Tyson Foods: Still A Good Meal For Your Portfolio

Summary

- Tyson Foods' Beef segment is struggling due to margin compression, while Chicken and Pork segments show improvement.

- The company's overall financial performance has improved, making shares attractively priced compared to similar businesses.

- Longer term, the firm will be better off if it shifts even more to chicken, but even in the near term that could prove positive for shareholders.

RiverNorthPhotography

Typically, I tend to shy away from companies in the food industry. This is because it is a significantly competitive market that is, by definition, commoditized. There are always some exceptions to this, however. Even though it deals in about as commoditized a market as possible, one company that I have been bullish on is Tyson Foods (TSN). In my last article about the business, published in early May of this year, I maintained that shares of the company were attractively priced. Analysts were also looking favorably at the business, though there were some weak spots.

Ultimately, I ended up reaffirming it as a ‘buy’ candidate. But since then, things have fallen a bit flat. Shares are up only 3.3% at a time when the S&P 500 is up by 10.5%. This is in spite of the fact that management has achieved some pretty impressive results on a year-over-year basis. Looking into the data, I would argue that some of the weak spots for the company remain. But given how cheap shares are, especially relative to similar enterprises, I don't think that my ‘buy’ rating on the business needs to change.

Taking another bite

Author - SEC EDGAR Data

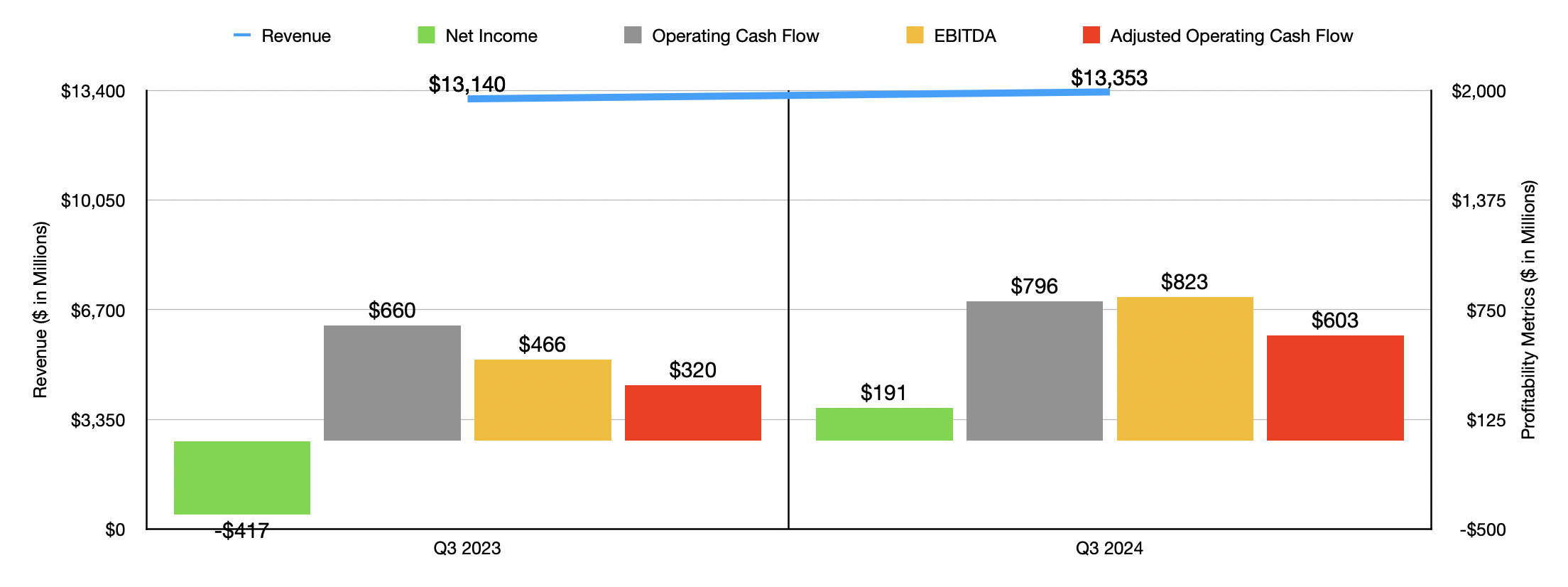

When analyzing Tyson Foods, I think it's best to look at the broad picture first and then to dig a bit deeper from there. Sticking with this approach, I think it's best to look at financial results covering the most recent quarter for which management has reported data. This would be the third quarter of the 2024 fiscal year. During this time, revenue for the company totaled $13.35 billion. This was 1.6% above the $13.14 billion the company reported one year earlier. But this is where digging deeper comes into play.

