A Summer To Remember

Summary

- U.S. equity markets climbed to record-highs while benchmark interest rates rebounded from eight-month lows on a relatively quiet end-of-summer week as investors parsed a 'Goldilocks' slate of economic data.

- PCE data showed modest inflationary pressures in July - keeping the Fed on course for multiple rate cuts by year-end - while consumer spending and consumer confidence data topped estimates.

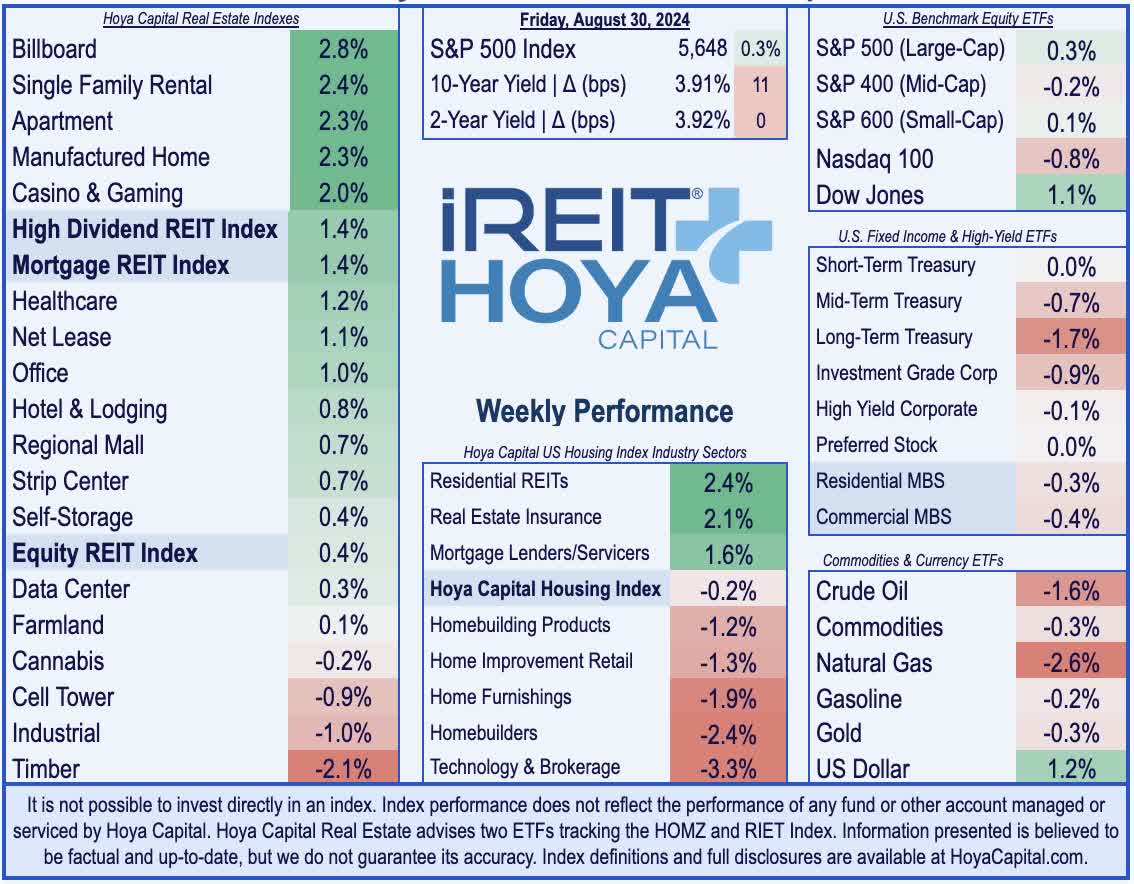

- Posting gains for a fourth week following a three-week skid in late July, the S&P 500 gained another 0.3% this week. The Dow Jones finished the week at all-time record-highs.

