BITO's Underperformance Is Likely To Continue

Summary

- We think BITO is inferior to other spot-based BTC products due to the fund's high expense ratio and futures-based approach to getting crypto exposure.

- High transaction costs, liquidity constraints, and a uniquely inefficient 'rolling' mechanic should cause structural underperformance vs. the underlying going forward.

- Despite some niche use cases, BITO's structure results in substantial performance drag, making it a sub-optimal long-term investment.

- We re-iterate our 'Sell' rating on BITO.

Torsten Asmus

In February of this year, we wrote an article titled, "BITO: Why Bother?".

The point of the article was simple - in an age of newly legalized Spot Bitcoin ETFs, why invest in the inferior, futures-based alternative?

In years past, ProShares Bitcoin Strategy ETF (NYSEARCA:BITO) might have made sense as an investment, as it was one of the only ways to get price exposure to Bitcoin in a traditional brokerage account.

However, as new products have come onto the scene - many of which that feature lower fees, less tracking error, and better tax treatment - it's been getting harder and harder to see where this fund fits into a modern portfolio.

Today, we wanted to re-visit and re-iterate our initial thesis on BITO, cover the fund's recent performance, and highlight why we think the ETF is poised to underperform its underlying cryptocurrency well into the future.

Let's jump in.

How BITO Works

In case you missed our initial article, BITO is a Bitcoin-tracking ETF that is meant to give investors exposure to the price of Bitcoin through a fully regulated product.

The Fund invests into Bitcoin Futures, which meet regulatory approval and are traded on the Chicago Mercantile Exchange (CME).

Here's more info on this setup, directly from the horse's mouth:

ProShares Bitcoin Strategy ETF (the "Fund") seeks investment results, before fees and expenses, that correspond to the performance of bitcoin. The Fund currently seeks to achieve this objective primarily through investments in bitcoin futures contracts. The Fund does not invest directly in bitcoin.

CME's futures began trading in late 2017, but it took several years - all the way until the end of 2021 - for BITO to launch.