Tyson Foods

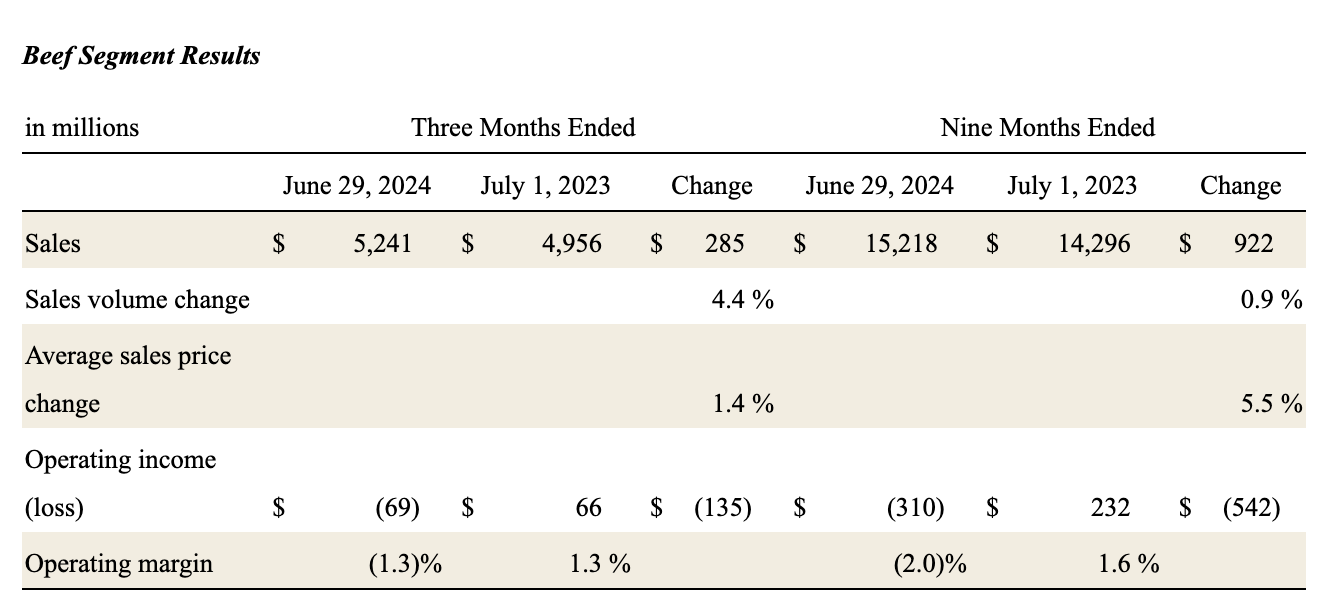

Even though it's accurate to describe Tyson Foods as a food company, it really is a collection of different food businesses. And these can be analyzed by looking at the firm’s segments individually. The largest of these, by a rather significant margin, is its Beef segment. During the most recent quarter, sales for the unit came in at $5.24 billion. This happens to be 5.8% higher than the $4.96 billion reported just one year earlier. Most of this growth was driven by a 4.4% rise in beef volume. However, the company also benefited to the tune of 1.4% from higher pricing.

This year has been an interesting time for the beef market. When you look at the first nine months of 2024 as a whole, revenue for the segment of $15.22 billion was 6.4% above the $14.30 billion reported one year earlier. In this case, the reason for the sales increase flips compared to just the third quarter on its own, with volume up by only 0.9% while average sales prices are up 5.5%.