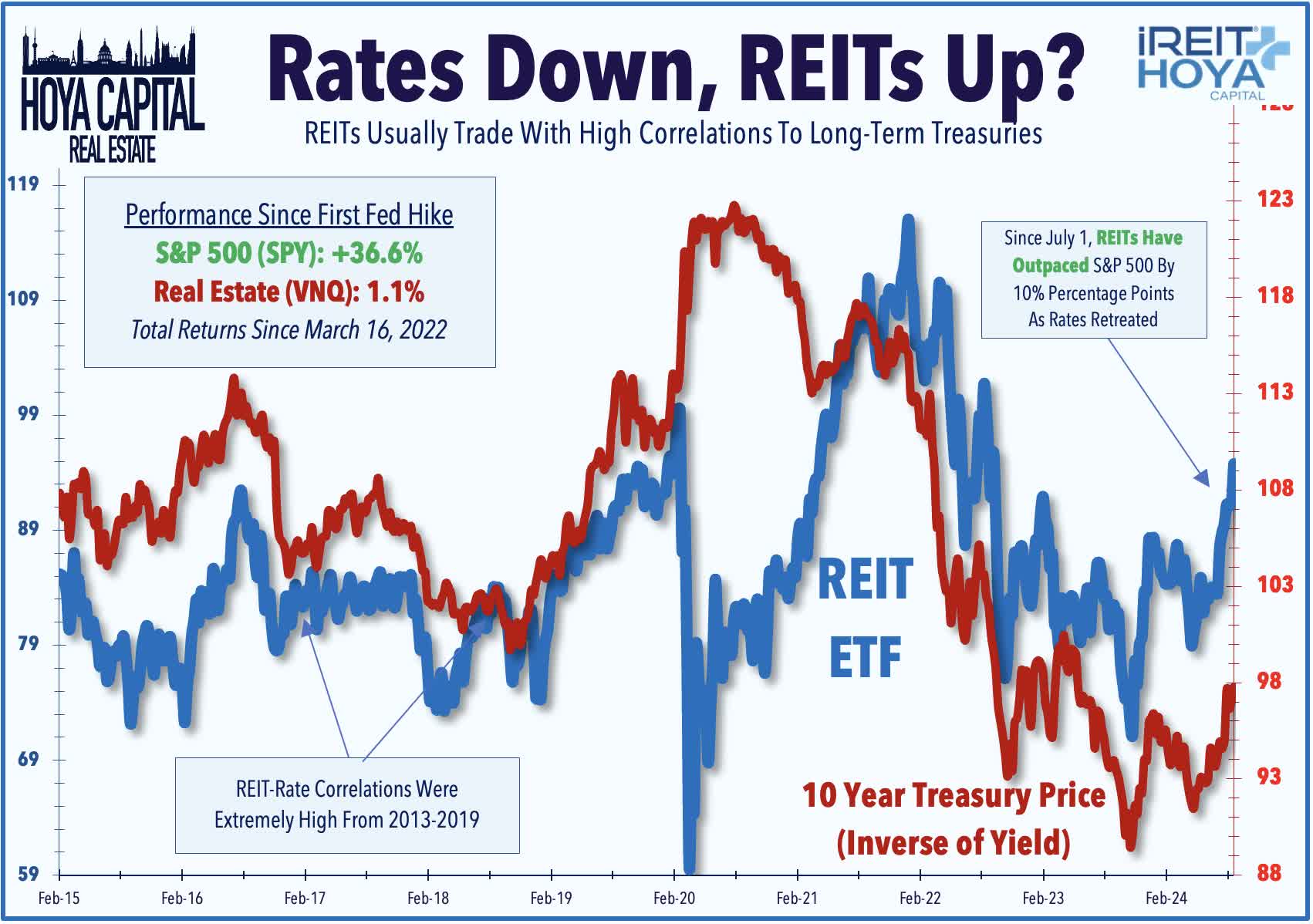

- Real estate equities continued their recent outperformance this week on indications that the rate retreat will spark a revival across the long-floundering REIT sector. The Equity REIT Index advanced 0.4%.

