Dollar General: Oh Boy...

Summary

- Dollar General's recent earnings report shows weak growth and declining profits, leading to a sharp drop in its stock and concerns over consumer health.

- Rising competition from Walmart, Aldi, and ultra-low-cost brands like Temu further challenges DG's business model, especially in non-food categories.

- While the stock is down, risks remain high. I believe DG's landlords offer safer returns in this tough market, with more stability and income potential.

jetcityimage

Introduction

It's time to talk about Dollar General Corporation (NYSE:DG). The discount retailer just released its 2Q24 earnings, causing its stock price to drop to a new multi-year low.

While I am writing this, the company has lost roughly 30% of its market cap as it made crystal clear it was not satisfied with its financial numbers. Not only is this bad news for the company, but it also tells us a lot about the consumer.

Data by YCharts

Data by YCharts

On top of that, assessing Dollar General is important for many landlords because the company is one of the most desired tenants in the retail space.

Most major net lease REITs have at least some exposure to Dollar General, as the company has aggressively expanded in the past few decades.

Hence, in my most recent article, written on May 28, I discussed the strategy of owning both Dollar General shares and shares in some of its major landlords.

I used the example below, which shows a DG property in Missouri with a cap rate of 6.6%. For many, this is highly attractive because it offers decent income provided by a tenant with a great reputation.

LoopNet

Hence, the company's poor earnings warrant a closer look, as this impacts the company and landlords and because it tells us a lot about the state of the consumer.

So, let's dive into the details!

What Just Happened? Why Is It Important? And Why Does It Matter?

In the second quarter ending August 2, America's largest discount retailer reported net sales of $10.2 billion. That's 4.2% higher compared to the prior-year quarter.

That's not so bad.

The problem is that adjusted for new stores, the company's sales were up just 0.5% - that's the organic, same-store sales growth rate.

When including operating expenses, it gets worse, as the company reported a 20.6% decline in operating profit to just $550 million. Diluted earnings per share were down 20.2%.

Unfortunately, the company's comments did not instill confidence. This is what the company said (emphasis added):

"We made important progress on our Back to Basics plan in the second quarter," said Todd Vasos, Dollar General's chief executive officer. "However, despite advancing several of our operational goals and driving positive traffic growth, we are not satisfied with our financial results, including top line results below our expectations for the quarter." - Dollar General

As expected, the company commented on the state of the consumer as well. Needless to say, I added emphasis again:

"While we believe the softer sales trends are partially attributable to a core customer who feels financially constrained, we know the importance of controlling what we can control. With the evolving retail and consumer landscape in mind, we are taking decisive action to further enhance our value and convenience offering, as well as the in-store experience for our associates and customers." - Dollar General

Since 2021, inflation has been an issue. Although inflation rates have come down in most major Western nations, inflation is still a big issue.

