3D Systems: Green Shoots Amidst Ongoing Macro Challenges

Summary

- 3D Systems reported weak results in Q1 but returned to sequential growth in the second quarter and now appears to be more optimistic about its near-term prospects.

- 3D Systems expects to be profitable on an adjusted EBITDA basis in the fourth quarter on the back of revenue growth and cost-cutting efforts.

- 3D Systems' valuation is now fairly modest, which could result in solid returns if the company can meet its guidance.

- Industry dynamics remain tough, though, and I continue to think that there are better ways to capitalize on additive manufacturing than hardware companies.

simonkr

After significant reporting delays, 3D Systems (NYSE:DDD) has now released its first half results for 2024. While Q1 results were extremely poor, the company returned to sequential growth in Q2 and appeared fairly upbeat on the earnings call. Assuming 3D Systems can deliver on guidance, the company will return to growth later in the year and achieve cash flow breakeven.

I previously suggested that 3D Systems was facing another difficult year and that its valuation was relatively high given macro headwinds and its lack of differentiation. This has largely proven to be the case, with the stock down over 40% since then.

While the worst may now be behind 3D Systems, demand is likely to remain soft in the near term and competition from China and customer concentration in the dental business continue to pose challenges.

Market Conditions

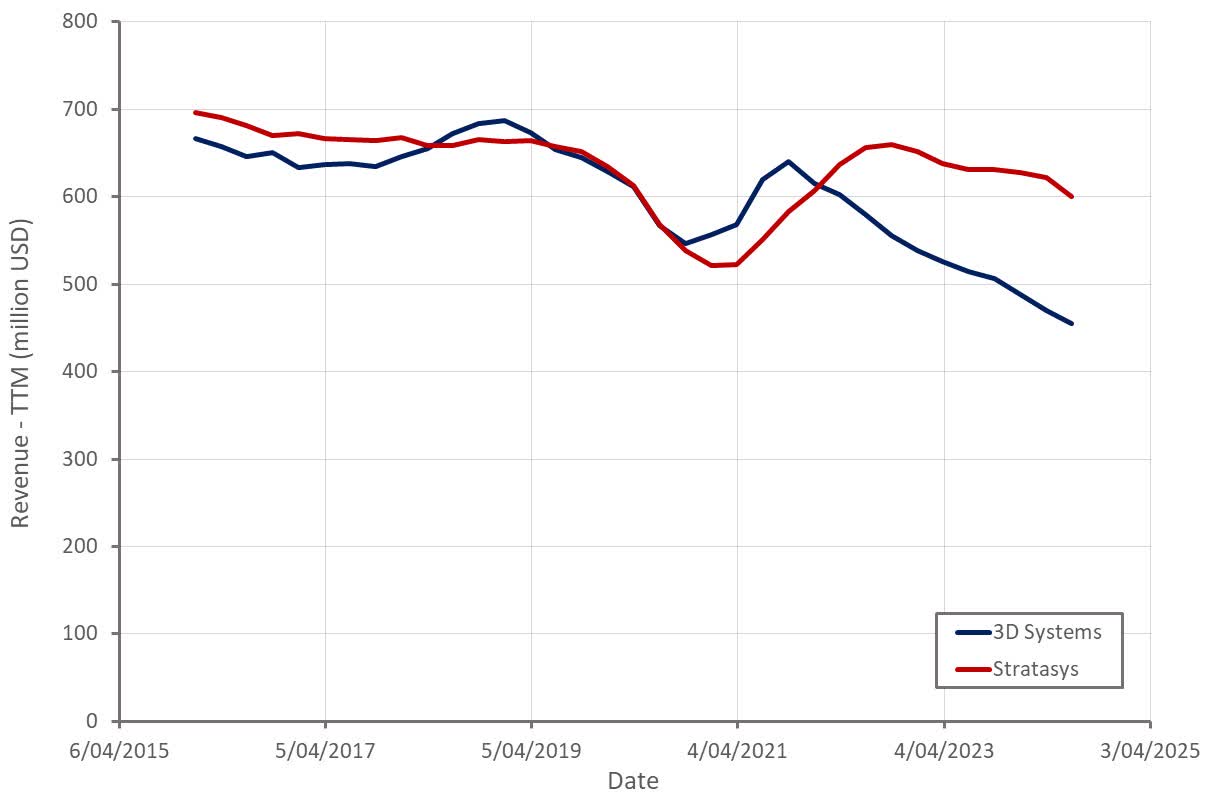

3D Systems’ results have been poor in recent years, but it is not alone in this regard. Stratasys (SSYS) also reported soft Q2 results and announced a restructuring initiative.