You would probably think that this rise in sales, particularly to the extent that it was driven by price increases, would be bullish for the firm from a profit perspective. But you would be wrong. In the most recent quarter, the segment lost $69 million. That compares to the $66 million of profit reported just one year earlier. And for the first nine months of this year, losses were $310 million compared to the $232 million in profit generated for the first nine months of 2023. According to management, these operating losses came about because of compressed beef margins. There were some other factors as well, such as the recognition of a legal contingency accrual and a plant closure. But most of the problem is undeniably being caused by the aforementioned margin compression.

For those who follow the beef industry closely, this should come as no surprise. But if you have not dug into the data previously, it would be understandable for there to be a bit of confusion. One source, published in April of this year, provide some more detail into the state of the beef market for the US. That source accurately points out that beef prices are increasing because beef demand has remained strong. However, overall supply is dropping. For a couple of years now, beef herds have been declining in size. High input costs, combined with drought and supply chain issues, have all played a role in this. It's this piece that should finally click why margins are compressing when prices and volumes are rising. It's because the reduction in industry output is being caused by pressure being applied to the beef providers, and it's just due to its own operational purposes that Tyson Foods is seeing output grow. The company is essentially being put in a position to hike prices, but not by enough to offset the price increases that it has to contend with. Unfortunately, this trend is likely to continue into 2025. So if anything, the beef situation will get worse before it gets better.