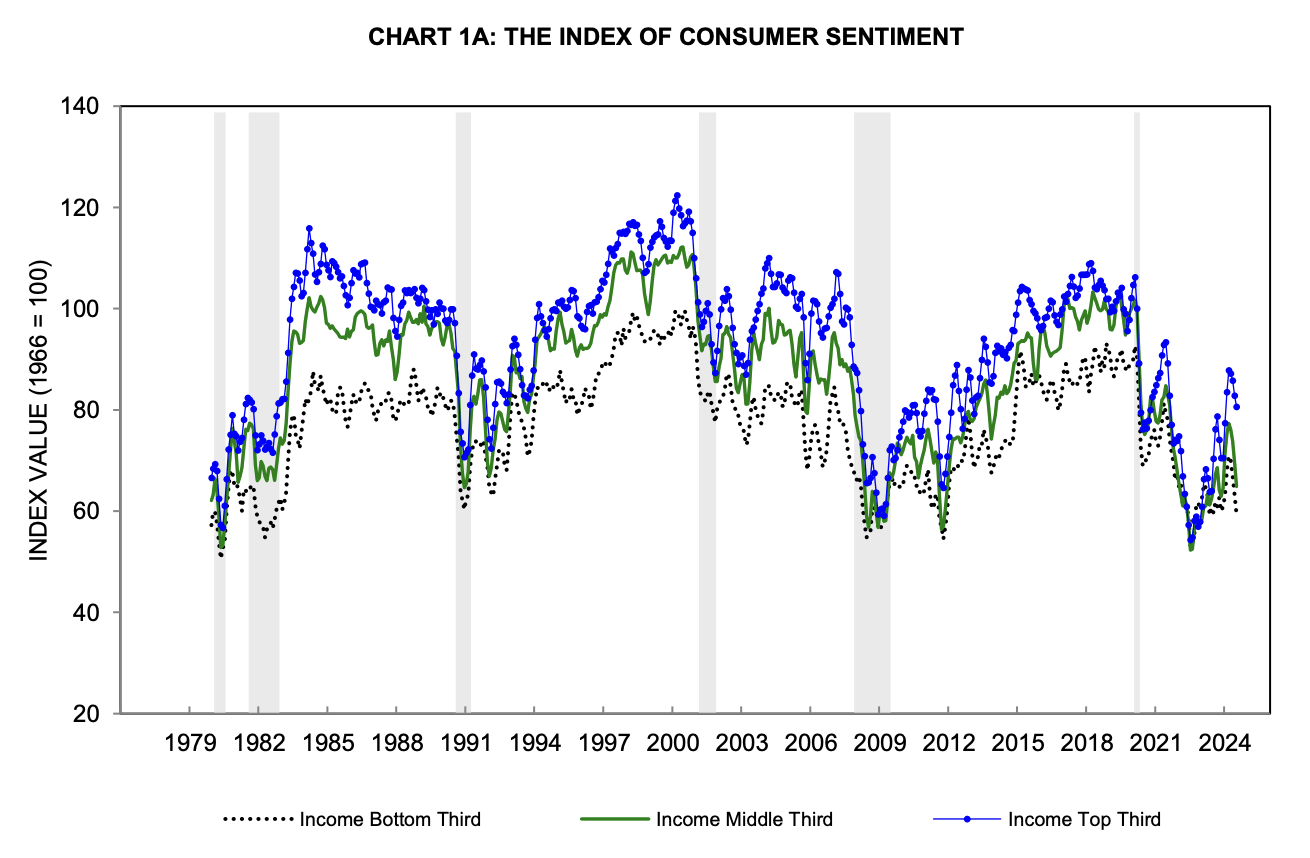

As we can see below, the University of Michigan finds that sentiment for the poorest third of Americans is at levels we saw during the bottom of the Great Financial Crisis. Only the richest third is doing "fine," although all consumers have become more downbeat in recent months - despite lower inflation!