Figure 1: 3D Systems and Stratasys Revenue (source: Created by author using data from company reports)

Customer CapEx remains soft, negatively impacting printer hardware sales across most of 3D Systems’ end markets. 3D Systems believes that this is due to high-interest rates, geopolitical tensions and uncertain end market demand.

The company’s pipeline is now strengthening though, and sequential growth is expected through the remainder of the year, provided macro conditions remain stable. While 3D Systems now appears more optimistic, there isn’t really much hard data to support an optimistic outlook.

The company's guidance appears to be based on expectations of lower interest rates and the impact that this could have on demand. While this is probably not unreasonable, there is a real risk that lower rates will coincide with economic weakness, meaning increased demand may not materialize.

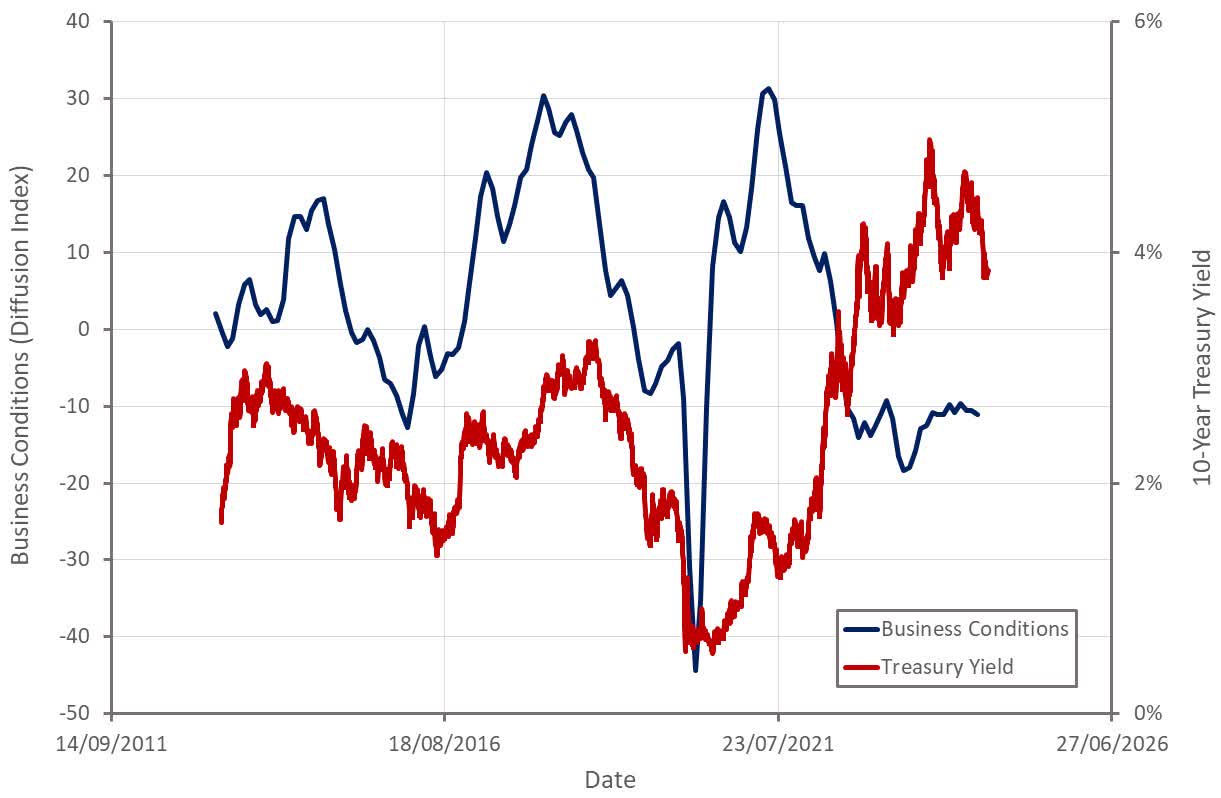

In recent years, higher yields have generally coincided with stronger economic data. The large and rapid rise in rates that began in 2022 crushed sentiment though and is significantly impacting economic activity in some areas.

