DigitalBridge: Rapid Expansion But Wait For Progress On Costs (Rating Downgrade)

Summary

- DigitalBridge's share price has slid by more than 25% despite its revenues increasing rapidly over the last year.

- The reason appears to be connected to profitability as expenses have varied widely, raising doubts as to what will happen when the company scales further.

- On the other hand, it has rapidly advanced equity assets for which it earns fees (FEEUM) to $32.7 billion while accelerating capital formation to develop more data centers together with the power needed.

- Also, the high expectations for earnings growth seem to be unjustified meaning that the stock could suffer from volatility.

- I consider it to be a Hold until it makes progress on sustainably increasing profit margins.

halbergman/E+ via Getty Images

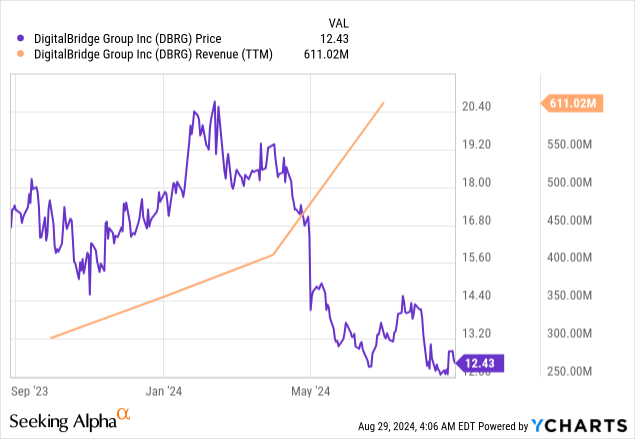

Since I was bullish on DigitalBridge (NYSE:DBRG) because of AI opportunities through its data center portfolio one year ago, its revenues have trended upward on a TTM (trailing twelve months) basis as seen in the orange chart below. Still, the stock returned -25.7%, proving me wrong.

Data by YCharts

Data by YCharts

This thesis will uncover the reason for such a price action using the sales and profitability metrics. Also, by going through the financing model including related risks in building the digital infrastructures to house the accelerated computing chips needed by super smart applications, I show how this stock could represent an opportunity as it dips further.

I first dive into the income statement to extract the bigger picture after it reported second-quarter financial results for the financial year 2024 (2Q24).

The Broader Picture

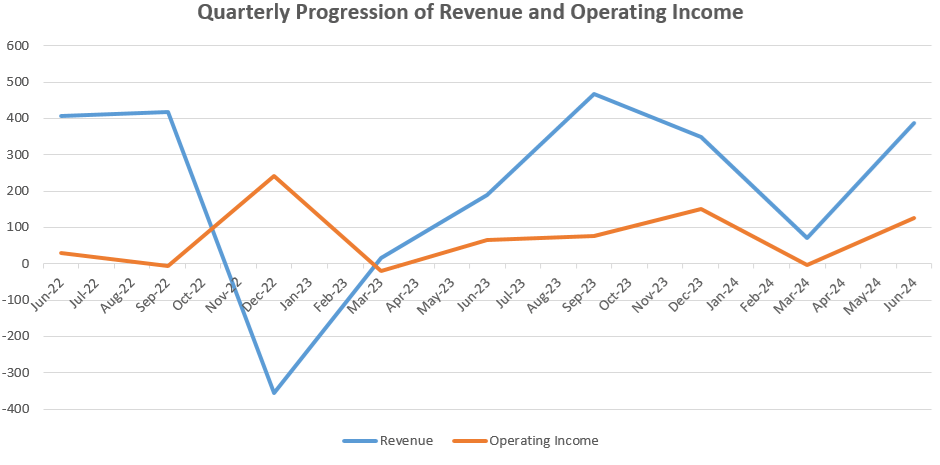

The broader picture covering the last eight quarters as per the chart below shows revenues and operating income fluctuating widely with the company returning a loss on two occasions. Also, despite revenues surging by 316% in the March quarter (1Q24), it suffered from a loss.

