Preferred Bank: Solid Upside Should Continue Despite Some Weaknesses

Summary

- Preferred Bank shares have outperformed the market slightly, up 10.1% in recent months.

- Despite some weaknesses in financial results, deposit, and loan growth have powered the bank to greater heights.

- Shares are attractively priced relative to earnings, with high-quality assets and low debt, making the company a sensible 'buy'.

Edwin Tan/E+ via Getty Images

Some companies end up being gifts that keep on giving. One good example of this that I could point to involves a rather small regional bank by the name of Preferred Bank (NASDAQ:PFBC). In the past, I have written about the institution, which emphasizes serving the Chinese American market, on two separate occasions. In my last article, which was published in March of this year, I stated that the company still represented a solid prospect for investors. This led me to reaffirm the ‘buy’ rating I had on the stock previously. Since then, shares have outperformed the market slightly, being up 10.1% at a time when the S&P 500 is up 9.2%. And since I first rated it a ‘buy’ in July of last year, shares have generated upside of 24.7% while the S&P 500 has risen by 22.2%.

Even though this is technically outperforming the market, I wouldn't say that the outperformance has been significant. But strong performance is strong performance nonetheless. After seeing the moves higher that shares have seen, it stands to reason that investors might wonder how much additional upside, if any, can still be had. Looking at the company's most recent financial results, we do see a bit of weakness on its top and bottom lines. But relative to earnings, even projected earnings, shares remain attractively priced. The company might be a bit pricey relative to its book value. This is especially true when you consider how little revenue comes from non-interest income. But when you come to understand just how high quality its assets are, and you pair that up with the affordability of shares relative to earnings, it's difficult to rate the company anything other than a ‘buy’.

