A Superior Business Model: Why I Just Put Wheaton Precious Metals On My Watchlist

Summary

- Wheaton Precious Metals uses a streaming model, financing mining projects in exchange for discounted future production, and avoiding operational risks.

- WPM's high margins, strong growth prospects, and focus on gold and silver make it a compelling investment compared to traditional miners.

- Despite a high valuation, WPM’s fundamentals are solid, with robust dividends and exposure to low-risk jurisdictions, making it a top pick for gold exposure.

GeorgePeters

Introduction

I have been bullish on gold for a while. For example, last year, I wrote "Buy GDX Before It's Too Late." GDX is the VanEck Gold Miners ETF (GDX), which I often use as a proxy for this industry.

Since then, gold miners have returned 36%. They have been supported by the price of gold, which has made its way above $2,500 per troy ounce.

Data by YCharts

Data by YCharts

My gold thesis has mainly been based on expectations of lower rates in the future, potentially triggered by the Fed having to pick between fighting inflation and protecting economic growth.

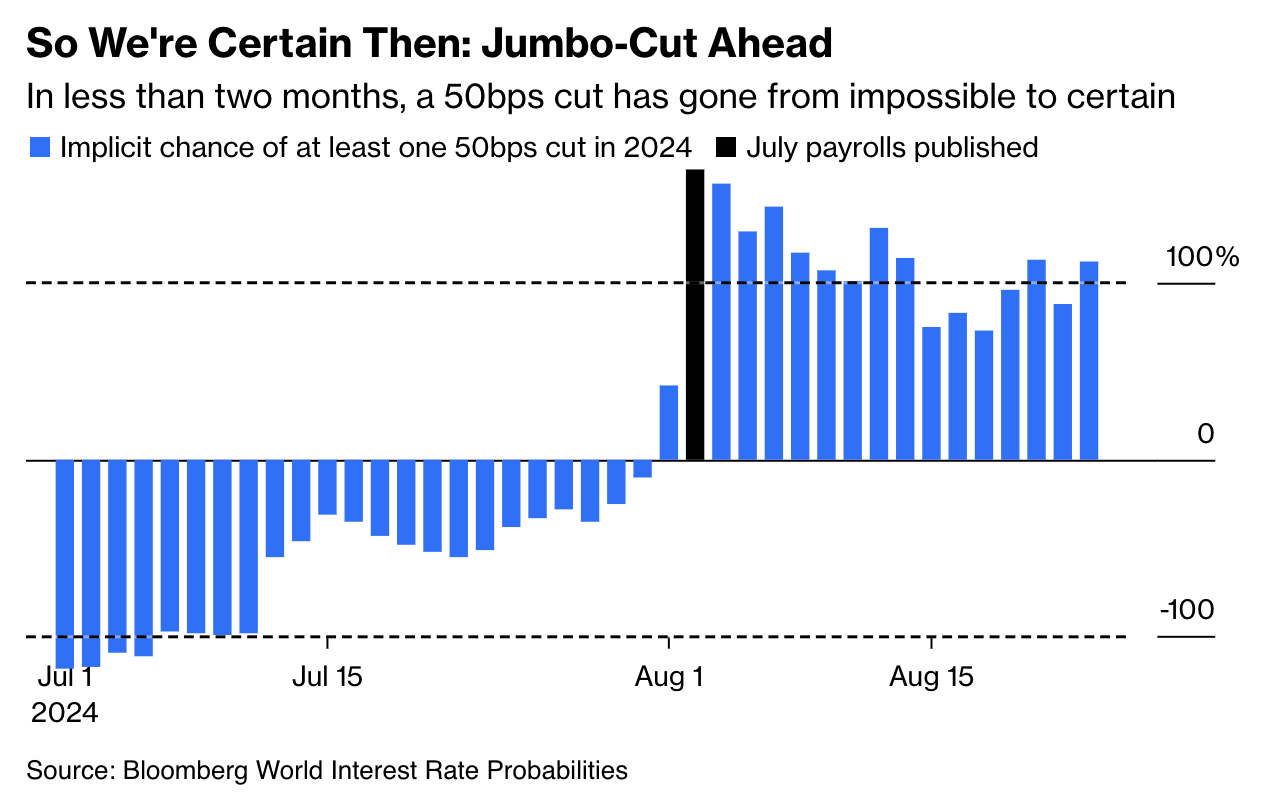

So far, this thesis is working out quite well, as poor economic growth conditions have caused the market to expect lower rates in the future. In this case, the market expects a 100% change of 50 basis points in cuts this year. This could be one cut of 50 basis points or two cuts of 25 basis points.

Bloomberg

It also helps that real rates (interest rates adjusted for inflation) are falling, which makes gold more attractive on a relative basis. After all, we can think of gold as a "currency" that does not pay any interest. The moment dollar-denominated bonds see a drop in real yields, gold becomes more attractive.

Bloomberg

This also explains why analysts are increasingly bullish in light of accelerating demand:

For now, Citigroup Inc. sees inflows into ETFs expanding "significantly" over six to 12 months, with demand bolstered by looser monetary policy, as well as a potential increase in volatility amid recessionary risks. Gold may reach $3,000 by mid-2025, the bank said in a note before Powell's address. Spot bullion traded at $2,525.73 an ounce at 9:18 a.m. in New York, close to its peak.

The market can expect large ETF flows, as well as ongoing speculator demand, when the Fed actually makes its first rate cut, according to UBS Group AG, which sees prices at $2,600 for the last quarter of this year. Increasing geopolitical risks should also lift demand for portfolio hedges, said Wayne Gordon, commodities strategist at UBS Global Wealth Management. - Bloomberg (emphasis added)

Personally, I have no idea where gold will trade next year. I'm not even going to attempt to predict it.

What matters to me is that the fundamentals are good. After years of subdued inflation, we're now in a situation of sticky inflation, elevated monetary policy uncertainty, and geopolitical risks. This bodes well for the shiny "competitor" of the U.S. dollar.

However, when it comes to buying gold, I'm not buying physical gold. Although I believe physical gold is a terrific investment, I'm not doing it for a number of reasons:

- Safety. Because I'm using my own name as a writer, I do not want to hold physical gold at home. It's not worth it to me.

- Flexibility. For various reasons, I need to remain flexible. This means I am planning on moving around quite a bit. Holding a substantial amount of money in physical gold (at a bank) would make this a bit more difficult.

Although I am fully aware that alternatives exist, I stick to the category I like most: public equity.

That's where Wheaton Precious Metals Corp. (NYSE:WPM) comes in. As some readers may know, I'm not a big fan of gold miners (although I like some of them). Because of operational risks, poor capital allocation decisions (in some cases), geopolitical risks, and inflation risks, the average gold miner has a horrible track record.

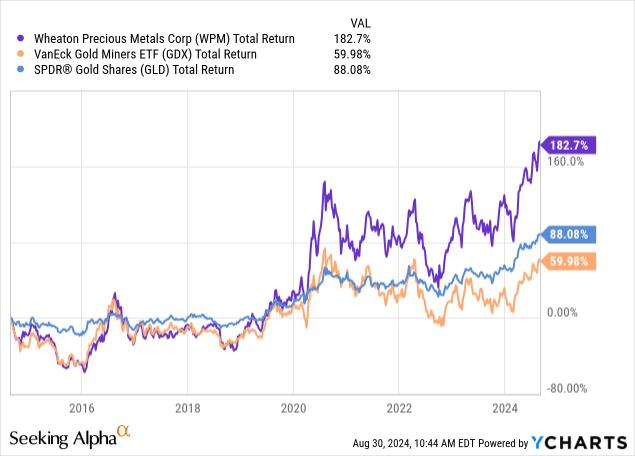

Over the past ten years, gold has returned 88%. Gold miners have returned just 60%. Wheaton has returned 183%.