University of Michigan

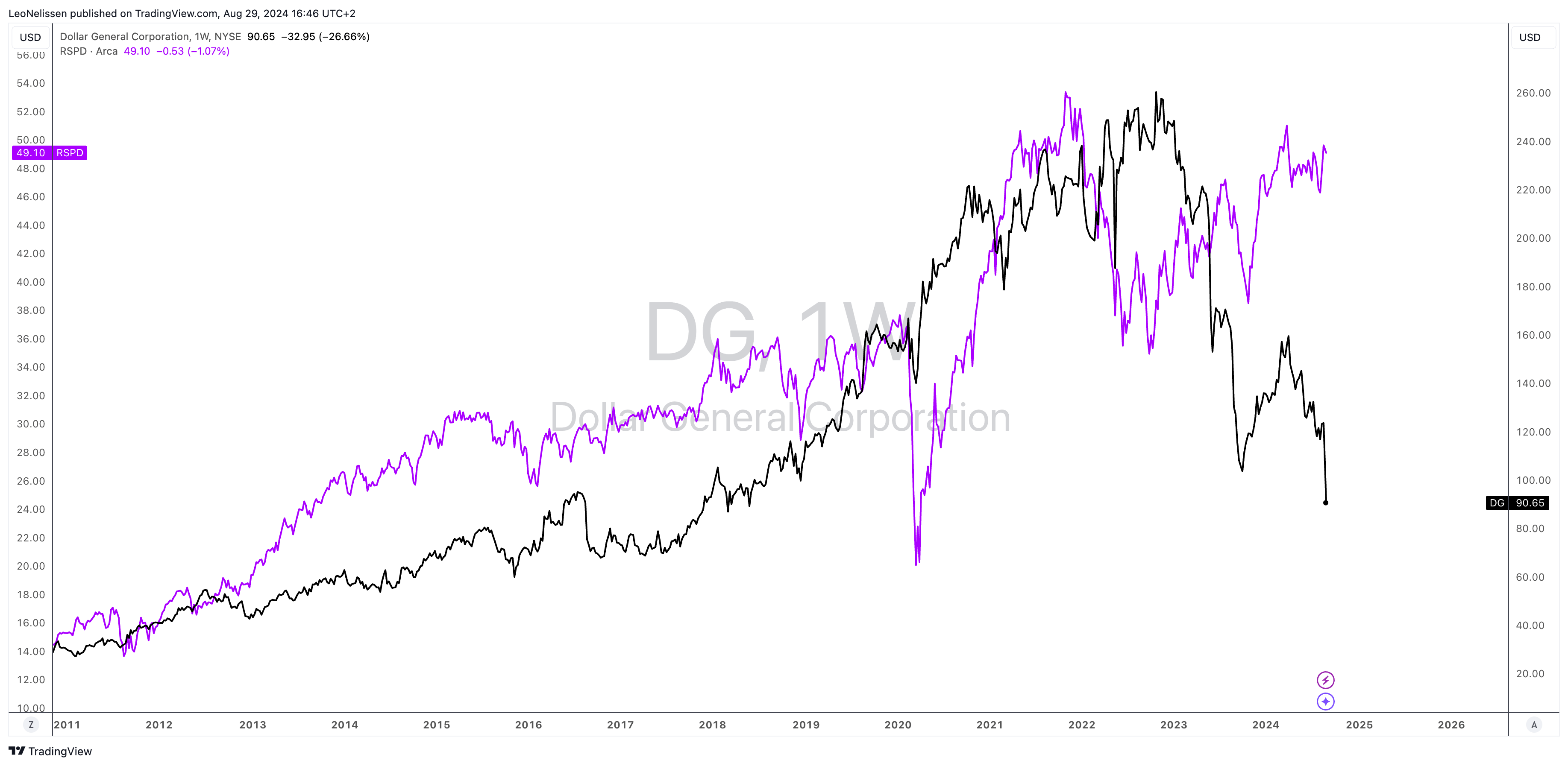

In general, this does not bode well for consumer stocks. The chart below compares Dollar General to the Invesco S&P 500® Equal Weight Consumer Discretionary ETF (RSPD). For both, it was easy sailing until 2021. Since then, cracks have started to appear.

Today's Dollar General news made it so much worse.

TradingView (DG, RSPD)