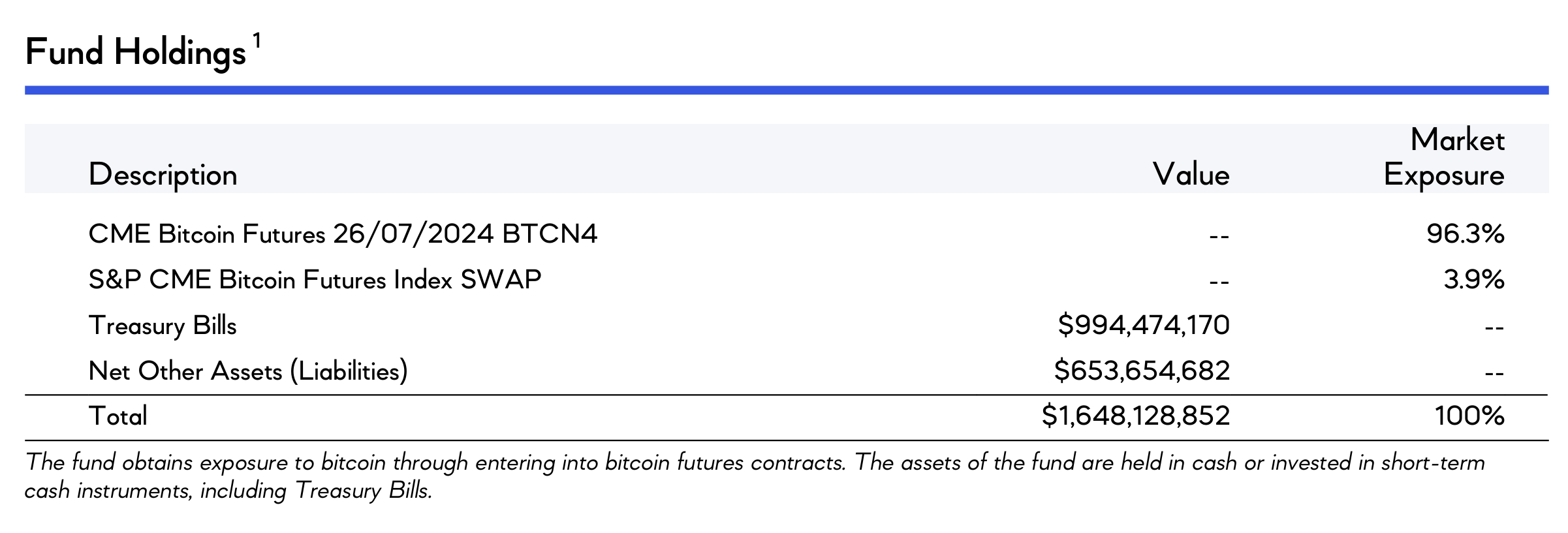

As we just mentioned, the fund buys and holds Bitcoin futures, and here you can see the fund's positions as of Q3 2024:

ProShares

This shows that the fund is primarily invested into treasuries and other cash-like instruments, and then it uses those positions as a margin to fund futures positions that roll every so often as the futures expire.

Problems With BITO

As we see it, there are three key problems with BITO's structure: Transaction Costs, Taxes, and the Expense Ratio. Let's dig into each of these.

First off, BITO, as a futures-oriented fund, pays a lot of fees in transaction costs that get subtracted from your returns as an investor.

As a billion-dollar+ fund, BITO has significant liquidity constraints that drive costs up. Larger trades lead to wider spreads and less efficient pricing vs. the market.

Additionally, given that BTC futures are mostly in contango, the fund will consistently 'sell low' and 'buy high' the core asset, which leads to additional costs:

TradingView

Here's more info on this from the prospectus:

Futures contracts with a longer term to expiration may be priced higher than futures contracts with a shorter term to expiration, a relationship called "contango." When rolling futures contracts that are in contango, the Fund will sell the expiring contract at a relatively lower price and buy a longer-dated contract at a relatively higher price.

Finally, the inbuilt trading increases base commissions and transaction costs, which eat into profits.

Between rolling costs, liquidity constraints, and commissions, BITO has a very high-cost structure that is built into the DNA of the fund.

This leads to severe tracking errors, which is something we'll look at in the performance section in a minute.

Aside from the transaction costs, BITO's 'rolling' procedure can create monthly, mandatory distributions to investors that are taxed as ordinary dividends, not qualified dividends.

That means that unless you hold this fund in an IRA, your otherwise unrealized investment gains are crystallized on a monthly basis and shipped back to you to be taxed, which creates a huge drag over time.

