Tenet Healthcare: Strong EPS Growth, But Shares Near FV (Rating Downgrade)

Summary

- Health Care stocks, particularly Eli Lilly, have surged recently, with Tenet Healthcare (THC) also performing well post-COVID, but now near intrinsic value.

- Despite strong earnings and high free cash flow, I downgrade THC from buy to hold due to its fair valuation and potential mean reversion.

- THC's growth in ambulatory surgery centers and shareholder rewards are positives, but risks include high-interest rates, regulatory issues, and a high P/E ratio.

- Technically, THC shows strong momentum but is extended from its 200-day moving average, suggesting possible pullback during historically weak periods.

JHVEPhoto

Health Care stocks have put on a show in recent months. While not in the limelight, the sector mixed with high-growth names and defensive equities has notched all-time highs, driven in large part by massive gains in pharma giant Eli Lilly (LLY). But smaller stocks within the broad sector have also been on the rise as the space has undergone changes post-COVID.

I am downgrading Tenet Healthcare (NYSE:THC) from a buy to a hold, however. The No. 6-ranked out of 1034 members of the Health Care sector has grown earnings substantially in the past few quarters, and shares trade at a fair valuation while its chart is outstanding with high momentum. A strong Q2 beat and raise affirmed a strong fundamental outlook, but I now see the stock near intrinsic value.

The stock has been a stunning winner since my last analysis in May 2023 – that was right before earnings took flight, and now is an ideal time to review where things stand on this Texas-based Health Care stock.