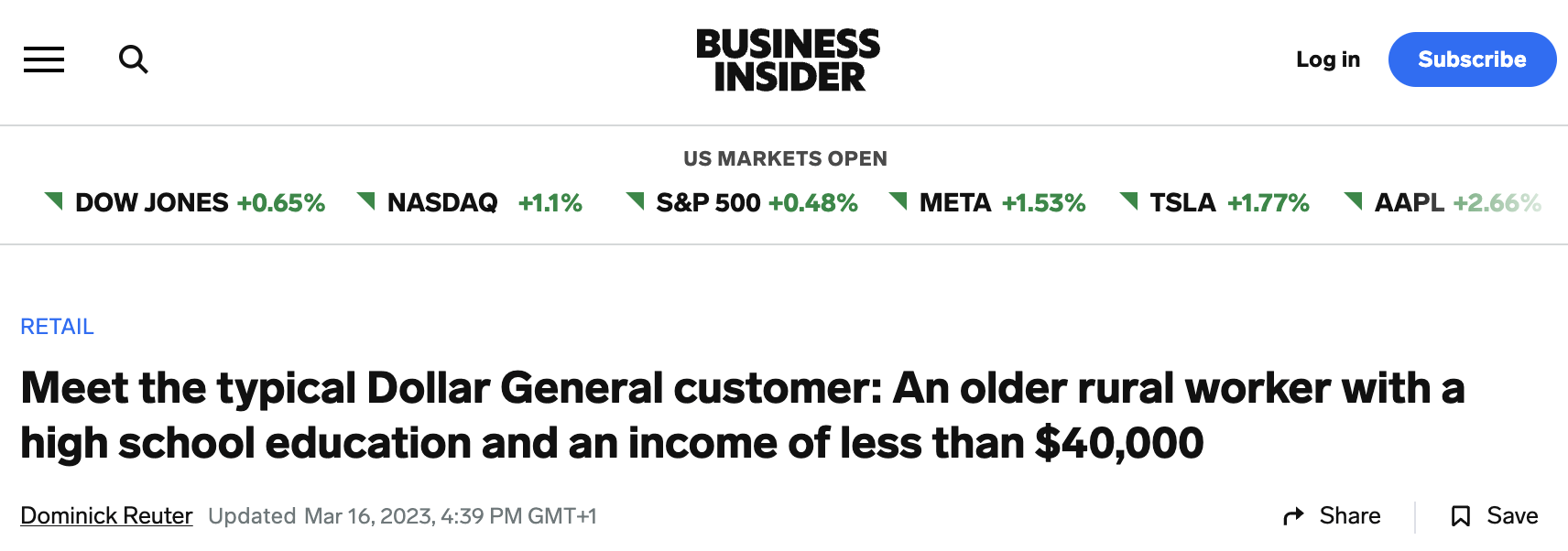

With that said, it makes sense that the company reported a weakening core consumer. After all, its core consumer is an older rural worker with a high school education and an income of less than $40,000.

Business Insider

These people are in deep trouble.