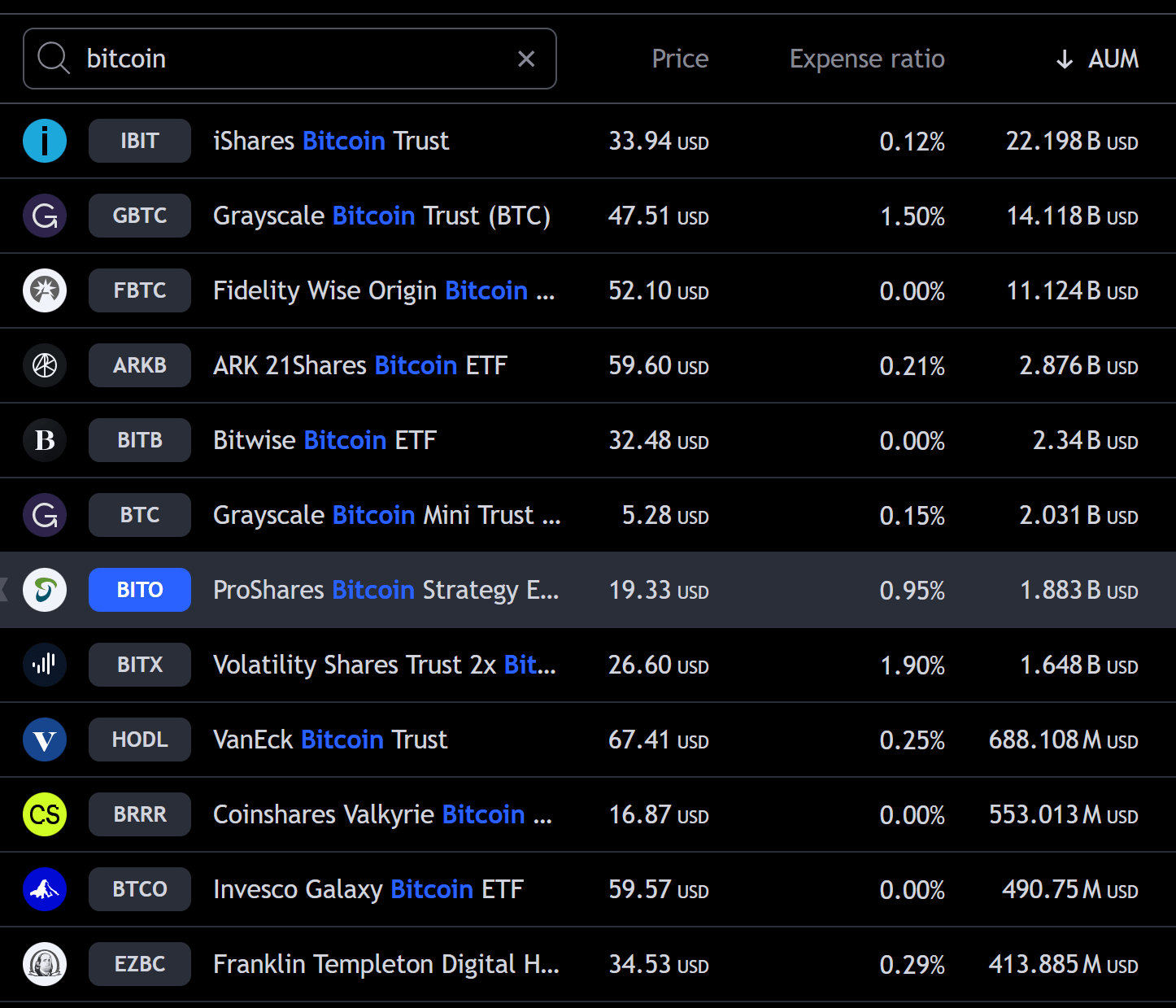

Lastly, BITO's expense ratio stands at 0.95%, which is a lot higher than other non-leveraged BTC products on the market today:

TradingView

All of these may seem like 'small things', but added together, and cumulatively over time, it can lead to some pretty big differences in performance that we'll take a look at now.