Data by YCharts

Data by YCharts

Although Wheaton is sometimes put in the same category as miners, it's not a miner. It's a streamer.

Hence, on May 13, when I wrote my most recent article on this company, I went with the title "Bullish On Gold? Don't Buy Gold Miners, Buy Wheaton Instead."

Since then, shares have returned 14%, beating the 8% return of the S&P 500 by a decent margin.

In this article, I'll update my thesis in light of new developments, updated earnings, and my belief that high-margin streamers are the place to be.

What Is A Streamer?

As I wrote in my prior article, streamers have a fascinating business model. Instead of producing precious metals, they finance mining projects.

However, instead of giving a loan, a streamer purchases a percentage of future metal production from the mine. The miner can use this capital to build or expand mines, acquire a competitor, or reduce debt. It can do this in a "non-dilutive" way, as it does not require issuing shares.

Wheaton Precious Metals Corp.

Once the mining project is operational, the streamer gets to buy a certain percentage of the mine's production at a discount to the spot price.

The cash generated from metal sales can be used for various purposes, including investments in new streams, the distribution of dividends, and other purposes.

Wheaton's Near-Perfect Business Model

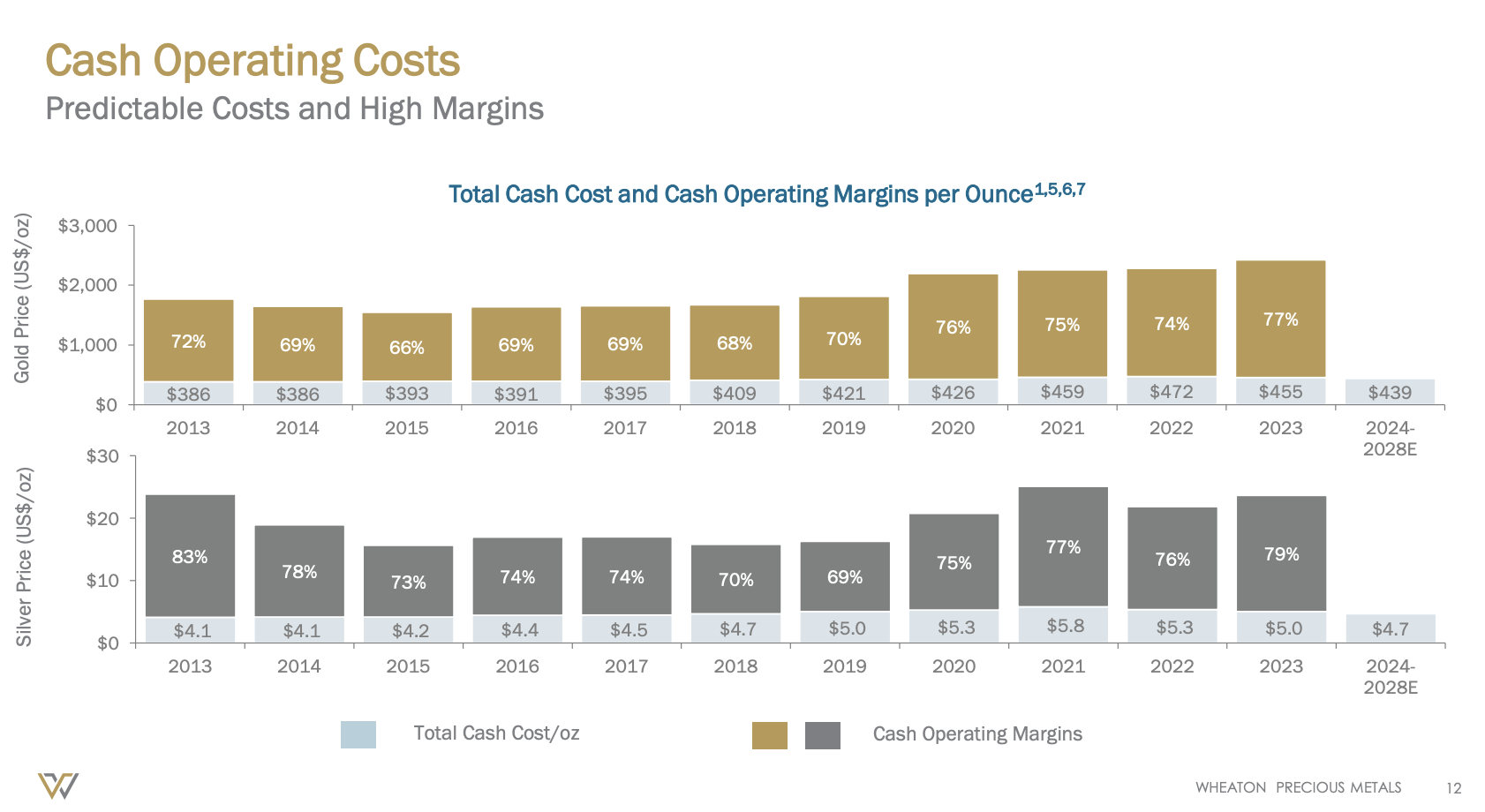

Thanks to this business model, the company has cash operating margins of almost 80%, something gold miners (or most companies, in general) can only dream of.

Wheaton Precious Metals Corp.

