Taylor Morrison Home Corporation: Despite Weaknesses, Picture For The Business Is Bullish

Summary

- Taylor Morrison Home Corporation has seen significant stock appreciation despite mediocre financial performance, driven by undervaluation and a growing backlog of home orders.

- Revenue, profits, and cash flows have declined due to high interest rates impacting home prices, but the company remains attractively priced compared to peers.

- Improved cancellation rates and a potential future cut in interest rates could boost housing demand and home prices, supporting a continued 'buy' rating.

jsnover

One company that I have been consistently bullish about over the past few years is homebuilder Taylor Morrison Home Corporation (NYSE:TMHC). With a market capitalization as of this writing of about $7.1 billion, the company is rather sizable. But it hasn't always been this large. Since I last wrote a bullish article about the company in May of this year, the stock has risen by 15.9% while the S&P 500 is up only 5.8%. And since I first rated it a ‘buy’ back in January of 2022, shares have skyrocketed 125.9% while the S&P 500 has risen only 28.4%.

The performance achieved by the company is a real demonstration of successful value investing. You would think that the company would have been exhibiting tremendous growth during this time. But the fact of the matter is that financial performance has been somewhat mediocre. There are some bright spots, such as growing backlog and year-over-year increases in new orders for homes. Those suggest that good times lie ahead. But revenue, profits, and cash flows have been shrinking for a while. The reason why the market has largely ignored this is because shares were tremendously undervalued. And even today, the stock is cheap compared to most similar enterprises. Given this and considering what likely lies around the corner with interest rates, I do think that keeping the company rated a ‘buy’ makes sense for now.