BITO's Performance

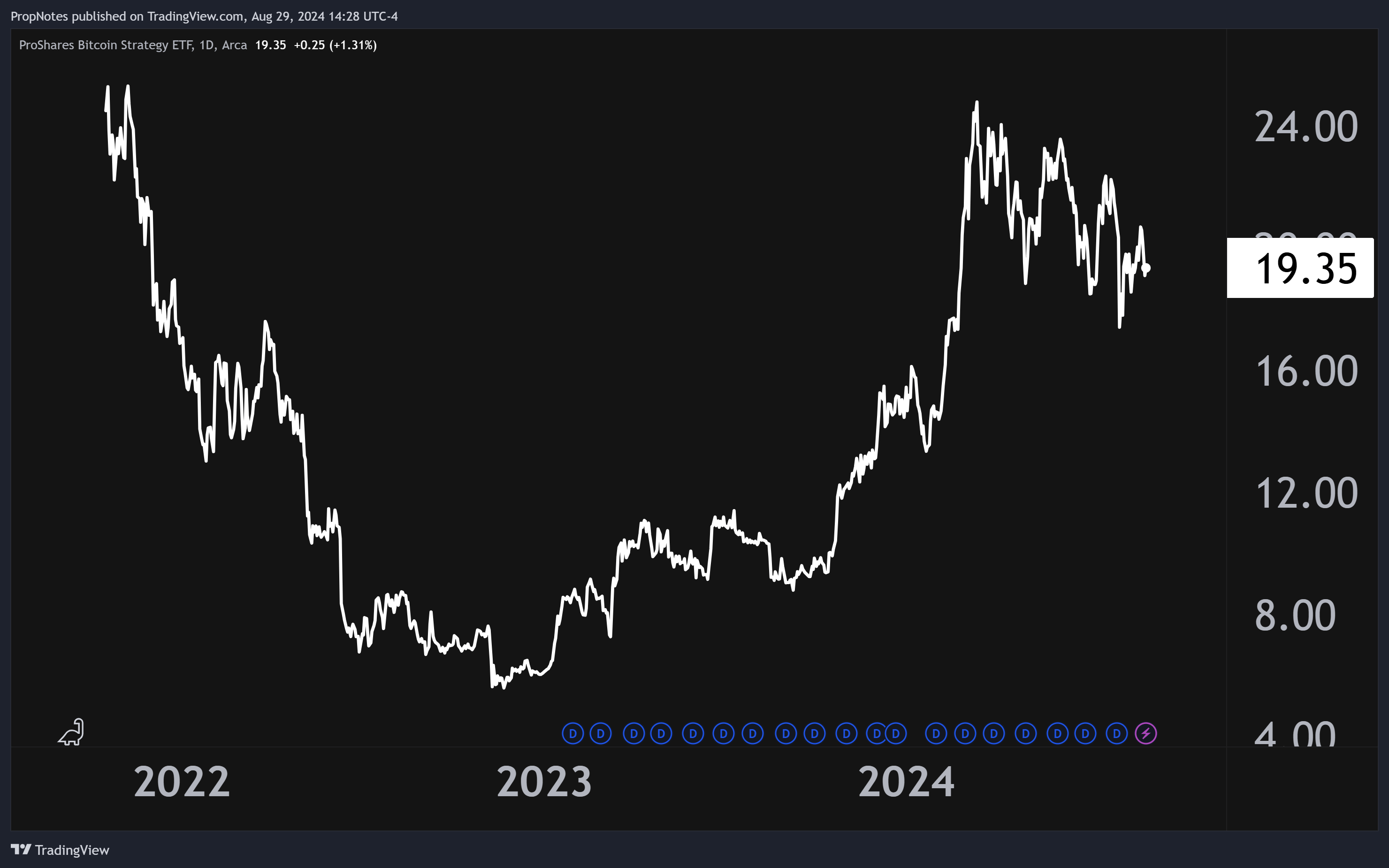

If you're just looking at BITO on a standalone basis, the performance looks somewhat familiar to a regular BTC chart.

Launched in 2021, the fund's performance suffered through the crypto bear in 2022, and has since perked up as BTC has done better through 2023 and 2024:

