QQQE: How NVIDIA's Result Could Continue Shifting The Landscape For Equal-Weight

Summary

- QQQ is a market-cap weighted ETF heavily influenced by the Mag 7 mega-caps, which has delivered well up to now.

- However, as the AI landscape continues to shift and the focus turns on monetization, there are pains ahead.

- This was demonstrated by the volatility in the aftermath of NVIDIA's financial results.

- Hence, QQQE's equal-weight approach makes more sense to reduce concentration risks and for diversification purposes.

- This thesis makes the case for further upside while adopting a cautious tone as shifts are normally accompanied by volatility risks.

Vertigo3d

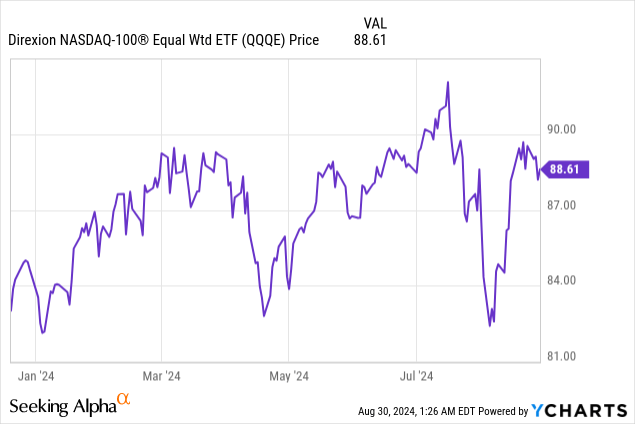

Since I last covered the Direxion NASDAQ 100 Equal Weighted Index Shares ETF (NASDAQ:QQQE) in my bullish thesis on December 20 last year, it has returned nearly 6.75% and is trading at $88.6 as shown below. While this is not a significant gain, it still shows the rotation away from the Magnificent 7 (Mag 7) group has started, as I detail further.

This thesis aims to show that the momentum could continue thereby making a case to invest in the equal-weighted fund instead of the market cap-weighted Invesco QQQ Trust ETF (NASDAQ:QQQ) for those wanting to gain exposure to the AI theme as the landscape continues to shift and the focus turns on monetization as I had elaborated in a recent piece.

In this context, NVIDIA's (NASDAQ:NVDA) second quarter 2025 (FQ2-25) financial results released on Thursday should provide further impetus to this shift, and, its earning call is instrumental in understanding what lies ahead.

The Picture Painted by NVIDIA's Earnings Call

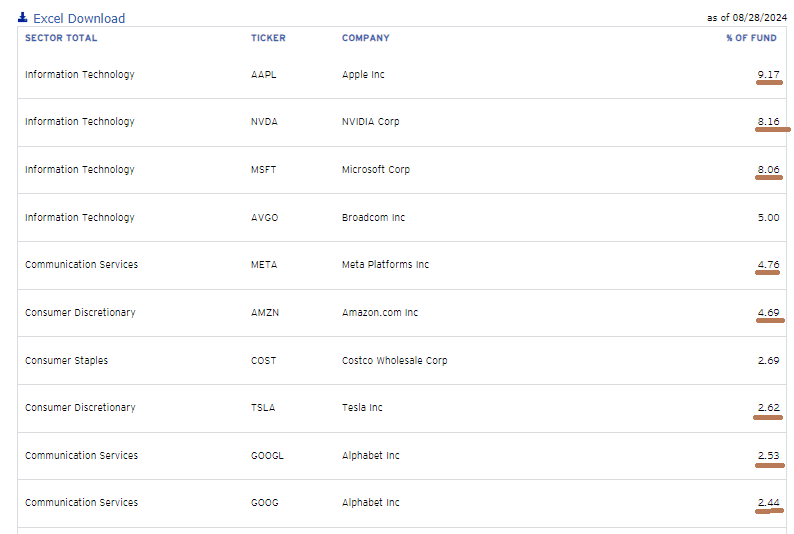

First, as the leading Mag 7 stock and forming part of QQQE’s top holdings as shown below, NVIDIA beat both the top line and bottom line as has been the case for the past seven quarters, but its Data Center revenue decelerated both on a sequential and year on year basis. This slowness for a segment that includes the flagship H100 GPU, the very building block for the AI infrastructures that support intelligent apps could be temporary as the guidance (midpoint) for the third quarter is above what analysts were expecting. However, the stock subsequently falling by over 8% suggests that investors are either not convinced or taking some time to make sense of the results.