Great upside despite some weaknesses

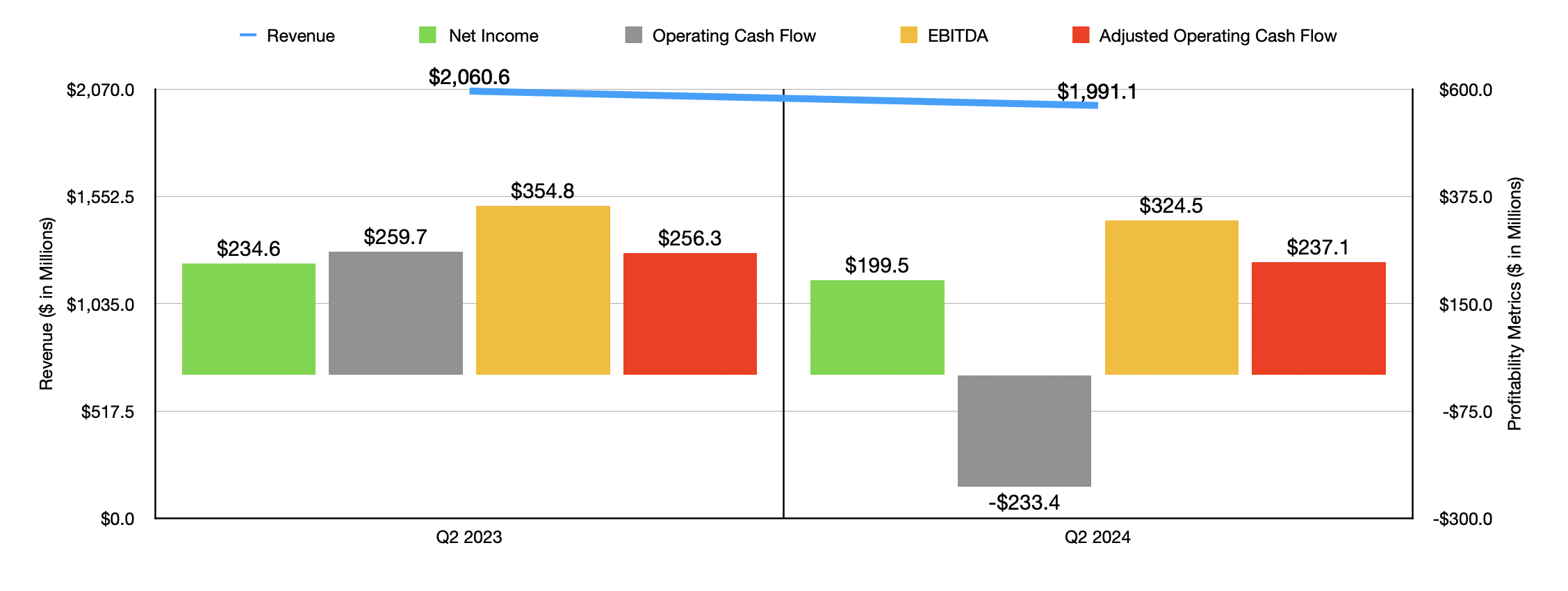

In my most recent article covering Taylor Morrison Home Corporation, I detailed financial performance from 2022 to 2023. My goal is not to rehash those details now. The important thing to keep in mind is that, year over year, revenue, profits, and cash flows, all took a hit. The most recent data that I have regarding the business covers the second quarter of 2024. So that might be a great place to start. During that time, revenue for the company came in at $1.99 billion. This represents a drop of 3.4% compared to the $2.06 billion the business reported just one year earlier.

Author - SEC EDGAR Data

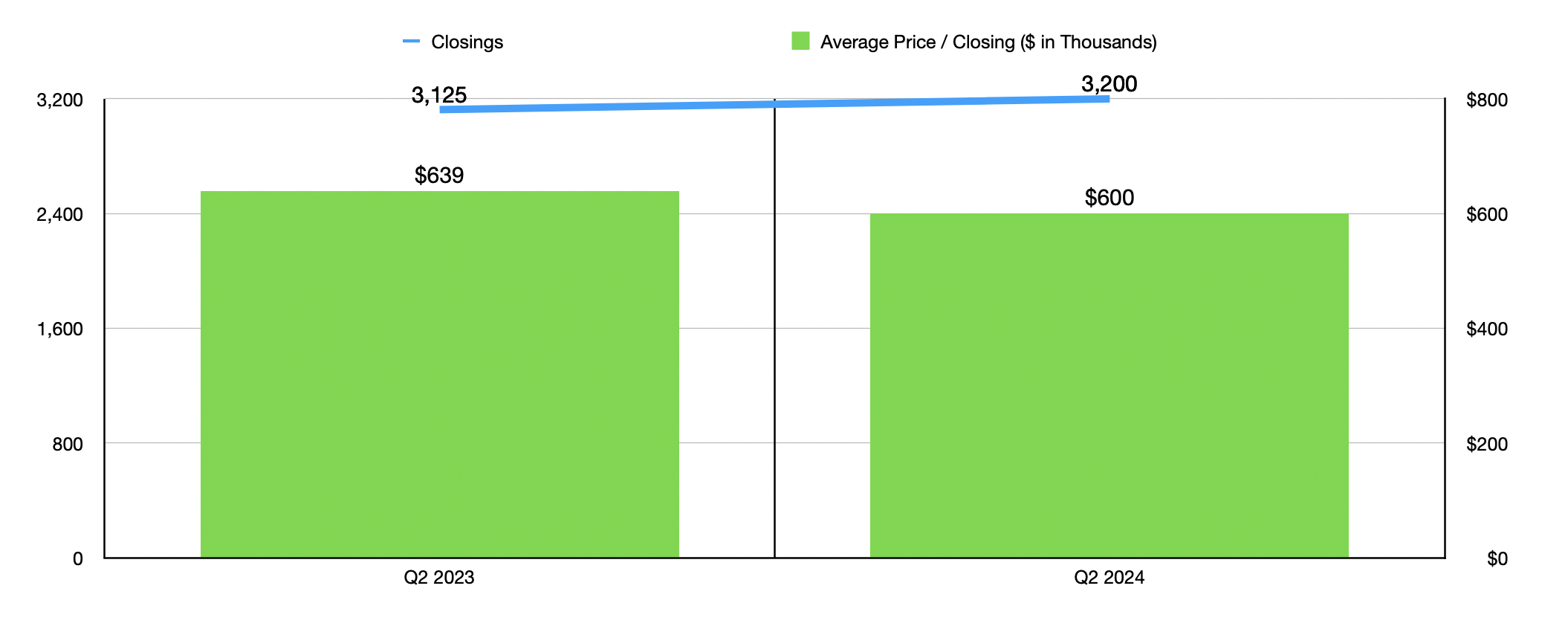

With a company in the homebuilding space, revenue is largely determined by two primary factors. The first would be the number of homes closed on, and the second would be the price at which those homes were closed on. Total closings in the second quarter came in strong at 3,200. That's a modest uptick from the 3,125 reported the same time last year. You would think that this would cause revenue to rise. However, the average price of a closing dropped a year over a year, falling from $639,000 to $600,000. The fact of the matter is that high interest rates have a negative impact on home prices. And right now, interest rates are the highest they have been in decades. Or at least that is what the data shows when it comes specifically to the rates set by the Federal Reserve.