TradingView

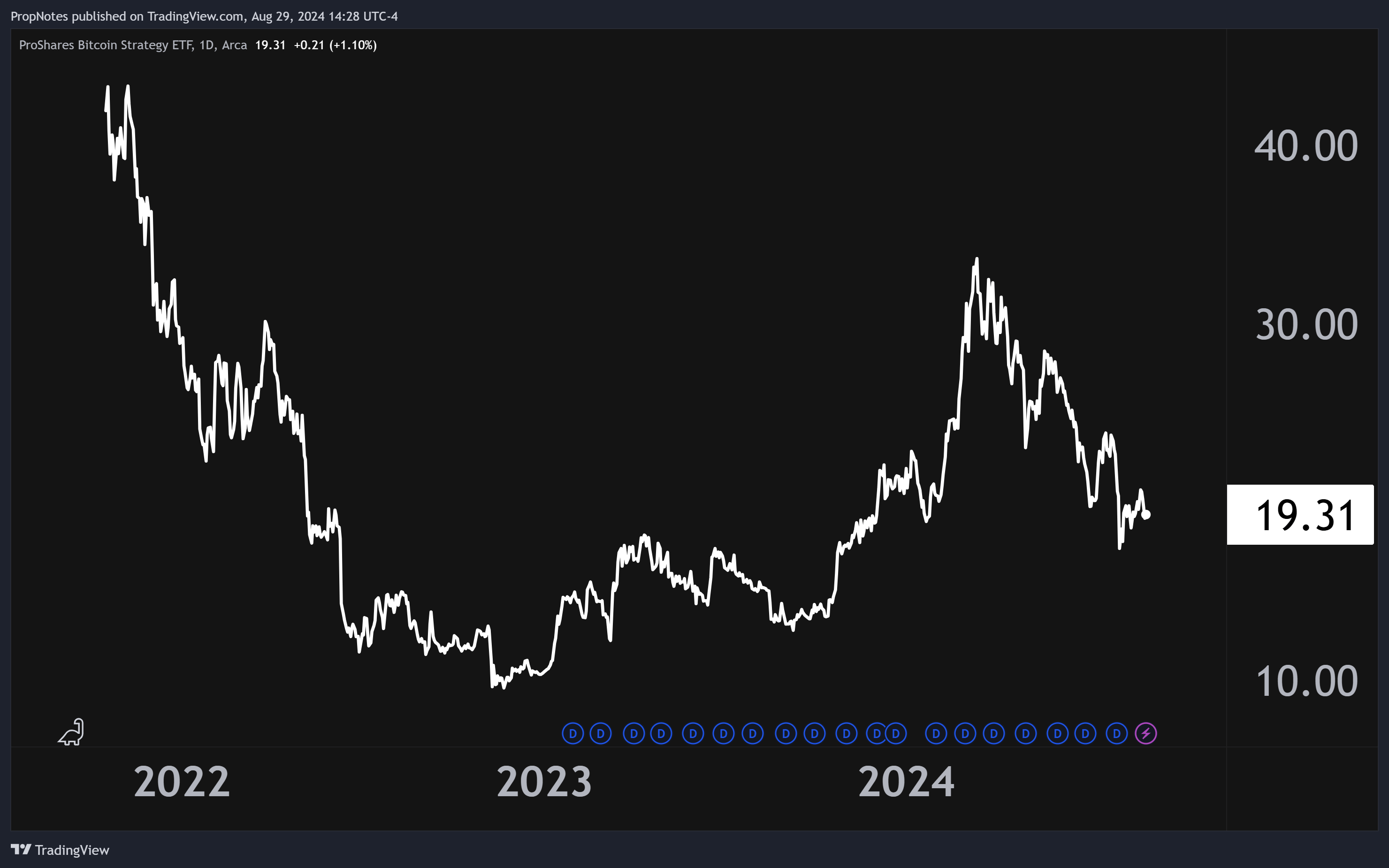

Of course, this takes distributions into account. If you're not re-investing these dividends, then your position is down quite a bit since inception:

TradingView

That said, some of the issues don't come out until you dig in and begin comparing the fund's performance over time to other assets.