Tyson Foods

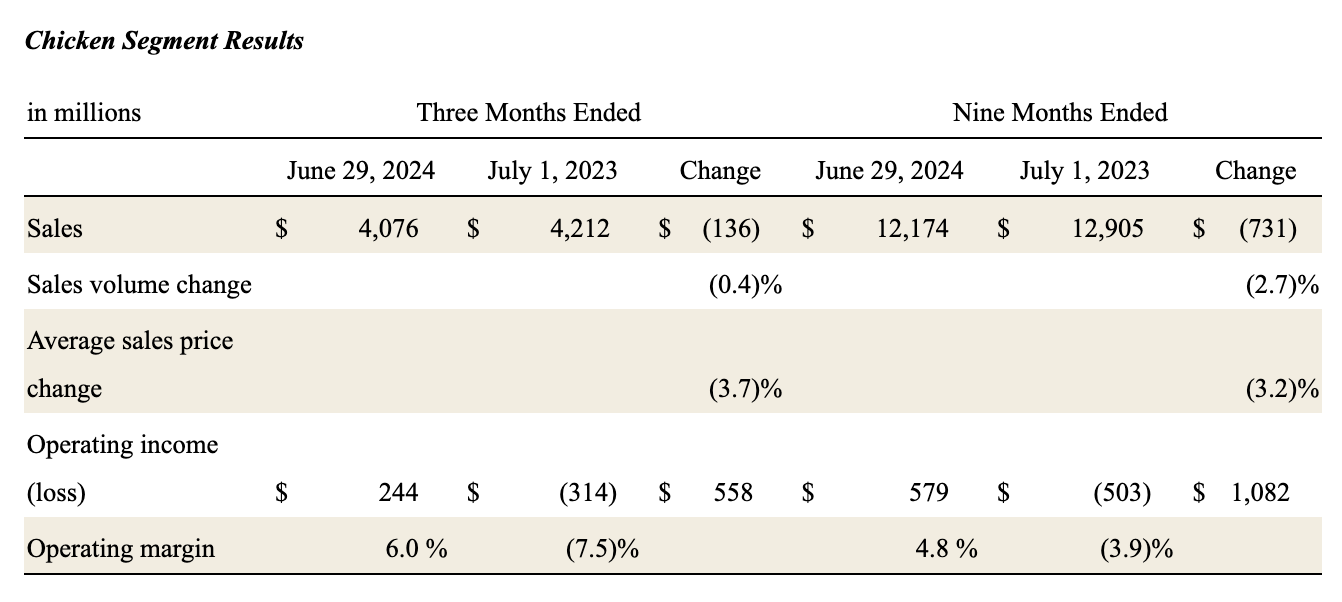

Fortunately, other parts of the company are doing considerably better. The best of them is the Chicken segment. Revenue has dropped year over year, falling from $4.21 billion in the third quarter of last year to $4.08 billion the same time this year, and falling from $12.91 billion in the first nine months of last year to $12.17 billion the same time this year. This is because of a decline in volume and lower pricing. It may seem odd for me to say that this is the best performing segment that the company has at this point in time given these circumstances. However, even as management has to reduce costs, certain input costs are improving significantly. In the most recent quarter, segment profits came in at $244 million. That's far better than the $314 million loss reported the same time last year. A big part of this, but not the only part, was a reduction in feed ingredient costs of $305 million. And for the first nine months of this year, the $579 million in profits generated far exceeded the $503 million loss reported for the same time of 2023. In this case, the company benefited from a $665 million reduction in feed ingredient costs. I will happily accept lower revenue but higher profits.

Tyson Foods

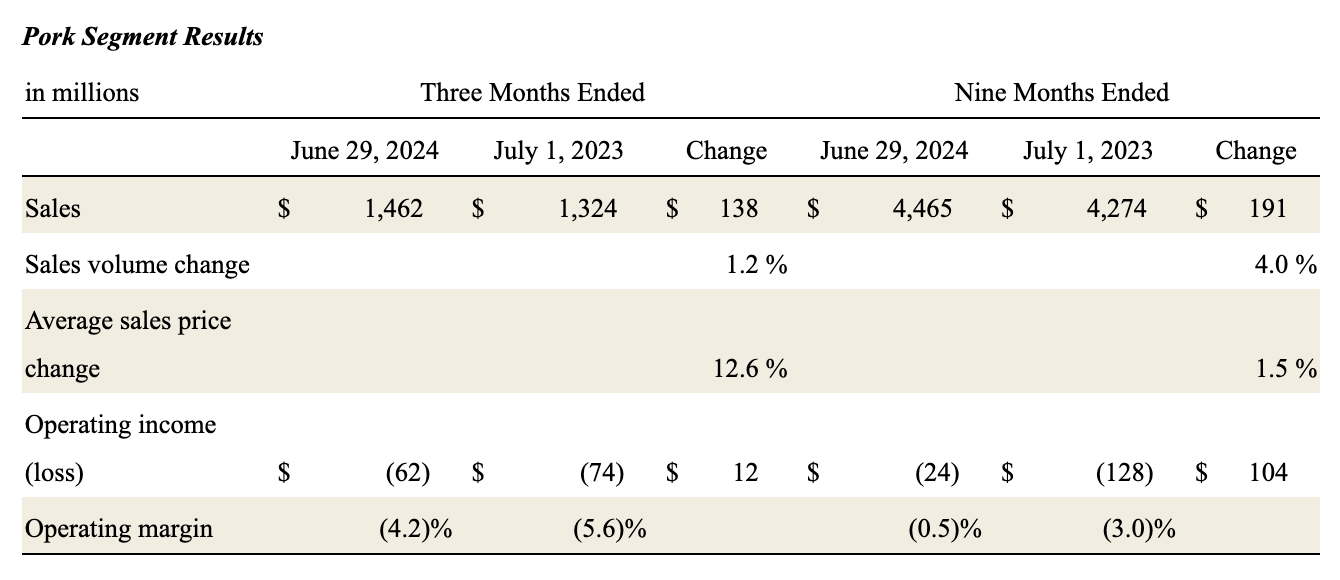

We also saw some improvement when it comes to the Pork segment. In this case, higher sales volumes and higher prices have pushed revenue up. In the most recent quarter, the company generated $1.46 billion from pork. That's up from $1.32 billion reported one year earlier. And for the first nine months of this year, sales of $4.47 billion beat out the $4.27 billion reported the same time last year. As you can see in the image above, operating losses have narrowed, both during the most recent quarter and for the first nine months of this year, all relative to the same time last year. Higher pork margins were the result of improvements in live hog operations, plus the absence of certain expenses that the company had related to a facility fire in the third quarter of 2023.