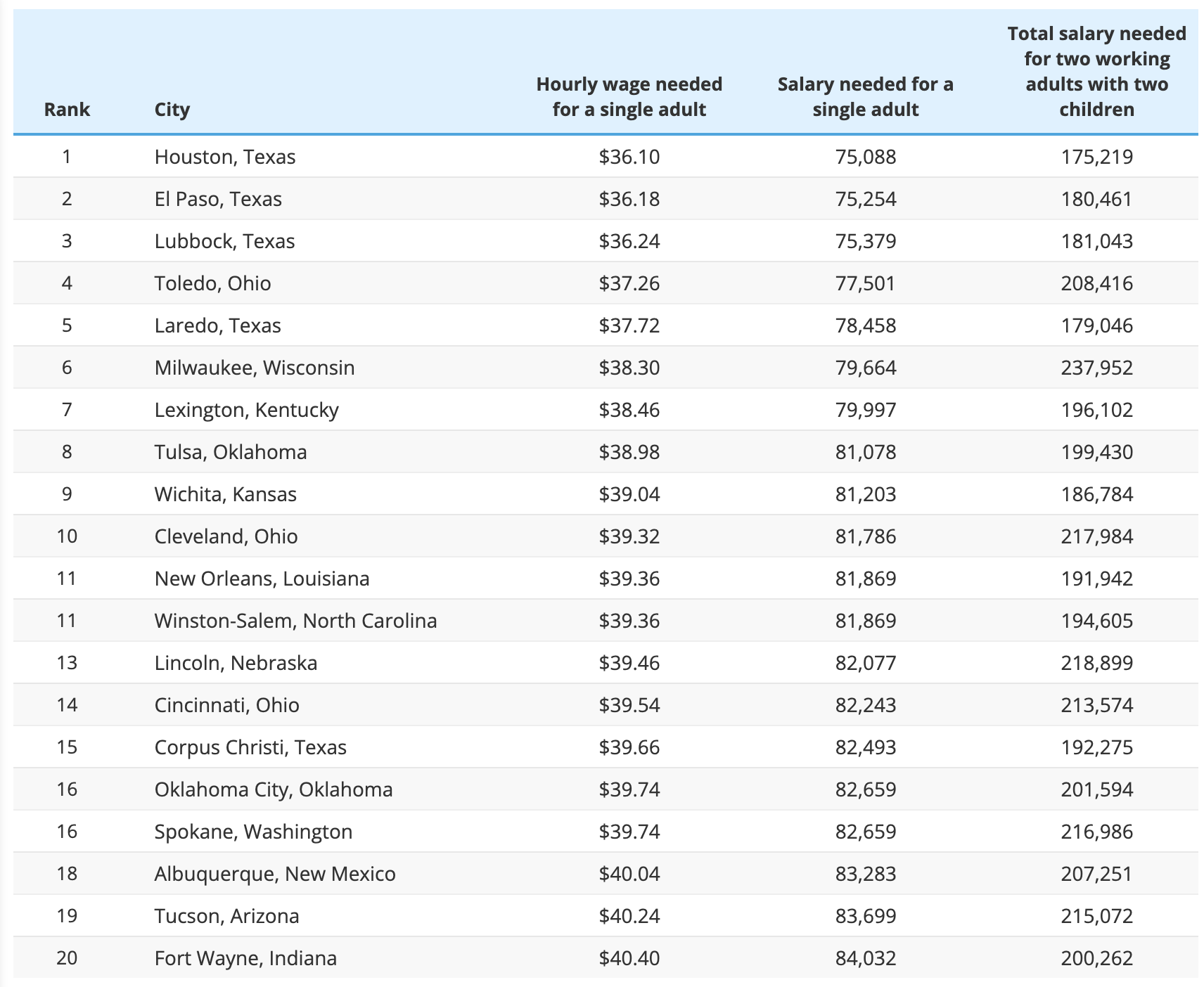

Even in the "cheapest" cities to live comfortably (according to SmartAsset), single adults need to make at least $75,000 per year.

SmartAsset

Based on this context, generally speaking, dollar stores benefit from tough economic environments, as it increases their addressable market. After all, when "everyone" is doing fine, higher-cost retailers become more attractive to investors.

This is what CNN wrote in 2022 when inflation started to bite:

CNN Business

According to the article:

"The highest trade-in that we've seen and the most robust has actually been between the $75,000 and $100,000 group," Vasos said at a retail conference Wednesday. Some of these customers first shopped at Dollar General earlier in the pandemic and have now returned, he added.

Dollar General has been a lifeline for lower-income shoppers, particularly in rural areas with few other retail options. The company says its "core customer" makes under $40,000 a year. - CNN (2022)

Unfortunately for Dollar General, this tailwind was not strong enough to keep its earnings from cratering.

To make matters worse, there are two new headwinds.

- According to Bloomberg, competition from companies like Walmart Inc. (WMT) and Aldi is heating up. Aldi has always been a low-cost store. As the German company is expanding in America, it is taking market share away from Dollar General in certain areas. When adding that Walmart is increasingly offering low-price items, consumers with low budgets have a lot more opportunities to pick from.

- Super-low-cost producers in China are hurting Dollar General's non-food items.