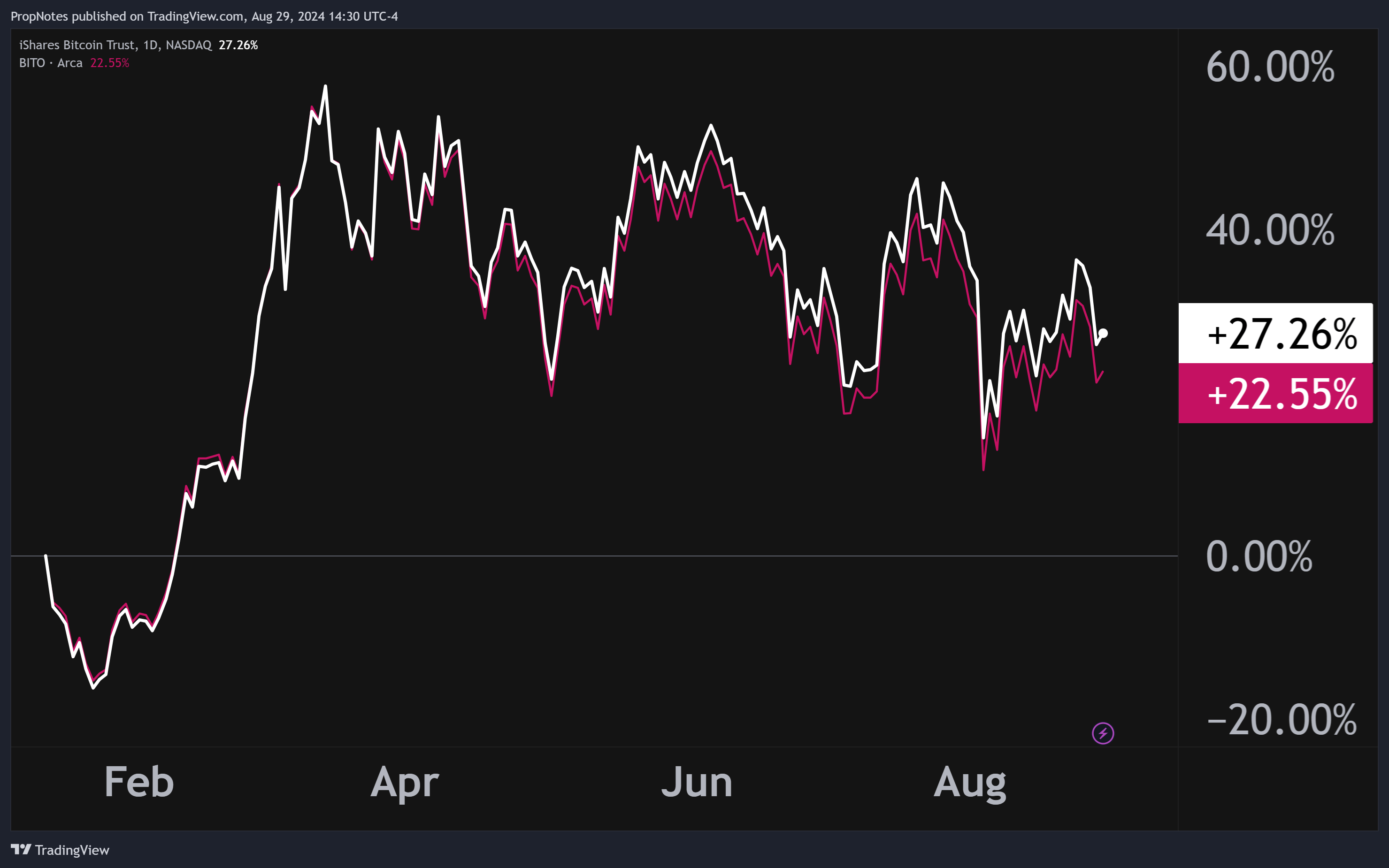

Remember those transaction costs we talked about? Year-to-date, they haven't been too bad, and BITO is tracking IBIT pretty closely over time, with only a 5% tracking error:

