CCD: Caution Is Warranted As It Trades At A 25% NAV Premium

Summary

- Calamos Dynamic Convertible and Income Fund (CCD) achieved a 28.36% total return in the last year, outperforming the market's 25% return, despite an initial dip.

- The fund's long-term total return is 138.4% over 8 years, with a nearly flat price performance and a consistent 10% annual distribution yield.

- CCD trades at a 25% NAV premium, indicating high investor confidence but reducing the margin of safety and increasing risk if sentiment shifts.

- Convertible bonds' performance is tied to stock market trends; CCD's high yields are sustained by capital gains, posing risks in market downturns.

Marina_Skoropadskaya

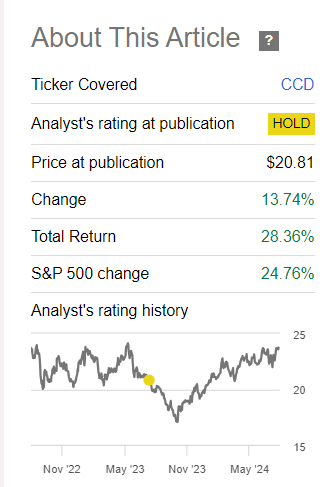

Calamos Dynamic Convertible and Income Fund (NASDAQ:CCD) is a high-yield fund that aims to generate income by investing in convertible corporate bonds. I covered this fund last year in an article titled CCD: Good Way To Generate Income If You Are Bullish On Growth Stocks, and it actually performed above my expectations by being up 28.36% in total returns since then despite an initial dip shortly after the article was published. The fund's total return even beat the overall market performance (SPY) which itself posted an impressive total return of almost 25% during the same period.

Recent Performance (Seeking Alpha)

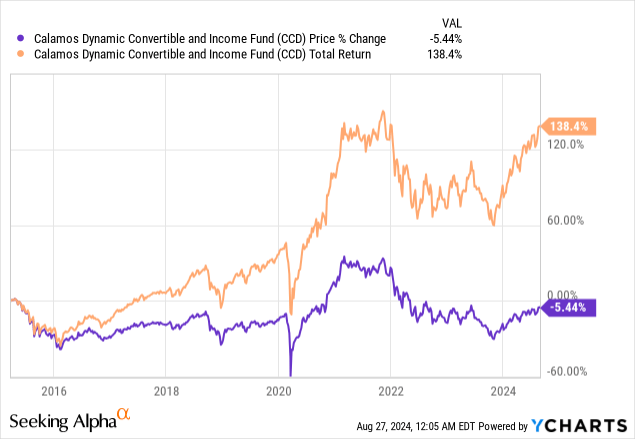

In the longer term, the fund resulted in total returns of 138.4% in the last 8 years while its price performance stayed more or less flat during the same period, being down about -5%. This is not bad for a CEF that supports an annual distribution yield of almost 10% since we've seen too many of similar CEFs lose more in NAV decay than what they pay in distributions, effectively taking money from investors' right pocket and putting it into their left pocket and charging them a fee for doing so. This fund has so far proved to be one of value creation, which we appreciate.

Data by YCharts

Data by YCharts

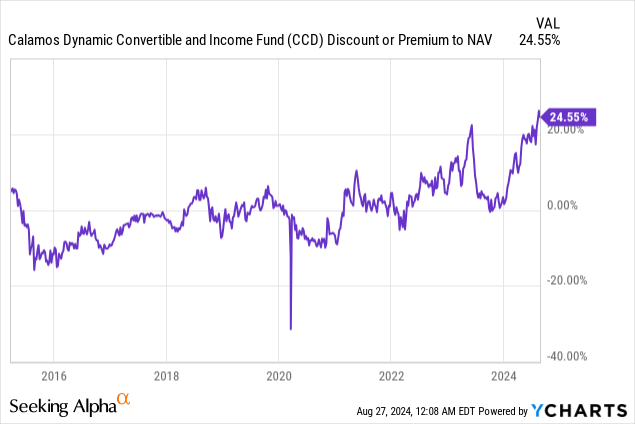

Having said that, there are some areas of concern which I must also mention. First and most important, the fund now trades at a NAV premium of almost 25% which is the highest it's ever been since the fund's inception. This means that for every $100 worth of assets the fund owns, investors are paying it a price of $125. This also explains some of the fund's outperformance in the last year, as its premium climbed significantly, accounting for much of the price increase we saw in the fund. Just because a fund is trading at a large premium against its NAV doesn't mean it will underperform or crash, either. Many times, investors will pay premium prices for funds which they consider to be of high quality. Many people are familiar with bond funds of Pimco that often trade at a premium, as well as Cornerstone funds that also allow people to reinvest their dividends at the NAV price, which allows investors to get a "discount" on their reinvestments. While a fund having a premium can show that investors have a lot of faith in its quality, it also reduces the margin of safety significantly. Investor sentiment tends to be fickle, and they can have a love and hate relationship with funds. If investors suddenly started trading this fund at a lower premium or even at NAV price, you might see your share price drop significantly. This is also true in the unlikely event where the fund might want to liquidate and close down because it means investors will get paid at the price of NAV, but this fund is not likely to close down anytime soon.

