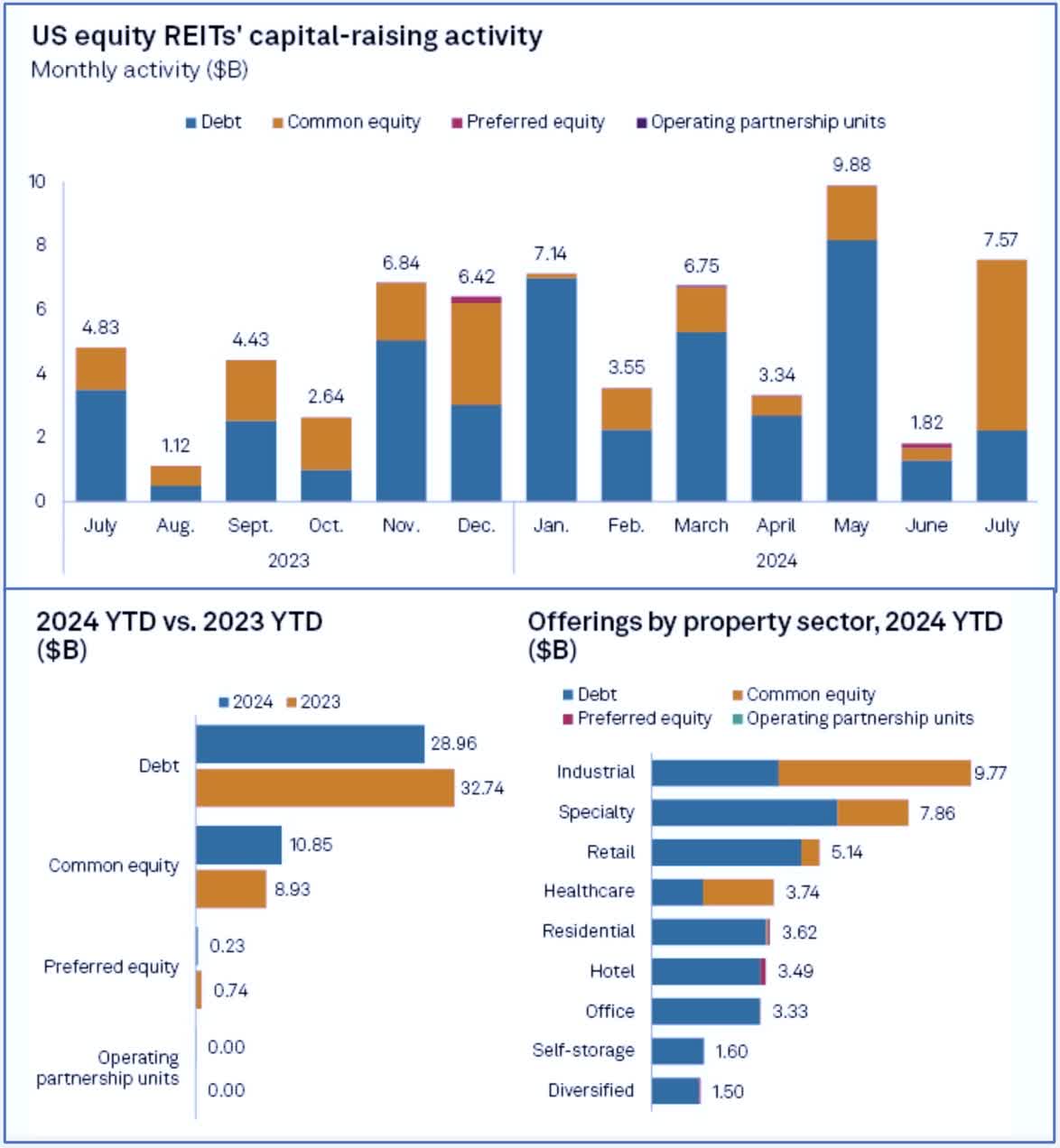

Speaking of animal spirits, S&P reported this week that capital raising activity among U.S. REITs accelerated significantly over the past three months following a sluggish start to 2024. REITs raised $7.6B in new capital in July - a solid rebound after a slow month of June and up 57% from July 2023. The offerings in July brought the year-to-date total to $40.0 billion, down 5.6% from the first seven months of 2023. Debt offerings have accounted for roughly 70% of the total haul this year, above the long-term historical average of around 60%. REITs remained very active over the past week: Realty Income (O) - the largest net lease REIT - raised $500M of 30-year senior unsecured notes due 2054 at a 5.375% interest rate. West Coast-focused industrial REIT Rexford Industrial (REXR) raised $575M of three-year exchangeable senior notes due 2027 at a 4.375% in a private transaction. West Coast apartment REIT Essex Property (ESS) raised $200M of ten-year senior notes due 2034 at a 5.50% interest rate. Independence Realty (IRT) raised $150M through a pair of private placements: $75M of 5.32% unsecured notes due 2031 and $75M of 5.53% unsecured notes due 2034.