Author - SEC EDGAR Data

With revenue falling, profits have also taken a hit. Net income dropped from $234.6 million in the second quarter of 2023 to $199.5 million the same time this year. The drop in sales certainly contributed to this. But it was also the fact that the drop was driven by price changes as opposed to volume changes that really negatively impacted margins. Other cash flow metrics followed a similar trajectory. Operating cash flow went from $259.7 million to negative $233.4 million. If we adjust for changes in working capital, we get a smaller drop from $256.3 million to $237.1 million. And finally, EBITDA for the company managed to fall from $354.8 million to $324.5 million.

Author - SEC EDGAR Data

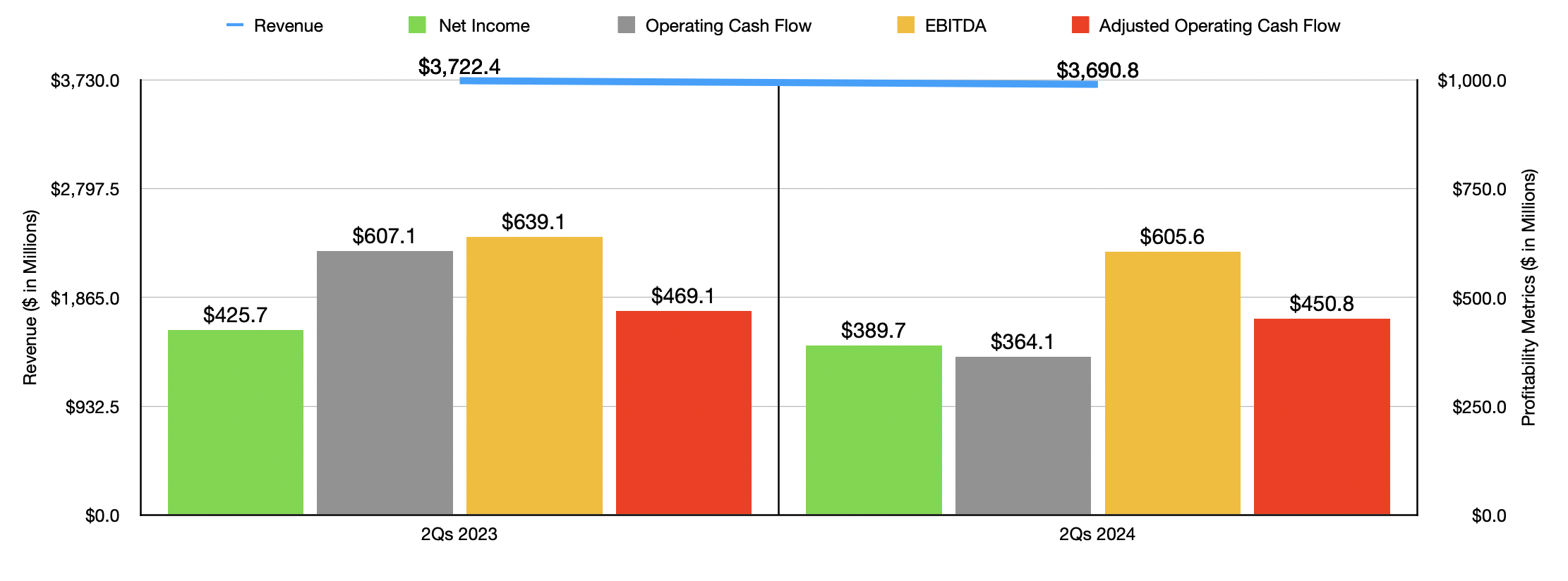

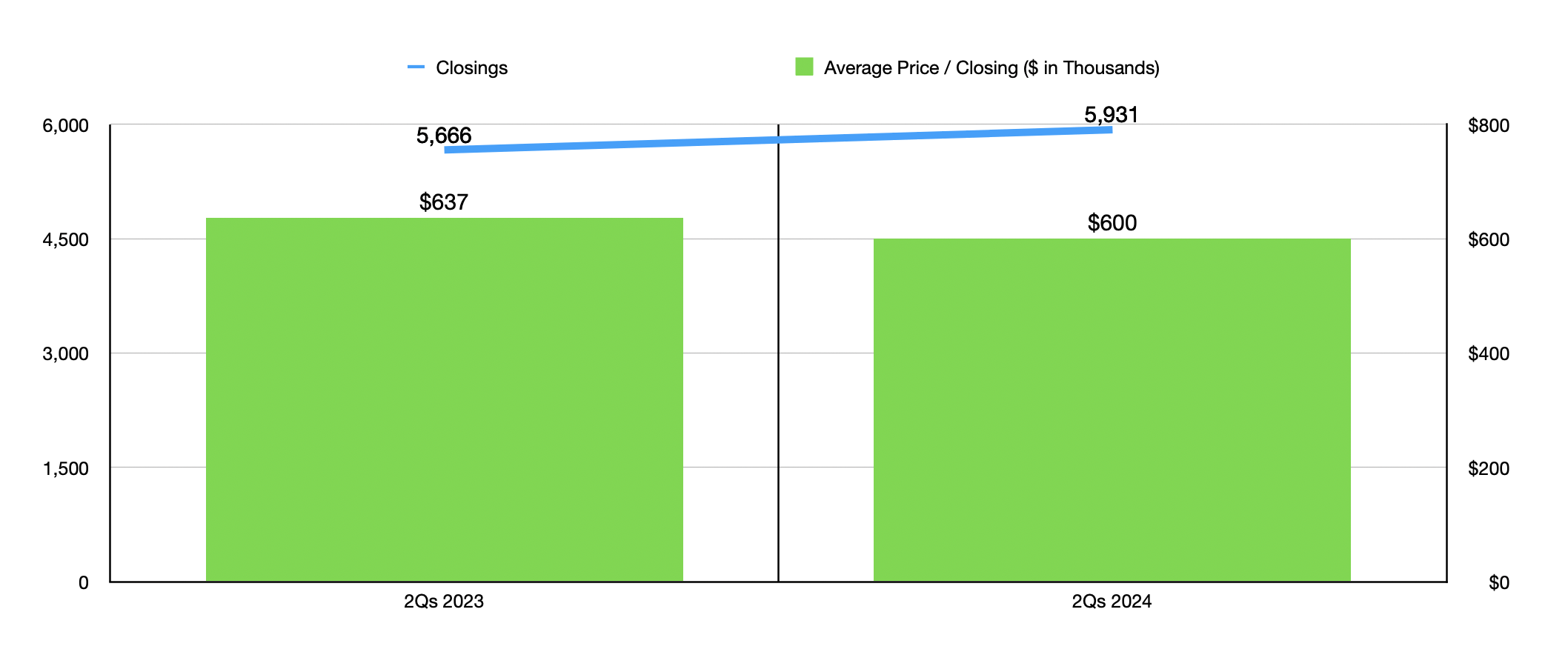

In the chart above, you can see financial results for the first half of 2024 compared to the same time in 2023. As was the case in the second quarter alone, revenue, profits, and cash flows, all took a hit on a year-over-year basis. This was in spite of the fact that the number of home closings jumped nicely from 5,666 to 5,931. Not surprisingly, the pain for the company came from a decline in the average price of a home closed from $637,000 to $600,000.