TradingView

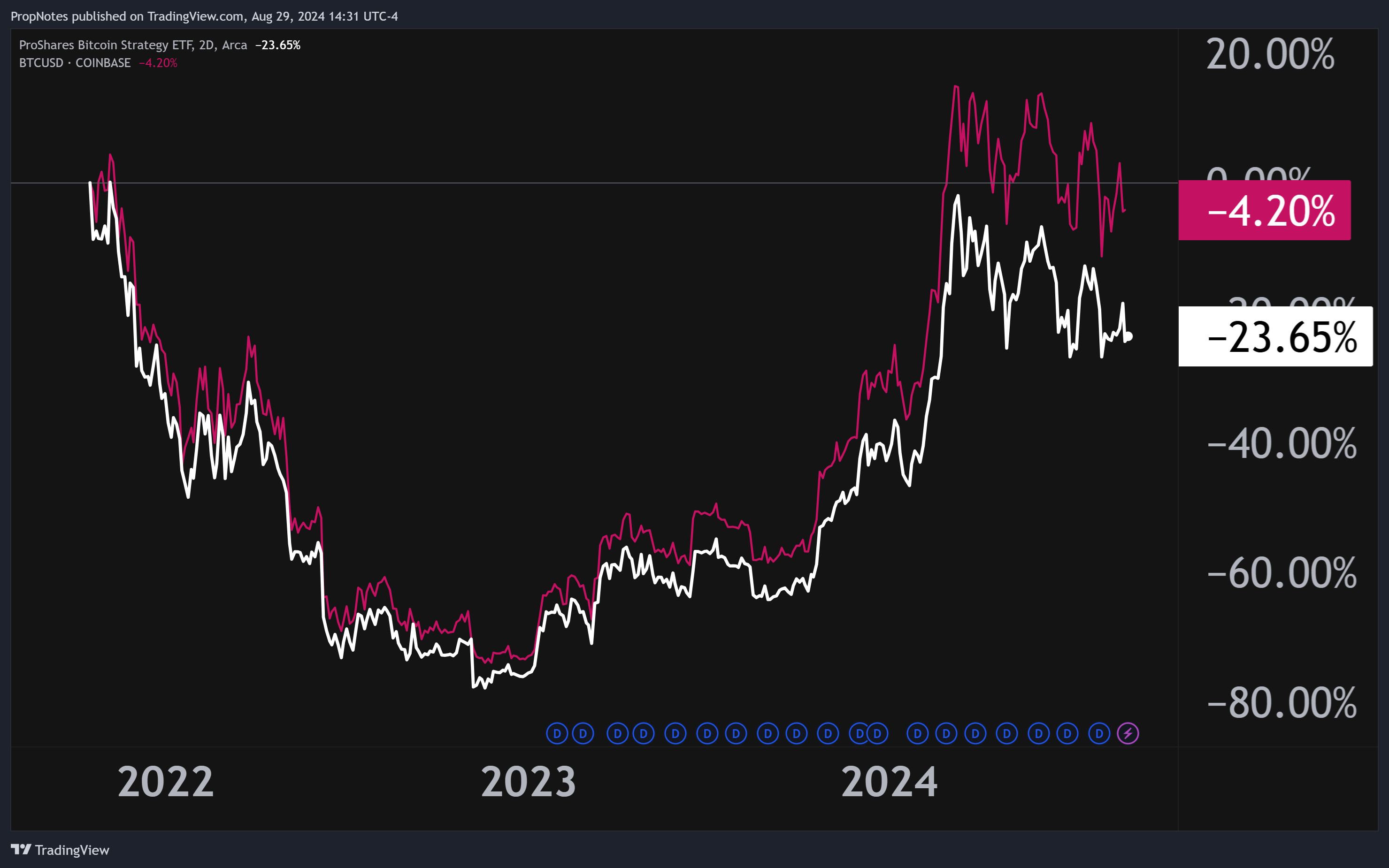

That said, if you zoom this out and compare BITO to BTC's spot performance since the end of 2021, the difference is a lot starker:

TradingView

Same instrument, same index, same underlying instrument.

The only difference here is how BITO's transaction fees and distributions cause significant tracking errors over time vs. the underlying target.

If you were to invest $100,000 into BITO and spot bitcoin from inception, BITO's costs would have eaten up about $19k in performance difference over time, given the ~1900ish bips of differential.

That's also not taking into account taxes, which may have compounded this effect.