The picture remains sound

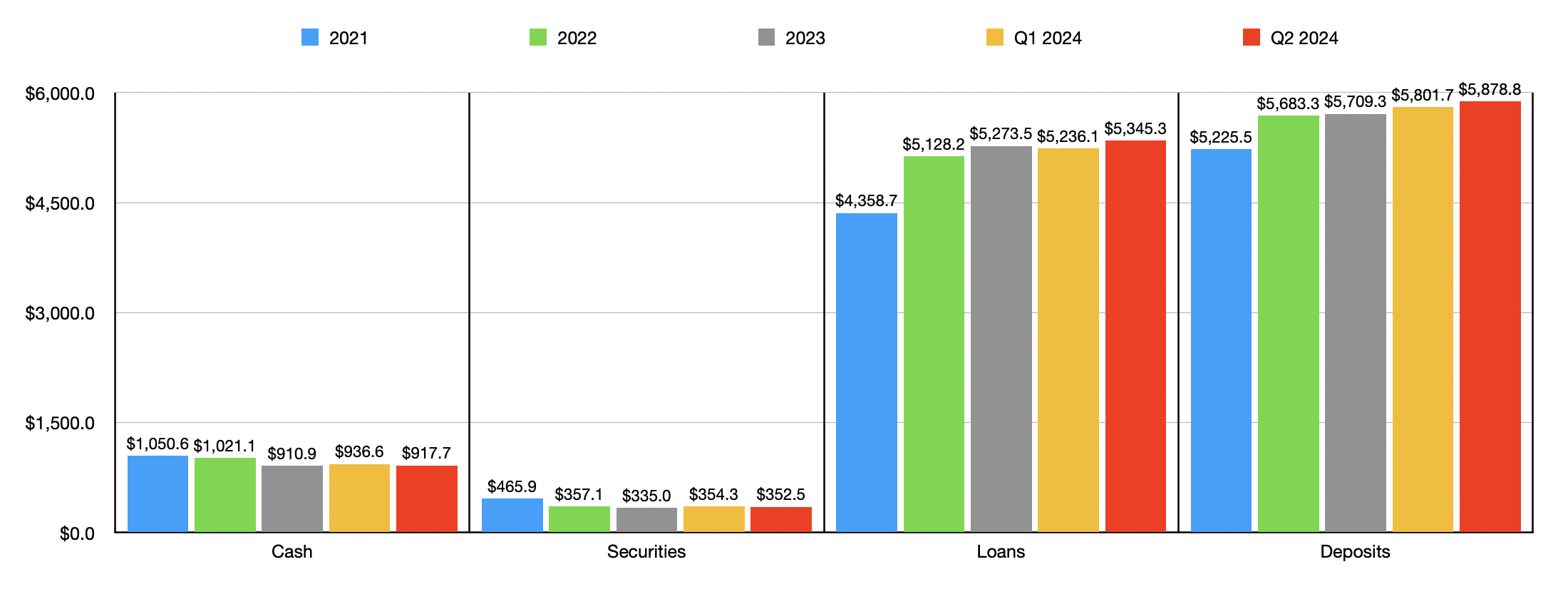

In my last article about Preferred Bank, we only had data covering through the final quarter of the 2023 fiscal year. Today, results now extend through the second quarter of 2024. The great thing about Preferred Bank is that the company continues to achieve growth, even during these uncertain times. Take deposits as an example. At the end of 2023, the business had deposits of $5.71 billion. These increased to $5.81 billion in the first quarter of this year, before climbing further to $5.88 billion in the second quarter. At the end of the day, deposit growth is integral to any bank that wants to grow. And this is because the deposits are what banks use in order to give out loans, invest in securities, and ultimately generate a profit.

Author - SEC EDGAR Data

This deposit growth has, sure enough, powered the company to even greater heights when it comes to certain parts of its balance sheet. In the most recent quarter, loans totaled $5.35 billion. This is up from the $5.24 billion reported just one quarter earlier, and it stacks up nicely against the $5.27 billion the bank ended last year at. Over the same window of time, the value of securities on its books went from $335 million to $352.5 million. It is worth mentioning that the second quarter figure was a tad lower than the $354.3 million reported for the first quarter of the 2024 fiscal year. But you will see fluctuations from time to time.