Charts were built using data from (seekingalpha.com)

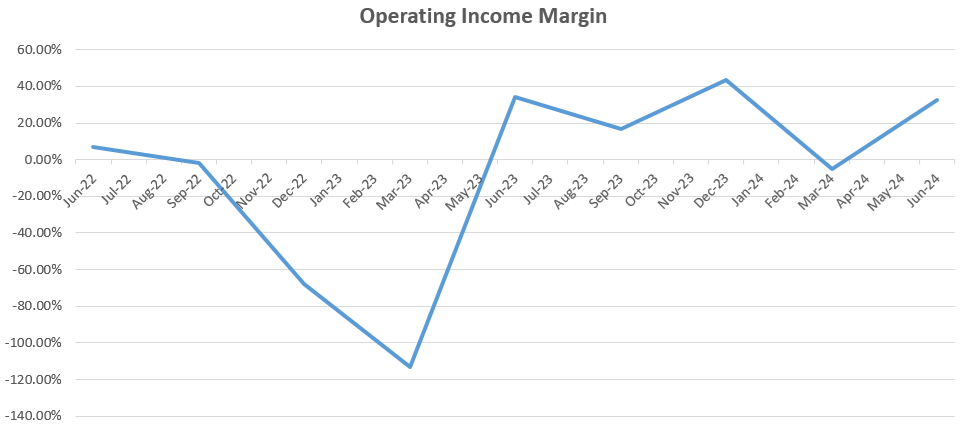

The reason is the high amount of cash and equity-based compensation which amounted to $51.2 million and when added to the administrative expenses of $24.3 million did offset the fee revenues of $73 million. Subsequently, things improved in 2Q24 when profits were back, but again looking at the bigger picture, the operating income margin has been on a net downtrend during the last four quarters, casting doubts as to how expenses are being managed as DBRG scales rapidly and obtains more fee income.

The chart was built using data from (seekingalpha.com)

Such performance may not have been easy to digest, especially for investors used to the relatively stable income and profits of the real estate sector which DBRG forms part of. Consequently, this could explain why despite revenues in the June 2024 quarter doubling relative to the same period last year (as per the introductory chart) investors were not convinced.

Looking at valuations, its trailing P/S of 1.6x last year has increased by 22% to 1.96x, while its shares fell by around 25%. This indicates that investors have higher expectations of future revenue growth for a stock that remains underpriced relative to the sector median, but I do not consider it a buy. The reason is the disconnect between the financial performance, achieved on the back of the FEEUM (or Fee Earning Equity under Management) increasing by 12% YoY to $32.7 billion, and what investors perceive to be the actual value of the stock.

Digging further into its value, the forward non-GAAP price-to-earnings ratio exceeding the sector median by 29% hints at high expectations for earnings growth. However, this may not justified as the management update mentions that margins should continue to increase in the remainder of this year as DBRG continues to raise capital but without providing any precision by how much.

Therefore, I believe that with such a high level of expectations built into the stock price, it could sink in case it does not deliver, and its uneven margin track record does not help either. However, I am not bearish on this alternative asset manager's prospects.

Resilient Financing Model for AI Infrastructure but There Are Risks and Competition

The reason is the resilient financing model with the company managing to raise capital while continuously adding properties for development to its portfolio. For this purpose, digital (or AI) infrastructure is a demand-driven market, one which has been accelerating since 2023 after the world was mesmerized by the abilities of OpenAI's ChatGPT, driven by Generative artificial intelligence.

