Qorvo: AI-Related Gains With Apple, Cost Optimization, And Potential Fed Easing

Summary

- Qorvo's stock is a buy due to expected Federal Reserve rate cuts and Apple's AI-capable devices, despite recent dips and competition.

- The company is optimizing manufacturing, transitioning to larger wafers, managing inventory, and improving product mix to enhance gross margins.

- China-related risks and competition from Broadcom and Qualcomm exist, but Qorvo's segmentation strategy and outsourcing improve flexibility and gross margins.

- Valued better due to improved cash flow, strategic acquisitions, and AI-driven smartphone market growth, with a potential target price of $129.

Eduard Lysenko

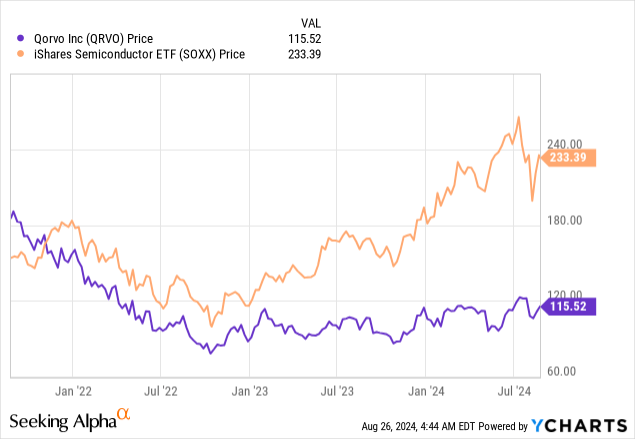

Qorvo's (NASDAQ:QRVO) share price has dipped from mid-July alongside the iShares Semiconductor ETF (SOXX) as shown in the chart below. However, unlike the ETF which benefited from its artificial intelligence holdings, the stock has not recouped the losses suffered after the Federal Reserve aggressively hiked interest rates in 2022.

Data by YCharts

Data by YCharts

This could change as rates are highly likely to be cut next month and, Apple (AAPL), Qorvo's largest end customer, launches its AI-driven iPhone, a move started earlier by South Korean electronics giant Samsung (OTCPK:SSNLF) for its smartphone models.

In such a context, this thesis aims to show the stock is a buy, but first, by going through the first quarter results for fiscal 2025 (FQ1), I emphasize how it is optimizing manufacturing to improve gross margins, in a way that will positively impact its cash flow too.

Focusing on Gross Margins

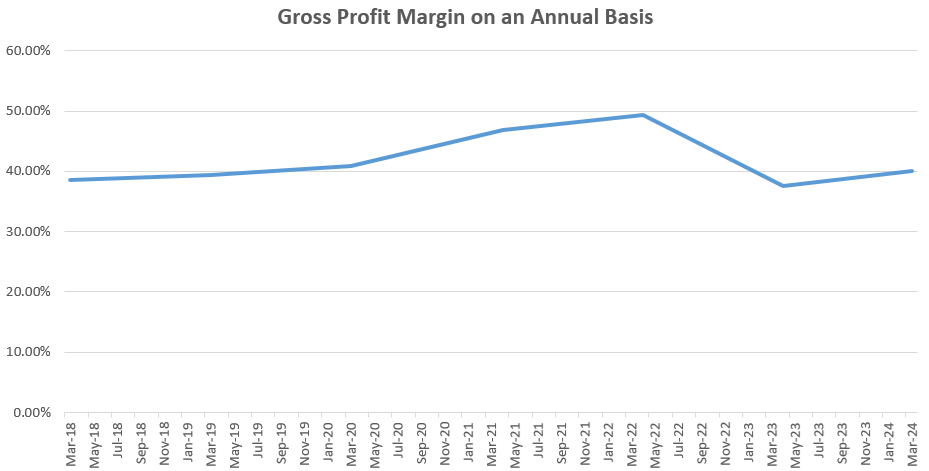

The revenues of $887 million represented a 36% YoY increase, while gross profits improved only by 34%. Looking at the broader picture in the chart below, 47% and 49% margins for fiscal years 2021 and 2022 respectively slid to 37.6% in fiscal 2023 before recovering to slightly above 40% in fiscal 2024 which ended in March.

The chart is drawn using Income Statement data from (seekingalpha.com)

This is low compared to the 47% achieved by industry peer, ON Semiconductor (ON) for its latest fiscal year. Now, similarly to Qorvo, it is not only a fabless company but also has manufacturing activities and, by introducing advanced production techniques and leveraging a global production network, it has optimized the efficiency of its processes.