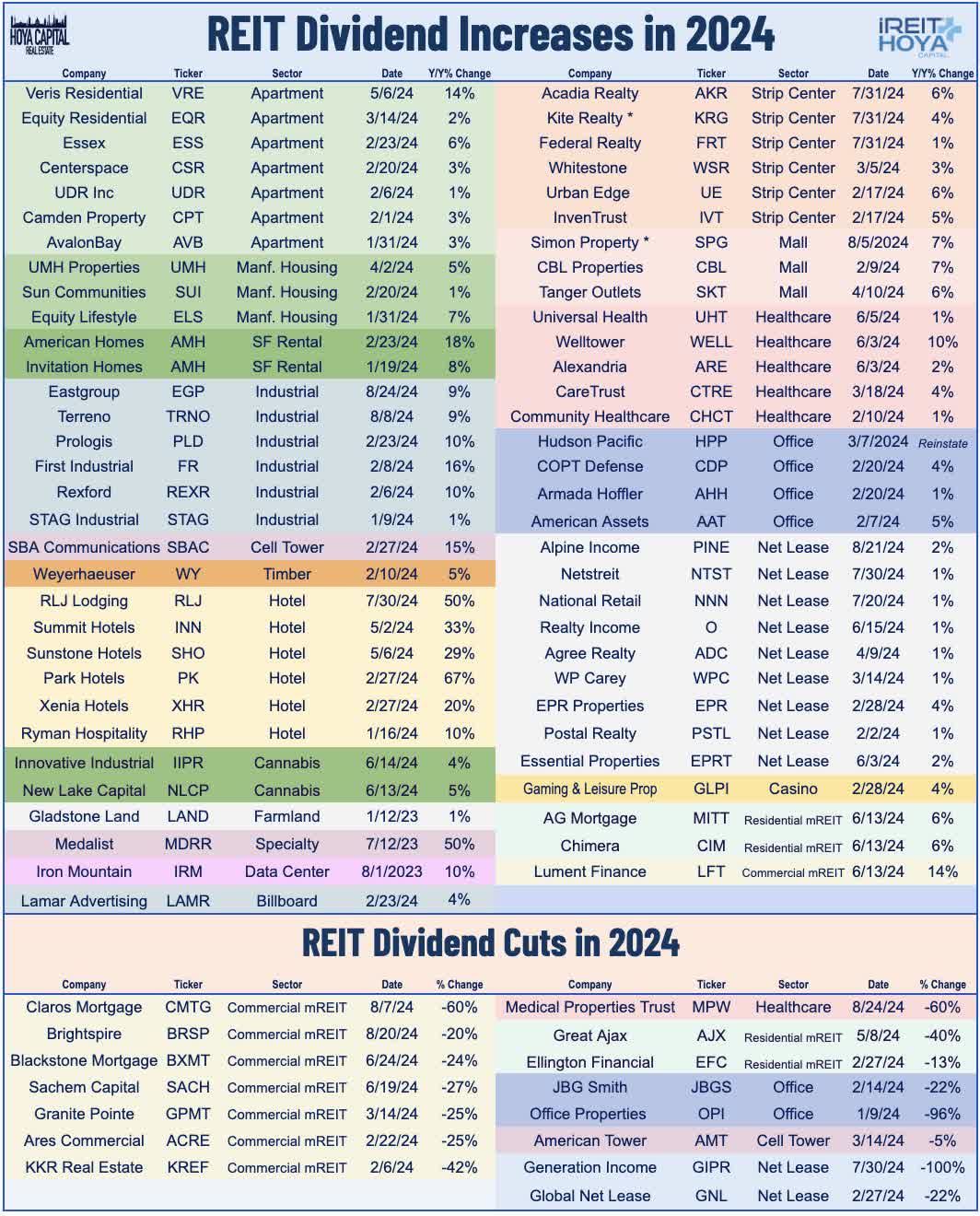

- Billboard REIT Lamar Advertising rallied after it raised its dividend for the second time this year, hiking its payout by 8%. Signs of a revival of REIT "animal spirits" was a theme throughout the week, with notable acquisition and capital-raising activity from a handful of REITs.

Matteo Colombo

Real Estate Weekly Outlook

Hoya Capital

U.S. equity markets climbed to the cusp of record-highs while benchmark interest rates rebounded modestly from eight-month lows on a relatively quiet end-of-summer week as investors parsed a "Goldilocks" slate of economic data showing modest inflationary pressures alongside resilient consumer activity. Posting gains for a fourth week following a three-week skid in late July, the S&P 500 gained another 0.3% this week - lifting the major benchmark to back within 0.2% of all-time record-highs - while the Dow Jones Industrial Average closed the week at fresh records. Tech stocks were laggards this week, however, with the Nasdaq 100 slipping 0.8% after earnings results from chip giant Nvidia were softer than lofty expectations. Real estate equities continued their recent outperformance this week on indications that the rate retreat will spark a revival across the long-floundering REIT sector. The Equity REIT Index advanced 0.4% this week, with 15-of-18 property sectors in positive territory, while the Mortgage REIT Index gained 1.4%.