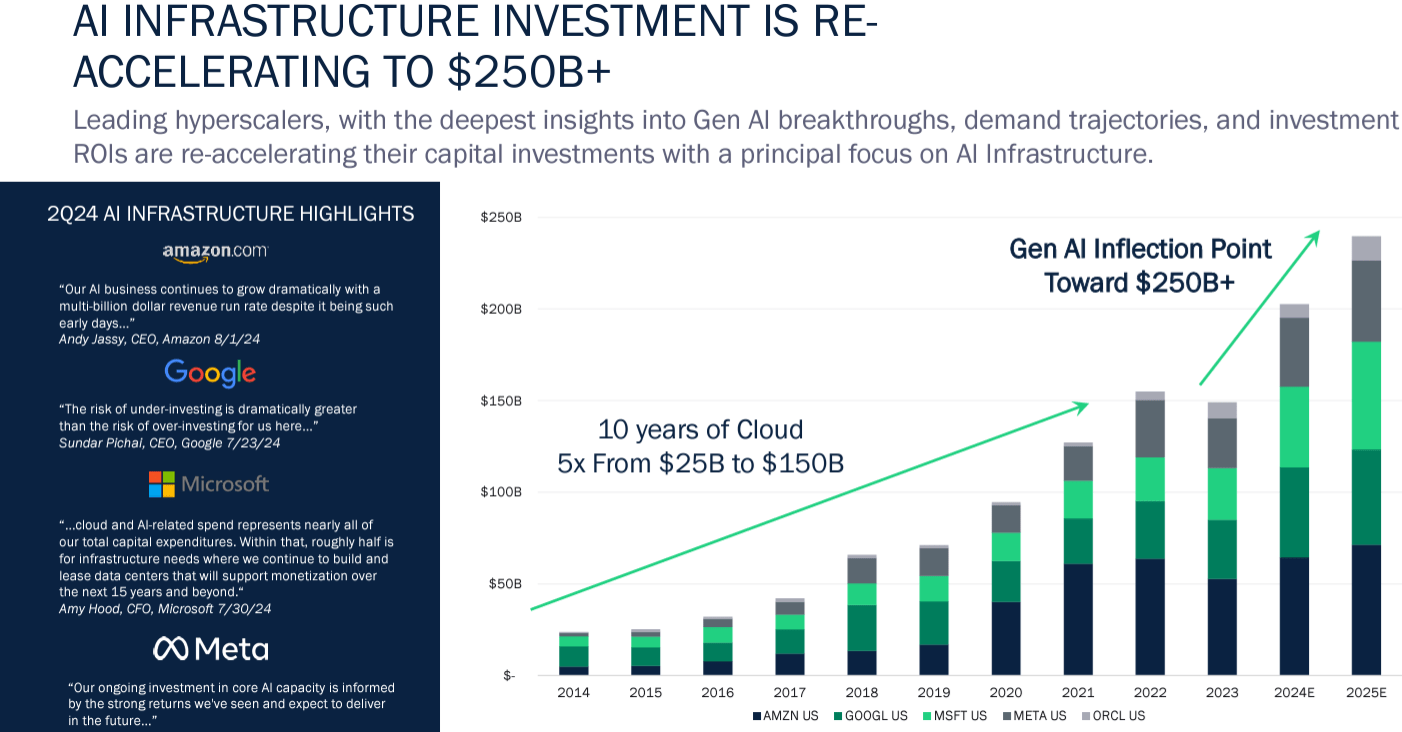

In this context, DBRG not only provides data center space to house the billions of dollars worth of accelerated computing GPUs Nvidia (NVDA) is selling every quarter but also the energy needed to power them. Also, it is expanding its already sizeable portfolio of assets with the construction of 90 data centers while adding 3.5 gigawatts of power to its existing capacity.

Company Presentation (seekingalpha.com)

Assessing for risks, data center pricing or the costs associated with hosting has surged by 20% YoY for North American data centers due to high demand and supply shortages. The problem is this may reach a breaking point whereby the hyperscalers such as Amazon (AMZN) as pictured above which are DBRG's customers start to build given that they have the financial capability to do so. Currently, hyperscalers are dedicating most of their billions of dollars of data center Capex to acquiring GPUs from Nvidia, together with AI networking.

Thinking aloud, in case hyperscalers were to resort to self-building, not only the developer would see dwindling demand for its assets but the very financing model which consists of aggressively raising capital through co-investments would be at risk. In this respect, while this type of financing effectively shares the investment burden thereby mitigating the risks while reducing the need to borrow at higher interest rates, it also introduces certain challenges. In this regard, when things are running smoothly, people tend to be happy but when the going gets tough, disagreements start to emerge leading to conflicts over investment decisions and exits.

Furthermore, the competitive landscape has changed considerably with incumbents like Digital Realty Trust (DLR) expanding to become an AI factory while Bitcoin (BTC-USD) miners have also diversified to become HPC or high-performance computing providers by taking advantage of the fact they have access to some of the nation's best renewable power sources. Pursuing further, there is competition from other asset managers who have acquired data center REITs and are well positioned in connection to AI infrastructure with Blackstone (BX) acquiring QTS for $10 billion in 2021. The same year, KKR (KKR) and Global Infrastructure Partners partnered to acquire CyrusOne for $15 billion.

