Hokkaido Electric Power Company: Tomari Nuclear Power Restart Is A Strong Tailwind

Summary

- Hokkaido Electric Power Company is poised for growth with the potential restart of the Tomari Nuclear Power Station, which could significantly boost its energy output and financial performance.

- HEPCO is currently undervalued compared to its peers, with lower valuation multiples despite stable revenue growth and profitability.

- Key risks include public opposition to nuclear energy in Japan and the dependence on the Tomari restart for future growth.

Richard Drury

My view is that investing in international stocks can uncover lucrative mispricing opportunities for U.S. investors. If we agree that markets fall in line with the efficient market hypothesis ("EMH"), then smaller or more obscure markets overseas may be less efficient, and thus have a great number of growth prospects that have been overlooked by the broader market. It can be difficult to find information on stocks located in non-English-speaking countries too, as access to news articles, analyst opinions, and market information rests behind a walled garden of language and cultural barriers. If relevant stock information is harder to come by from smaller and more opaque markets, it could then be argued that researching and investing in foreign stocks can potentially lead to market-beating returns due to this information asymmetry.

Japan has caught my attention as a market that’s relatively untapped by U.S. investors. I have a particular interest in the country’s persistent energy shortage, as its large number of older power plants are coming near the end of their life cycles and are being replaced, leading to lucrative opportunities in the sector for companies stepping in to fix the shortage.

I feel that one such opportunity can be found with Hokkaido Electric Power Company, (OTCPK:HKEPF) which is a major electric utility company headquartered in Sapporo, Japan. As a part of my thesis, the company is seeking approval to restart its Tomari Nuclear Power Station, which has been dormant since the Fukushima Daiichi nuclear disaster in March 2011. The restart of Tomari coincides with a rapid change in Japan's energy needs, with management guiding that new industries are spurring demand. Final approvals and safety checks for the restart of its plant should be completed by October this year.

Overall, I think that HKEPF is a buy, and I also believe that it is presently undervalued, as I will unveil later in the article.

Company Overview

Hokkaido Electric Power Co ("HEPCO") is one of the largest companies in Hokkaido, the second-biggest island in Japan. It was founded in 1951 and is a key player in the generation and distribution of energy. The company operates via an energy portfolio consisting of thermal, hydroelectric, and renewable sources. The company is also exploring phased investment of hydrogen and ammonia to help it reach its decarbonization goals.

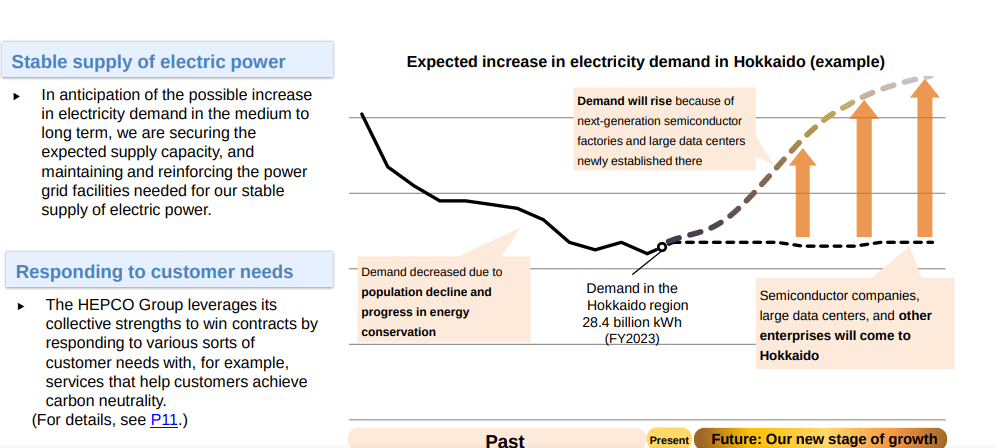

Although Hokkaido has faced a steep population decline from lower birth rates and lack of immigration, which has reduced the demand for energy, management expects that industries such as semiconductor factories and data centers will find a presence in Hokkaido and increase demand for its electricity.

HEPCO annual report

I believe that a large part of HEPCO's optimism comes from the Rapidus venture, which is government-backed and intends on accelerating Japan's semiconductor production facilities. As part of this effort, a new semiconductor plant is due to be operational by April next year, and will be the region's largest development project to date.