Figure 2: Manufacturing Survey Data and Treasury Yields (source: Created by author using data from The Federal Reserve)

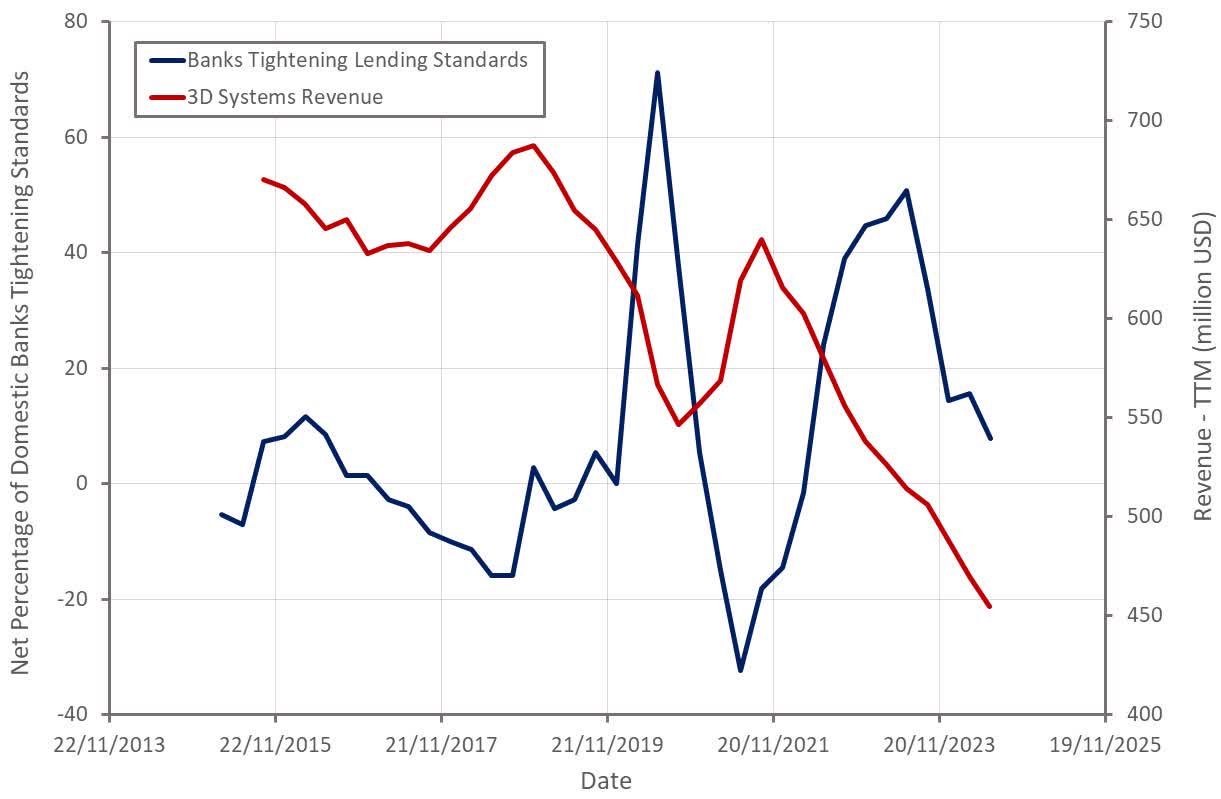

Bank lending standards may be a better proxy for printer hardware demand, assuming bank loans are an important source of financing. While interest rates remain elevated, lending standards are normalizing, which could lead to a rebound in hardware demand, assuming economic conditions hold up.

Figure 3: Banks Tightening Lending Standards and 3D Systems Revenue (source: Created by author using data from The Federal Reserve)

While weak demand for hardware is hitting the industry, the underlying trends in printer usage appear more positive, as indicated by rising consumables revenue. At some point this will likely force customers to increase their investment in printers, but 3D printing vendors appear to have little visibility into when this will occur.