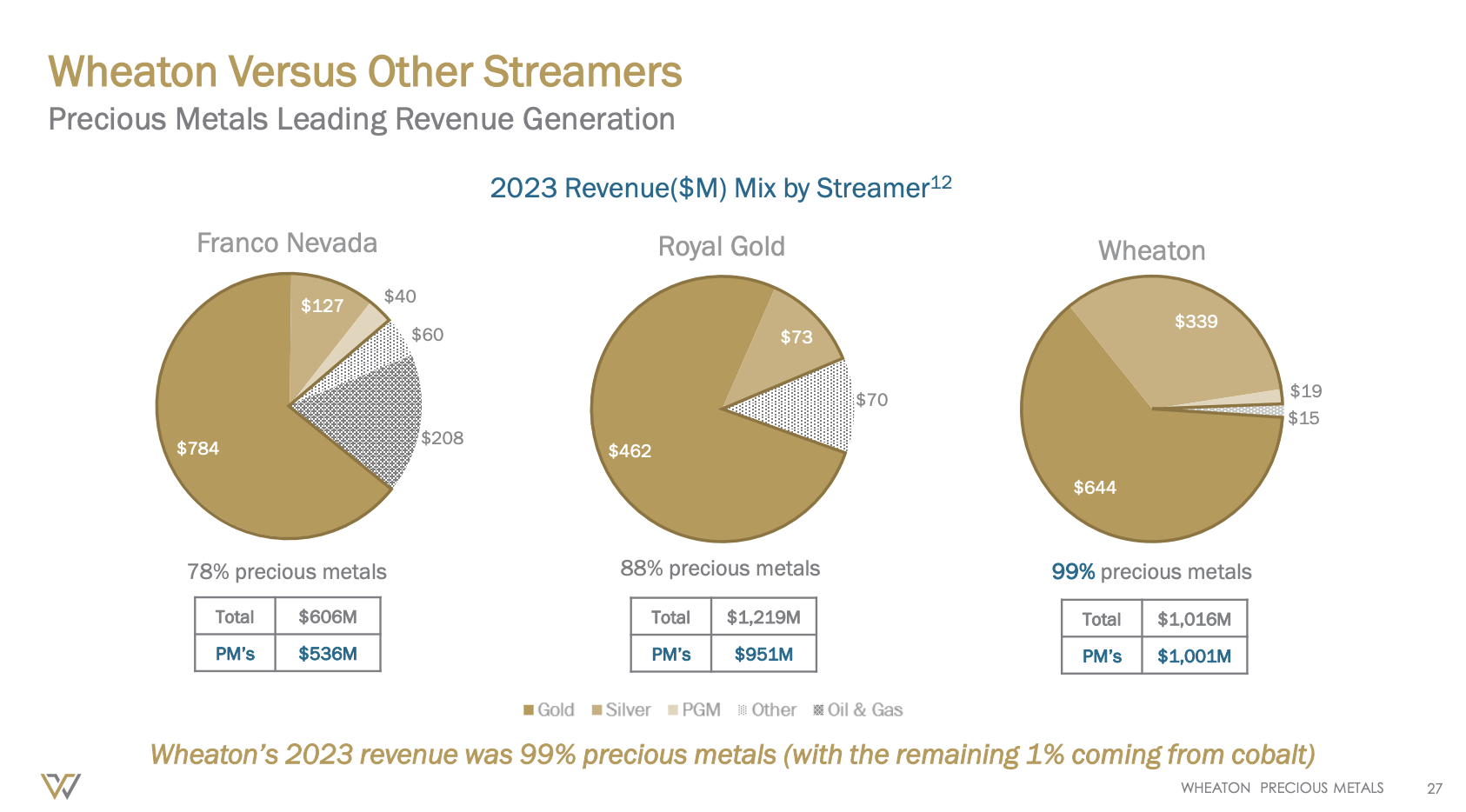

Moreover, Wheaton is the only major streamer with almost 100% exposure to gold and silver. Although there is nothing wrong with non-precious metal streams, the Wheaton Corporation has decided that gold and silver are superior.

Wheaton Precious Metals Corp.

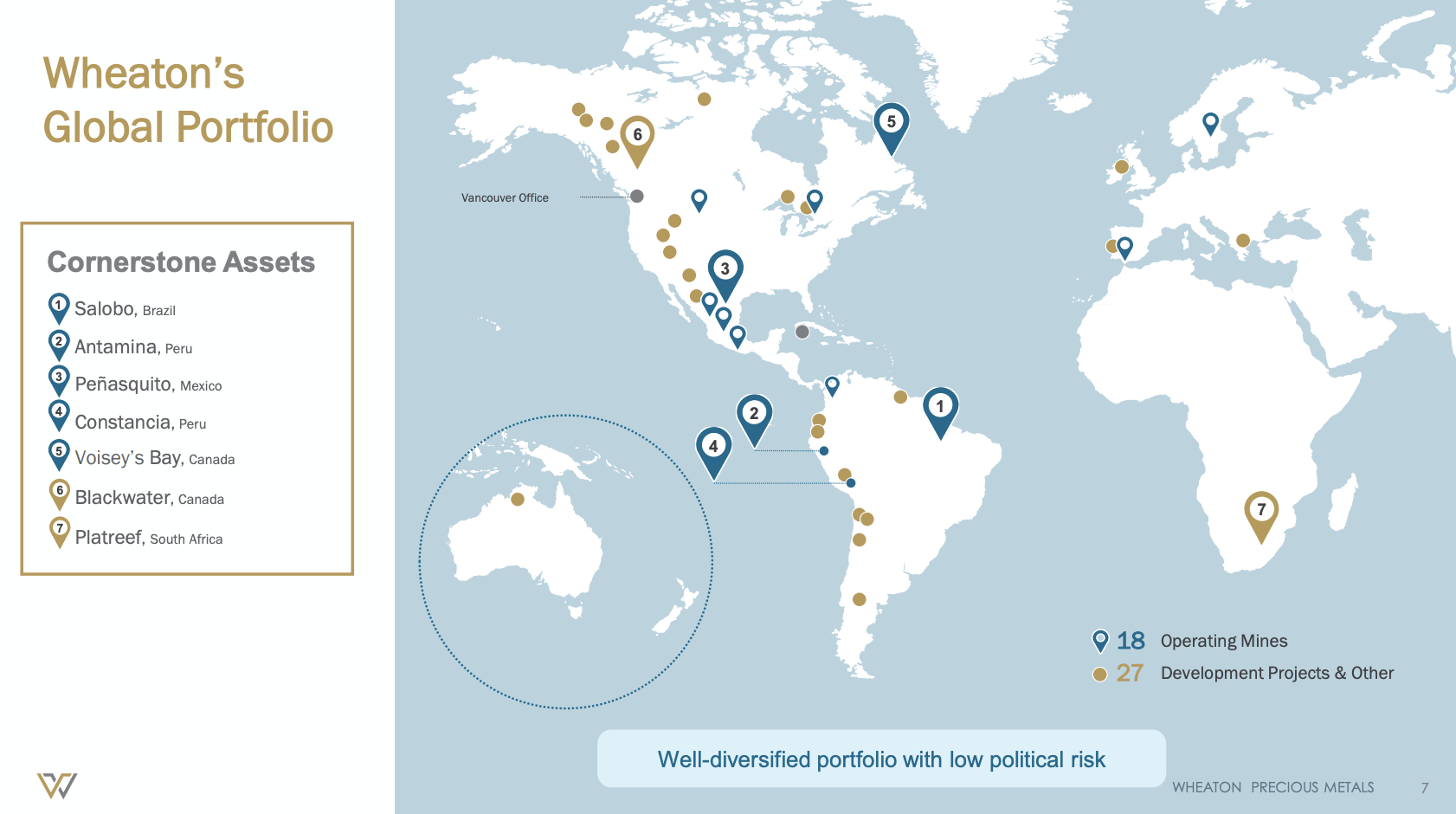

It also benefits from the fact that most of its mines are in low-risk jurisdictions, including Brazil (34% of revenues), Mexico (20%), Canada (12%), and Europe (13%). This excludes projects under development, most of which are located in North America.

Wheaton Precious Metals Corp.