iREIT®+HOYA Capital

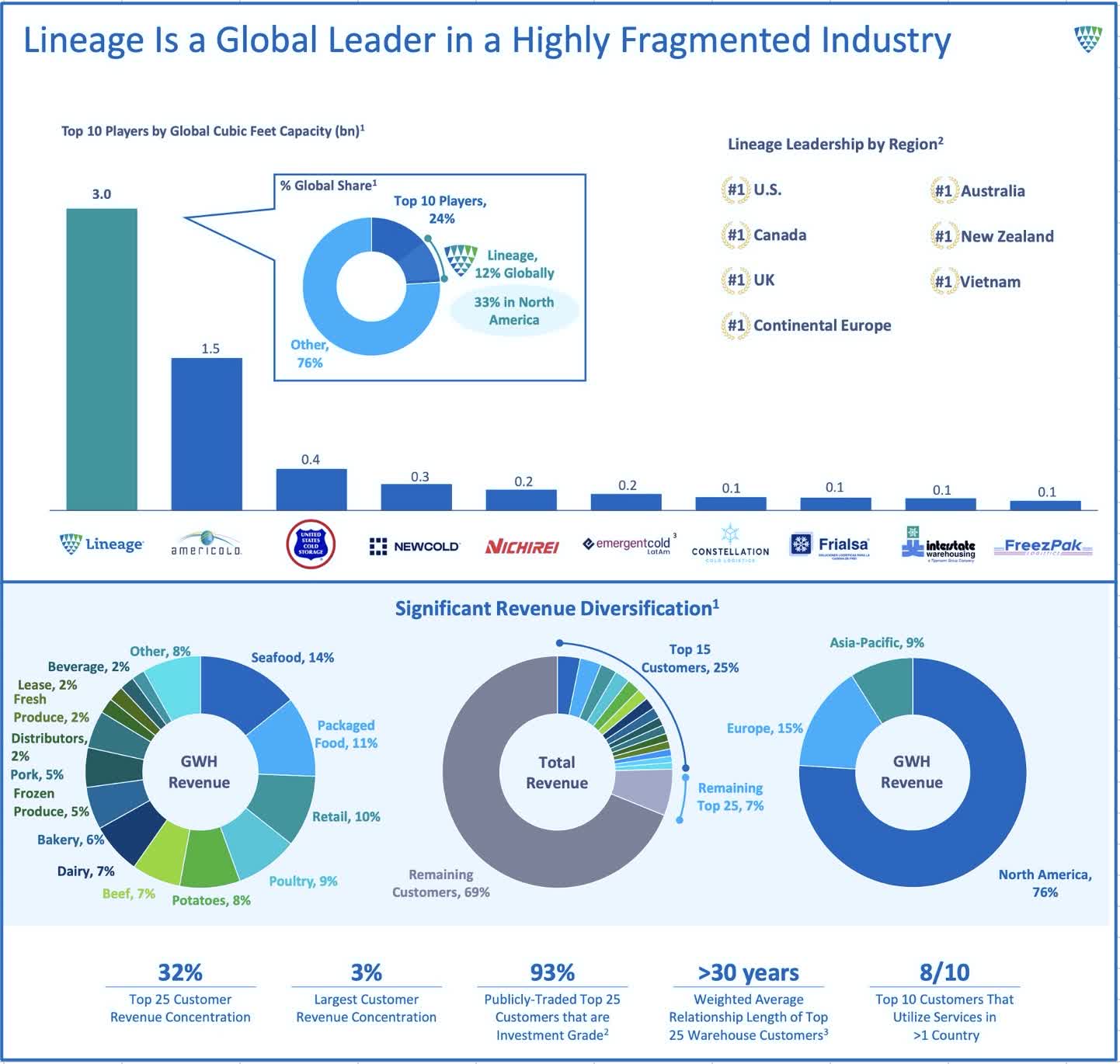

Industrial: On that note, Lineage (LINE) - the newest REIT following its IPO last month - was among the underperformers this week after filing its first quarterly report as a public company. LINE reported that comparable economic occupancy at its warehouses was 84.4% for the six months ended June 30, 2024, a decrease of 360 basis points compared to 88.0% for the six months ended June 30, 2023. By comparison, its peer Americold (COLD) reported earlier this month that its economic occupancy was 78.8% for the six-month period, down 540 basis points from the prior year. For the first six months of 2024, LINE reported Core FFO of $1.75/share, down about 16% from the $2.09/share reported in the first six months of 2023. Americold, by comparison, reported that its adjusted FFO increased 30% during the first six month of 2024 compared to the prior period. Lineage owns a network of roughly 480 facilities totaling over 84.1 million square feet and 3.0 billion cubic feet of capacity across countries in North America, Europe, and Asia-Pacific. LINE received "Buy/Outperform" ratings from ten Wall Street research firms this week, including Goldman Sachs ($105 price target), Piper Sandler ($102), Truist Securities ($100), BofA ($100), Morgan Stanley ($100), Scotiabank ($95), RBC ($94), JPM ($93), KeyBanc ($92), and Baird ($91). Five banks issued "Hold/Neutral" ratings, including Deutsche Bank ($90), UBS ($88), Evercore ($88), Wells Fargo ($86), and Mizuho ($86).