Author - SEC EDGAR Data

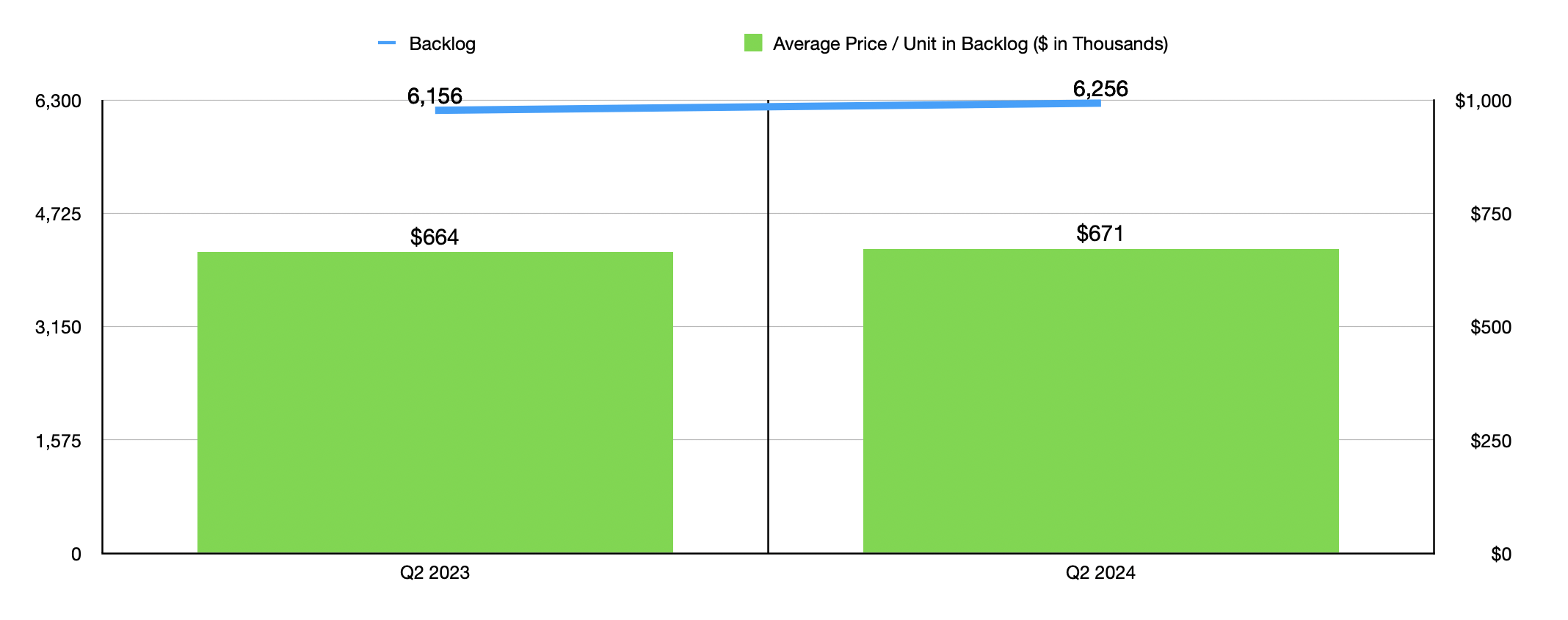

Sometimes, a rise in closings can translate to a decline in backlog. This occurs when new contract orders come in weaker than what closings have been. But that is not what we have seen. By the end of the most recent quarter, Taylor Morrison Home Corporation boasted 6,256 homes in its backlog. This represented an increase over the 6,156 homes in its backlog the same time last year. And even though the average price of a home closed dropped, the average price of one in backlog grew from $664,000 to $671,000.