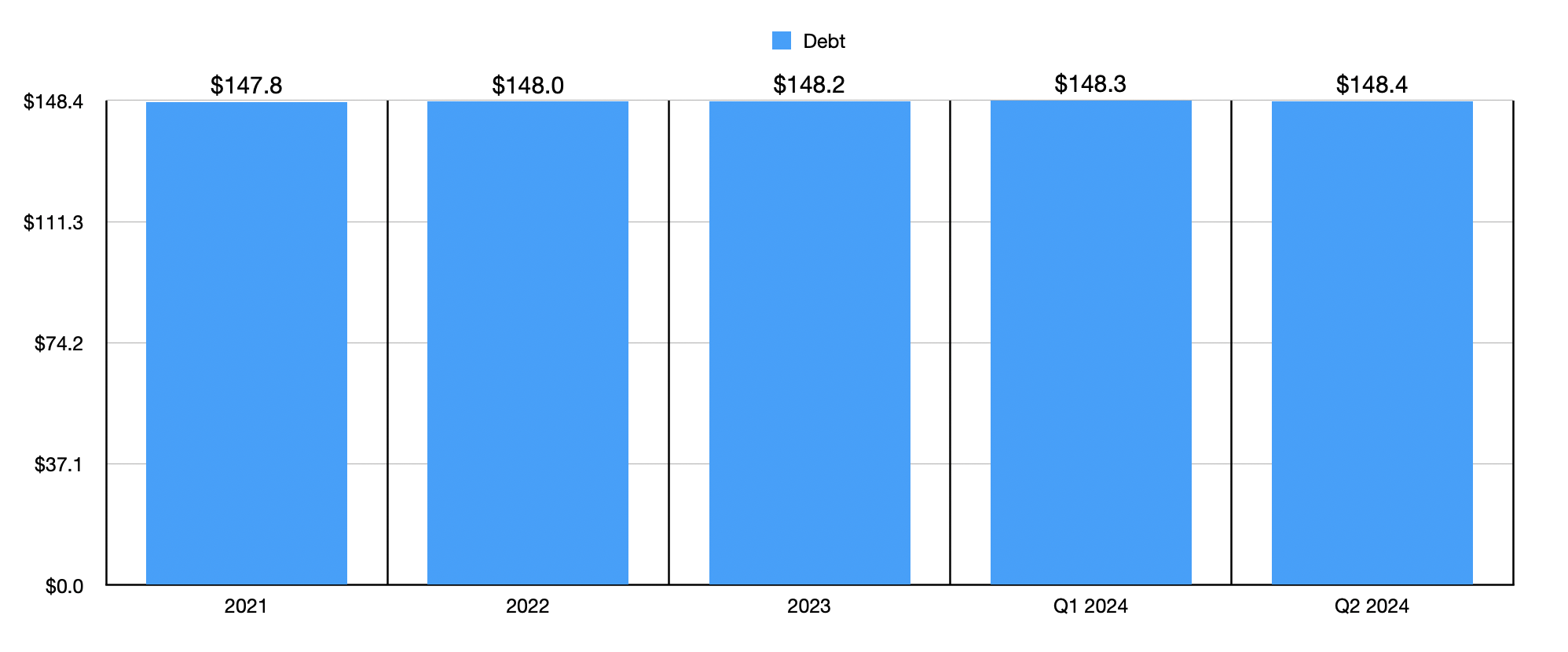

Cash and cash equivalents have been a bit more volatile. After climbing from $910.9 million at the end of last year to $936.6 million in the first quarter, they did dip down to $917.7 million in the second quarter of this year. Even though I don't like to see declines in any major asset, these fluctuations are inevitable. One thing that has barely budged, however, has been debt. At the end of the 2023 fiscal year, the company had $148.2 million in debt on its books. This number inched up only slightly to $148.4 million in the most recent quarter. This is a fairly small amount of debt that should result in fairly low risk to investors.