To catch up, Qorvo has been progressing on several fronts, like reducing operational inefficiencies associated with manufacturing smaller wafer diameters and transitioning to larger formats, culminating with the migration to 8-inch BAW (Bulk Acoustic Wave) in FQ1. Second, is working on inventories to closely align shipments with variations in demand and ensure less cash is locked in unused items. Third, the product mix is being reoriented to favor higher-margin products and eliminate those that result in reduced factory utilization. Fourth, business processes are being realigned using software and AI to become nimbler and more competitive.

As a result of these actions, gross margins are expected to improve substantially in September, with the June quarter (FQ1) expected to mark the lowest point for this year. Looking ahead, margins in the mid-40s are expected for fiscal year 25, prompting analysts to upgrade their consensus EPS estimate from $6.10 to $6.21.

China-Related Risks and Competition

However, this would still constitute a 0.15% YoY decrease, and one of the reasons for higher gross margins not reverberating on the bottom line is higher operating expenses. This includes digital transformation-related and R&D costs, further detailed below.

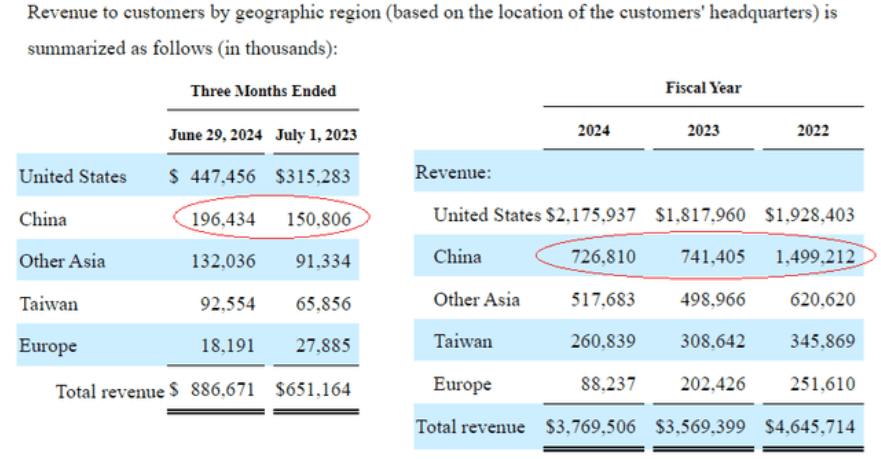

Now, these higher expenses could be offset by the revenue mix if the company's second-largest market, China, continues to rebound.

Thus, sales from the East Asian country increased by nearly 30% YoY or from $151 million to $196 million during FQ1 compared to a decline for fiscal 2024 as shown below with Qorvo managing to expand its customer engagements to include four 5G Android OEMs (original equipment manufacturers) with the associated shipments starting this year.

Well, this suggests that unless the Chinese recovery stalls, demand is likely to be sustained, and checking further, the management remains "very cautious" about the economic turnaround and expects revenue from that country to be flat quarter over quarter.

SEC Filings (seekingalpha.com)

To this end, with China accounting for a sizeable 19% of its revenues in fiscal 2024, this dependence could also prove detrimental to sales in case 60% tariffs are imposed on Chinese goods after the November U.S. elections and these trigger a tit-for-tat reaction from Beijing thereby making the company's products dearer.

Pursuing further, Qorvo also competes with giants like Broadcom (AVGO) and Qualcomm (QCOM) which are also IDMs (integrated device manufacturers) in the sense that they manufacture some of their connectivity chips as these have become increasingly commoditized or more indistinguishable from one another resulting in increased price-based competition.

As a solution to this issue, Qorvo came up with a segmentation strategy whereby it classifies the dosage of RF components in smartphones into three categories consisting of low, medium, and high content silicon, all depending on cost sensitivity, mid-tier, and high-end markets respectively. This strategy not only helps it adapt faster to the requirements of different customers but also differentiates its products from bigger competitors by offering better pricing flexibility.

Talking profitability, this also means that certain aspects of the manufacturing process for the low-cost chip can be outsourced to OSATs (outsourced semiconductor assembly and test) in a way to boost gross margins.

Valuing the Stock based on the Management of Cash

At the same time, such a strategy also allows it to respond faster to customer demand for higher frequency product shipments by rapidly scaling production without increasing Capex, namely for post-fabrication tasks. Such optimization of the company's manufacturing strategy may have prompted its divestment from its Beijing assembly and test assembly in December last year.