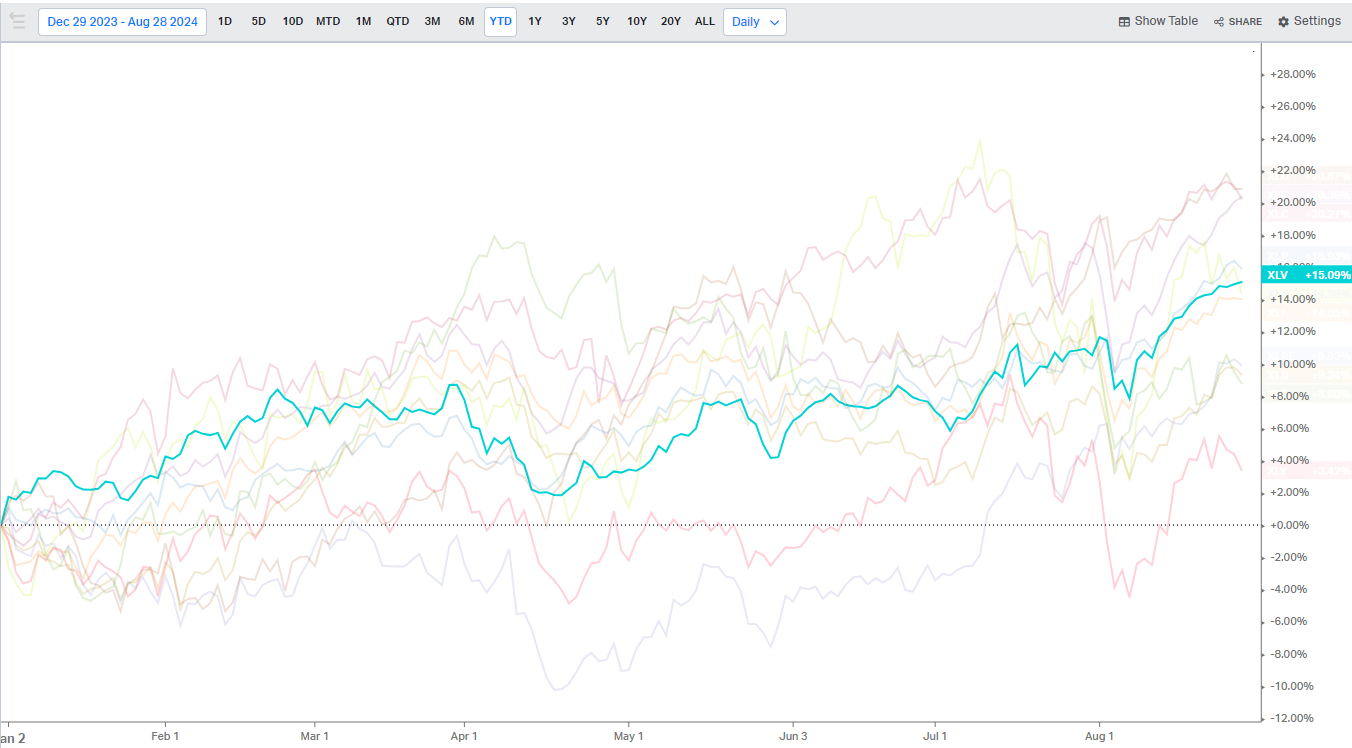

Health Care Sector Hits New Highs

Koyfin Charts

According to Bank of America Global Research, THC provides healthcare services primarily through the operation of general hospitals and related health care facilities. Its hospitals offer acute care services, operating and recovery rooms, and radiology services, among others. Through its subsidiaries, partnerships, and joint ventures, including USPI, THC operates 61 acute care hospitals, 24 short-stay surgical hospitals, about 440 ambulatory surgery centers, and over 100 other outpatient facilities.

Back in July, Tenet reported a very strong set of quarterly numbers. Q2 non-GAAP EPS of $2.31 topped the Wall Street consensus target of $1.91 while revenue of $5.1 billion, up fractionally from year-ago levels, was a modest $100 million beat. The $16 billion market cap Health Care Facilities industry company posted consolidated adjusted EBITDA of $945 million last quarter, a 12% increase from Q2 2023 while Ambulatory Care adjusted EBITDA surged 21% year-over-year to $446 million.