Top holdings with Mag 7 stocks underlined in brown (www.direxion.com)

This this end, the earnings call revealed that the spending made by cloud service providers accounted for 45% of NVIDIA’s Data Center segment's sales in FQ2, which is consequent as it was about the same (mid-40s) as during the first quarter. Still, this should continue to rise as according to analysts at Barclays PLC (BCS), these CSPs which include the big cloud providers or hyperscalers will see their capex spending for 2024 and 2025 reach $218 billion and $251 billion respectively which is huge.

These hyperscalers include Alphabet (GOOG), Amazon (AMZN), Meta Platforms (META), Microsoft (MSFT), and Oracle (ORCL) without forgetting Tesla (TSLA) which may not be a CSP but still has big plans when it comes to spending money on AI infrastructure building for making cars more intelligent. Hence, it should purchase 85K GPUs with 35K GPUs already secured, with these estimated at $10 billion.

These billions of dollars spent raise the question of ROI, as I had highlighted in my earlier thesis on QQQ, especially since you consider that these mostly consist of only accelerated chips (Hopper and Blackwell-based) used for the training and inference (usage) of Generative AI models. However, about 22 months after the launch of ChatGPT by OpenAI, it is time to think about revenue-generating services.

Monetization Could Take Time and take a Toll on Investor Patience

In this case, the application ecosystem is not growing fast apart from new bright spots like ChatGPT and Adobe (ADBE) and a few others, most apps are available for free on the internet. Microsoft as a major investor in OpenAI has innovated with Copilot but this is on top of its Office 365 product line. Similarly, Google is also charging users for access to gen AI features as add-ons to its office productivity software suite. Looking further, Amazon plans to release paid Gen AI-based Alexa in October. Now these services are subscription-based (SaaS) meaning that can take 0.9 years to 2.5 years to achieve payback. Furthermore, hyperscalers Amazon, Microsoft, and Alphabet also make money by leasing GPUs to a multitude of smaller companies but this is again done using a subscription-based (IaaS) model that typically takes around four to five years.

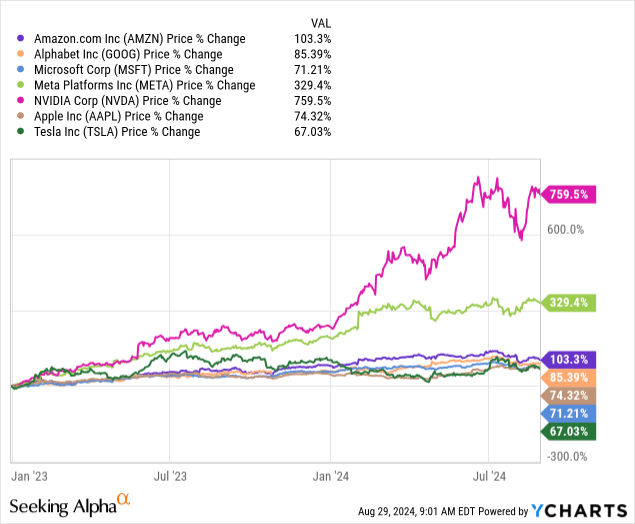

This means the bulk of the effort and financial resources is dedicated to building AI infrastructure with Gartner estimating that the area of IT spending to grow the most is data center systems at 24.1% again implying that monetization, or making money by selling services is likely to take time. The problem is that investor patience tends to run out especially because Mag 7 stocks have gained 67% to 759% since January 2023, or a few weeks after the advent of ChatGPT, showing the level of hype associated with AI.