iREIT®+HOYA Capital

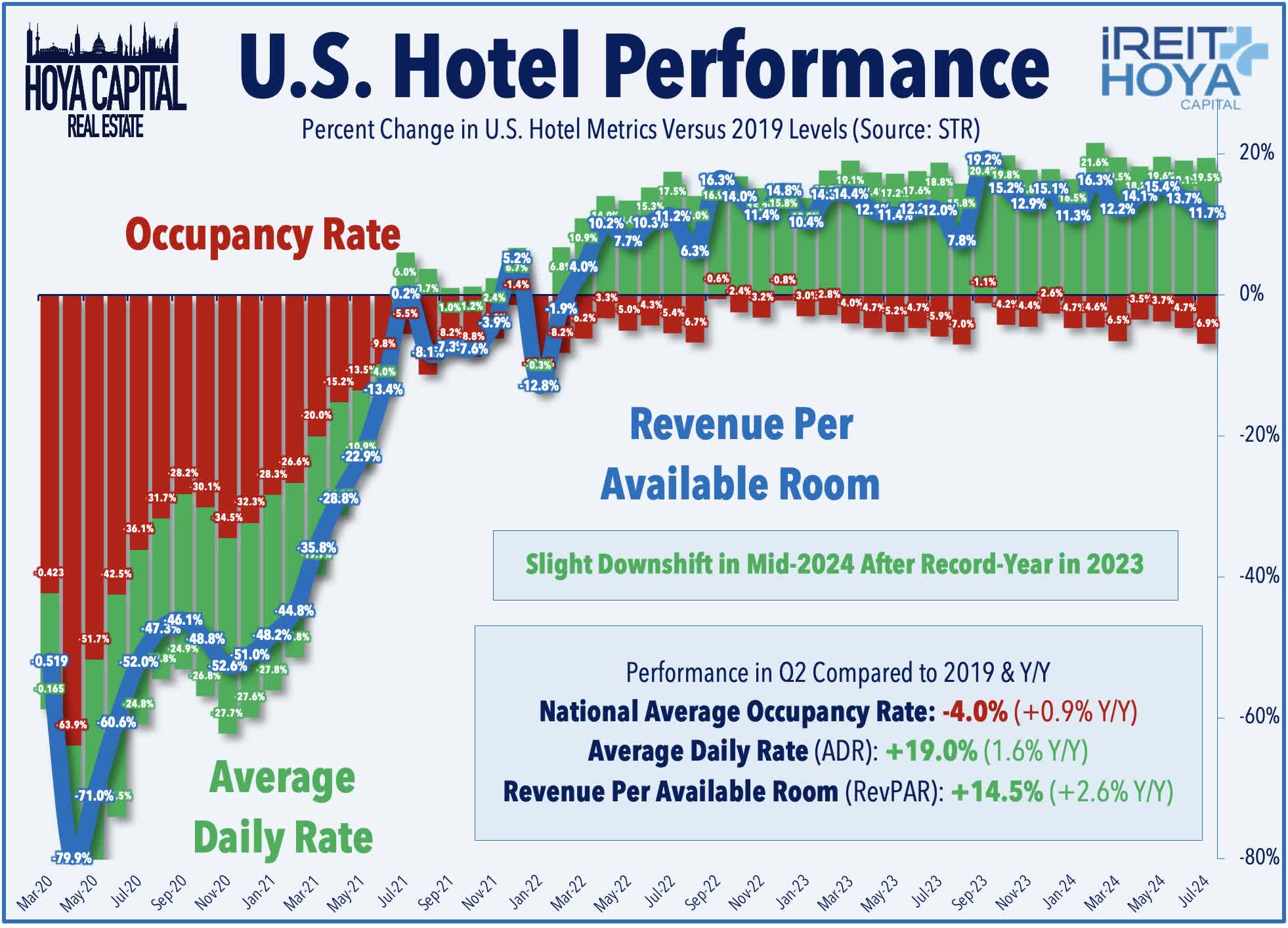

Hotel: Pebblebrook (PEB) rallied 4% this week after it announced an update on recent operating trends showing a slight acceleration in demand in August following a slow month of July. PEB noted that it expects July is expected to be the softest month for RevPAR growth in Q3, and reaffirmed its full-year outlook for each of its metrics. For PEB, a continued rebound in business travel helped to offset weaker pricing power in its leisure segment. PEB noted that urban weekday occupancy - a proxy for business demand - climbed by 3.7% year-over-year. Its leisure-focused resort segment reported a more-modest 1.9% y/y increase in occupancy, while Average Daily Rates ("ADR") for these resorts dipped 5.3% due "primarily to demand shifts in the leisure transient segment and continued value shopping by some leisure travelers." Hotel REITs were among the "losers" of REIT earnings season, as ten of the eleven hotel REITs lowered their full-year RevPAR outlook, while four REITs lowered the full-year FFO outlook. Hotel data provider STR reported that industry-wide Revenue Per Available Room ("RevPAR") was lower by -0.5% on a year-over-year basis in July, continuing a trend of moderation in recent months after a strong start to 2024. TSA Checkpoint data shows that domestic throughput cooled to around 4% above 2019-levels in July - the softest month since mid-2023 - but has rebounded thus far in August to roughly 6% above 2019-levels.

iREIT®+HOYA Capital

It was also a relatively busy week of dividend news in the REIT space, with a pair of dividend increases and one dividend reduction. Industrial REIT EastGroup Properties (EGP) - which we own in the Dividend Growth Portfolio - rallied 4% after raising its quarterly dividend by 10% to $1.40/share (3.0% dividend yield). Small-cap net lease REIT Alpine Income (PINE) rallied 5% this