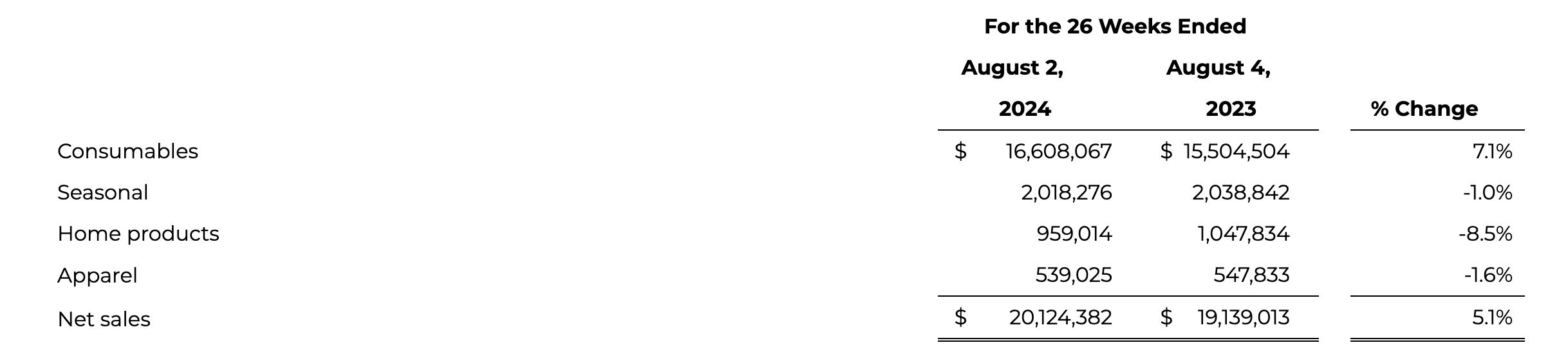

In the second quarter, the company did very well in the consumables segment, where sales were up 7.1%. This makes sense, as the increasing focus on food items has paid off, thanks to high inflation. However, all other segments were under much more pressure. This is likely due to Chinese companies like Temu who ship very cheap non-consumable products to the U.S. and Europe. This is a big issue for companies like Dollar General, which cannot compete with that, as its business model is built for different goals.

Dollar General

This also explains why Amazon.com, Inc. (AMZN) decided to directly compete with Temu and Shein by building its own low-cost apparel, home goods, and general retail storefront.

Dollar General cannot easily make these changes, as its business model is based on expanding its physical footprint to get closer to lower-income customers in rural areas.

While I believe Dollar General is a critical part of many smaller towns and an important source of supplies for lower-income families, it simply does not have the capabilities to compete with new threats - at least not anytime soon.

This is visible in its guidance.

What's Next?