Data by YCharts

Data by YCharts

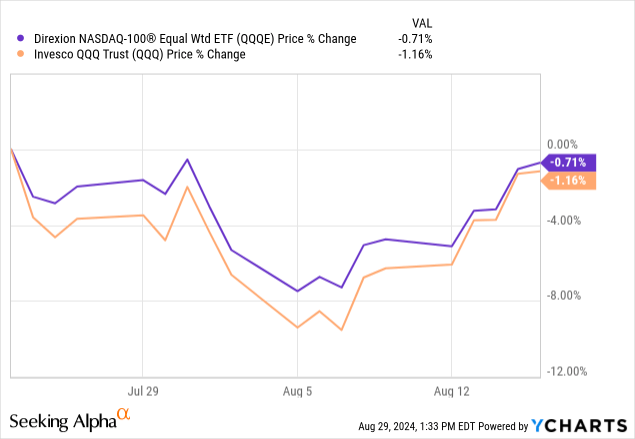

As a reminder, there have been signs of weakness for Tesla, Alphabet, and Amazon when they reported results in the last week of July which caused QQQ to dip below QQQE as shown in the chart below. This was because when mega-caps reported results, the scrutiny was on the AI investments, especially the GPUs, and how these would translate into sales with investors no longer satisfied by strong management rhetoric. Talking figures, analysts at BofA, have estimated AI capex by some of the hyperscalers to surge by 9 times for every dollar of sales, something uneconomic unless proven otherwise.

Eventually, QQQ recouped its losses in the second week of August thanks to strength seen in the stocks of Apple and Microsoft as well as fears of a recession starting to emerge in the first week of August, which tends to favor the Mag 7.

Data by YCharts

Data by YCharts

The Bull Market for AI Hardware is Over As the Fed Eases and the Focus Shifts to Software

However, more recently it is the opposite, with fears of a U.S. recession receding after weekly jobless claims fell on August 29, when the stock market rallied despite NVIDIA losing value, showing that investors may be diversifying away from mega-caps. However, one can argue such a move should be sustained, but three drivers could make this happen.

First, as touched upon earlier, economic prospects becoming less uncertain is good for corporate and consumer spending alike. Second, monetary conditions are likely to improve with the Federal Reserve likely to start cutting interest rates next month. This favors stocks whose balance sheets are not as cash-rich as the Mag 7, or smaller caps which tend to rely more on borrowing to finance investments. Thus, with the costs of borrowing being lowered, they can access external financing to expand, thus driving revenue growth.

Third, it is about the IT value chain. Up to now the AI theme has mostly benefited hardware players, chip designers, manufacturers, OEMs, data centers, and network suppliers. Here, after NVIDIA's superfast GPUs are used to build the infrastructure, and the AI models are trained, comes the software development part, to develop apps to be monetized.

Again coming back to NVIDIA’s management comments, there is mention of companies like ServiceNow (NOW), and SAP SE (SAP) just to name a few leveraging Gen AI. Digging further, according to a report by Atlassian (TEAM) which forms part of QQQE's holdings, inefficiencies in software development can be corrected with Gen AI which can boost productivity by 20%-50% depending on the complexity of the task being optimized.

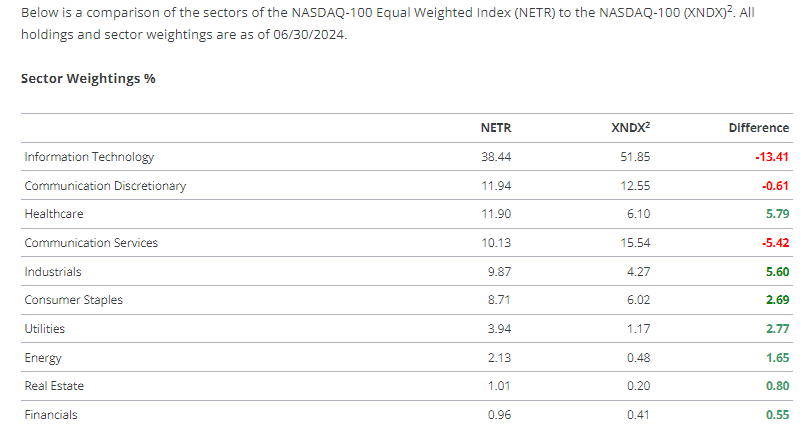

In this respect, the QQQE's advantage is that in addition to being less concentrated in terms of mega-caps, it provides exposure to many software names, including Adobe. Also, as shown below, 11.9% of its weight is dedicated to Healthcare, a sector where according to NVIDIA’s CFO, AI is revolutionizing medical imaging and drug discovery driven by the company's rich software ecosystem which simplifies AI model development.