Hoya Capital

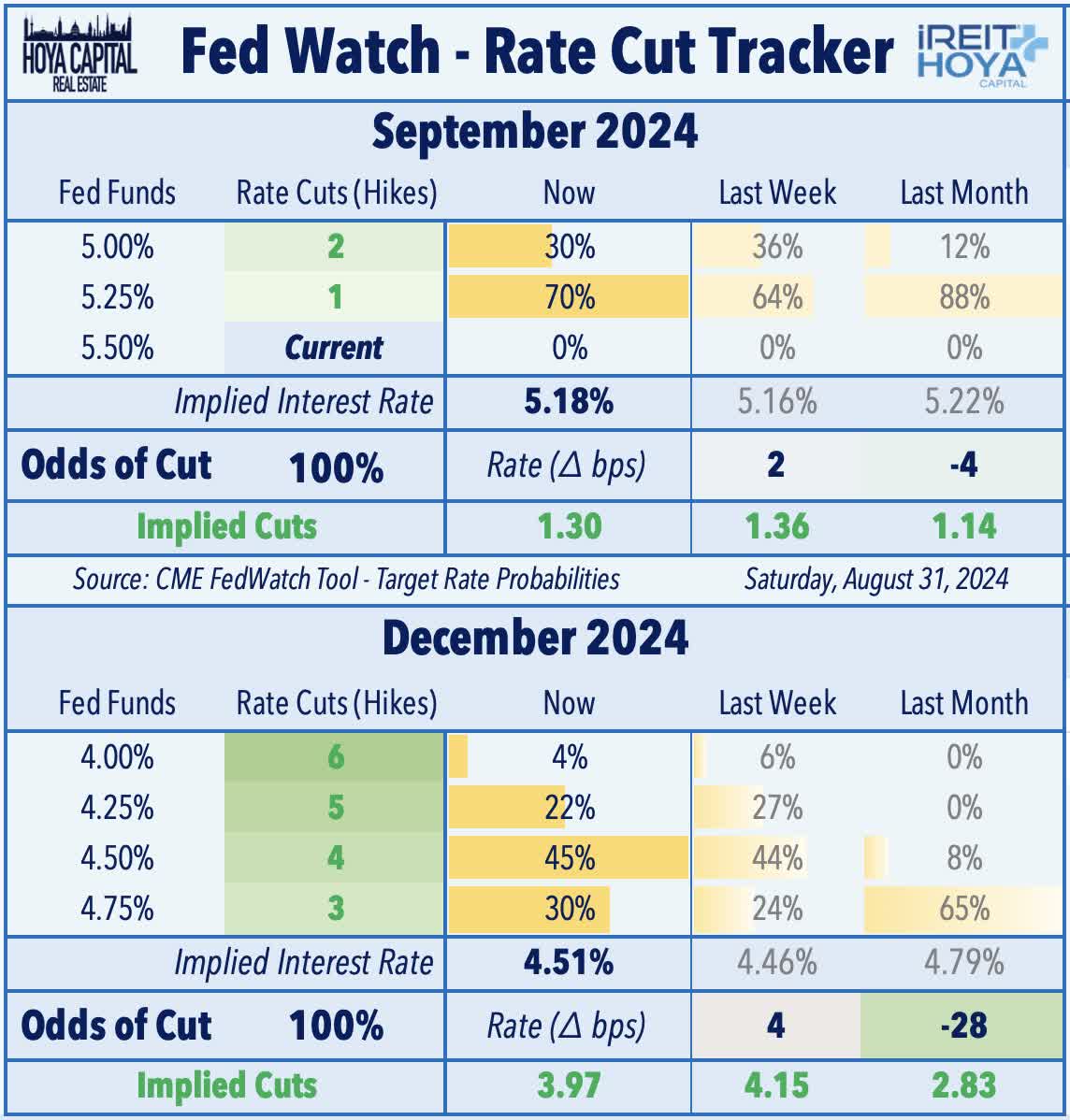

Bond markets were under a bit of pressure this week - particularly at the longer end of the curve - after the latest slate of economic data and retail earnings results indicated that the U.S. consumer remains on more stable footing than feared following a soft patch of data in early August. The Conference Board reported that its Consumer Confidence Index posted its highest reading since February, while several major retailers - Nordstrom (JWN) and Kohl's (KSS)- raised their full-year earnings outlook. Rebounding from its 2024 lows set earlier this month, the 10-Year Treasury Yield climbed 11 basis points this week to close at 3.91%, but the policy-sensitive 2-Year Treasury Yield was unchanged at 3.92%. Swaps markets now price-in 1.30 rate cuts in September (down slightly from 1.36 implied last week) and 3.97 rate cuts by the end of the year (down from 4.15 last week). In commodities markets, WTI Crude Oil dipped 2% on the week to fall back below $74/barrel - erasing an early-week bounce on Libyan supply concerns - and now trading back on the lower-end of its 2024 range between $70 and $87.