week after it raised its quarterly dividend by 2% to $0.275/share (6.5% dividend yield). On the downside this week, embattled hospital owner Medical Properties (MPW) slid 8% after it confirmed its previously-announced dividend cut to $0.08/share, a 47% reduction from its prior quarterly dividend of $0.15, and down from the $0.30 rate in 2022. With the dividend adjustments, we've now seen 61 REITs raise their dividend in 2024, while 15 REITs have announced dividend reduction. As we'll discuss in our State of the REIT Nation report next week, the average REIT dividend payout ratio was 69% in the second quarter - an improvement from the 78% in the first quarter and well below the historical average dividend payout ratio of around 80%.

iREIT®+HOYA Capital

2024 Performance Recap

Performance trends have shifted dramatically over the past month, as the long-underperforming real estate sector has closed some of the historically wide gap with other segments of the equity market amid a sharp pull-back in benchmark interest rates. Nearing the end of August, the Equity REIT Index is now higher by 9.5% this year, while the Mortgage REIT Index is higher by 3.7%. This compares with the 19.0% gain on the S&P 500, the 12.2% gain for the Mid-Cap 400, and the 8.1% gain for the Small-Cap 600. Within the REIT sector, 15 of the 18 property sectors are higher for the year, led by Healthcare, Residential, and Retail REITs - while Timber, Farmland, and Hotel REITs have lagged on the downside. At 3.80%, the 10-Year Treasury Yield is now lower by 8 basis points on the year, while the 2-Year Treasury Yield has dipped by 51 basis points to 3.92%. The aggregate Bloomberg US Bond Index is now higher by 3.6% this year. WTI Crude Oil is higher by 13.4% this year, while the broader Commodities complex is higher by just 1% on the year as higher oil prices have been offset by a dip in Natural Gas prices.