www.direxion.com

QQQE is Better than QQQ in the Diversification Versus Concentration Debate

Thus, as the market landscape continues to shift, it is time to move away from QQQ whose weight is dedicated to Mag 7 at 42.4% as pictured below.

www.direxion.com

Moreover, over 50% of its weight is concentrated in its first ten holdings as shown below, compared to only 12% for QQQE. With an equal-weighted approach and tracking the NASDAQ-100 Equal Weighted Index or NETR, the Direxion ETF mitigates risks by more evenly spreading its assets across its holdings.

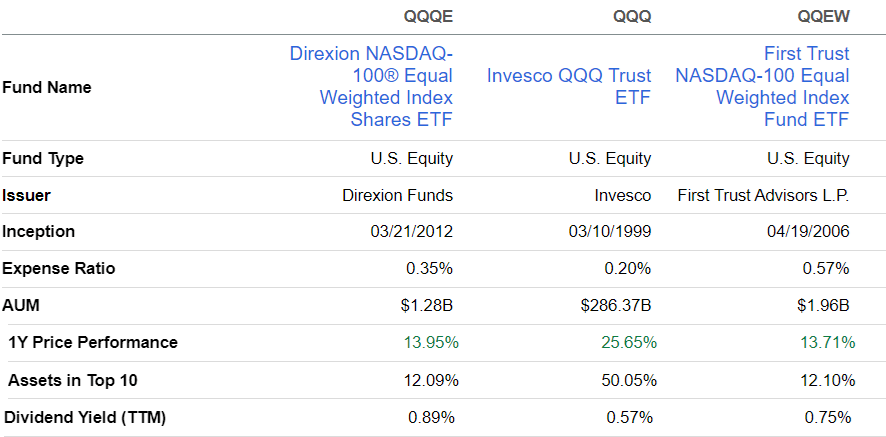

Looking across the ETF space for an alternative, there is also the First Trust NASDAQ-100 Equal Weighted Index Fund ETF (QQEW) but it comes with a higher expense ratio and pays less dividend.

seekingalpha.com

Now, QQQE charges higher fees than QQQ but let us not forget that it is a more active fund in the sense that the managers have to constantly adjust the weight of the holdings, either through sales or purchases of shares so they do not exceed the 1% threshold, done quarterly.

Emphasizing the diversification rationale, by investing in QQQE instead of QQQ, the idea is to remain invested in tech and AI but in a less concentrated way while gaining exposure to a wider spectrum of stocks, which carry more weight across sectors other than IT. On a cautionary note, this diversification approach has meant lower returns as shown by the one-year price performance above, but this period covered the bull market where those involved in supplying the chips and building AI infrastructure outperformed. However, as seen in July and more recently by NVIDIA’s stock volatility in the aftermath of earnings, Mag 7 has lost its luster.

Furthermore, for the sake of clarification, this thesis does not make the case for the bull market to end, but instead for a new stage in AI development involving leveraging the technology to generate sales and profits. Thus, for investors looking to capitalize on the growth of large and medium caps, it makes more sense to opt for QQQE instead of QQQ. In this context, the Direxion ETF should continue progressing since at $89.33, it still trades below my previous target of $93.56 by 4.7%. Also, its P/E of 24.98x has now moved above its December value of 20.81x but remains underpriced relative to QQQ's P/E of 27.52x by around 11%.

Finally, it could potentially move higher by 11%, but I maintain a target of $93.56 as again coming back to NVIDIA, volatility should persist during future results announcements. The reason is the deceleration in its Data Center segment which grew at an astounding pace of 154.6% YoY during FQ2 potentially continuing because Gartner expects data center systems to grow by only 24% this year.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.