Author - SEC EDGAR Data

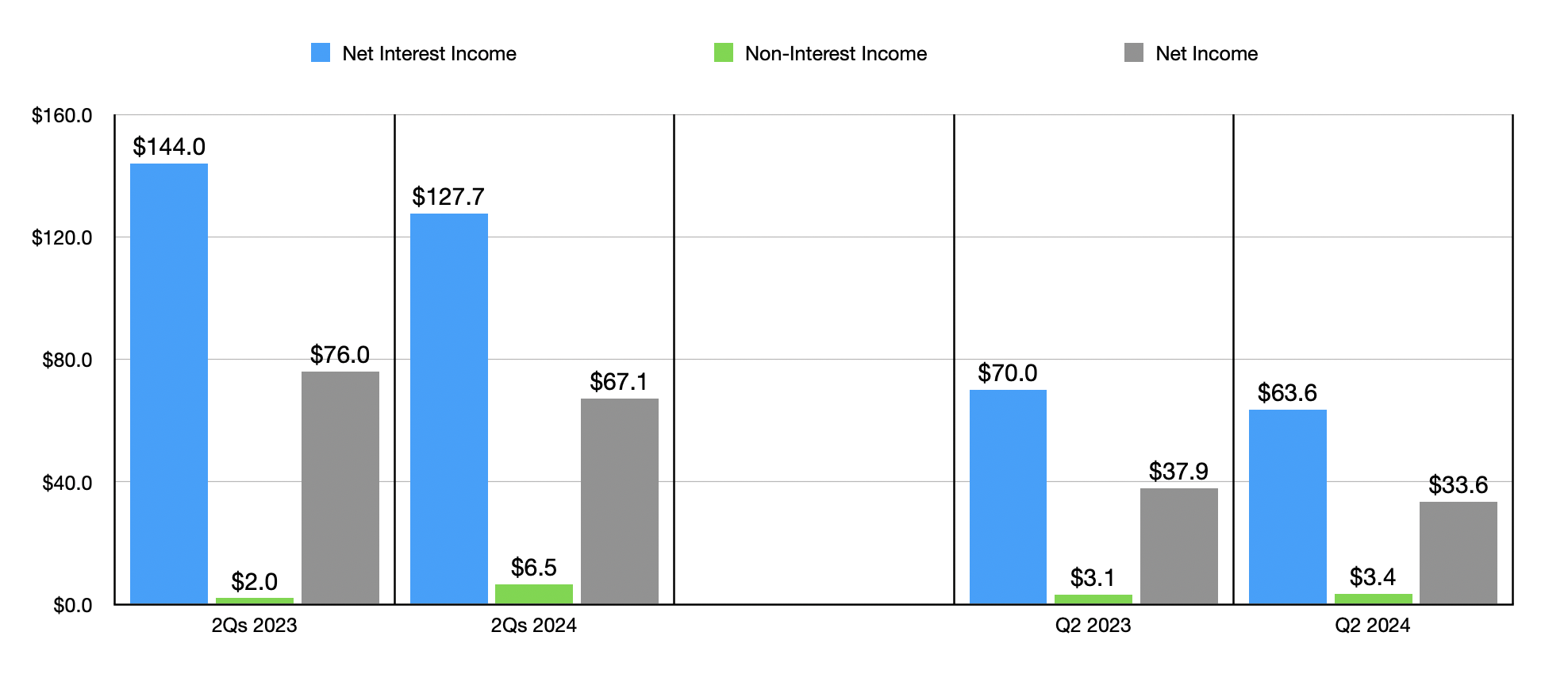

Moving on to the income statement, we have seen some weaknesses. Even though loans and securities have increased and debt has remained almost unchanged, net interest income dropped from $70.8 million in the second quarter of last year to $63.6 million the same time this year. For the first half of this year as a whole, the amount was $127.7 million, compared to the $144 million reported one year earlier. This drop was driven by a plunge in the company's net interest margin from 4.58% in the second quarter of last year to 3.96% the same time this year, and from 4.67% in the first half of last year to 4.07% the same time this year.

Author - SEC EDGAR Data

The fact of the matter is that high interest rates have proven to be problematic for many institutions. They have had to, unfortunately, increase the amount that they pay depositors in order to grow deposits or, in some cases, to even keep them unchanged. As an example, in the second quarter of last year, the company had only pay 3.69% per annum on all interest-bearing deposits. That number in the most recent quarter of this year was 4.63%. And for all interest earning liabilities, the rise was from 3.73% to 4.60%. By comparison, for all interest earning assets, we saw only a modest uptick from 7.39% to 7.61%.

Even though net interest income took a hit year over year, the same cannot be said of non-interest income. The rise for the most recent quarter was from $3.1 million last year to $3.4 million this year. And for the first half of this year, it was $6.5 million compared to the $2 million reported last year. This is mostly because, last year, Preferred Bank incurred $4.1 million in net losses on the sale of investment securities. This more than offset growth elsewhere, such as the rise in letters of credit fee income from $2.9 million to $3.3 million. Unfortunately, these improvements were not enough to prevent net income from dropping. In the most recent quarter, the company generated profits of $33.6 million. That's a decline from the $37.9 million reported one year earlier. For the first half of this year, the $67.1 million that the company generated was down from the $76 million reported for the first half of 2023.