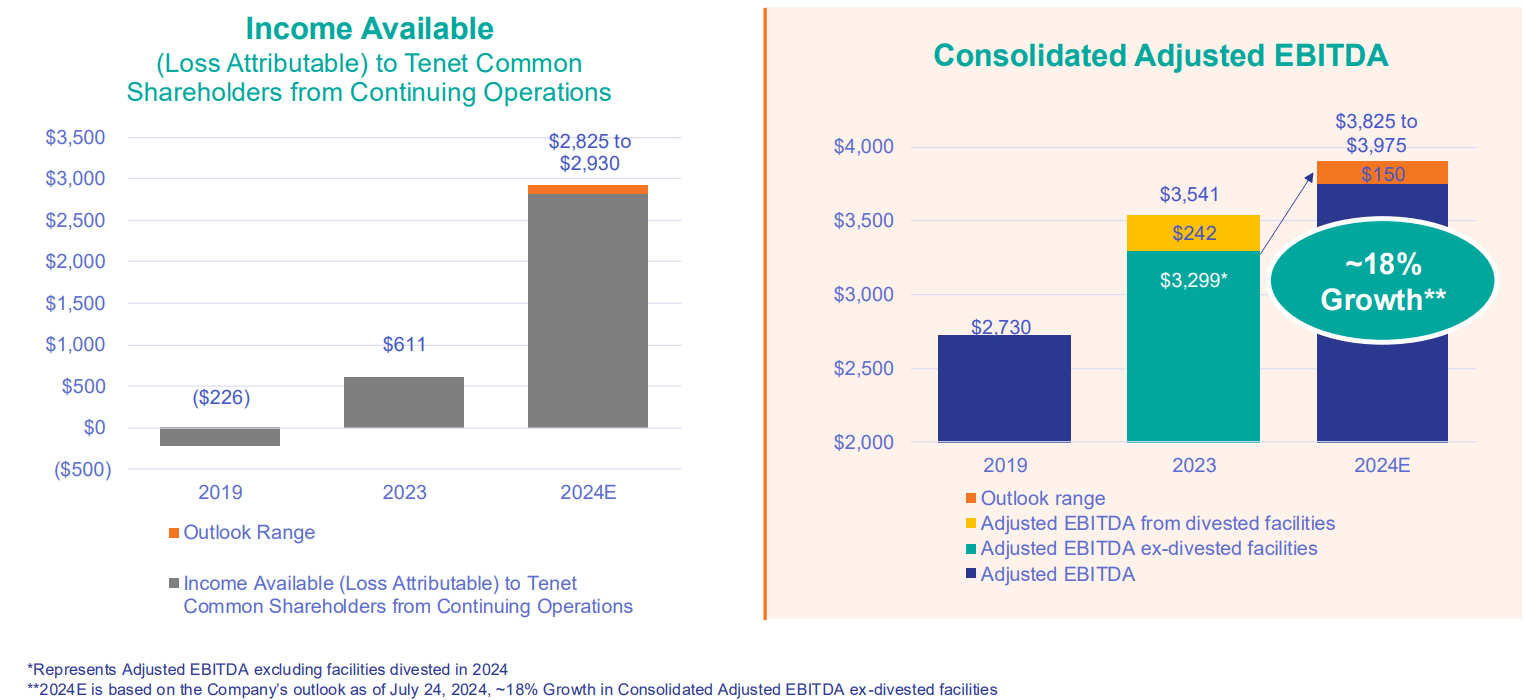

Cash flows from operations rose by nearly $300 million compared to Q2 last year, hitting $1.333 billion over the April through June period, and free cash flow was $948 million for the first half of 2024. Along with high earnings growth, the management team authorized a new $1.5 billion stock buyback plan. Finally, it was an earnings triple play as FY 2024 adjusted EBITDA is now expected to verify in the range of $3.825 billion to $3.975 billion, a material $300 million increase from the previous guidance range.

2024 Financial Outlook

THC IR

The second quarter bottom-line beat was the latest in a series of strong reports – THC has topped estimates in each quarter going back to September 2019. Shares traded higher by 4.8% in the session that followed. Remarkably, the stock has rallied post-earnings in each of the past eight quarters – a very impressive streak as the firm continues to offer upside surprises.

Helping to more than double the stock from 12 months ago are expansions into higher-acuity services that can drive better sales, margins, and profits. Its shift toward ambulatory surgery centers has been a key growth catalyst and helps support the optimistic outlook. Given the high free cash flow, not only is the firm rewarding shareholders through buybacks, but it is also reducing its debt burden, though financial leverage is still to the high side.

Key risks include higher interest rates and a weaker macro situation, which could pressure demand for THC’s services. Adverse regulatory outcomes amid an uncertain political backdrop are also reasons for worry, given the high price-to-earnings valuation compared to THC’s history.