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

Hoya Capital

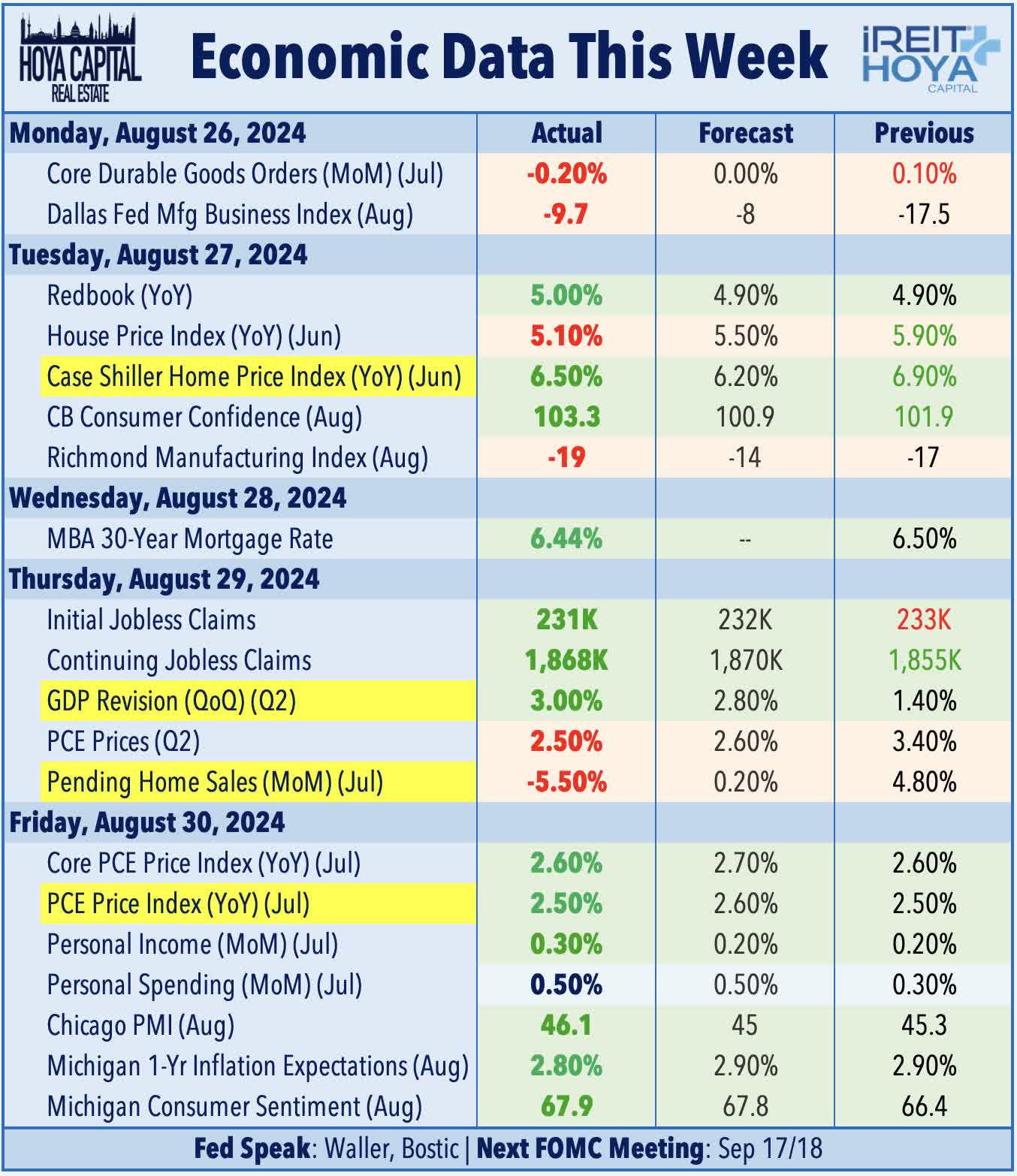

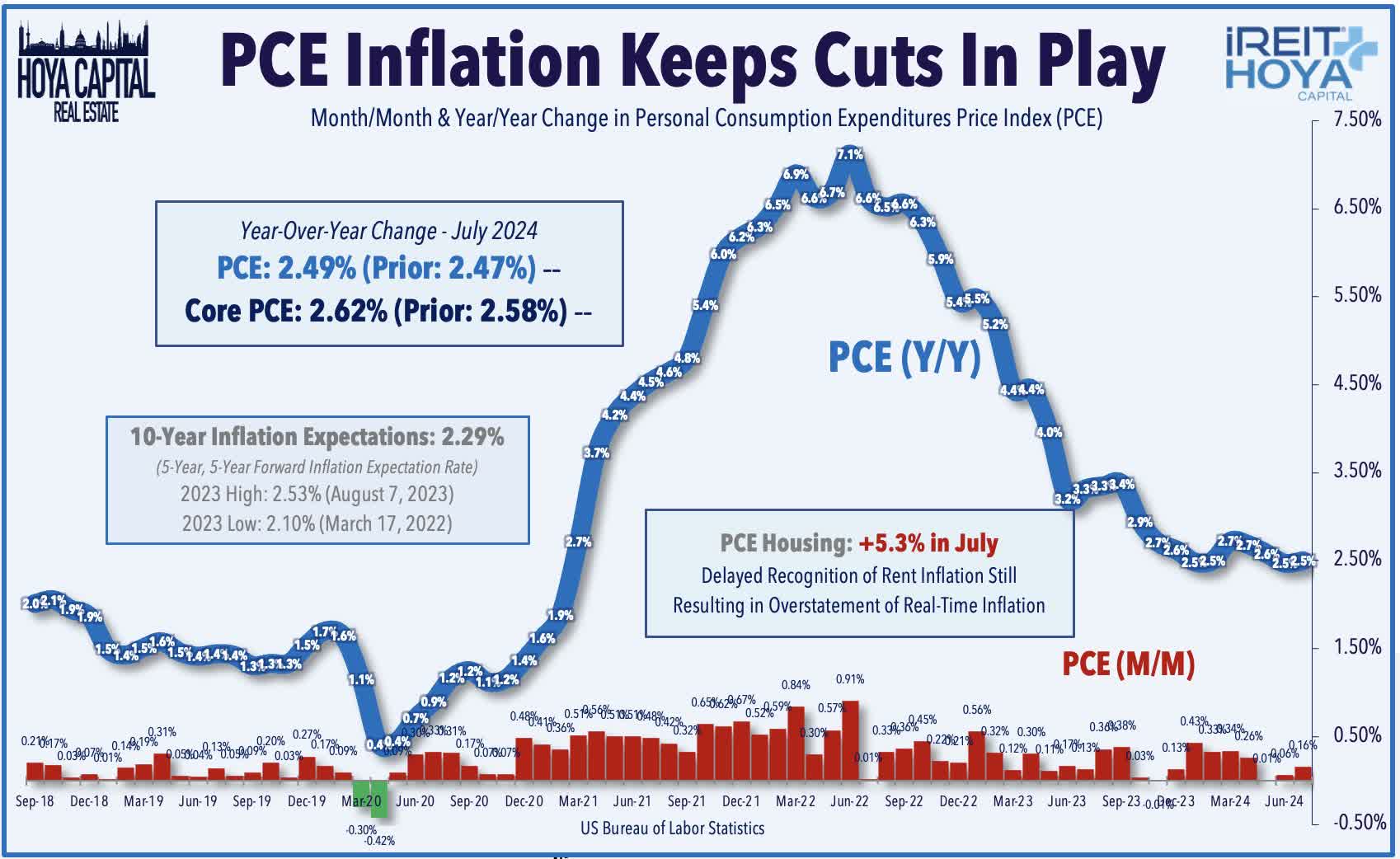

Following cooler-than-expected Consumer and Producer Price Index data earlier this month, PCE Price Index data this week provided further evidence of modest inflationary pressures in July, keeping the Federal Reserve on course for multiple rate cuts in the final months of 2024. Headline PCE rose 0.2% for the month - in line with expectations - which maintained the year-over-year increase at 2.5%, matching the lowest level since February 2021. Core PCE - the Fed's preferred gauge of inflation - also rose 0.2% in July - matching expectations and keeping the annual increase unchanged from the prior month at 2.6%. The report was a bit more encouraging under the surface, as Core PCE ex Housing increased just 0.1% on the month. We've noted that real-time shelter inflation - as measured by a half-dozen private market data providers - is closer to the 0-2% range, far below the 5.3% increase reported in government data. Substituting the Apartment List National Rent Index (ALNRI) for the PCE Housing component shows that Headline PCE has averaged less than 2% this year.