Author - SEC EDGAR Data

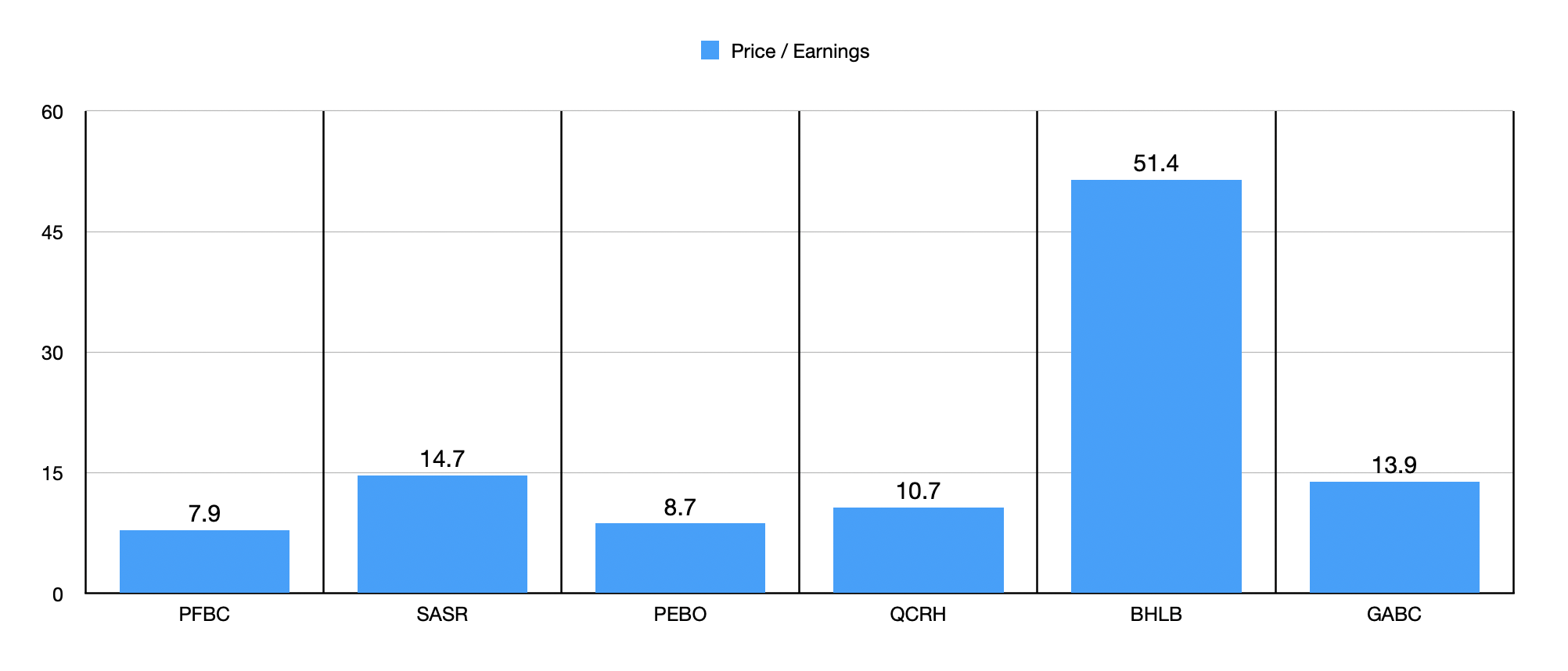

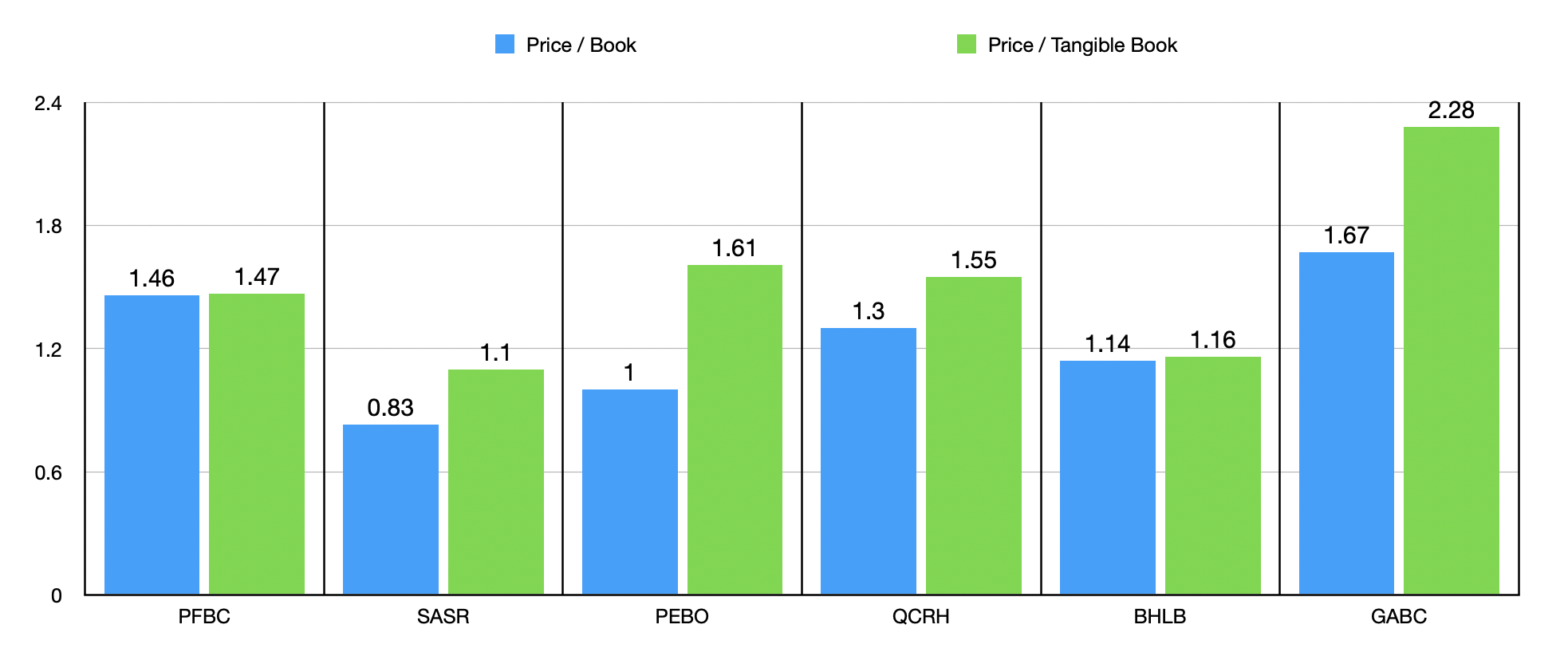

When it comes to valuing the company, the first thing I did was look at its price relative to earnings. I actually annualized the results that we have seen so far for 2024 to get a more conservative reading than if we were to use results from 2023 as a whole. During this, we get a price to earnings multiple of 7.9. In the chart above, I compared Preferred Bank to five similar firms. And of the five, it ended up being the cheapest. Unfortunately, that was not the case on a price to book or price to tangible book basis. In the chart below, you can see exactly what I mean. On a price to book basis, four of the five institutions ended up being cheaper than our target. Fortunately, this drops to only two of the five when using the price to tangible book approach.