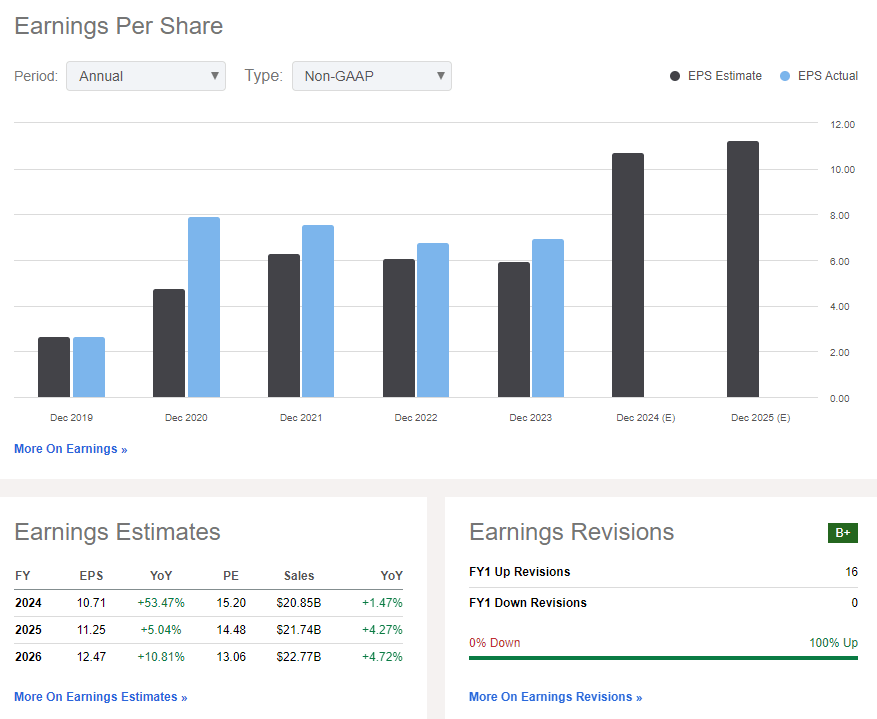

On the earnings outlook, analysts expect big EPS growth this year, more than 50%, while Tenet’s bottom line is seen steadying in the out year. By 2026, though, THC is expected to see double-digit operating EPS growth. All the while, revenues are seen rising at a low to mid-single-digit pace through 2026. But given three consecutive quarters of massive earnings beats, we’ve seen a slew of sell side EPS upgrades.

Tenet Healthcare Earnings & Sales Outlook

Seeking Alpha

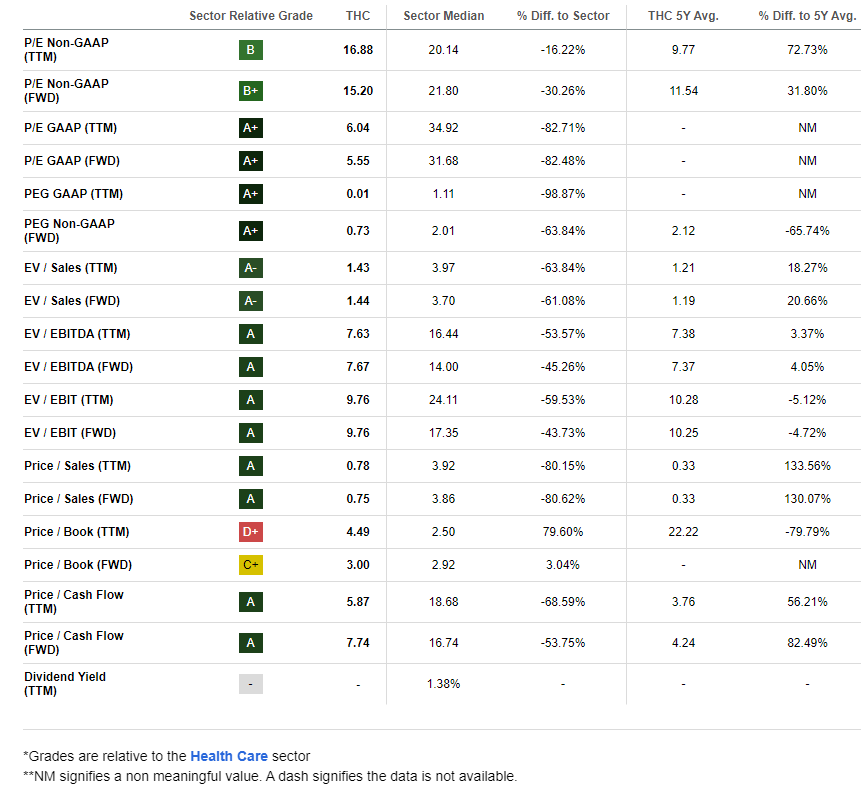

On valuation, THC is not cheap relative to its historical average P/E of 11.5. Now trading above 15x, there’s clearly an upbeat outlook from analysts. If we assume normalized EPS of $11 over the next 12 months and apply a 15x P/E, between its long-term average and the sector median, then shares should trade near $165.

That puts THC close to fair value on a fundamental basis – but there’s more to the story. The company’s free cash flow per share over the past four quarters is now $18.94, resulting in a FCF yield above 11%. Finally, its PEG ratio is ultra-low at just 0.73.

