Powell's Jackson Hole Speech: Rate Cuts Due, But The Economy Looks Just Fine Too

Summary

- Fed Chair Powell essentially confirmed upcoming rate cuts at his speech at the Jackson Hole economic symposium earlier today, on decreased inflation risks and increased labor market risks.

- He also shed light on why the US economy has stayed strong despite tight monetary policy, pointing to higher labor supply and easing off of inflation distortions following the pandemic.

- With the extent of rate cuts likely data dependent, upcoming GDP, labor market and inflation reports will be key.

- All in all, his speech is positive on the economy and if the present macro trends continue could be good for the markets too.

Andrew Harnik

With no surprises in Fed Chair Jerome Powell's much awaited speech at the annual Jackson Hole economic symposium earlier today, the stock markets haven't responded much to it so far. The key indices of S&P 500 (SP500), Dow Jones Industrial Average (NYSEARCA:DIA) and NASDAQ-100 (NDX) are up between just 0.3-0.6% as I write.

The markets have priced in a rate cut in the Federal Open Markets Committee [FOMC] in September for some time now. Powell has all but confirmed that these are indeed underway.

But his speech does more than just that. It also offers insight into a key question on the US economy - how has the economy stayed in good health even as interest rates have been high? Or as Powell puts it "...why inflation rose to levels not seen in a generation, and why it has fallen so much while unemployment has remained low".

Rate cuts are coming

First, let's talk about the all important rate cuts. The speech is dotted with remarks on Powell's growing comfort with progress on inflation, even beyond what was expressed in the latest FOMC statement earlier this month.

While the FOMC statement said that "Inflation has eased over the past year but remains somewhat elevated.", Powell today said "Inflation has declined significantly" and further added later "The time has come for policy to adjust". The latter remark, in particular, gives a clear signal of the coming rate cuts, and it is further backed by the following statement, which makes it clear that the present economic scenario is compatible with lower inflation rates.

All told, labor market conditions are now less tight than just before the pandemic in 2019—a year when inflation ran below 2 percent. It seems unlikely that the labor market will be a source of elevated inflationary pressures anytime soon. We do not seek or welcome further cooling in labor market conditions.

Why the economy can still do fine

Next, the answer to the puzzle. In the present scenario of firm interest rates and falling inflation has been the continued buoyancy of the US economy and even the labor markets. After softening to below trend levels in the first quarter (Q1 2024), GDP growth bounced back with a 2.8% growth in Q2 2024. Further, even with the latest increase to 4.3%, the unemployment rate is below the long-term average of 5.69%.

Powell points to three reasons that help explain this phenomenon:

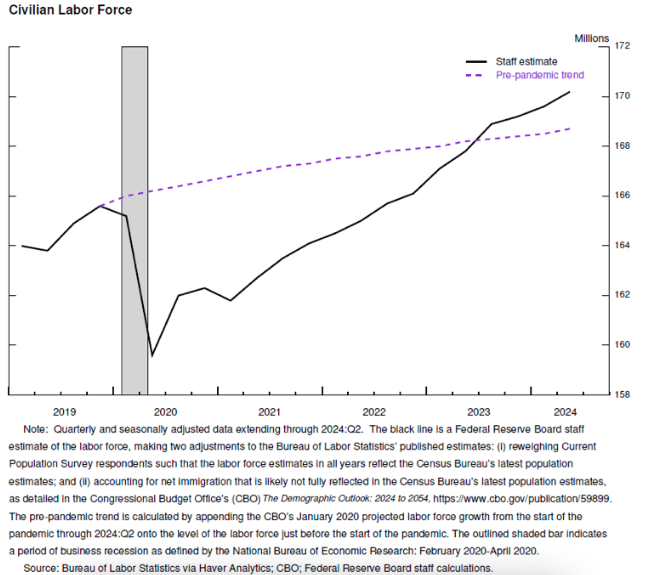

1. Higher labor supply: The unemployment rate rise, even if it's still below the historical average, is not due "to elevated layoffs, as in the case in an economic downturn", as Powell says, but because post-pandemic there has been a return to the labor force. As the chart below shows, if the pre-pandemic trend was to continue, the civilian labor force would have been smaller compared with the Fed's estimate of actual labor force.

Source: Federal Reserve

This is not to say that the pace of hiring hasn't slowed down. He points to a multiple jobs related data points like hiring and quit rates and nominal wage gains to point out that the labor market is now more relaxed. At the same time, it's worth noting that the "ratio of vacancies to unemployment has returned to its pre-pandemic range", even as it falls substantially below the highs of 2021 and 2022 (see chart below). In 2019, the US economy grew by 2.3%, which is essentially consistent with a trend growth rate. It can by extension also imply that the present labor market trends are consistent with the same as well.

The key point here, as I see it, is that the inching up of the unemployment rate is only partly explained by a softening in the job market. It also has to do with the rising numbers in the labor force.

Source: Federal Reserve

2. Pandemic driven distorted inflation trends: Powell also points out that COVID-19 related demand and supply distortions impacted inflation. On the demand side, pent-up consumer demand after the pandemic, the fiscal stimulus and increased savings led to a "historic surge in consumer spending on goods" he says.

While on the other hand, supply was constrained. The labor force was slow to return, and supply chains faced disruption in international trade channels. The commodity price shock from the Russia's war on Ukraine further exacerbated inflation.

There has been significant improvement, though. On the supply side, as the chart below shows, the pressure on supply chains is even below pre-pandemic levels now (for details on how the Global Supply Chain Pressure Index is calculated, click here). On the demand side, Powell points to the tight monetary policy as having played a role.

The crux of Powell's inflation discussion is that high inflation wasn't simply a case of an overheated economy, but also significant supply side constraints, which eased over time. And the combination of both demand and supply easing, inflation has now come-off to manageable levels.

Source: Federal Reserve

3. The role of inflation expectations: Finally, he points to the role of inflation expectations in the assumption that a "slack in the economy" was required to ensure that inflation comes back to a sustainable rate.

The Fed aims to "anchor" these expectations at 2%, which means that even if there are short-term fluctuations in inflation, the long-term expectations are still of the Fed's target rate. However, if these expectations are not anchored as was the case in recent years (see chart below), they can put further pressure on existing inflation. It's estimated that expectations of a percentage point increase in inflation, will also increase actual inflation by as much.

Clearly, though, the assumption didn't hold, as the chart below shows. Inflation expectations have now come off substantially in the past year, without the economy suffering as was feared.

Consumer Inflation Expectations (Source: Trading Economics)

What next?

In a nutshell, Powell's speech is rather encouraging. Not only does it point to a softening in interest rates very soon, it also indicates that there's limited concern on the health of the economy. The questions now is how much can rates be cut by. While the predominant expectation is of a 25 basis points [bps] reduction, there's also expectation of a 50 bps cut.

In line with Powell's mention of incoming data as one of the factors, along with outlook and evolving risks, in determining the "timing and pace of the rate cuts", it's then key to look out for the big data points to forecast the extent of rate cut likely. These include the release of the second revision to Q2 2024 GDP and PCE inflation data later this month and the August labor market report CPI report earlier in September, before the Fed meeting on September 17-18.

From the investing perspective, the speech to my mind, encourages optimism. As a result, barring any unexpected surprises to the numbers, there could even be better times ahead for the stock markets, as a recent study points out. For more risk averse investors, however, there are still options as I've pointed out here and here.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.