Tyson Foods

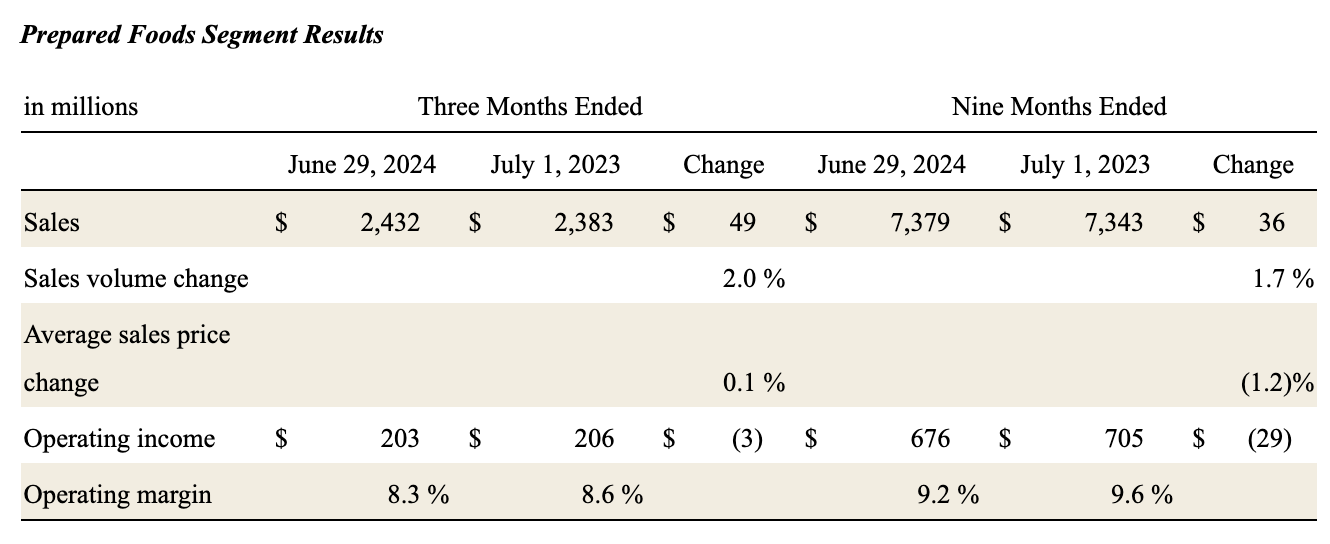

It is worth noting that Tyson Foods does have a rather small International/Other segment. But with this accounting for only 4.4% of overall sales in the most recent quarter, I don't consider it important enough to really delve into. That leaves us with only one other segment, which is the Prepared Foods segment. In this case, as the image above shows, sales have increased modestly during the time periods that we are discussing. But there has been a slight decline in operating income, particularly when it comes to the first nine months of this year compared to the same time last year. Raw material costs have risen and impacted the company negatively. For the first nine months, the company also suffered from a decline in average sales prices. However, reduced marketing, advertising, and promotional spending helped to offset some of these pain points.