Author - SEC EDGAR Data

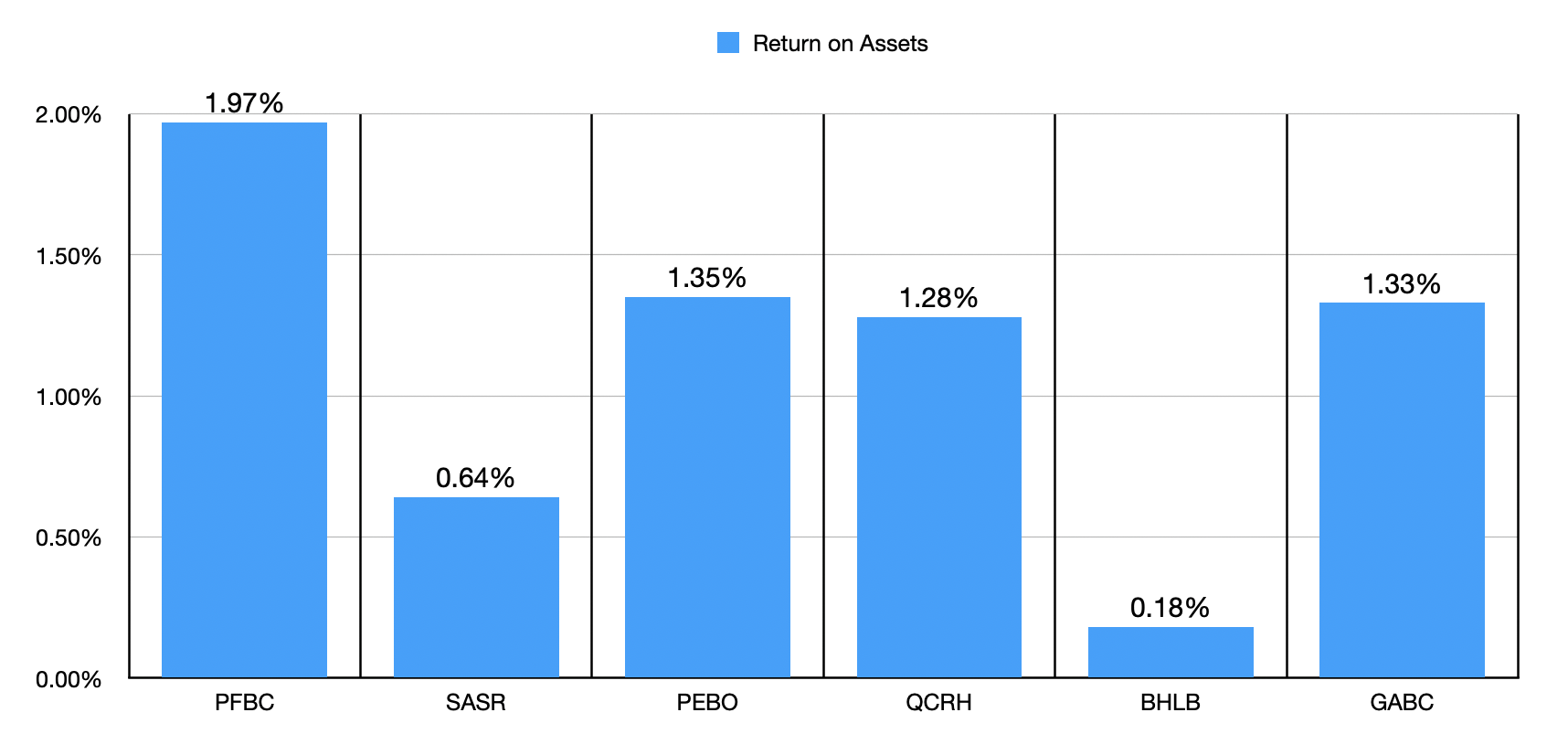

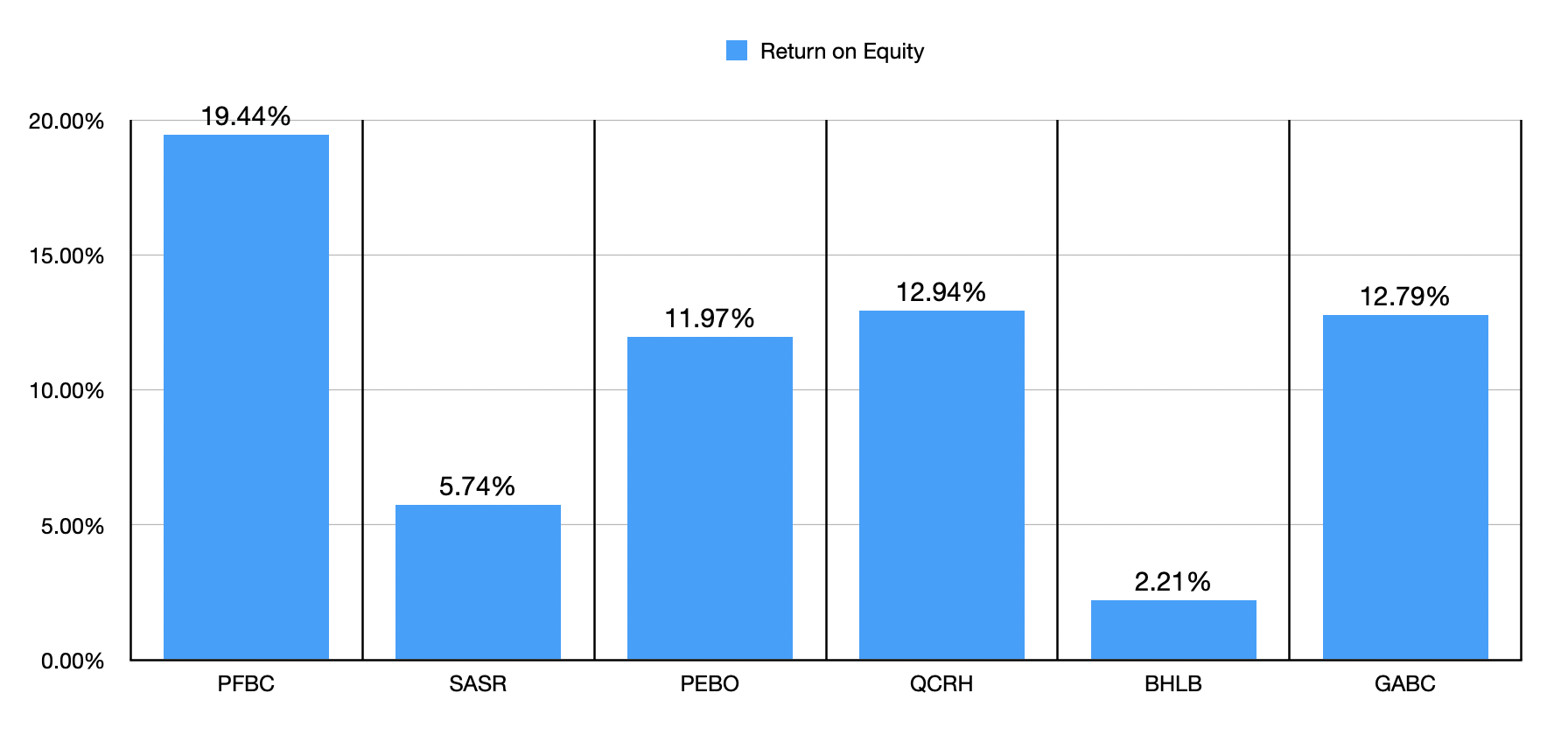

Another thing that we should be paying attention to is asset quality. Normally, asset quality is higher when you are talking about an institution that has a large portion of its revenue coming from non-interest income. But that's not what we see here. With a return on assets of 1.97%, as shown in the first chart below, Preferred Bank is superior to the other five companies I am looking at in this article. The same can be said, looking at the subsequent chart, when it comes to return on equity. Once again, our candidate is the crème de la crème.

Author - SEC EDGAR Data

Author - SEC EDGAR Data

Takeaway

Fundamentally speaking, the picture for Preferred Bank has been quite solid. It is disappointing to see the drop in profits this year. But not everything can be perfect. Debt remains low, while securities and loans follow deposits higher. Shares are cheap on a price to earnings basis and, relative to similar firms, they aren't exactly expensive when it comes to book value. Asset quality is high on both fronts. Add all of this together, and I do think that keeping the company rated a ‘buy’ is sensible.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.