iREIT®+HOYA Capital

Economic Calendar In The Week Ahead

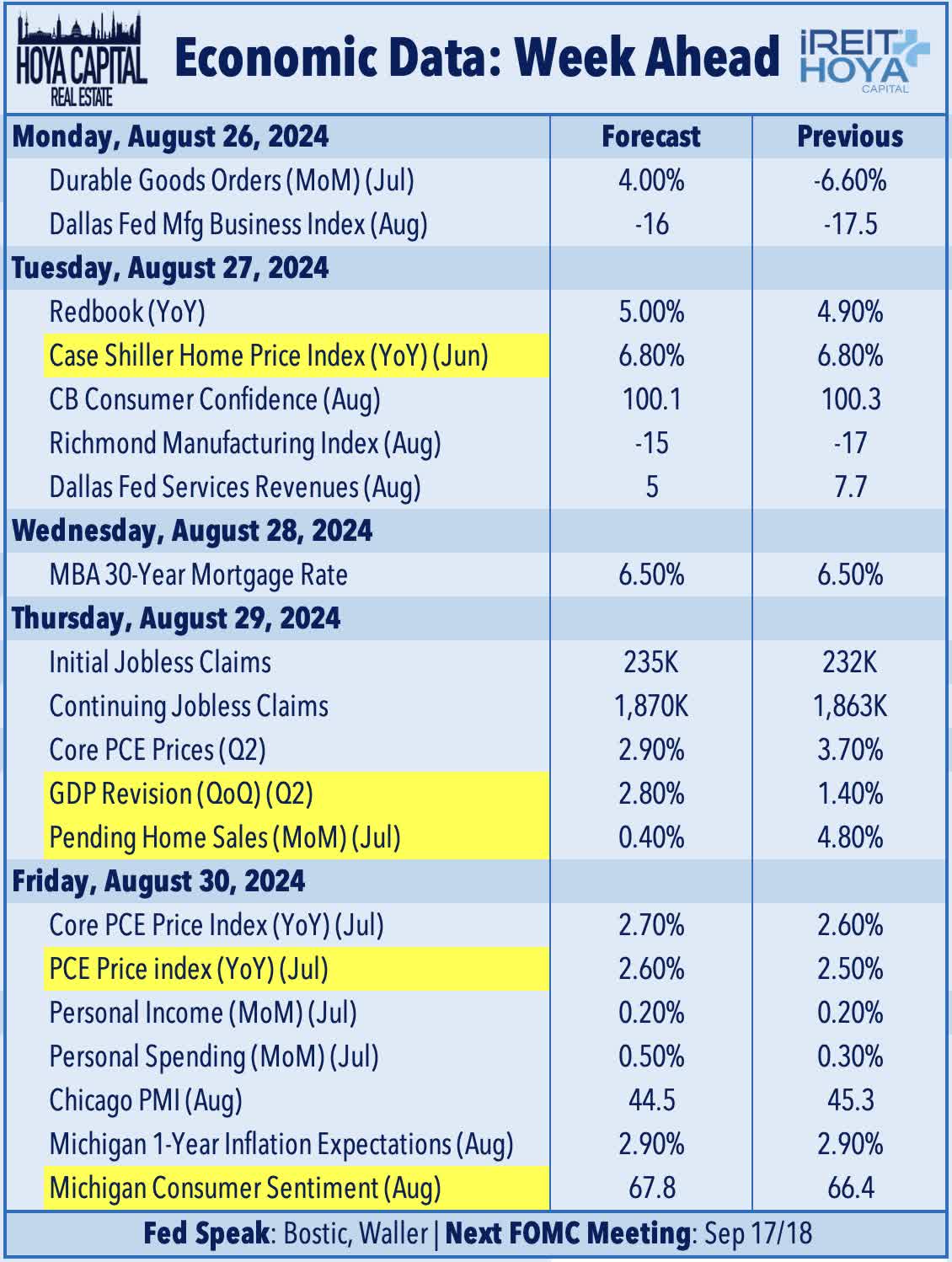

We'll see another relatively busy week of economic data in the week ahead, highlighted by the PCE Price Index report on Friday. The Fed's preferred gauge of inflation, Core PCE is expected to tick slightly higher to 2.6% in July - up from last month - but down from its peak of 5.6% and now within range of its stated 2% policy objective. On Thursday, we'll see the revised second-quarter Gross Domestic Product, which is expected to confirm real economic growth of 2.8% in the second quarter - unrevised from the initial report last month - which followed a disappointing 1.4% growth rate in the first quarter. Since Q1 2022 - corresponding to the start of the Fed's tightening cycle - real GDP has averaged 1.8% while the CPI Index has cooled from 6.3% to 3.4%. The Atlanta Fed's GDPNow forecast now estimates GDP growth of 2.0% in the third quarter, which is down from an initial estimate of around 3% in late July. We'll also see several additional housing market indicators, including Case Shiller Home Price Index on Tuesday alongside the FHFA's home price report, and we'll see Pending Home Sales data on Thursday. We'll also be watching weekly Jobless Claims data on Thursday, and Consumer Sentiment data from the Conference Board and the University of Michigan.

iREIT®+HOYA Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

iREIT®+HOYA Capital

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.