Hoya Capital

Equity REIT & Homebuilder Week In Review

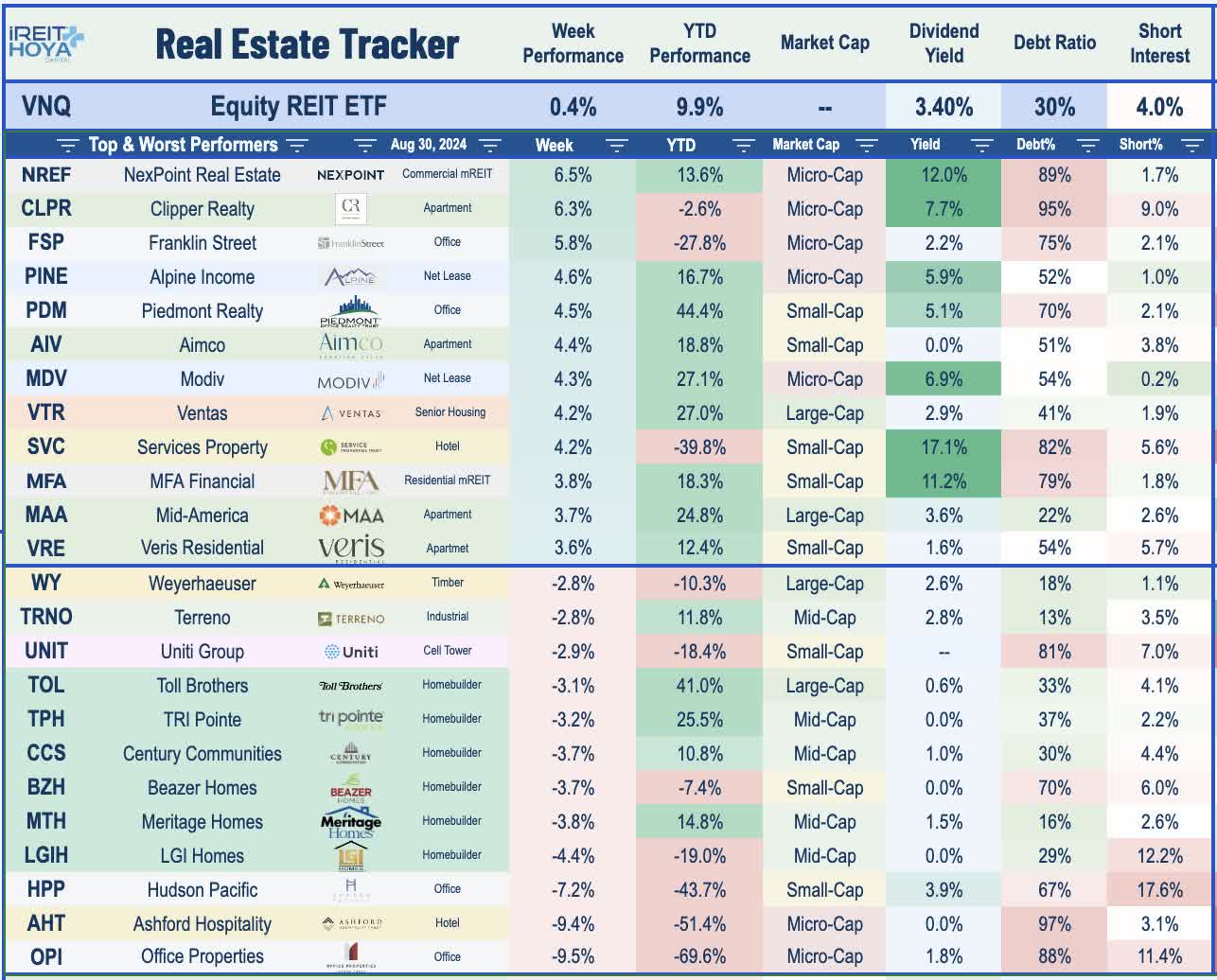

Best & Worst Performance This Week Across the REIT Sector

Hoya Capital

This week we published our State of REIT Nation report, which focused on higher-level macro themes affecting the REIT sector at large. We noted that two years of persistent rate-driven pressure on residential and commercial real estate markets appears to finally be abating as the worst of pandemic-era inflationary pressures subside. This 'light-at-the-end-of-the-tunnel' comes as commercial property values approached the critical 20% drawdown level, a level that can result in cascading distress that extends beyond the weakest players. Despite the outperformance since mid-July, the Equity REIT Index has underperformed the S&P 500 by a whopping 35 percentage points since the start of the Fed's rate hike cycle in March 2022. We discussed that the real estate sector at large is not completely out of the woods; however, as expectations of "Higher for Longer" are merely shifting to "High for Long" in which benchmark rates will likely remain well above pre-pandemic levels into 2025. While conditions will remain challenging for debt-heavy entities - including private equity funds and non-traded REITs - these macroeconomic conditions are ideal for low-levered entities with access to "nimble" equity capital - conditions that maximize the true competitive advantage of the public REIT model, sparking a flow of assets from private into public markets.

Hoya Capital

Billboard: Beginning with dividend news, Lamar Advertising (LAMR) - the largest of two billboard REITs - rallied 3% this week after it raised its dividend for the second time this year, hiking its payout by 8% to $1.40/share (4.6% dividend yield), which is 12% above its payout in the third quarter of 2023. LAMR noted in its earnings call that it expects dividend growth of "low double digits" in 2024 and 2025 - above its mid-single-digit FFO growth trend - to meet its REIT distribution requirements. In the same call, LAMR commented that it expects dividend growth should "normalize in 2026 and be more in line with FFO growth." As noted in our State of REIT Nation report, we've now seen 61 REITs raise their dividend in 2024, while 15 REITs have announced dividend reductions. The average REIT dividend payout ratio was 69% in the second quarter - an improvement from the 78% payout ratio in the first quarter and below the historical average dividend payout ratio of around 80%.