THC: Solid Valuation Metrics, But No longer Cheap on Earnings Relative to Its Historical Average P/E

Seeking Alpha

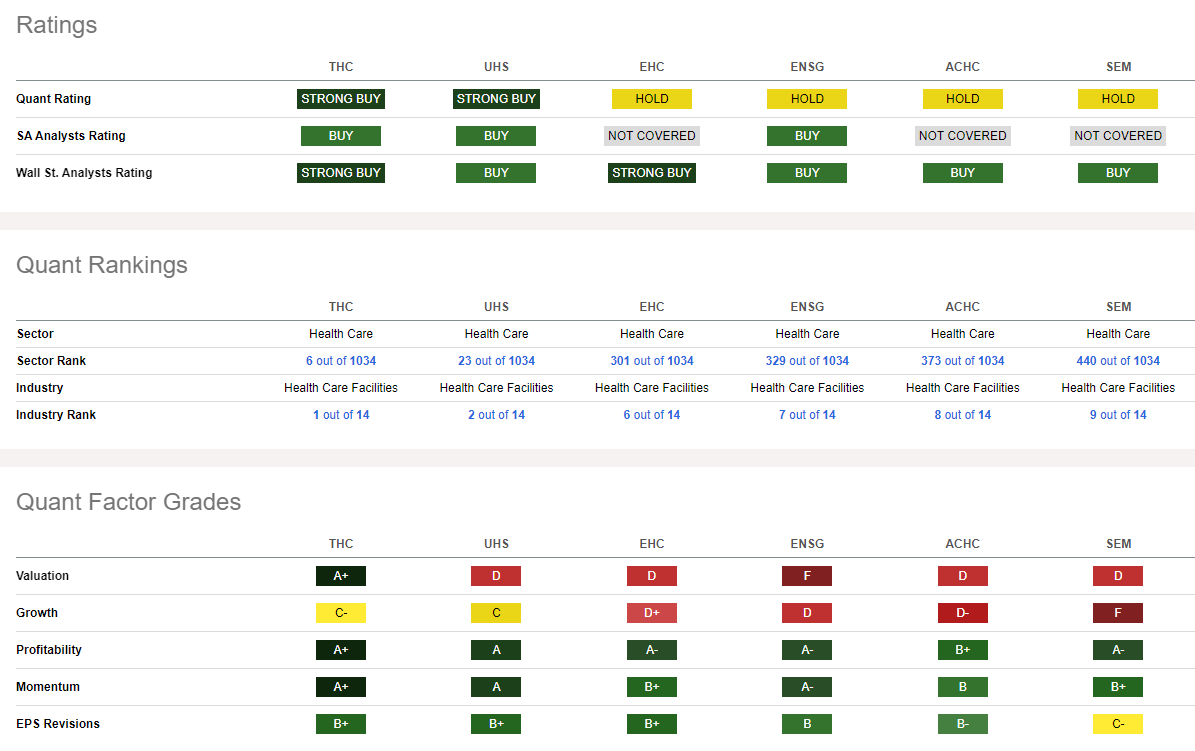

Compared to its peers, THC sports a valuation rating that is best in class, while the growth trajectory is less sanguine, but still in line with many of its competitors.

With a very robust profitability rating and 16 upward EPS revisions in the past 90 days (compared with no downgrades), THC appears as a solid GARP stock in some aspects. Finally, share-price momentum is extremely strong, and I will outline key price levels to monitor on the chart later in the article.

