Very Good News For Utilities Stocks

Summary

- Utilities have underperformed the broader market since the beginning of 2023 due to a plethora of factors.

- However, that has begun to reverse and there are several reasons to believe this market reversal will continue.

- We share several attractive ways to gain exposure to this trend.

matdesign24

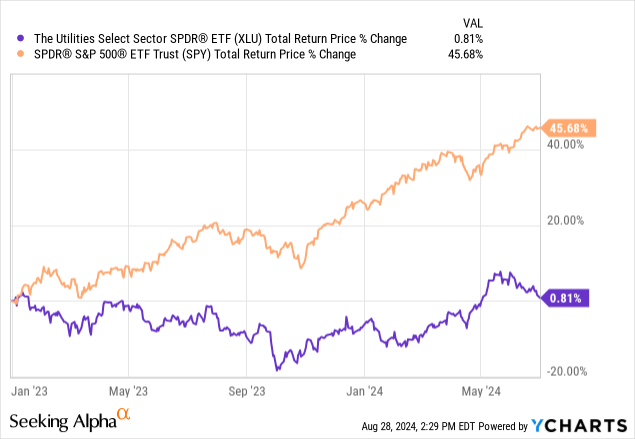

The US economy has proven to be remarkably resilient in the post-COVID era, even as many of its leading trading partners in Europe, China, and Japan have encountered economic challenges. However, with interest rates rising significantly since the start of 2022, and the artificial intelligence boom driving big tech stocks higher, the utility sector has faced the perfect storm. Rising interest rates have made its bond-like cash flows less attractive to investors, while the AI boom has sucked capital away from what has traditionally been viewed as a more boring and defensive sector, like utilities, and toward more speculative, high-growth names in the technology space. As a result, the utility sector has significantly lagged the broader market.

Data by YCharts

Data by YCharts

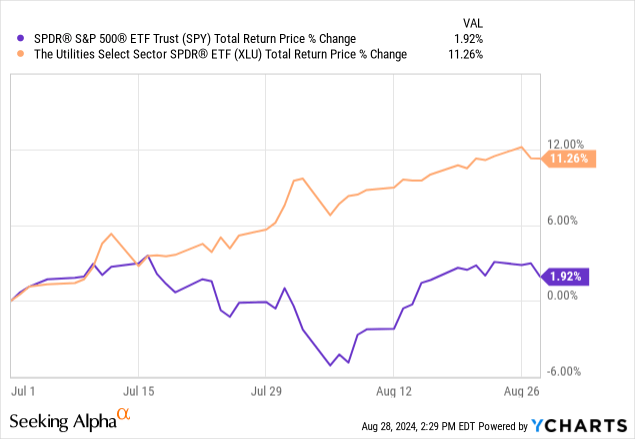

However, in recent weeks and months, the market has undergone a reversal, and utilities are now meaningfully outperforming the broader market.

Data by YCharts

Data by YCharts

Moving forward, there is a growing likelihood that this recent reversal will continue. In this article, we will detail why.

Good News Part 1

The biggest piece of good news for utilities is that interest rates appear likely to be moving lower, with the Federal Reserve now all but certain to cut interest rates in September. The market expects the Fed to continue cutting rates in the months and quarters that follow. This will be a major boon to utilities for two big reasons.

First of all, it will make their bond-like cash flows more attractive on a relative basis, as fixed income will yield less, thereby enabling the market to price utilities at a lower earnings and dividend yield, pushing utility stock prices higher. Additionally, it will mean that the cost of capital for utilities, which tend to be fairly capital-intensive businesses, should decline, as interest rates fall, making debt easier to raise. If their stock prices do indeed move higher, their cost of equity and preferred equity will also decline. This will enable them to raise more capital on more accretive terms to invest in growth opportunities, thereby fueling earnings per share growth and, ultimately, likely dividend growth. It will also ease some of the pressure on their balance sheets that some utilities have felt in recent months and years, as rising interest expense and increased cost of equity made it harder for them to achieve their leverage targets, invest in growth, and sustain their dividends.

Good News Part 2

Another big reason why we think the current macro environment is going to be favorable for utilities is due to the fact that the chances of a recession are rising. While recessions, in general, tend to be negative events for equity markets, utilities are often one of the few exceptions. They tend to meaningfully outperform the broader market during such circumstances because utilities, as regulated or, at the very least, contracted assets and businesses, generate very stable cash flows as they provide essential services to individuals and businesses through all sorts of economic cycles, making them have very low sensitivity to economic downturns. Meanwhile, the broader market, which consists of companies that tend to be more cyclical in nature, tends to underperform during recessionary environments.

While it is not a sure thing that we are heading into a recession, Goldman Sachs recently increased its odds of a recession hitting the US economy from 15% to 25%, due to the fact that unemployment recently surged to 4.3% in July, up 20 basis points from just a month prior. This move meant that the national jobless rate has risen by 0.5 percentage points or more above its 12-month low, which has been a reliable indicator of an economic slowdown throughout many past decades. Additionally, US credit card debt is at record levels, which indicates that the consumer may be increasingly tapped out, and that consumer spending is likely to slow meaningfully moving forward. On top of that, decoupling efforts from China, continued global economic malaise, and increasing trade frictions mean that additional pressures could be put on the economy, further accelerating the slowdown.

This should further drive outperformance for utilities. So when you combine the fact that interest rates are likely going to be falling and the economy might be entering a period of slow to no growth, or even a decline in GDP, utilities appear poised to outperform the broader market for the foreseeable future.

Investor Takeaway: How To Invest In Utilities

With that in mind, here are two ways to play the likely continued utilities bull market right now. Outside of low-cost ETFs like the Utilities Select Sector SPDR Fund (XLU), one option is the Reaves Utility Income Fund (UTG).

The reason we like UTG is because it currently trades roughly in line with its net asset value and its 52-week average, so it is not overvalued despite strong tailwinds behind the sector. It offers a distribution rate of about 7.6%, paid out on a monthly basis. Its leverage is at a very reasonable level of just 18.32%, so it is not overly sensitive to a market crash, and its expense ratio is 0.93%, which, while certainly not low, is quite reasonable for an actively managed, leveraged CEF. For investors who want a higher yield while still maintaining diversification in the utility space, UTG is a good option.

For investors who want to pick individual utilities and process it, and enjoy the total return outperformance that could come with it, while also wanting a higher yield than the 3.91% that XLU offers, we think that Brookfield Infrastructure Partners (BIP)(BIPC) with its 5.1% dividend yield and mid-to-high single-digit expected annualized distribution per unit growth rate and double-digit projected annualized FFO per unit CAGR, make it a compelling opportunity.

While it is not a pure utility, it does have significant exposure to utilities as well as other utility-like businesses like midstream, which enjoys regulated and long-term contract assets, transportation, which also generates utility-like long-term contracted or regulated cash flows, as well as a rapidly growing data center business that also has long-term contracted cash flows and strong growth dynamics. Additionally, it has a very strong BBB+ credit rating and excellent management from its parent Brookfield (BAM)(BN).

By allocating an increasing amount of funds to the utility space, investors can make their portfolio more defensive while also increasing dividend yields and positioning themselves to outperform in a period where interest rates are likely to continue falling and the economy is likely to slow down meaningfully.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.