Hoya Capital

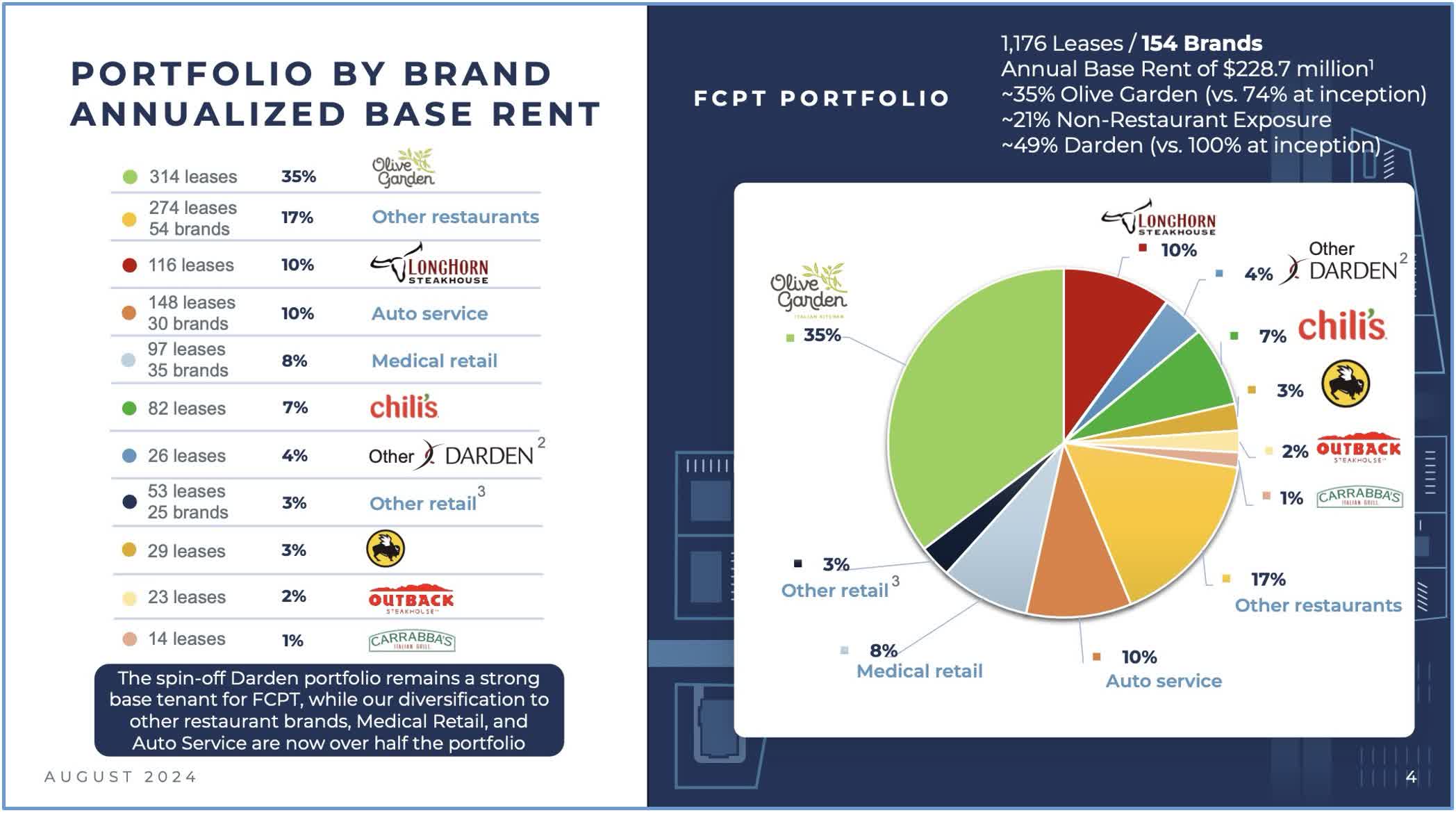

Net Lease: Signs of a revival of REIT "animal spirits" was a theme throughout the week. Restaurant-focused net lease REIT Four Corners (FCPT) - which had spun out from Darden in 2015 - rallied 3% this week after it provided a business update and announced a $66.4M deal to acquire 20 Bloomin’ Brands restaurant properties. As of the closing date, Bloomin’ Brands - which operates a handful of fast casual brands, including Outback Steakhouse and Carrabba’s Italian Grill - has become FCPT's third-largest tenant, accounting for approximately 3.3% of FCPT's annual rent. Of note, this transaction lowers the tenant exposure of Dardens Restaurants' brands to below 50% for the first time. FCPT acquired the properties for a cap rate of roughly 7.2%, and are under a pair of long-term master leases of ten restaurants each. In the accompanying business update, FCPT noted that it has been active on the capital-raising front in recent months, raising $148M in equity via its At-the-Market ("ATM") program. FCPT provided color on its strategic use of its ATM, noting that 90% of its total equity issuance since inception has come through its ATM rather than through one-off secondary equity offerings, commenting that it has "worked exceptionally well for FCPT over the past eight years."