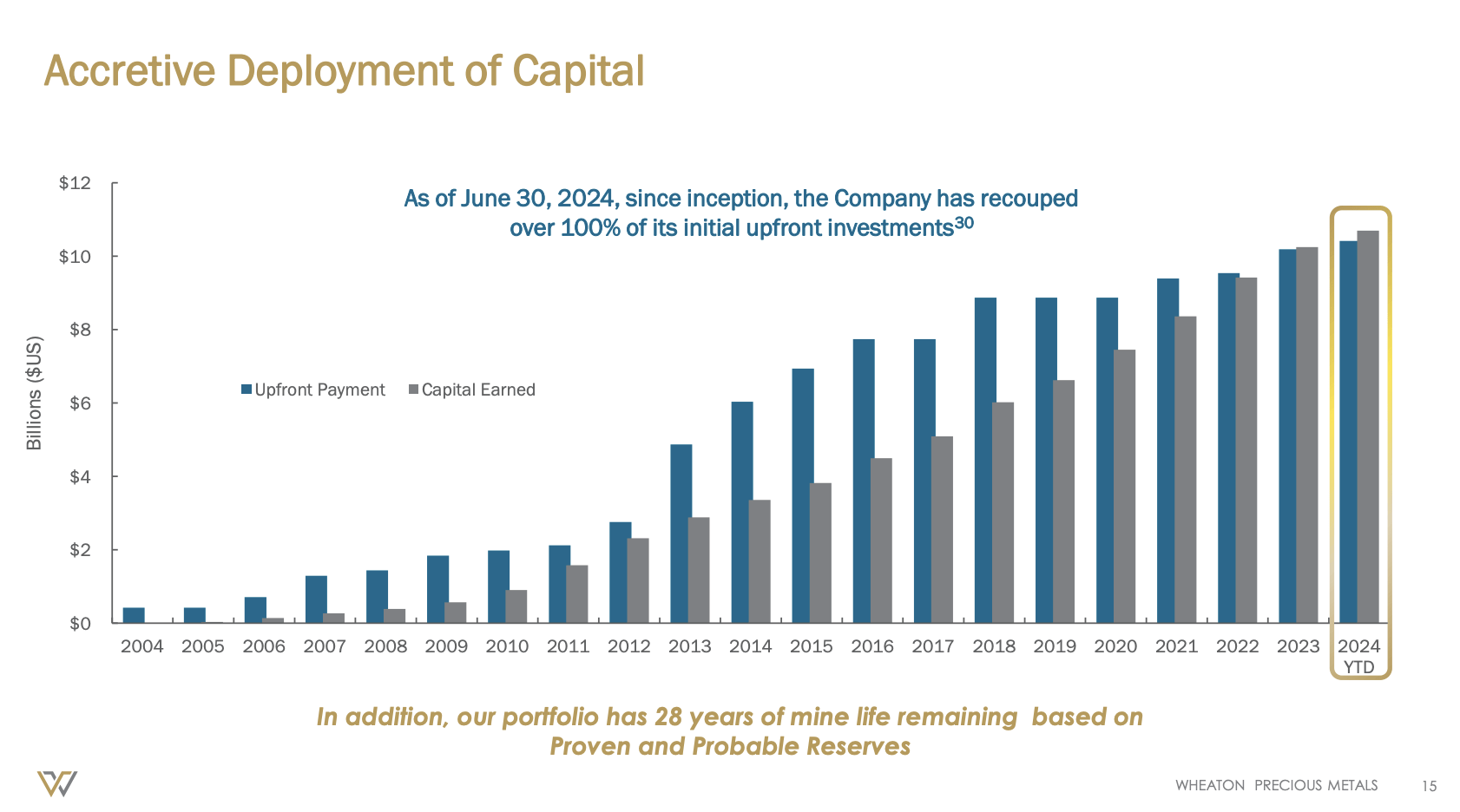

What's fascinating is that, to date, the company has invested $10.4 billion in streams. It has generated $10.7 billion in cash flows, $2.2 billion of which has been distributed as dividends.

In other words, the company has recouped every penny of past investments, while still benefitting from its right to buy production at a discount!

Wheaton Precious Metals Corp.

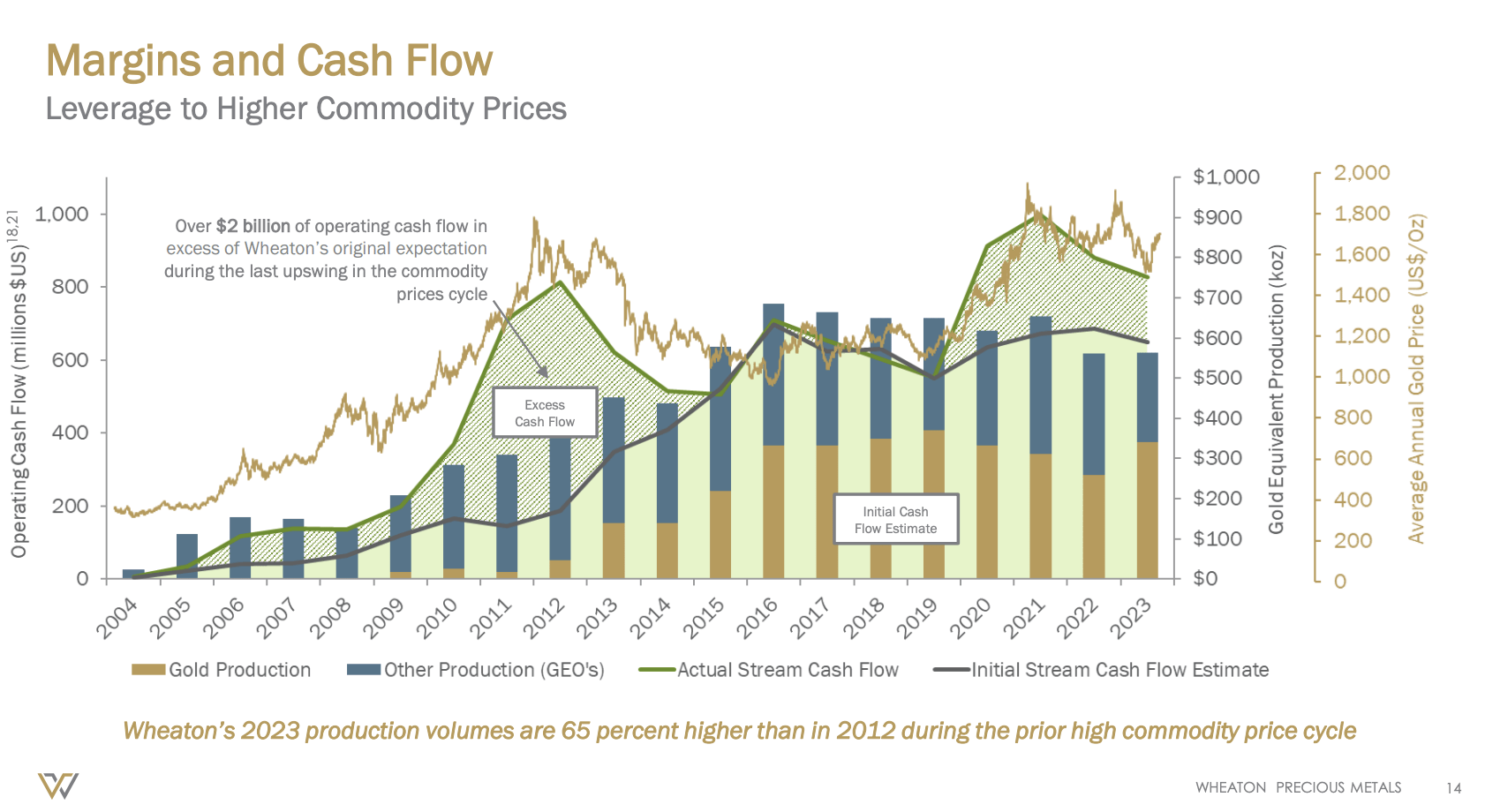

It also needs to be said that current production and pricing tailwinds are much stronger than initially expected. Last year, its production was 65% higher than in 2012, when the prior commodity cycle peaked. Compared to its initial cash flow estimate, it is now producing hundreds of millions more in streams, as we can see below.