Author - SEC EDGAR Data

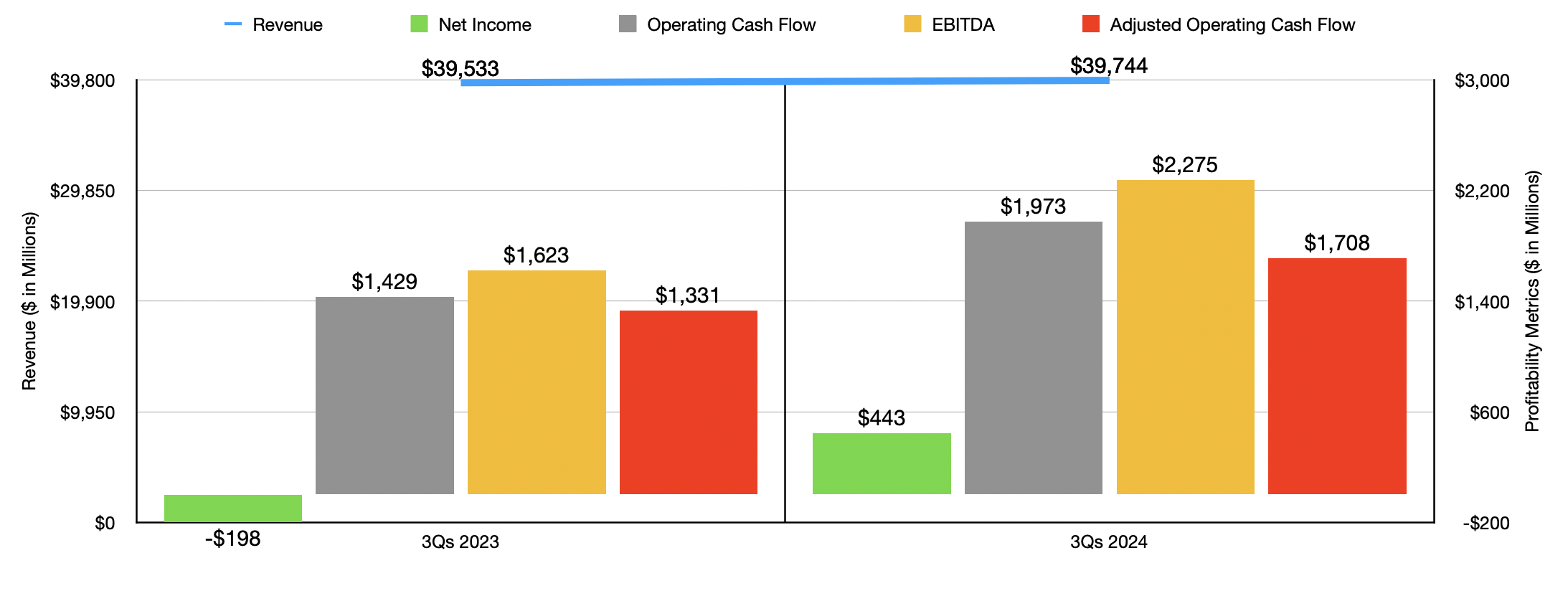

Thanks to the improvements and Chicken and Pork, Tyson Foods has seen a meaningful improvement on its bottom line. In the most recent quarter, the company generated a net profit of $191 million. That's far better than the $417 million loss reported one year earlier. Operating cash flow jumped 20.6% from $660 million to $796 million. If we adjust for changes in working capital, we get a near doubling from $320 million to $603 million. And finally, EBITDA shot up from $466 million to $823 million. In the chart above, you can also see results for the first nine months of this year compared to the first nine months of last year. As was the case with just the third quarter on its own, revenue is up slightly, but profits and cash flows have seen material improvements.