Author - SEC EDGAR Data

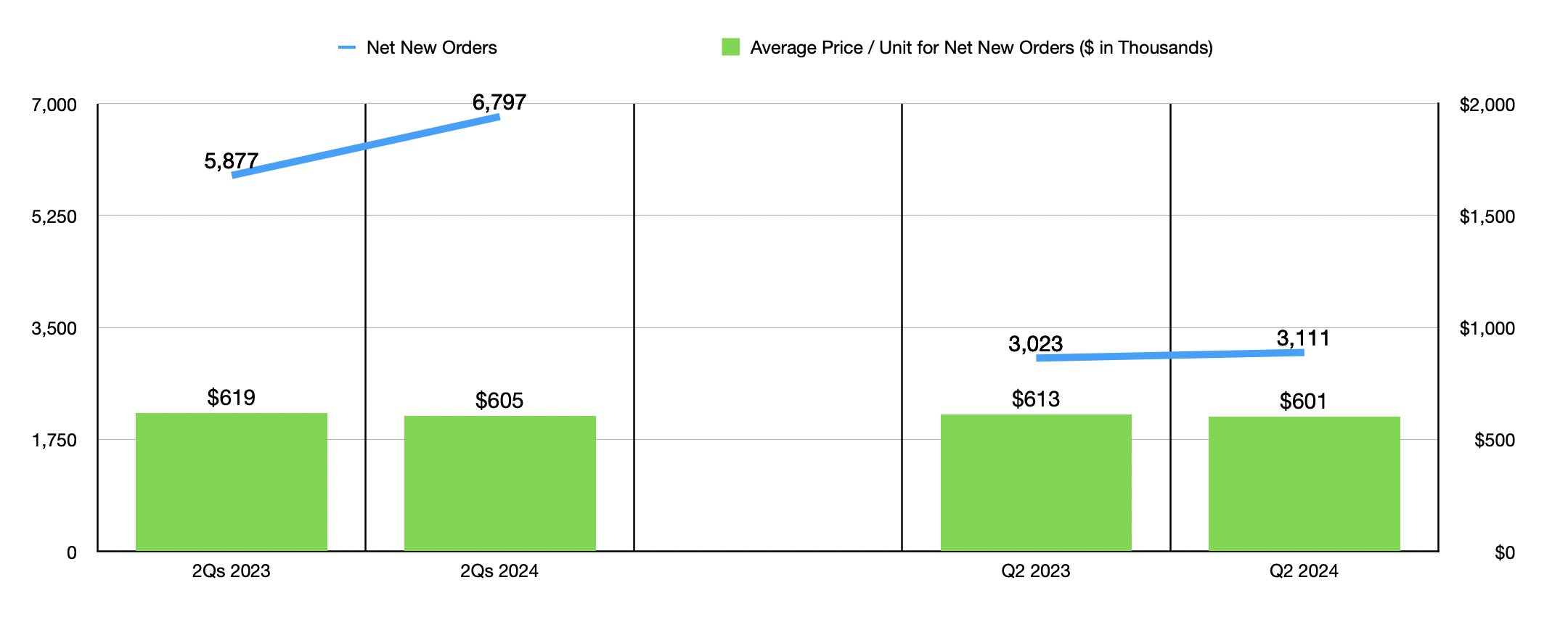

This improvement in backlog was made possible by net new orders in the most recent quarter of 3,111 homes. That is higher than the 3,023 homes ordered the same time last year. Year to date, the improvement was even better, with 6,797 homes ordered on a net basis far outpacing the 5,877 homes ordered the same time last year. Unfortunately, the new contracts coming to the company involve lower priced homes. For the most recent quarter, these homes were valued at $601,000 apiece. That's down from $613,000 reported the same time last year. And for the first six months of this year, the value is $605,000 compared to $619,000 reported for the first half of 2023.