Wheaton Precious Metals Corp.

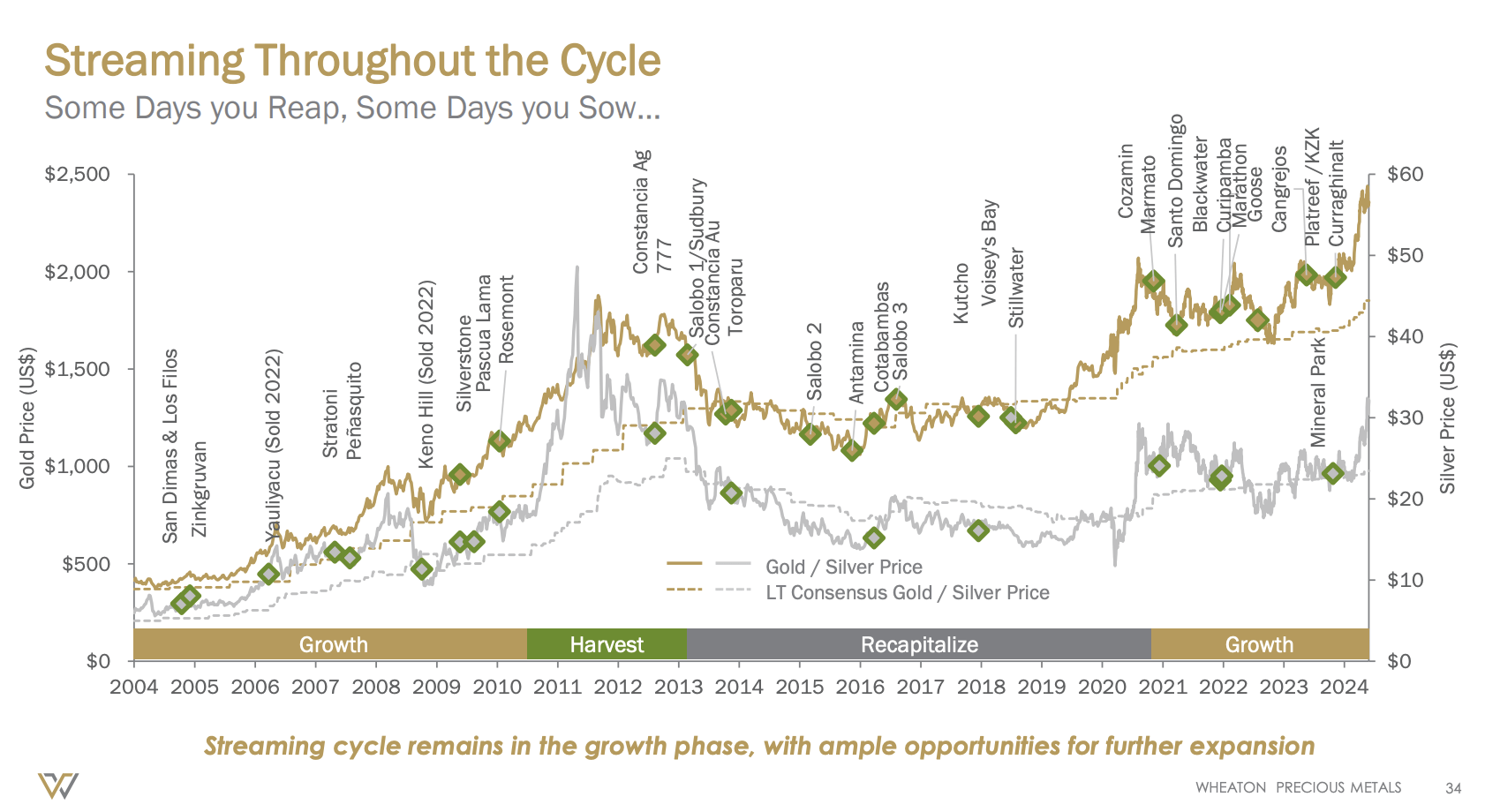

With that in mind, the company is currently in the "growth" phase. In fact, it has been in this phase since 2020. Looking at the bigger picture, the situation could not be better:

- Past investments have been 100% recouped, as we just briefly discussed.

- It has a healthy balance sheet, including $2.5 billion in liquidity. Only looking at gross debt and available cash, the company has $540 million in net cash, meaning more cash than gross debt.

- It has a lot of room for growth without the need to aggressively invest more cash.

Wheaton Precious Metals Corp.