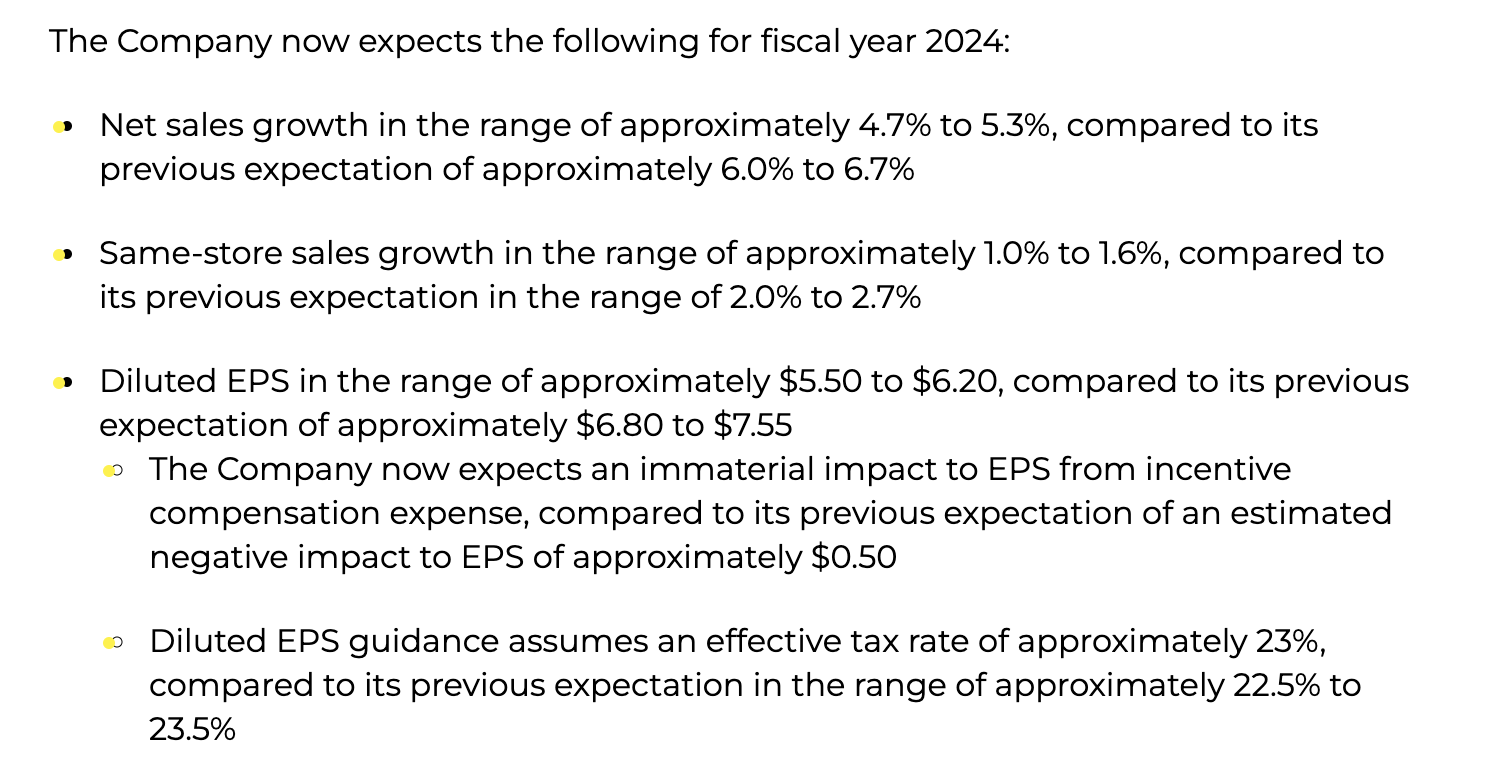

On top of delivering horrible 2Q24 results, guidance was adjusted lower.

- The company sees net sales growth between 4.7%-5.3%. This is down from previous expectations of 6.0%-6.7% growth.

- Same-store sales are expected to grow by no more than 1.6%. As we can see below, the upper bound of this range has been adjusted by 110 basis points.

- EPS is expected to come in between $5.50 and $6.20, down from the prior range of $6.80-$7.55.

Dollar General

The good news for landlords is that the company is not changing its strategy. It will stick to expanding its physical footprint by adding 730 new stores.

Moreover, while improvements in inventory management are "encouraging" according to Bloomberg, a lot more is needed to win back confidence:

Dollar General's reduced forecasts for full-year revenue, same-store sales, and diluted EPS may indicate its back-to-basics plan isn't yet resonating enough with lower-income households that remain financially constrained. Progress in areas like inventory reduction is encouraging, but an acceleration in investments to improve value perception and in-store execution may still be needed. - Bloomberg

The inventory comment makes a lot of sense, as the retailer saw an 11.0% decline in inventories. Getting rid of excess inventory will help the company streamline its product offering without having to engage in needless discounts.

Unfortunately, the market is just too weak for the company to turn this into a tangible benefit - at least for the time being. These inventory adjustments will be a big tailwind the moment demand improves.

Valuation-wise, the stock is now trading at less than 13x earnings, a mile below its average multiple of roughly 18.0x.

Data by YCharts

Data by YCharts

Using 2024 guidance numbers ($5.85 EPS midpoint), the company has a fair stock price value of $105. That's 16% above the current price and based on an 18x multiple.

Unfortunately, in this market, investors won't apply an 18x multiple. Uncertainty is just too high.

While I expect DG to survive this environment and recover, I don't know where it will bottom. Sure, after losing almost a third of its value in a single day, a lot of bad news has been priced in.

However, I don't expect DG to turn into a sustainable wealth compounder anytime soon. Given the challenging environment, I continue to prefer buying its landlords. They have more safety and income. In this economic environment, I think that's the place to be.

Takeaway

Dollar General's recent earnings report was a wake-up call, revealing significant headwinds.

Sales growth is slowing, costs are rising, and new competition from Walmart and Aldi is heating up.

With inflation squeezing its core customers and super-low-cost competitors like Temu disrupting non-food sales, DG is caught in a tough spot.

Even though the stock looks cheap after a steep drop, I'm not rushing in, as I believe DG's landlords offer a safer bet in this turbulent environment given their steady income and lower risk.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.