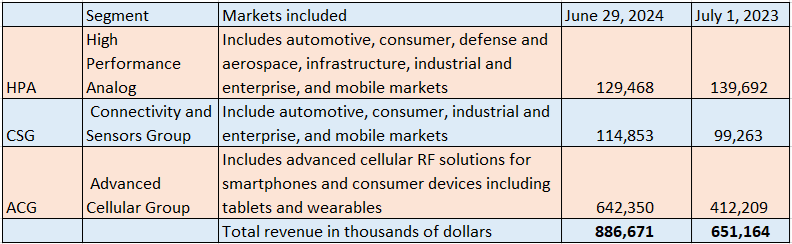

Furthermore, by reducing factory-based investments, it can also increment its FCF margin, a metric where Qorvo already exceeds the median for the IT sector by more than 80%, provided it generates more cash from operations. This is entirely possible firstly, after improving time-to-market by outsourcing part of production activities to OSATs thereby ensuring less cash is locked in the manufacturing process, and second, by allocating the savings made to innovation (R&D), and acquisitions. Thus, it acquired Anokiwave to be better positioned in Defense and Aerospace and 5G Infrastructure which forms part of the HPA or High Performance Analog as shown below.

Table prepared using data from (seekingalpha.com)

This signifies it deserves to be valued better, especially since its forward price to cash flow of 14.26x is underpriced relative to the sector median by nearly 36%.

However, incrementing the current share price of $115.5 by 36% would mean a target of $157, or $28 above its mid-July peak of $129. The problem with such a high target is it would ignore China-related risks. Here, I have in mind the management's cautious stance without forgetting that sales for FQ1 represented a sequential decline which could be due to mixed signals. Moreover, with relatively high product development costs and $10 million earmarked for the ongoing digital transformation program, operating expenses should continue to be on the high side with the EPS expectation of $1.85 (midpoint) for FQ2 representing a 22.7% drop from the same period last year.

Thus, $129, which represents a 13.4% upside from the current share price of $113.77 is a fair target, one that could also be helped by Apple-related sales positively impacting the cash flow, and in this connection, the stock gained about 3.5% on July 10 after news about more iPhone shipments.

Factoring A Rate Cut and Additional Design Wins

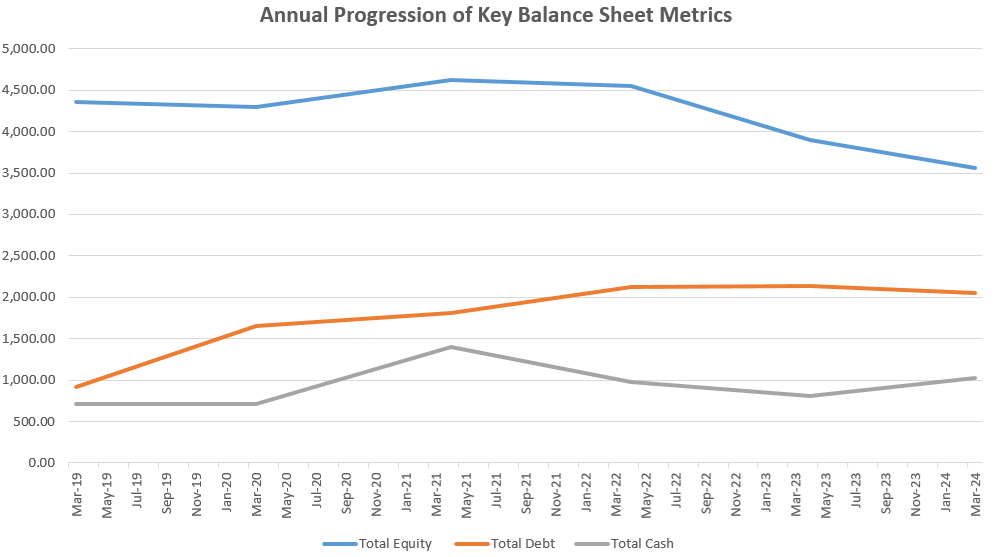

There is also a high probability of monetary conditions easing in Qorvo's biggest market, where recession risks have receded. Now, one of the reasons the company was hit hard in 2022 (as per the introductory chart) if its debt was on the rise while cash on hand was trending lower. Two years later, progress has been made on both metrics while total equity is on a downtrend indicating less issuance. Therefore, it is well-positioned to benefit from a more dovish Fed.