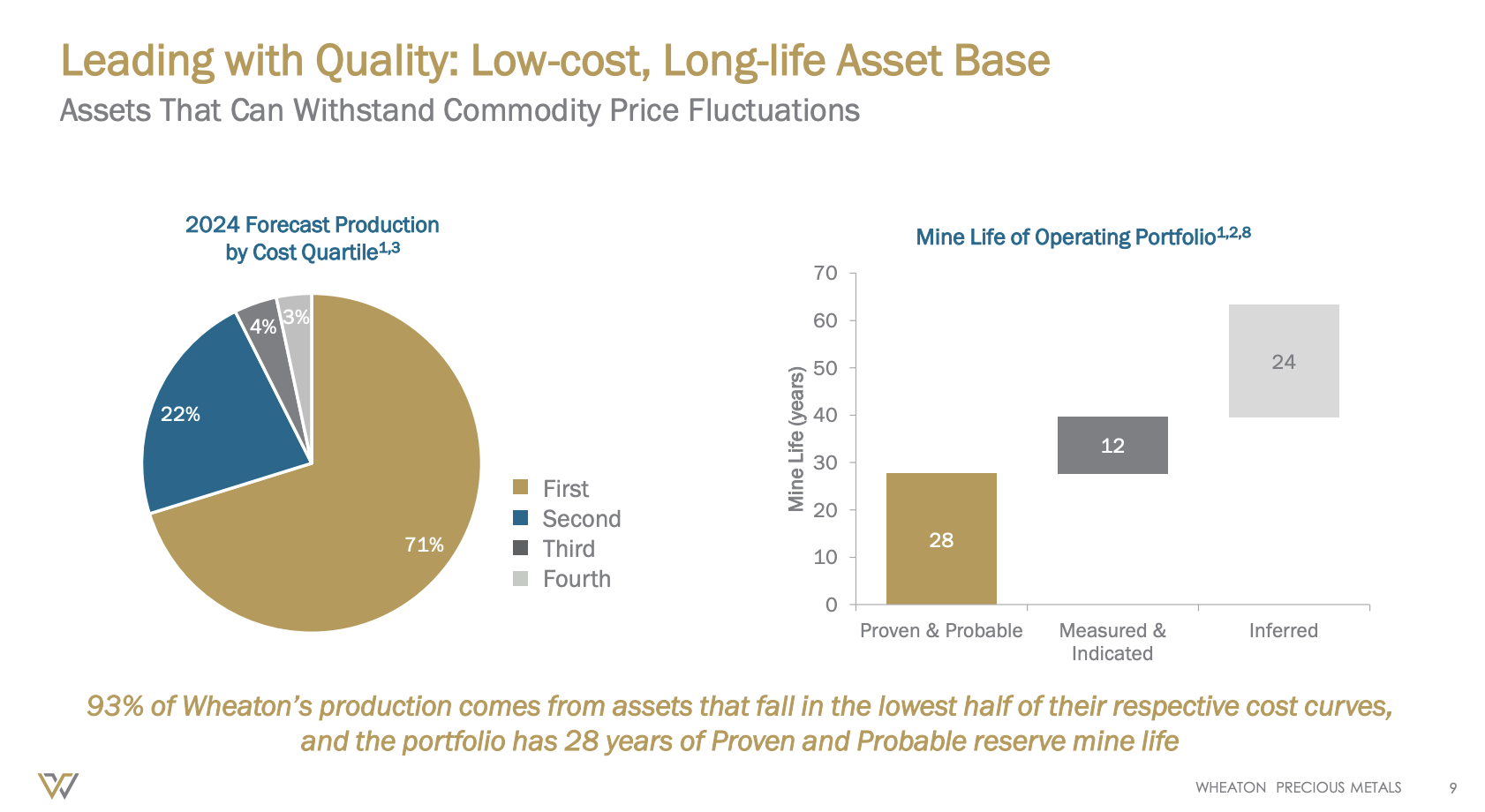

To add some more color, the company's existing mine life is 28 years. These reserves are proven and probably. These 28 years turn into 40 years when adding 12 years' worth of measured and indicated resources. It also has 24 years of inferred resources.

Even better, more than 90% of the company's production comes from assets that fall in the lowest half of the cost curve, making these operations profitable when other competitors may be struggling to remain profitable.

Wheaton Precious Metals Corp.

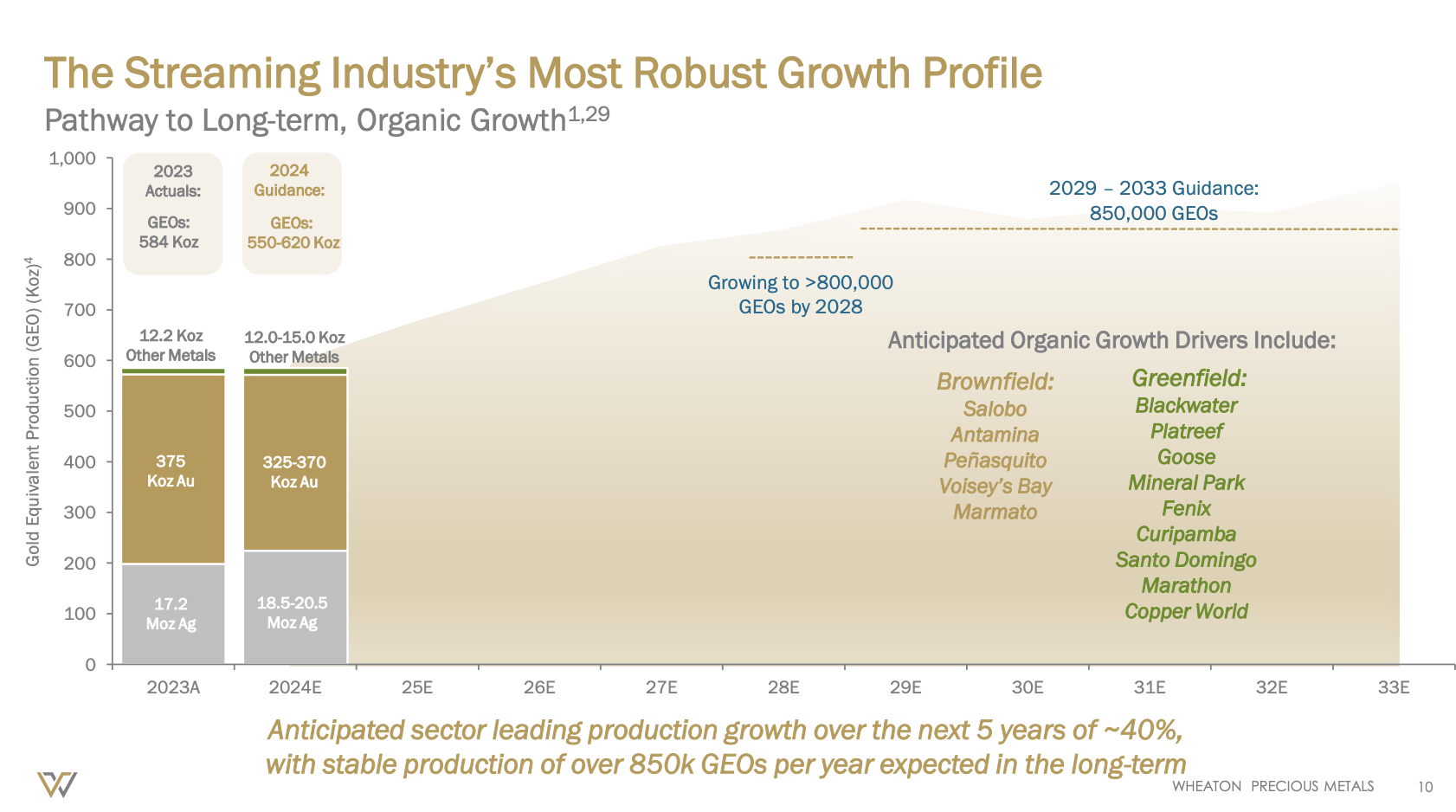

This year, the company is expected to produce between 550 thousand and 620 thousand GEOs. GEO means "gold equivalent ounce."