Competitor Analysis

Seeking Alpha

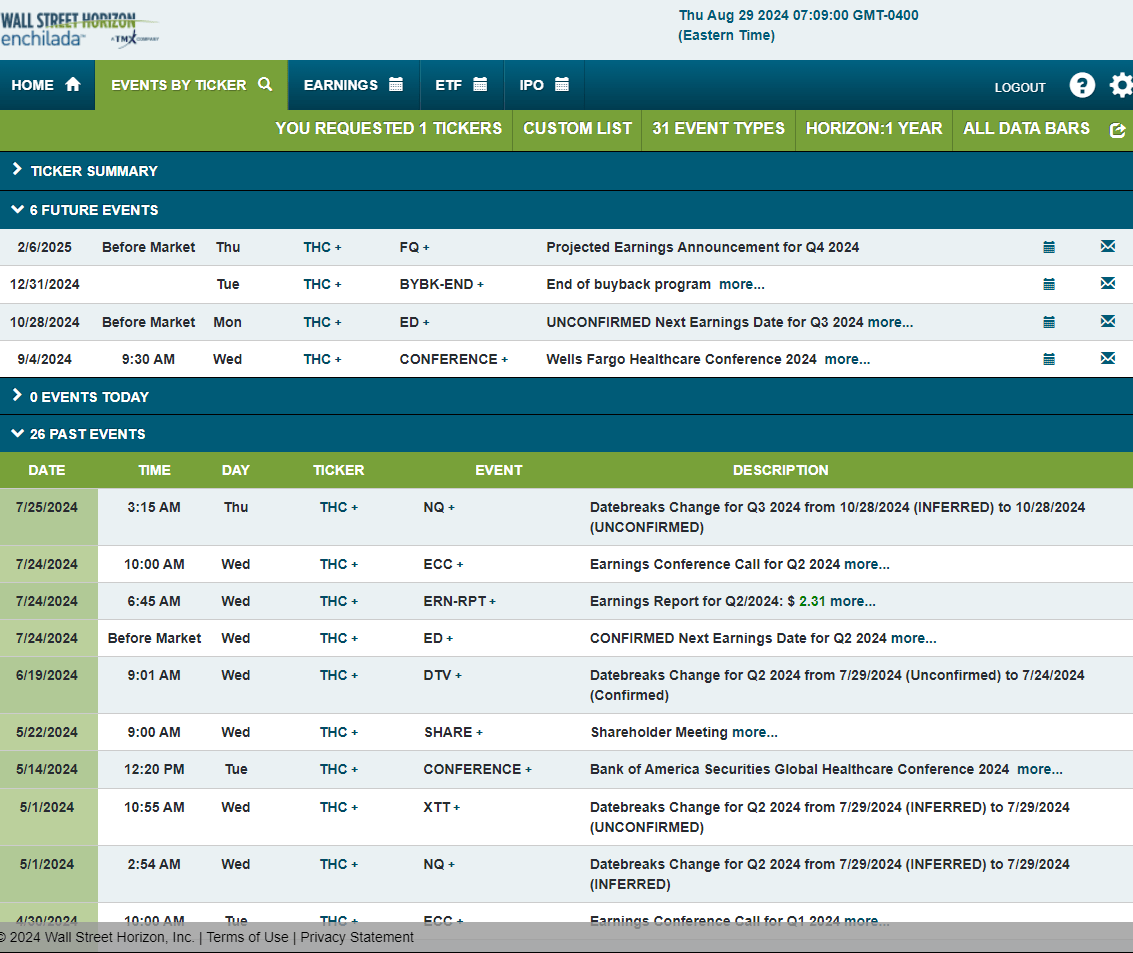

Looking ahead, corporate event data provided by Wall Street Horizon shows an unconfirmed Q3 2024 earnings date of Monday, October 28 BMO. Before that, Tenet’s management team is expected to present at the Wells Fargo Healthcare Conference 2024 from September 4-6. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