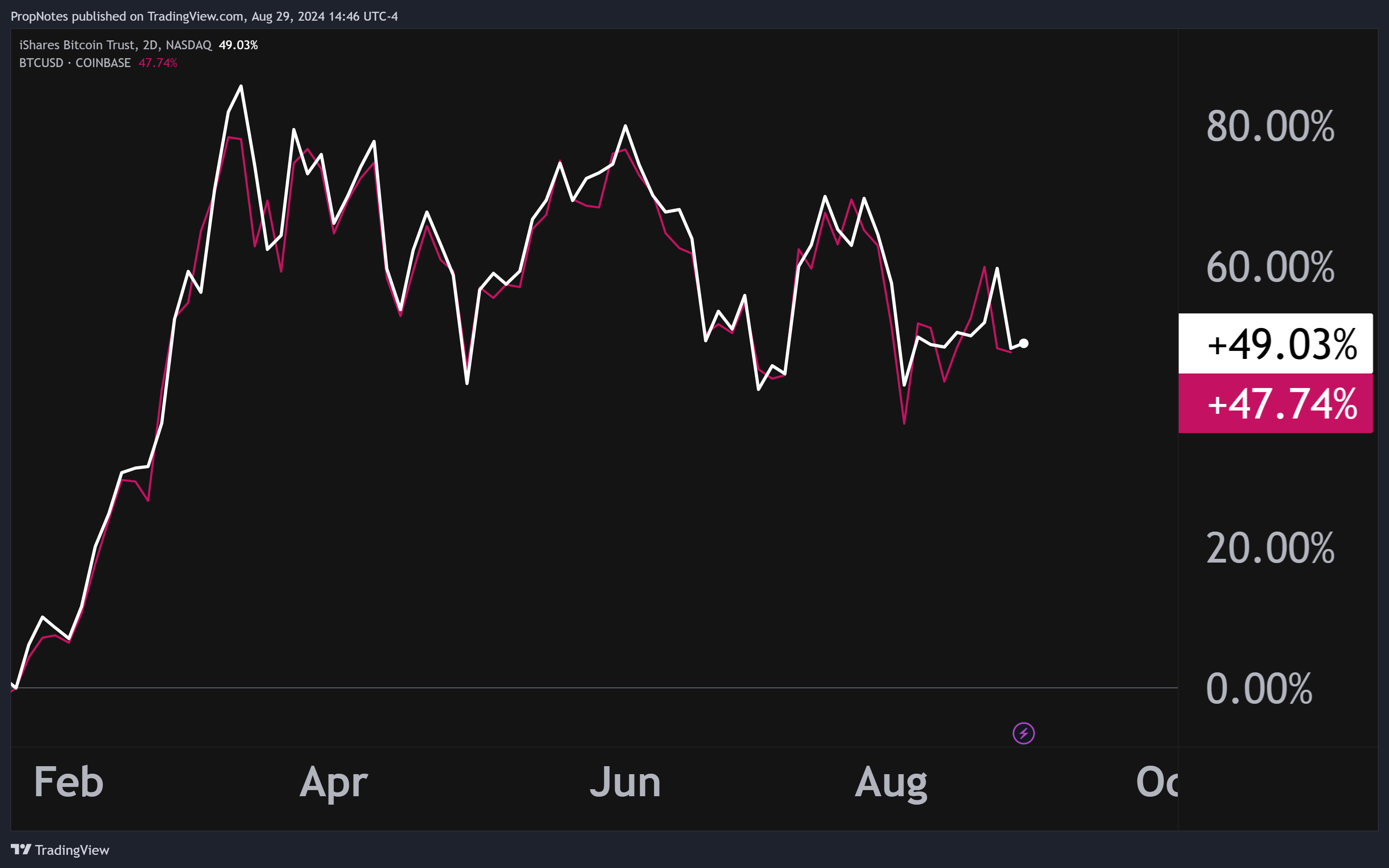

IBIT, the iShares spot product, has tracked spot bitcoin almost perfectly since inception, by contrast:

TradingView

Given the availability of better, cheaper, wrappers for investing in BTC, it's hard to label BITO as anything but a 'sell'.

To be clear - we're not saying anything about BTC in and of itself, but BITO, as a wrapper, we think is a poor long-term instrument.

Can BITO Be Useful?

Despite all of the issues we see with BITO, there are still two scenarios in which BITO might be the best choice.

First off, BITO uses regulated futures, which means that the funds are locked up and safe within the fund structure.

With IBIT and other products, they buy spot bitcoin directly, typically through a centralized exchange. This means that IBIT and other buyers are outsourcing their asset security to Coinbase (COIN) (or other custodians), which have hacking risk. In the event that COIN gets hacked, it's likely that BTC would drop substantially in price, but it would leave BITO shareholders better off vs. those in IBIT that may have seen their funds fully withdrawn away.

There are some insurances to protect against this, but it's tough to know how and when those would pay out in the event of a catastrophe.

The other use case is for leveraged speculation.

Right now, BITO is one of the only non-leveraged BTC instruments that has options trading enabled. The SEC hasn't yet approved options for spot bitcoin ETFs, which means that if you're looking to hedge, speculate, or run an income strategy on BTC exposure in a regulated environment, BITO might be your best option (no pun intended).

Summary

All in all, though, despite the niche use cases, we think BITO appears to be a sub-optimal medium- or long-term investment product as a result of the fund's high fee structure and suboptimal tax treatment, which will likely cause continued tracking error over time vs. the underlying.

This leaves us no room to do anything but re-iterate our 'Sell' rating.

Stay safe out there!

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.