Table 1: Stratasys Q2 2024 Systems and Consumables Revenue (source: Created by author using data from Stratasys)

3D Systems Business Updates

The multi-billion orthopedic market remains a focus area for 3D Systems. The company is able to offer end-to-end solutions for this market, from digital imaging to custom implants. Within orthopedics, 3D Systems continues to extend its portfolio into trauma, where quality and response time are both important.

3D Systems received FDA clearance for 3D-PEEK cranial implants in April 2023. PEEK has similar characteristics to human bone and has excellent biocompatibility. The craniomaxillofacial reconstruction market is expected to exceed 2 billion USD by the end of 2030.

PEEK has been on the market for some time, but 3D Systems is differentiated by its ability to print custom PEEK implants using its self-contained cleanroom environment EXT 220 printing technology. This helps to reduce lead times and provides cost savings of up to 85% compared to traditional manufacturing methods. FDA clearance for the EXT 220 MED printing system was secured earlier this year in the US. Whether this provides a boost to 3D Systems' business remains to be seen though. Companies like Stryker (SYK) have a strong position in orthopedics and have significant 3D printing capabilities.

3D Systems is now targeting all four major facets of dentistry, including:

- Alignment

- Protection

- Repair

- Replacement of teeth

This positions 3D Systems to capitalize on a global dental 3D printing market that is expected to be worth over 15 billion USD by 2032.

3D Systems has a focus on direct printed aligners, believing that the smaller printers involved open up more channels to market. 3D Systems also thinks that direct printed aligners have the potential to move teeth more effectively. The company wants to commercialize this technology in late 2025.

3D Systems also recently received the largest contract award in its history. The contract has an estimated value of close to 250 million USD over 5 years to support indirect manufacturing processes for clear aligners.

3D Systems' technology can also be used to produce mouth guards for sleep apnea. The company believes its solution is cost competitive and allows more design flexibility. For example, a dual material mouth guard can be created with a soft surface for around the gums and a hard surface for the teeth.