Author - SEC EDGAR Data

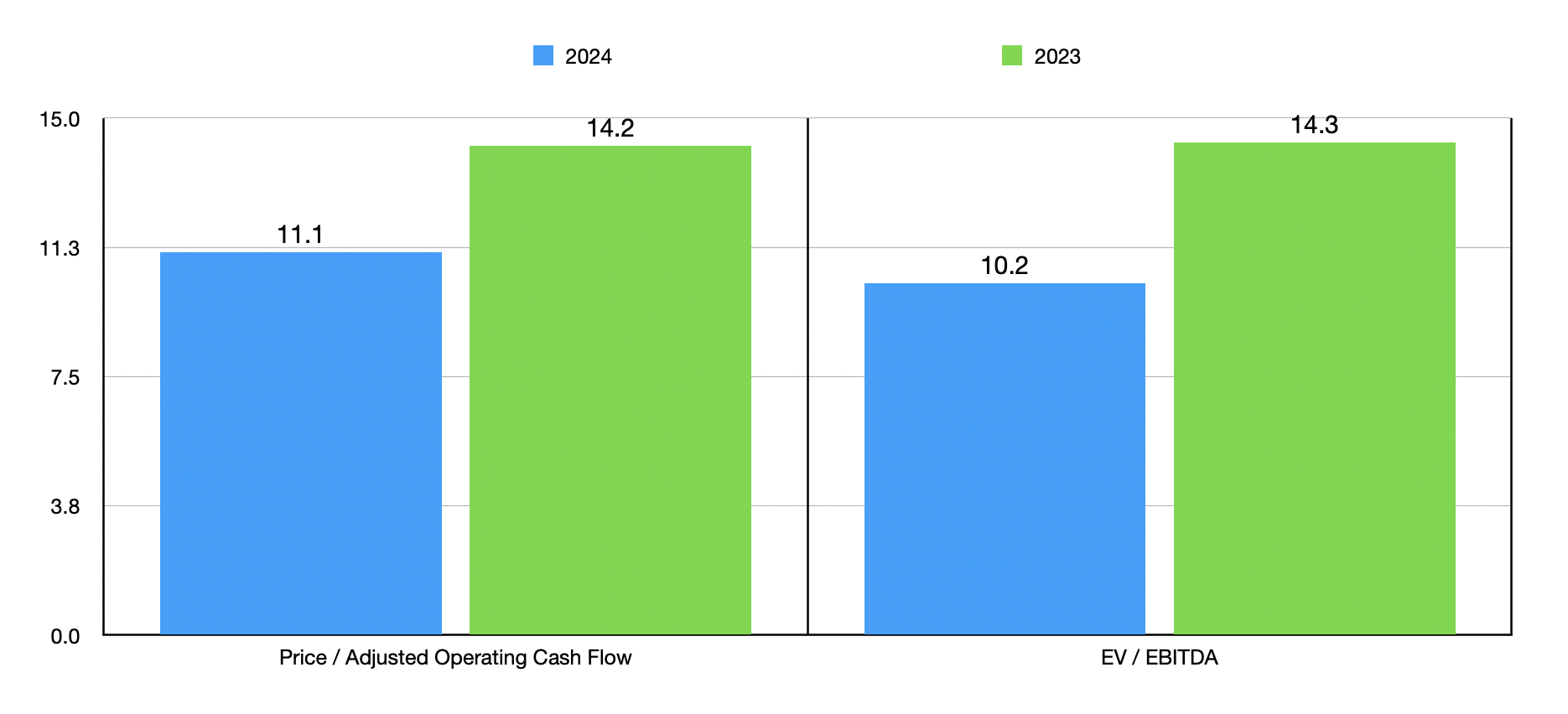

We don't really have any detailed guidance for what the rest of this year will look like. But if we annualize the results seen so far, we should anticipate adjusted operating cash flow of $2.01 billion and EBITDA of $3.01 billion. In the chart above, you can see what this does to the company's valuation on a forward basis. The chart, for context, also values the business based on results from 2023. Shares go from looking decent to looking fairly attractively priced. But this alone is not enough to warrant a ‘buy’ rating in my book. We also need to see how shares are priced compared to similar businesses. In the table below, I compared it to five such firms. On a price to operating cash flow basis, Tyson Foods was the cheapest of the group. And on an EV to EBITDA basis, only one of the five companies was cheaper than it.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Tyson Foods | 11.1 | 10.2 |