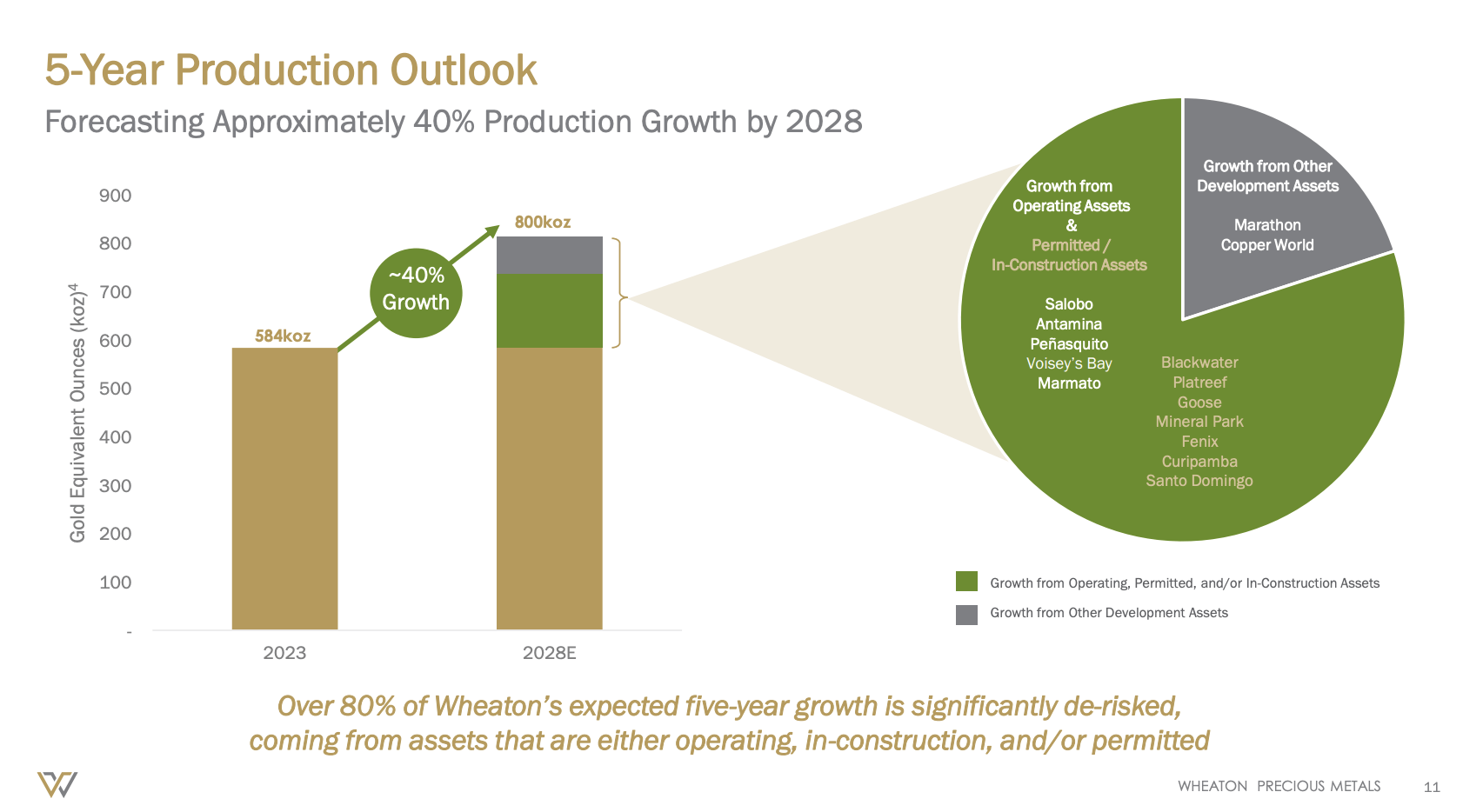

Over the next five years, the company sees a road to roughly 40% organic growth with a long-term production target of roughly 850 thousand GEOs (45% above the 2024 guidance midpoint).

Wheaton Precious Metals Corp.

As we can see below (and above), growth is mainly expected to come from already-developed assets (brownfield) and projects that have been permitted (greenfield).

Production is forecast to increase at an industry-leading rate of approximately 40% to over 800,000 ounces by 2028, primarily due to growth from operating assets, including Salobo, Antamina, Penasquito, Voisey's Bay and Marmato. Development projects which are in construction and/or permitted, including Blackwater Platreef, Goose, Mineral Park, Fenix, Curipamba and Santo Domingo, and predevelopment projects, including Marathon and Copper World, from which production is anticipated towards the latter end of the 5-year forecast period. - WPM 2Q24 Earnings Call

Wheaton Precious Metals Corp.

What does this mean for shareholders?

Dividends & Valuation

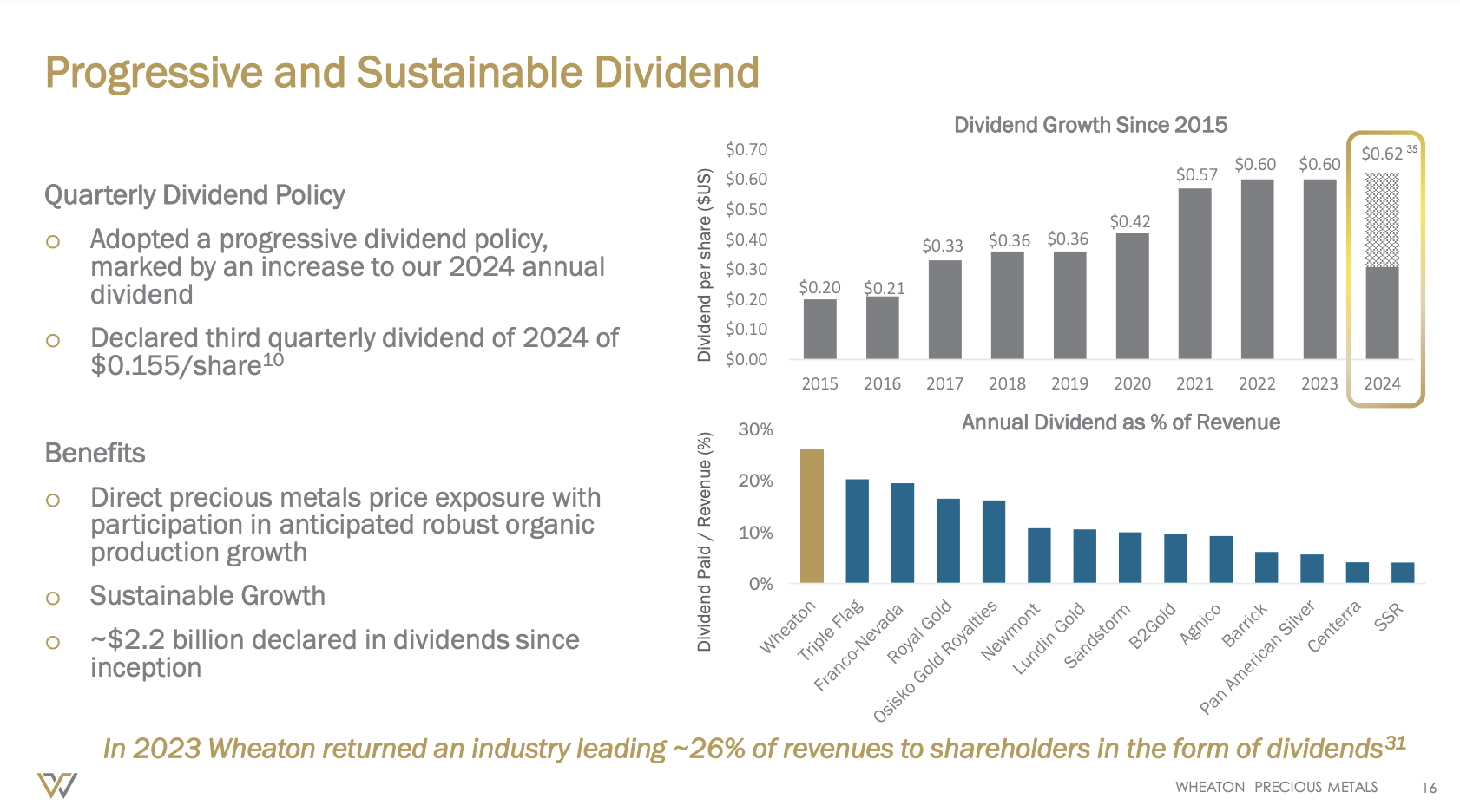

Wheaton Precious Metals is not a high-yield stock. However, that is not its fault, as it pays close to 30% of its revenues in dividends. The reason that number is so much higher compared to non-streaming miners is its elevated profitability.

For the third quarter of this year, the company has declared $0.155 in per-share dividends. Its most recent dividend hike was 3.3% on March 14%.

This translates to a yield of 1.0%.