Financial Analysis

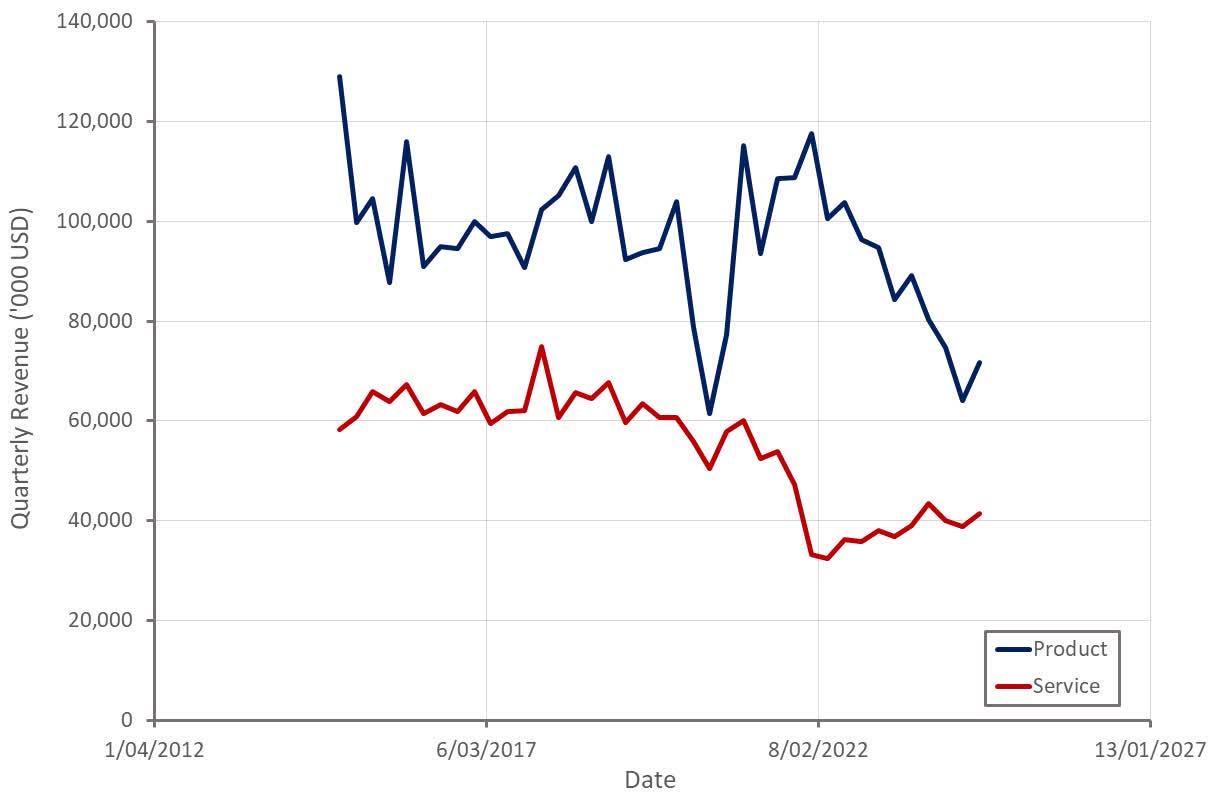

3D Systems generated 103 million USD revenue in the first quarter, down 15% YoY, and 113 million USD revenue in the second quarter, a decline of 12% YoY. This decline was almost entirely driven by soft printer sales, with materials largely flat and modest services growth. While hardware demand was weak, consumables and services were resilient. 3D Systems recorded fairly solid sequential growth across its business in the second quarter though.

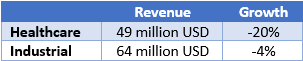

Healthcare revenue was down 14% YoY in the first half of 2024 to 94 million USD, while industrial revenue declined 13% to 122 million USD. Within industrials, semiconductors, aerospace and defense were unsurprisingly sources of strength. 3D Systems' new long-term supply agreement in the clear aligner market is expected to drive sequential healthcare growth going forward.

Table 2: 3D Systems Revenue by End Market (source: Created by author using data from 3D Systems)

3D Systems expects 450-460 million USD revenue in 2024, with continued sequential growth. This would see 3D Systems return YoY growth in the fourth quarter and fairly strong double-digit growth in 2025.

Figure 4: 3D Systems Revenue (source: Created by author using data from 3D Systems)