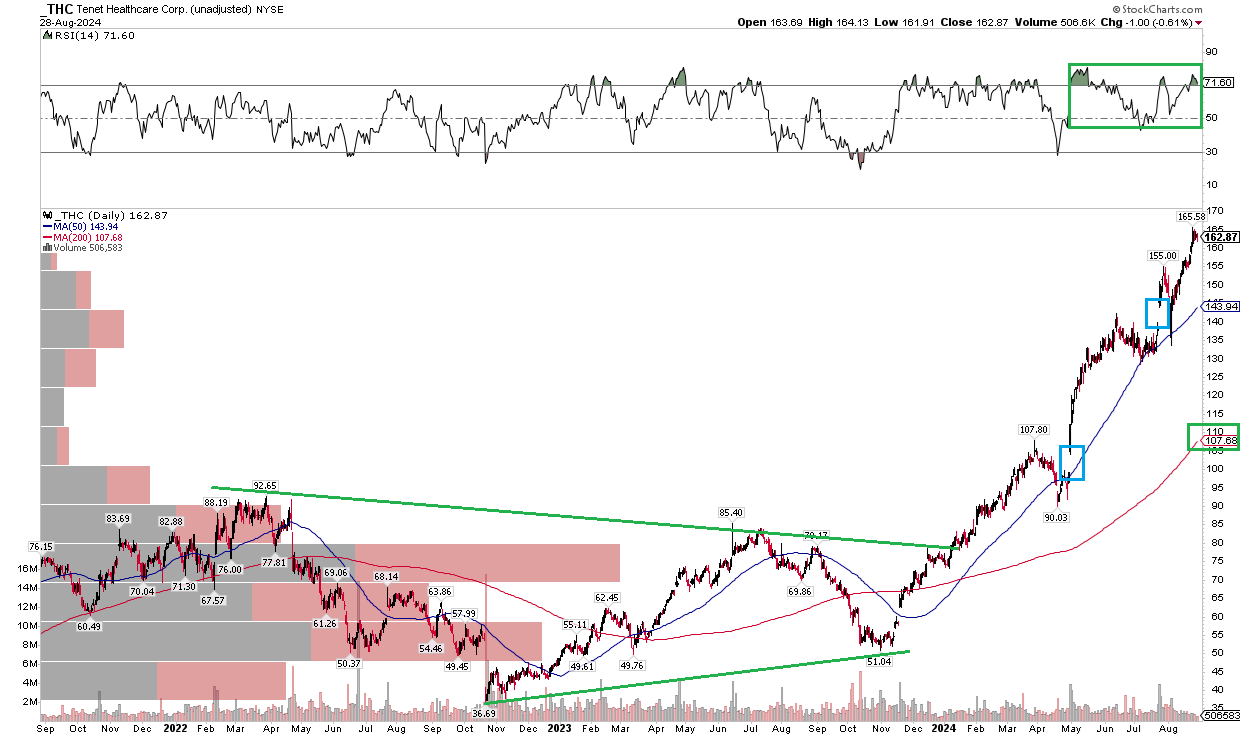

The Technical Take

With shares near fair value and very high free cash flow, THC’s technical chart is impressive. Momentum is important, and so long as the stock is at least reasonably valued, short-term traders may still want to play THC from the long side. Notice in the chart below that shares are up more than threefold from November last year, but the rally has been orderly.

The long-term 200-day moving average is way down at $108, which suggests that a pullback amid mean reversion could certainly come about, but take a look at the RSI indicator at the top of the chart – it has been ranging in a bullish zone between 40 and 80 since May. THC did endure a 15% drawdown in Q2 which dropped the RSI into oversold territory before buyers quickly snapped up the stock.

Also, take a look at the price gap that was successfully filled earlier this month – that helped support the next leg higher. Meanwhile, there’s an old unfilled breakaway gap near $100 that I don’t believe will be filled. While there is no resistance on the upside as THC is at all-time highs, support is seen near $130. Lastly, the August through October period has historically been tough on THC bulls, so we could see the stock pare some gains before year-end.

THC: Bullish Uptrend, Stock Extended From the 200dma

Stockcharts.com

The Bottom Line

I have a hold rating on THC. The valuation is reasonable, but the stock is not cheap as EPS growth slows in 2025. Technically, shares are in great shape but extended from their 200-day moving average, suggesting that we could see some mean reversion during this often weak period of the year.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.