Although this may be a low yield, there are benefits. One of these benefits is dividend consistency. The company has a history of dividend stability, as high margins protect its dividend even when gold prices are low.

Wheaton Precious Metals Corp.

The other benefit is the company's decision to boost the dividend payout. Before its new plan, the company aimed to maintain a 30% cash flow payout ratio. Now, it is much more upbeat. This is what the company said in its 4Q23 earnings call (it did not comment on it in its 2Q24 earnings call):

And so when we looked at our growth profile coming forward, we realized that if that -- with the current framework, we actually wouldn't be raising the dividend even though we're going to see some growth. And of course, current commodity prices would accelerate that. But we haven't seen that growth for a couple of years. And we just felt that having been flat for a couple of years, it was time to add some growth. We've had substantive growth in our dividend, peer group-leading growth in our dividend over the last 5, 6 years, but it has actually been held flat for a couple of years, and we just thought it was time to give it a bump. - WPM 4Q23 Earnings Call (emphasis added)

Especially in light of aggressive growth opportunities, I am very upbeat about the company's future dividend growth.

With regard to the valuation, there's some bad news.

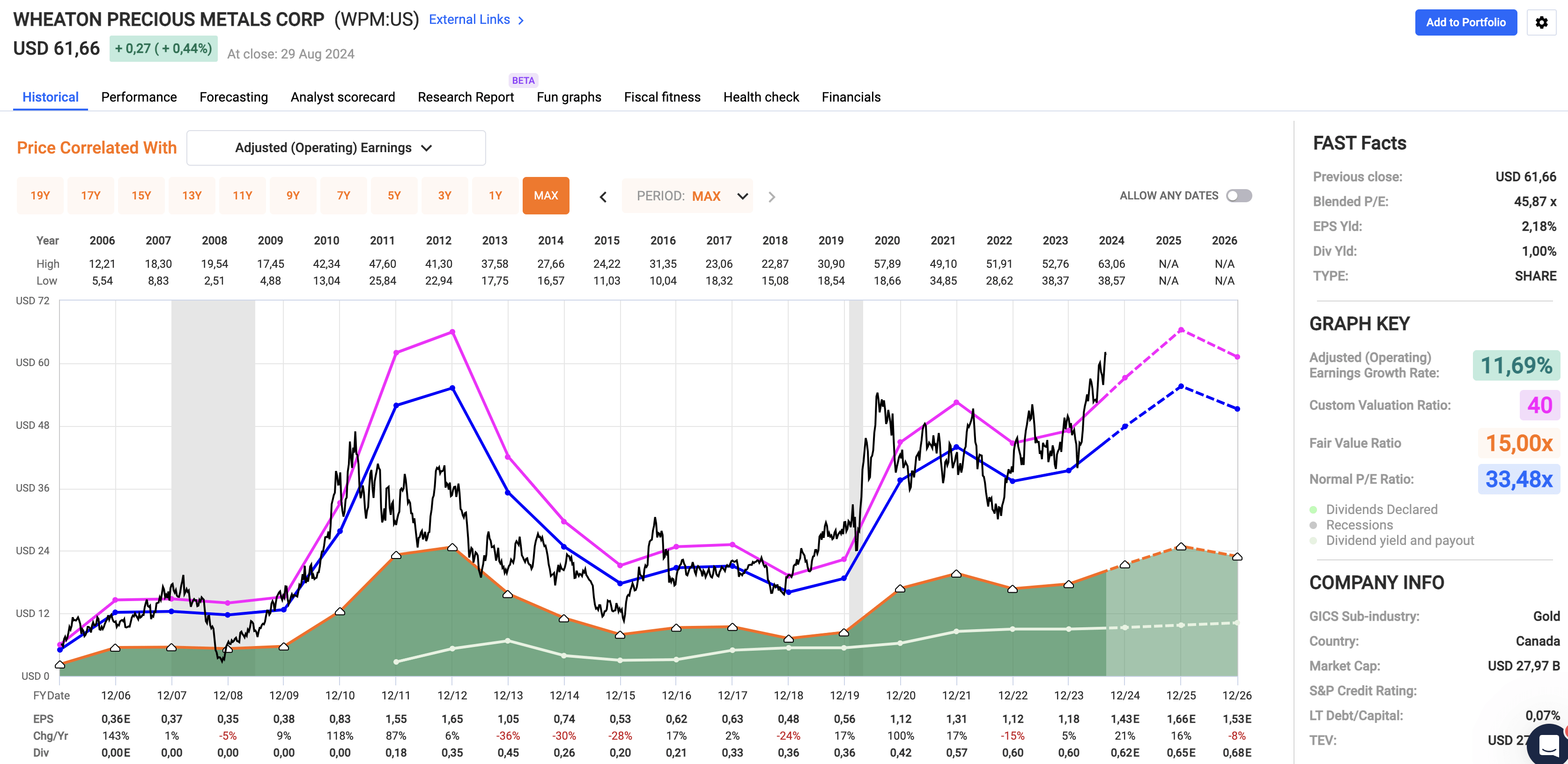

Currently, WPM trades at a blended P/E ratio of 45.9x. Long-term, I'm applying a 40x multiple. I did the same in my prior article and when I assessed its peer, Franco Nevada.

Although a 40x multiple may sound ridiculous, it's fair for a company with an ultra-high margin profile and a path to much higher output growth. Streamers and similar companies usually enjoy elevated multiples, as they squeeze more profits from every revenue dollar.

FAST Graphs

Unfortunately, based on current EPS expectations, the stock trades at its fair price.

Nonetheless, I'm still bullish on the company, as I believe gold will remain in a strong uptrend. When coupled with WPM's extremely favorable output growth outlook, I believe we will see a much higher stock price in the years ahead.

As such, I put WPM on my watchlist today, I would like to add it on a correction - depending on my cash situation.

Takeaway

Gold has been a strong performer, supported by macroeconomic factors like lower rates and rising geopolitical risks.

While physical gold is a great investment, I prefer flexibility and safety, so I prefer investments in streamers like Wheaton Precious Metals.

Unlike traditional miners, Wheaton's streaming model offers high margins and lower risks. I believe with its impressive growth outlook and solid balance sheet, Wheaton is well-positioned to benefit from the ongoing bull market in gold.

Although the stock is currently fairly valued, I remain bullish on its long-term potential and would consider adding it to my portfolio during a market correction.

Pros & Cons

Pros:

- High Margins: WPM's streaming model enjoys cash operating margins of nearly 80%, superior to traditional gold miners.

- Reduced Risk: Unlike miners, WPM avoids operational risks by financing projects instead of managing mines directly.

- Strong Growth Outlook: With proven reserves, a solid pipeline of projects, and low-risk jurisdiction exposure, WPM is set for significant output growth.

- Dividend Stability: Despite a modest dividend yield, WPM's dividends are well-supported by its high profitability and commitment to higher future shareholder distributions.

Cons:

- Valuation Concerns: WPM trades at a high multiple, currently at a P/E ratio of 45.9x. Although a "high" multiple is warranted, I would like to see a correction.

- Yield: The 1% yield isn't exciting, especially if you're looking for higher income from your investments.

- Gold and Silver Price Volatility: Fluctuations in gold and silver prices can impact WPM's revenues and stock performance, exposing investors to market volatility.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.