Risk Mitigation with a Diversified Financing Base

To differentiate itself from the competition, DBRG aims to be the leader in global AI infrastructure already equipped with 173 data centers powered by 4 gigawatts of capacity. In this case, scale confers the asset manager with a position of strength to negotiate with suppliers while a higher data center market share allows it to be more appealing to new customers, both leading to better returns. This is also attractive to partners and investors alike.

Looking at risk mitigation, firstly, DBRG makes sure that it has a customer for everything it is building and these include deep-pocketed hyperscalers like Alphabet (GOOG), Microsoft (MSFT), and Meta Platforms (META). Secondly, it carefully selects its partners and negotiates clear investment terms while maintaining a diversified portfolio of co-investments to reduce dependency on a single funding source. Moreover, in addition to co-investment, also raises capital through its flagship funds and credit facilities as shown below.

Company Presentation (seekingalpha.com)

This implies a multi-pronged approach to rapidly capitalize on opportunities in AI infrastructure without sacrificing operational flexibility. Also, with the Federal Reserve likely to cut interest rates next month, it could leverage more credit as part of the capital mix as borrowing costs start to decline.

Furthermore, up to now, there have been no signs of investor fatigue around the AI infrastructure ecosystem when it comes to capital formation with the company's successful track record in the digital infrastructure industry helping it to “progress across many of its key 2024 priorities”. Also, the balance sheet-friendly way it has raised capital resulted in only $421 million versus cash of $354 million while investing billions and boasting a FEEUM of $32.7 billion.

However, the AI theme is currently subject to a lot of hype, and monetization concerns have emerged, which is the reason for adopting a more cautious stance, especially after Nvidia's data center segment's growth has slowed. Therefore, there may be some pullback meaning that at this particular juncture, it is better to wait for more clarity before investing.