Another development in the vein of data centers is a joint project by Softbank and IDC Frontier in Tomakomai City, Hokkaido. This site is set to become Japan's largest data center in the country, "with a total power receiving capacity of 50 megawatts."

All of these developments are guided by the hand of the Japanese government and central bank, which ended its eight-year period of negative interest rates in April this year. But with the yen still being cheap, it makes completing these development projects very feasible, and its weak currency means it could have a competitive advantage in the export space as well. HEPCO then benefits from these tailwinds, and I expect a continued focus will be put on Hokkaido as a high-tech manufacturing and data center hub for Japan due to HEPCO and its peers providing a plentiful energy source.

Operating Segments and Future Energy Projections

HEPCO operates in three operating segments, as per its financial results for FY2024. These include the Hokkaido Electric Power Network, the Hokkaido Electric Power Company, and Other businesses.

Its main operating segment is naturally responsible for the supply of electricity. Broken down further, this encompasses HEPCO's operation of its various power plants, both thermal and renewable, and ensuring a stable electricity supply for its customers.

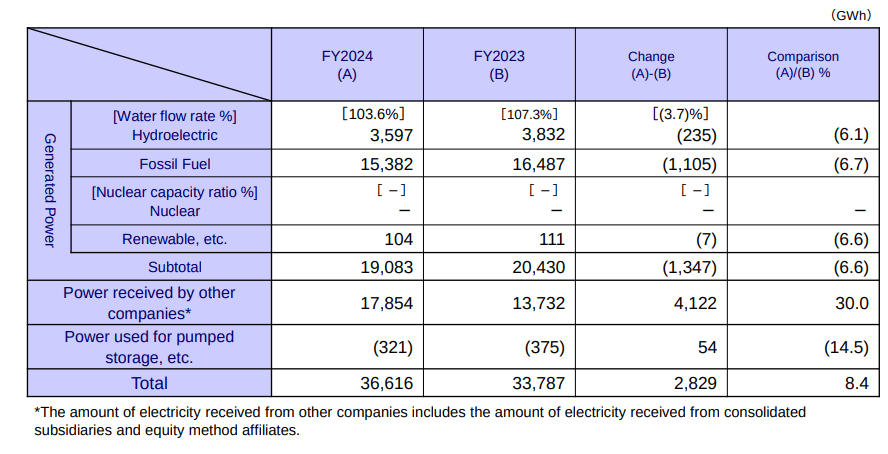

Although HEPCO has plans for restarting its nuclear power plant, it primarily generates energy through burning fossil fuels, with it contributing to around 80.6% of its total energy mix. This includes 18.8% from hydroelectric and 0.5% from other renewables.

HEPCO's total electricity production last financial year was 19,083 GWh. However, when one includes power received by its consolidated subsidiaries and equity method affiliates, this figure is 36,616 GWh.

HEPCO annual report

Looking ahead to the future, my analysis leads me to believe that HEPCO could generate an additional 17,178 GWh per year based on the projects that it has in its pipeline. If we assume that all else remains equal from last year's total energy output, this means it could output a total of 53,794 GWh of energy once and if these projects are completed and are fully operational.

It should be noted that I am making a number of assumptions regarding the capacity and operations of these energy projects. For instance, for the total energy capacity, I'm using estimates based on typical sizes for such projects in similar contexts as well as the data provided in the company reports. As such, the data was not specifically provided explicitly by the company, as it is only my personal estimation (which I have revised downwards).

Some of the projects HEPCO has in the pipeline to grow its total energy output include:

- Offshore Wind Farm in Ishikari Bay. This has a total installed capacity of 112 MW and it has 14 wind turbines. I believe a reasonable capacity factor for this wind farm (for how long it can be operated in the year) is around 35% when factoring in seasonality changes, leading to a contribution of 343.73 GW/h.

- Biomass Power Plant Project in Tomakomai. This has a stated capacity of 71.95 MW with an assumed biomass capacity factor of 80% based on estimates I could find online. If we assume continual operation, it could generate 525.43GWh per year. It should be noted, HEPCO is not involved directly in the construction or operation of the plant. However, it can be assumed that the power will be sold to HEPCO's subsidiary, namely the Hokkaido Electric Power Network Inc, which maintains the grid network and infrastructure. This is a typical practice of energy providers selling their output to grid network operators.