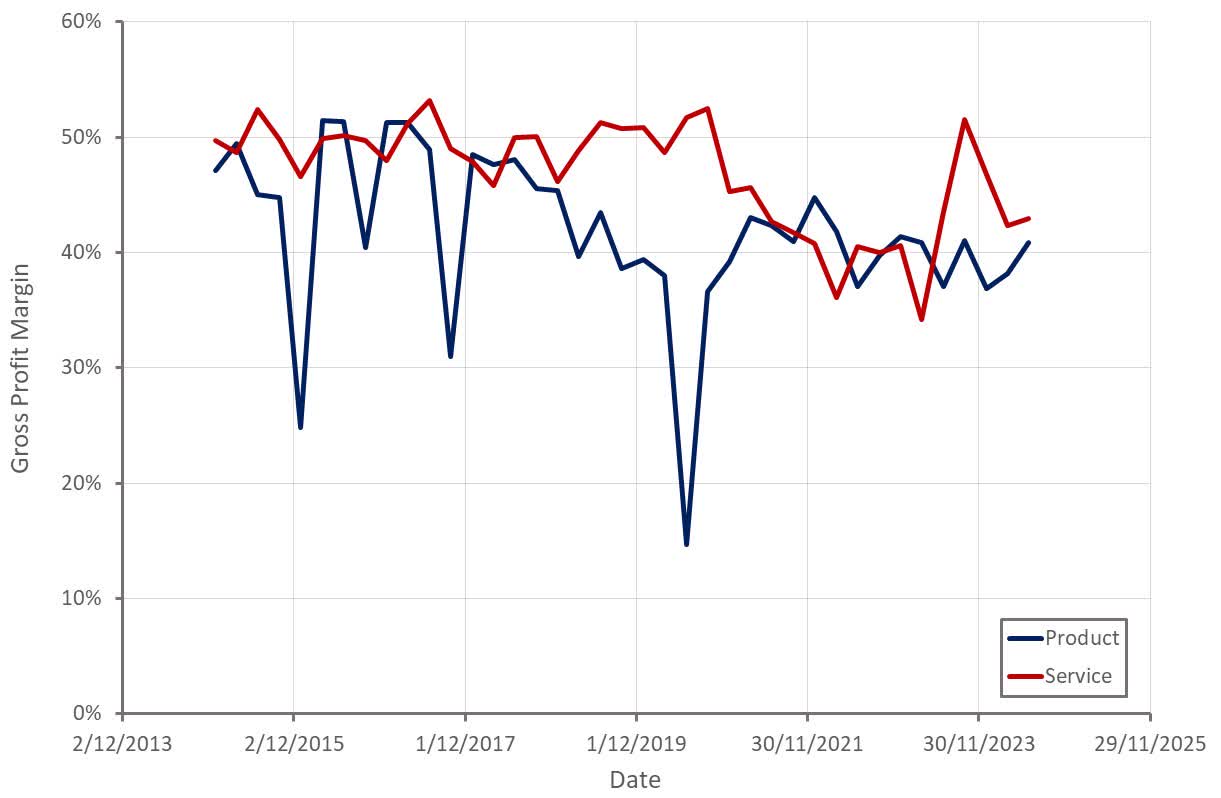

3D Systems' gross margins have stabilized in recent quarters, despite volume weakness, which 3D Systems attributed to revenue mix. Gross margins were hit by a 2.8 million USD increase in inventory obsolescence reserve in the first quarter though. 3D Systems expects its gross margins to continue improving going forward, driven by increasing volumes, in-sourcing and cost optimization.

Figure 5: 3D Systems Gross Profit Margins (source: Created by author using data from 3D Systems)