The chart was built using data from (seekingalpha.com)

At the same time, Qorvo has enjoyed more design wins for its 5G and Ultra-wideband for mobile, radar systems, and satellite communications in "Defense and Aerospace" together with chips that support the latest generation or MIMO (Multiple Input, Multiple Output) base stations for "Infrastructure and Connectivity". Also, more interest in V2X or Vehicles to Everything systems in China paves the way for the adoption of its products for years to come. Hence, analysts have revised its revenue expectations for fiscal 2025 from $3.89 billion to $3.95 billion, which would represent a 4.77% YoY increase.

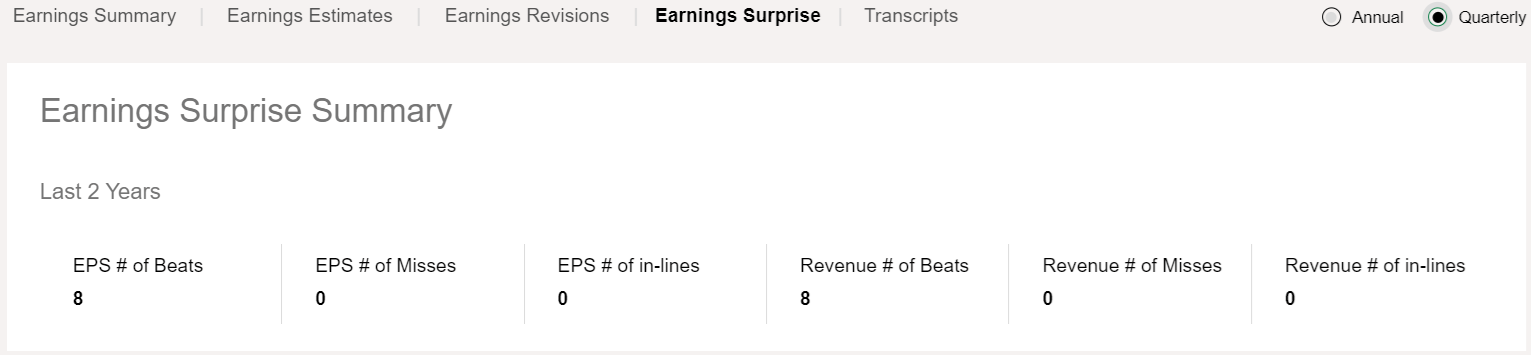

However, this target could be exceeded, resulting in the company beating analysts' consensus estimates as has been the case eight times out of eight during the last two years, as shown below.

seekingalpha.com

Better performance could also be driven by Gen AI.

Potential AI Gains with Apple's iPhone

In this context, 46% of Qorvo's sales came from Apple in fiscal 2024 and 12% from Samsung, and both are transforming their smartphones to be AI-capable. First, the South Korean giant integrated Google's Gen AI into its Galaxy devices in January this year, helping the company continue dominating the Android market. This has already benefited Qorvo when Samsung released the S24, where it obtained "excellent dollar content" per phone.

Apple was next after it partnered with Open AI in June to empower its iPhone, macOS, and iPadOS models with Gen AI and Qorvo could benefit by providing higher silicon content to its latest-generation and AI-capable phones. In this respect, as a trusted Apple supplier, it is capable of benefiting from more sales by driving more dollar content into the iPhone in a Gen AI-driven smartphone market expected to grow by a CAGR growth of 78.4% from 2024 to 2028.

To this end, the timing of an additional amount of product development spending in FQ2 could be explained by testing activities for its RF chips in the context of new iPhone 16 models, which will be launched on September 9. However, there are volatility risks related to this launch, especially in case the market perceives that it is taking more time than expected for consumers to adopt the AI-driven phone.

Still, OpenAI's ChatGPT was found to be a better solution than Google's Gemini when it comes to providing a user-friendly interface for chatting, querying, troubleshooting, and creating multimodal (text, image and video formats) content which means an increased chance for Apple to sell more iPhones than its competitor. Qorvo's advantage is it sells to both and could benefit as competition between the two heats up.

Finally, the stock may become volatile as the election nears especially in case the rhetoric around China becomes harsher, but to this end, Qorvo's cost optimization strategy should enable it to better absorb reduced pricing in case its products are negatively impacted by higher tariffs as a result of escalating geopolitical tensions.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.