- Tomari Nuclear Power Station. This could contribute 2,070 MW to the energy mix via its three reactors. Readers should not underestimate the potential of a restart for Tomari, as it once provided "around 30% of the total electricity consumption of Hokkaido." If we assume an 80% utilization rate, which is below its historical estimates. It would mean it contributes 16,309.08GWh/year to HEPCO's total output.

The Tomari nuclear power plant restart then is a major development for the company and a central part to my thesis. Estimates provided by the media assert that it could come online again in December 2026; however, the company is struggling with the red tape of regulations due to them needing to pass safety inspections, particularly for safety against earthquakes and tsunamis, which Japan being one of the most seismically active regions on the planet.

It should be noted that a Japanese court issued an injunction against Tomari's restart in 2022. The judge ruled that the Tomari plant "does not meet required safety standards against tsunamis" and that it is therefore unsafe to operate. The case is a bit more complex than I'm describing, with the Japanese public, residents, and media criticizing HEPCO harshly and alleging that it reportedly mismanaged its initial court hearings.

However, I feel that HEPCO has a good chance of restarting its power plant thanks to it initiating work on a 19-meter seawall at Tomari, which would ostensibly address the previous judge's main objection as it was specifically created to help protect the site against tsunamis. It will also have time to re-present scientific evidence to address a concern that suggests Tomari rests on an active fault line, an allegation that HEPCO has denied strongly.

I think there's a good chance that HEPCO will reach approval for a gradual restart, as the court balances the interests of public safety, Japan's energy needs and the soaring cost for electricity for residents in Hokkaido due to Tomari's dormancy.

Financials

HEPCO reported a strong year of financial stabilization and recovery last year compared with the previous year's results. The company reported an operating revenue of ¥953.7 billion for FY2024, representing a year-on-year increase of ¥64.9 billion. Net profit also soared to ¥66.2 billion, a major improvement from a loss of ¥22.1 billion from the previous corresponding period. Electricity sales volumes also increased 9.2% to 33,924 GWh.

During this time, HEPCO also underwent a deleveraging process with total debt falling to $8.7 billion, down from $9.2 billion. Its debt-to-equity ratio is 3.88 at the time of writing. It should be noted that around 67% of its total assets were financed by debt, as evidenced by its debt-to-assets ratio. Japanese interest rates, especially on commercial loans, is also a fraction of what it is in the United States and other developed countries, which to me makes its debt burden more manageable than what it looks like on paper.

Results were also mixed for its most recent quarter. The firm reported an operating revenue of ¥202.5 billion for Q1 FY2025, which is a decrease of ¥25.2 billion (11.1%) compared to the same quarter. Profit attributable to HEPCO also decreased 9.7% to ¥3.3 billion. Demand for HEPCO's services remained basically the same from last quarter, with total sales only slightly down 0.3% compared with the same period last year. However, lower fuel prices and fuel costing posting periods hurt both its top and bottom lines.

For the rest of the year, HEPCO believes that net profit will be around ¥43.0 billion, which is a significant dip from last year's result of ¥22.1 billion, but still reflects its stabilization efforts.

Valuation

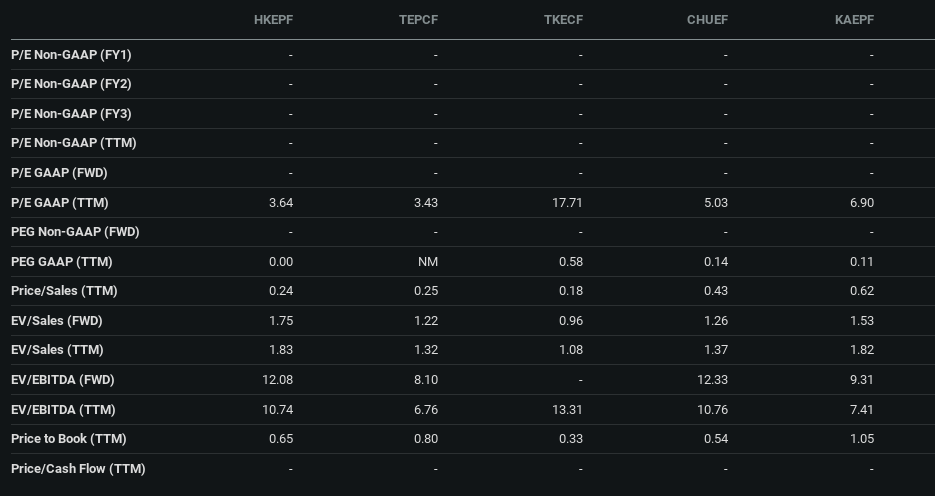

I think that HEPCO is undervalued when placed side by side against its peers. For this valuation analysis, I've chosen a universe of Japanese utilities stocks that operate a similar business model to HEPCO. All are major electricity providers. The companies I chose are the following:

- Tohoku Electric Power Company, Incorporated (OTCPK:TEPCF)

- Tokyo Electric Power Company Holdings, Incorporated (OTCPK:TKECF)

- Chubu Electric Power Company, Incorporated (OTCPK:CHUEF)

- The Kansai Electric Power Company, Incorporated (OTCPK:KAEPF)

HEPCO has outperformed half of its peers over the past five years, with half of them losing a substantial amount of value. HEPCO gained 1.60%.

Seeking Alpha

The company's earnings, sales, and book assets are cheaper on a per-share basis than almost all of its competitors in every case. Notably, its price-to-book ratio of 0.65 is the lowest among its peers, while its price-to-sales ratio of 0.24 is also the lowest. Its P/E of 3.64 is also among the lowest in the group.

I don't believe that HEPCO should be trading this cheaply then, considering that HEPCO has shown a stable revenue growth rate over the years, with a 3-year CAGR of 10.13%. Its net interest margin of 6.77% if it is also lower than its peers but still respectable.

Seeking Alpha

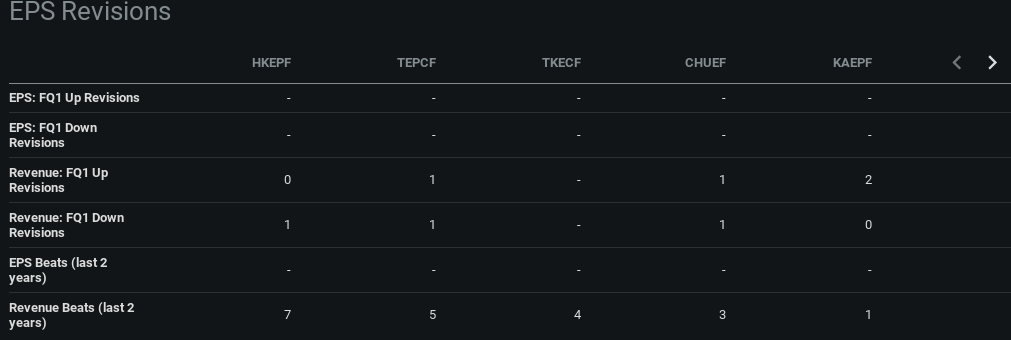

Something else which plays in HEPCO's favor is that it has managed seven revenue beats over the past two years. The company is also the smallest among its peers in terms of employees and market cap, at $1.4 billion and 9,206, respectively. I then expect it to have good growth potential (as far as utilities go), but much of this thesis hinges on Tomari being restarted.

Seeking Alpha

Risks

There are some idiosyncratic risks to Tomari's restart, especially concerning the culture of Japan and its perception towards nuclear energy. Although the country has 12 nuclear reactors currently running, there is an overtly negative public perception against nuclear energy in the country. As someone who has lived there, I can tell you that demonstrations and protests are not uncommon when the issue of nuclear power arises. World War II left deep scars on the Japanese psyche towards nuclear, and its frequent earthquakes and tsunami risks top it off to make it something the public doesn't want to engage itself with, which, I feel, could tip the balance in rejecting HEPCO's request to restart its operations.

Another key risk is that HEPCO currently has little in the way of substantial growth potential, aside from Tomari's restart. If it doesn't come online in a reasonable time frame, then its biomass and wind farm electricity generation may not support its valuation in the long-run, keeping it as a perpetual underperformer in terms of both earnings and revenue growth rate compared with its peers.

Conclusion

HEPCO is a buy despite the speculative risks of Tomari not coming online again or within a sufficient timeframe. I feel that it's taking the steps required to address the key objections against tsunami risks, and its valuation multiples reflect a strong implied upside if the restart goes ahead as planned. HEPCO then is a valuable opportunity for international investors looking to diversify themselves outside of the U.S. and other developed markets, and I therefore rate it as a buy and worthy of ongoing consideration

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.