| Kellanova (K) | 15.9 | 20.0 |

| McCormick & Company (MKC) | 18.4 | 20.1 |

| Hormel Foods (HRL) | 13.9 | 15.4 |

| Lamb Weston (LW) | 11.3 | 9.3 |

| Campbell Soup Company (CPB) | 13.5 | 13.7 |

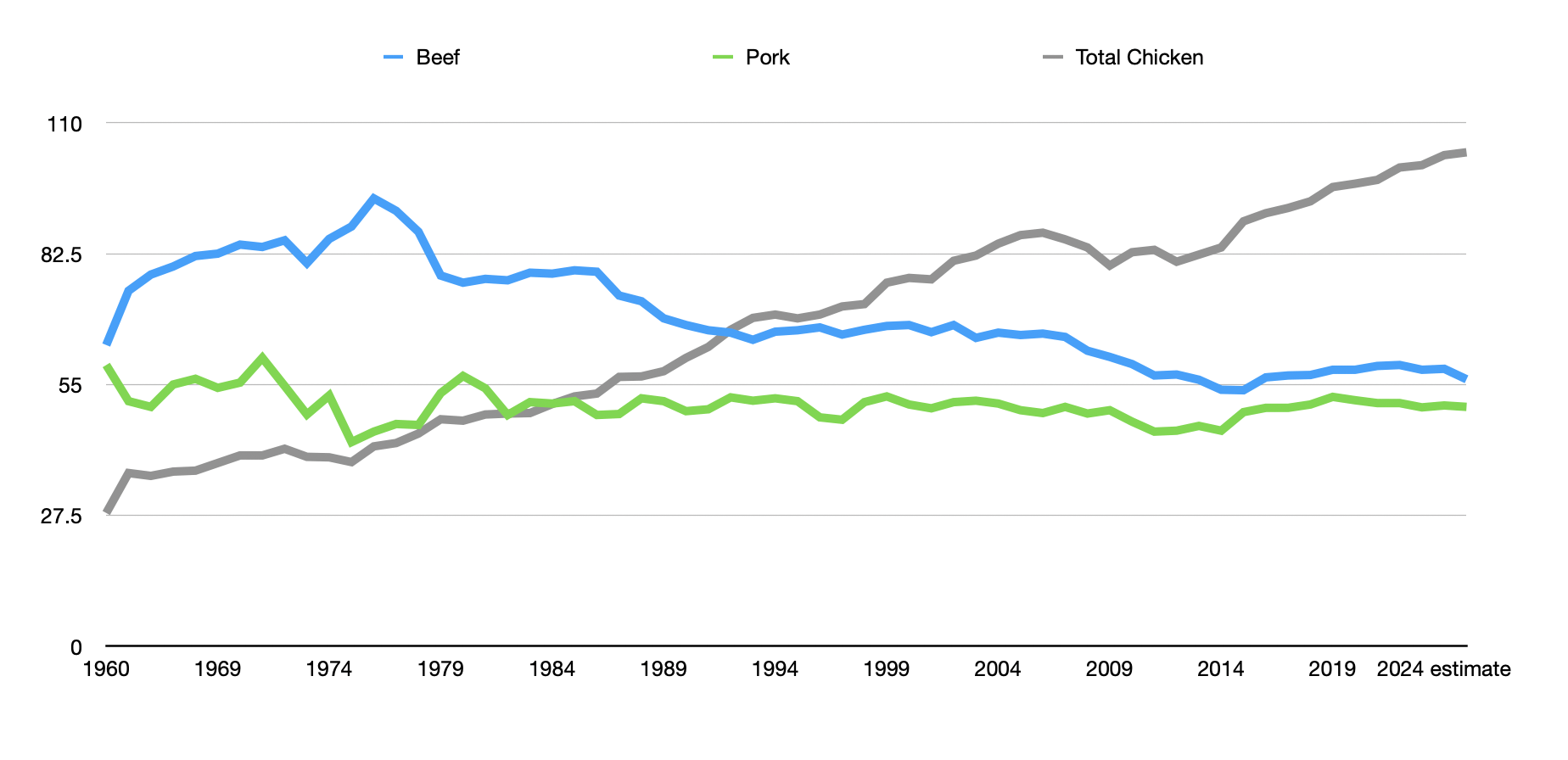

In the near term, it is possible that continued pain involving beef could weigh on the company. We should be paying attention also to the long run. Unfortunately, the outlook for beef is not that great. Beef consumption per capita in the US has been in an almost constant state of decline since the 1970s. There has been a small drop in pork consumption, but it has largely leveled off over the last 30 or so years. How well the industry adapts to reduced consumption of beef will play probably the largest role in how well Tyson Foods does on that front. And that is something that investors would be wise to pay careful attention to. But the bright spot involves chicken consumption. Due to the low cost of chicken, combined with favorable consumer preferences and health benefits that have come to light relative to beef, chicken consumption has exploded over the past several decades. Back in 1960, the average American consumed 28 lbs of chicken annually. By 2023, this had hit an all-time high of 101.1 lbs. This year, it's expected to grow to 103.2 lbs, before climbing even further to 103.8 lbs per capita next year. The fact that margins are currently very high for chicken should bode well for Tyson Foods, hopefully long enough for the beef industry to get its act together.

Author - National Chicken Council Data

*Per Capita in Pounds Each Year

Takeaway

Based on the data provided, I can understand why the market might have disagreed with me to some extent regarding the potential that Tyson Foods has. Beef operations are a particular problem at this point in time. But outside of that, the company is doing quite well. In fact, as a whole, things are going nicely. Shares might not be the cheapest thing out there, but they are cheap relative to similar enterprises. When you add all of this together, I think that maintaining the ‘buy’ rating I had on the stock previously makes sense.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.