Data by YCharts

Data by YCharts

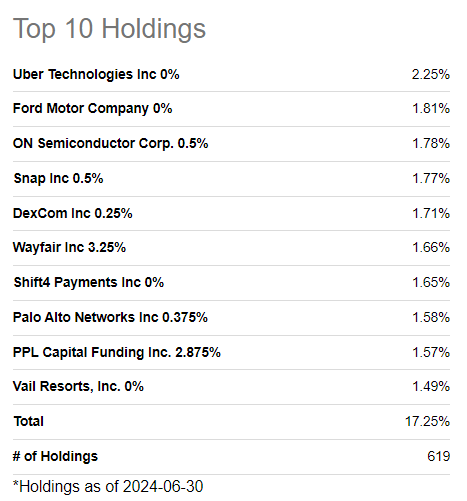

Secondly, equity prices themselves are also at a huge premium right now. The Nasdaq index is currently trading at a P/E of almost 35, which is the highest level it's been in the last 20 years. This introduces additional risk for this fund. Those of you that aren't familiar with this fund might be scratching your heads, wondering what tech stock valuations have to do with performance of a bond fund. Well, convertible bonds have more to do with stock prices than they have to do with the bond market. Convertible bonds are a special kind of corporate bond that are due to convert to stocks at a certain level. Since they can claim most of the upside in stocks while claiming almost none of the risks associated with the stock (by design), they tend to have a much lower yield as compared to other corporate bonds, sometimes as little as 0%. Corporations love these bonds because it allows them to issue debt at very cheap prices (in terms of interest rate) but it could also mean that their stock will get diluted if those bonds get converted to shares. When we look at CCD's top holdings, we see several bonds that yield either nothing or next to nothing, such as 0% yielding bonds from Uber (UBER), Ford (F) and 0.5% yielding bonds from Snap (SNAP).

Top 10 Holdings (Seeking Alpha)

When the stock price of these companies reaches a pre-agreed level, bonds convert into stocks and the owner of these convertible bonds enjoy all upside in stock price, so these convertible bonds act almost like a warrant or a call option. Meanwhile, if the company's stock price crashes, convertible bonds don't crash with them because bonds are still guaranteed by the company and their principal is still fully protected. The biggest risk for convertible bondholders (apart from a company going completely bankrupt) is that they end up holding bonds that yield 0% and miss out on gains.

This is why when the overall market is in a bull run, convertible bonds tend to perform very well as we saw them do in the last year and half, but when the stock market's performance falters, these bonds and bond funds also perform poorly. Still, if you have market where stocks are rising 25% per year, convertible bond funds could also rise by about 25% so you get to participate in almost all of the upside but when the market crashes -25% in a year, convertible bonds will probably only drop by 10% or so which means you are not participating in all downside while participating in most upside, but this comes with the territory of accepting near 0% yields.

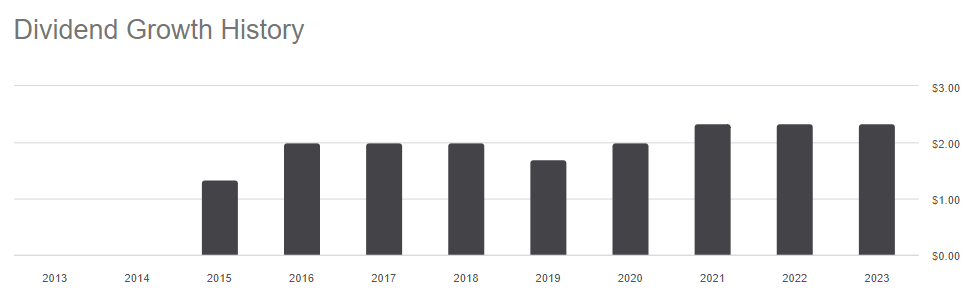

The fund currently pays a distribution of 9.8% which is within the ballpark of its typical yield of 10% which can go to as high as 12% when the fund is not trading at a NAV premium. You may be wondering how the fund can afford to pay such high yields while only collecting near 0% yields from its convertible bonds, and the answer is that it comes from capital gains. The fund pays about 10-12% of its NAV every year, regardless of whether it posts a profit or not during the year. This will probably work out fine and will be fully covered during a bull market like the one we've been enjoying for the last 15 years or so but could result in significant NAV decay during turbulent times. This is why stock valuations are very important for this bond fund.

Distribution History (Seeking Alpha)

Long-term investors can keep their shares and keep collecting those rich distributions, but I would advise against adding any new shares when valuations are at the current levels in terms of both stocks trading at historically high multiples, as well as, the fund itself trading at a NAV premium of 25%. If we see a dip in stock prices or NAV premium of this fund, it may be a good opportunity for long-term investors to add more shares and increase their position side.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.