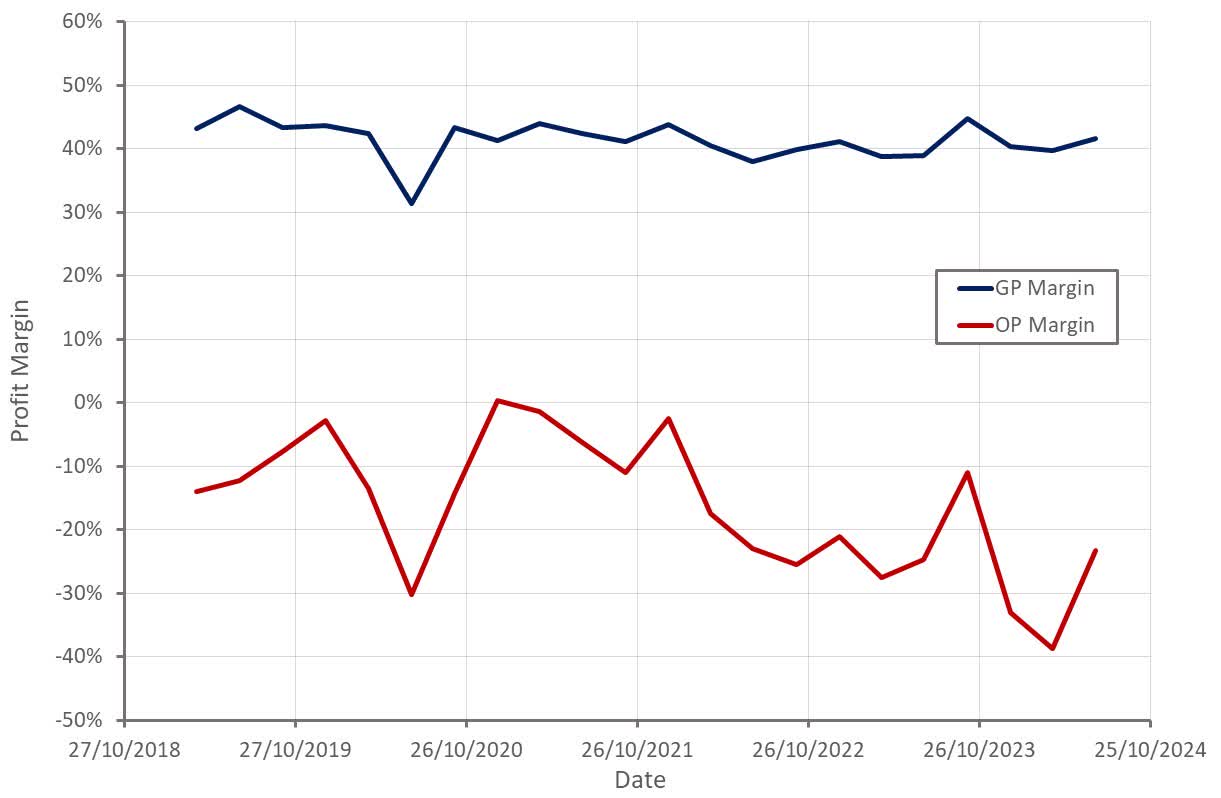

3D Systems' adjusted EBITDA was negative 20.1 million USD in Q1 and negative 12.9 million USD in Q2. 3D Systems recently changed their auditor, with the audit taking much longer than expected and involving significant costs. External audit fees and outside services were 5 million USD higher than expected in the first quarter and 2 million USD higher in the second quarter. These costs are transient though and are expected to subside in the second half.

3D Systems has been engaged in a restructuring effort since Q4 2023, closing and consolidating 15 sites globally and reducing its workforce. Savings from these efforts are expected to become more apparent later in the year. As a result, 3D Systems is targeting operating expenses under 60 million USD in the fourth quarter. 3D Systems is targeting adjusted EBITDA breakeven in the fourth quarter on the back of operating leverage, higher gross margins and lower OpEx.

Figure 6: 3D Systems Profit Margins (source: Created by author using data from 3D Systems)

3D Systems ended the second quarter with 193 million USD in cash and cash equivalents. While 3D Systems' cash balance has declined significantly over the past few years, the company still has a reasonably strong balance sheet.

3D Systems has reduced its long-term debt by over 50% after paying roughly 87 million USD to repurchase some of its 2026 convertible notes at a substantial discount.

Conclusion

While 3D Systems' business is struggling, the company is reasonably well-placed to weather the current downturn. The company's losses are relatively small, and cost-cutting efforts combined with a return to growth could see 3D Systems transition to profitability over the next 12 months. This is dependent on the macro environment stabilizing/improving, though, which is a risk.

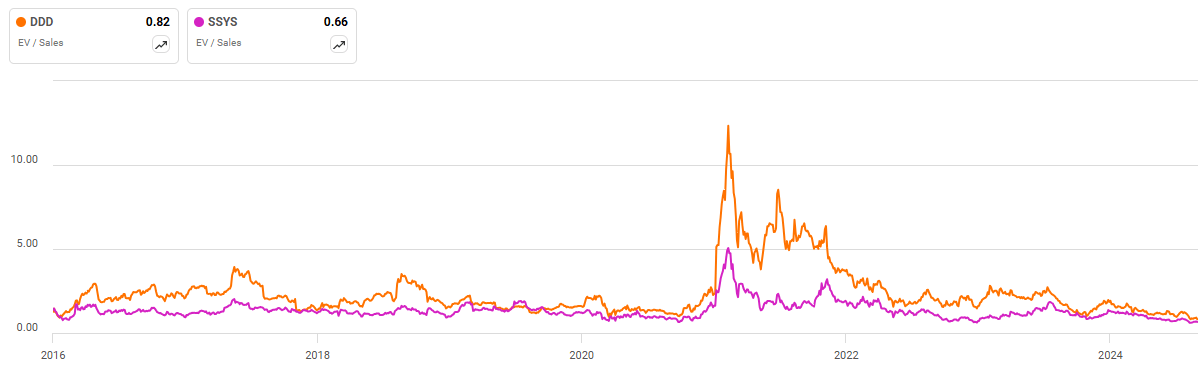

After large share price declines over the past few years, 3D Systems now has a fairly modest valuation. This is reflective both of the headwinds facing manufacturing at the moment and growing investor skepticism of 3D printing companies. While this could present an opportunity when the demand environment improves, there is a risk that 3D printing stocks continue to perform poorly due to unfavorable industry dynamics. Industry consolidation should improve profitability, but this will take time.

Areas like healthcare are likely to prove more lucrative than 3D Systems' historical focus on hardware. While little has been said about regenerative medicine lately, this also remains a large opportunity longer term. I continue to think that there are better ways to capitalize on the potential for additive manufacturing than hardware companies though.

Figure 7: 3D Systems EV/S Ratio (source: Seeking Alpha)

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.