Author - SEC EDGAR Data

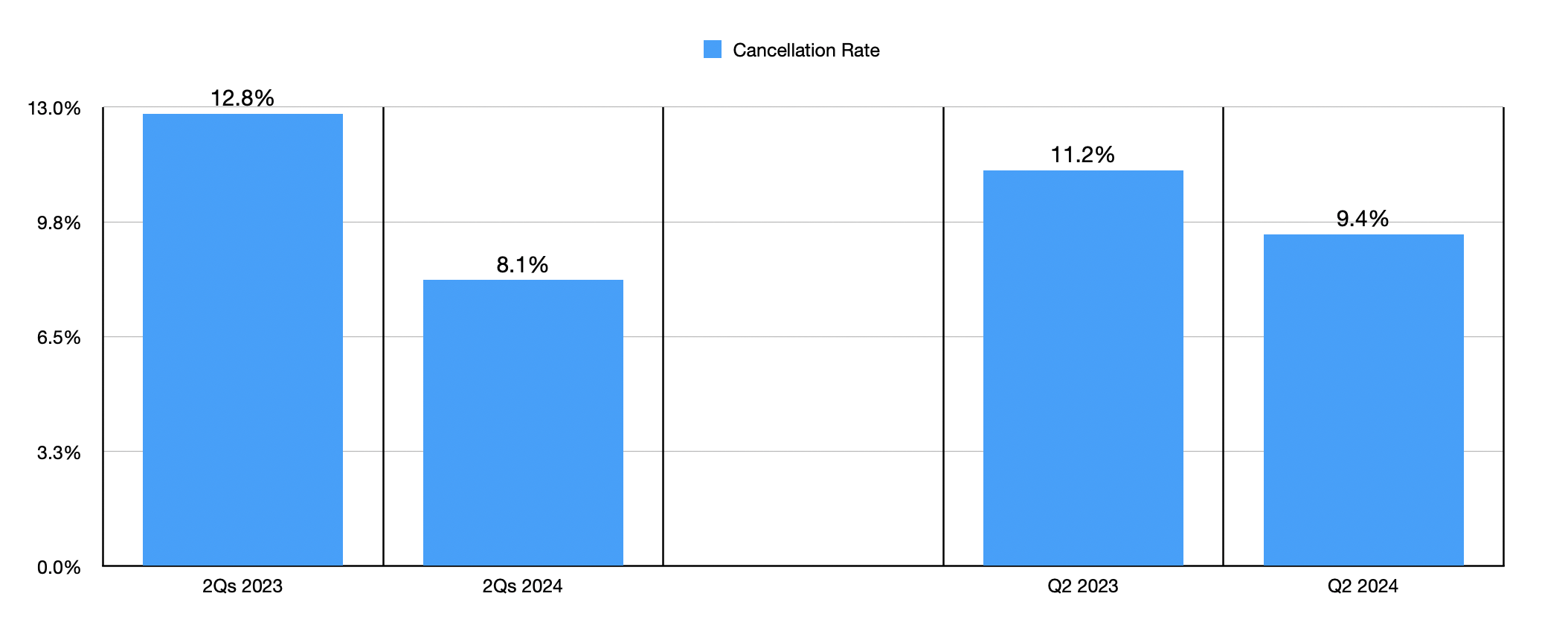

Another thing that has benefited the company has been a meaningful improvement in cancellation rate. Just because a home is ordered does not mean that the buyer will follow through on it. Over the past couple of years, the surge in inflation and the high interest rates aimed at combating that inflation resulted in cancellation rates skyrocketing. Companywide, cancellation rates spiked to 13.5% in 2022. Though in some parts of the country where it operates, this number was higher at 18.5%. And I have seen other homebuilders with rates far in excess of 20%. The good news is that, in the most recent quarter, the cancellation rate was only 9.4%. That's down from 11.2% one year earlier. And for the first six months of this year, the 8.1% reported by management was materially below the 12.8% achieved in the first half of 2023.

Author - SEC EDGAR Data

We don't really have much in the way of guidance when it comes to 2024 in its entirety. Or to be more precise, we don't have what I would like to have. However, management did say that investors should expect between 12,600 and 12,800 home closings this year. That would actually be, at the midpoint, the second highest in the company's history, second only to the 13,699 closed in 2021. These homes should come in at an average price of between $600,000 and $610,000. So the prices we have been seeing so far this year are unlikely to improve materially, if at all, in the second-half of the year.

Author - SEC EDGAR Data

That's not the end of the world. If we annualize the results seen so far for this year, we would expect a net profit of $703.9 million, adjusted operating cash flow of $821.5 million, and EBITDA of $1.19 billion. Using these estimates, as well as historical results from 2023, we can see in the chart above how shares of the business are priced. On a forward basis, they are more expensive than using the historical results. But they aren't significantly more expensive, and they do look attractively priced on an absolute basis. In the table below, I then compared the company to five similar firms. On a price to earnings basis, two of the five ended up being cheaper than our candidate. This number drops to one of the five on an EV to EBITDA basis. And if we use the price to operating cash flow approach, Taylor Morrison Home Corporation ends up being the cheapest of the group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Taylor Morrison Home Corporation | 10.0 | 8.6 | 7.5 |

| Legacy Housing Corporation (LEGH) | 12.3 | 81.2 | 9.3 |

| Meritage Homes (MTH) | 8.7 | 19.3 | 6.9 |

| Century Communities (CCS) | 10.2 | 74.7 | 9.7 |

| Beazer Homes USA (BZH) | 6.8 | 25.8 | 12.4 |

| KB Home (KBH) | 11.1 | 11.9 | 9.7 |

Recently, there have been some concerns about the state of the economy. Primarily, there was the development that jobs created in the private sector were overstated to the tune of 818,000 in the aggregate in the 12 months ending in March of this year. While broader economic weakness could cause a problem for housing demand, it's also true that the Federal Reserve will almost certainly cut interest rates for the first time since they began raising them. That cut is expected for September. In general, lower interest rates make the financing of houses more appealing because, all else being equal, it lowers the overall pricing of said houses. And according to most sources on the matter, there seems to be a shortage of houses in this country. Back in December of last year, it was estimated that the country was short on housing by 3.2 million units. More recent estimates have suggested that this number might be closer to 4.5 million. This pent-up demand will likely result in higher orders and potentially higher home prices once rates start falling consistently. So, absent a significant economic downturn, I don't see any reason to become bearish on the business just yet.

Takeaway

Fundamentally speaking, things might not have been the best for Taylor Morrison Home Corporation recently. But on the whole, the company is doing quite fine. Yes, revenue, profits, and cash flows are all dropping year over year. But shares are cheap and backlog is growing. Cancellation rates are declining, and an eventual cut in interest rates should prove bullish for it and companies like it. Add all of this together, and I have no problem keeping the company rated a ‘buy’ for now.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.