The Stock could Dip further and What to Look for Before Investing

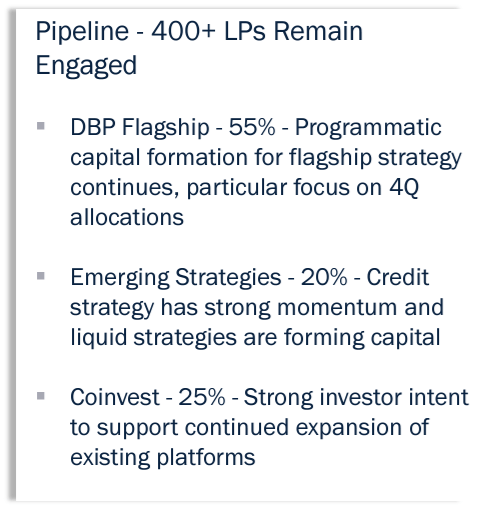

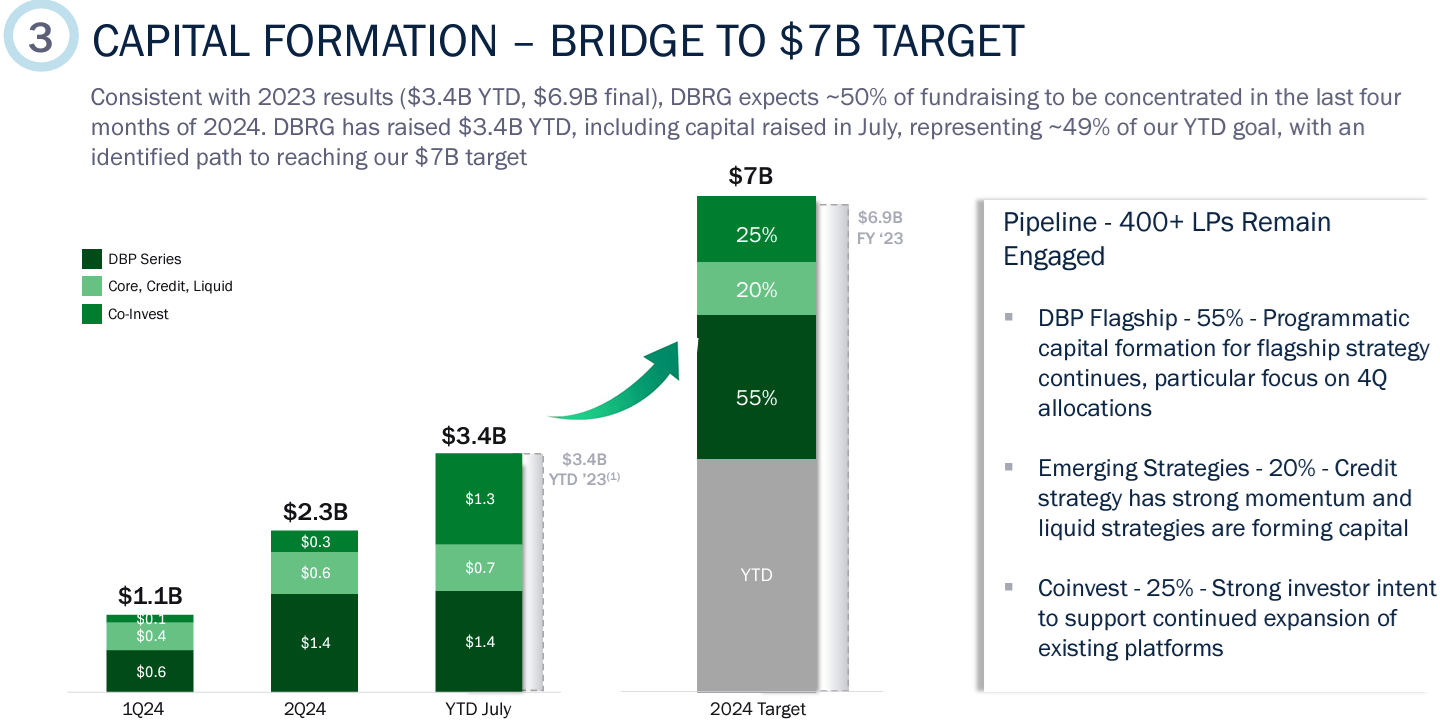

Thus, more risk-aware investors may want to wait for DRBG to achieve its capital formation target for the rest of this year. In this respect, it has already raised $3.48 billion as of July but plans to raise $7 billion in total within the balance of this year as shown below. Its ability to achieve this target while seeing oversubscriptions to its funds, as has been the case in the past, would demonstrate sustained engagement from its pipeline of Limited Partners (LPs).

Company Presentation (seekingalpha.com)

Along the same lines, bearing in mind the need to monetize services through fee revenues in a profitable manner, some would prefer to wait for margins to improve sustainably as discussed previously.

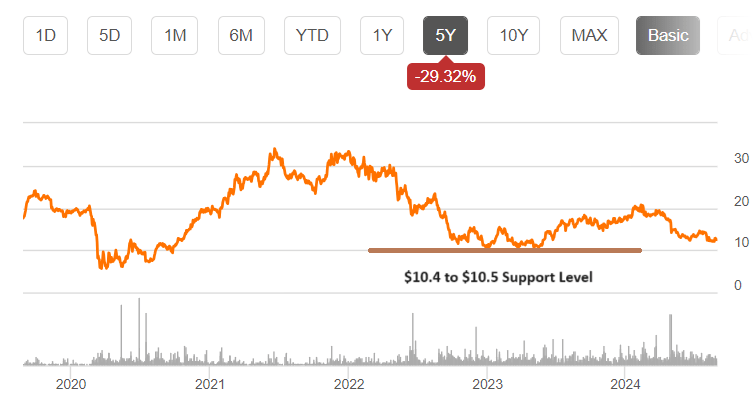

In the meantime, with the share price trading well below the 50-day, 100-day, and 200-day moving averages, there may be further downside, possibly to the $10.4 to $10.5 support level as shown below. This could constitute an opportunity to buy.

www.seekingalpha.com

In conclusion, this thesis has provided an update on why DBRG's share price has failed to appreciate despite the asset manager deriving more revenues and successfully financing the expansion of digital infrastructure assets. The reason is investors seem to be more concerned with the costs which explains my Hold position, but there should be continued demand for data centers, as, after building AI infrastructure for the training of LLMs (large language models), the next phase is for the inference or usage phase as Gen AI proliferates along the IT value chain.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.