Hoya Capital

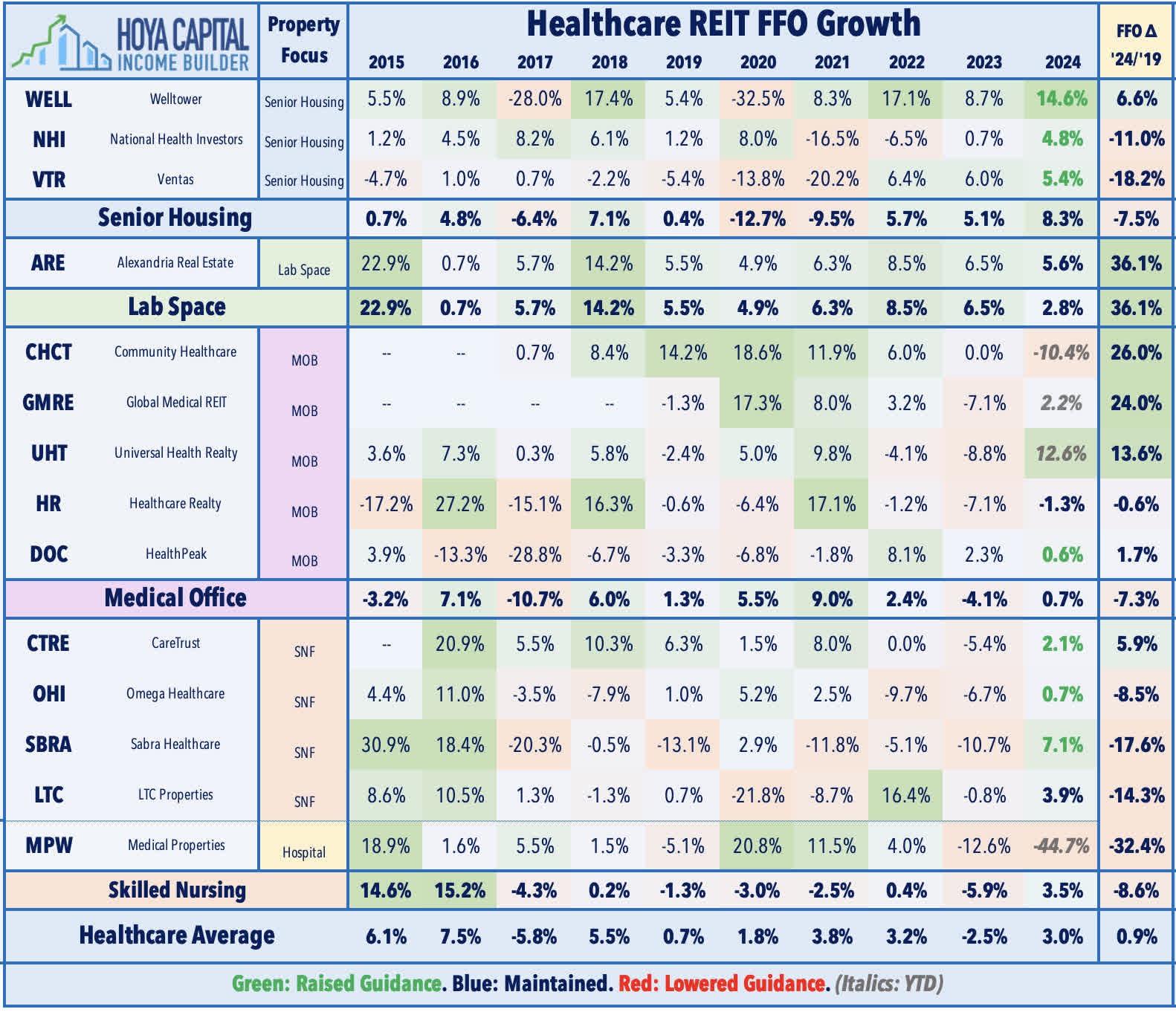

Healthcare: Skilled nursing facility REIT CareTrust (CTRE) gained 2% this week after it announced a pair of acquisitions and indicated that it plans to remain aggressive on the M&A front with a "replenished" pipeline of forthcoming deals. CTRE announced that it acquired two nursing facilities in separate transactions for a total investment of $62.1M, which include a 125-bed facility in the Mid-Atlantic and a 134-bed facility located on the West Coast. Among the most aggressive REITs relative to its size CTRE has already acquired $827in assets this year at an average yield of 9.5%. CTRE noted that it has "replenished" its pipeline with $230M of "near-term actionable real estate acquisition opportunities, not including larger portfolio opportunities the company is reviewing." While senior housing and skilled nursing REITs have been in "buy mode" for much of the year, other healthcare REITs in the medical office building ("MOB") and hospital space have remained net sellers. MOB owner Healthcare Realty (HR) gained 1% this week after it announced it further expanded its existing joint venture with KKR & Co (KKR) by contributing another $118M of assets into the JV, generating $94M in proceeds. HR initially formed the JV in May, announcing that it would sell 80% interest in a dozen medical office buildings for $383M in proceeds, and announced that it would increase this total to $500M "in the near term." HR noted that it has additional asset sales and JV transactions under contract that are expected to increase proceeds to over $1 billion, with proceeds "expected to fund accretive, leverage neutral share repurchases."

Hoya Capital

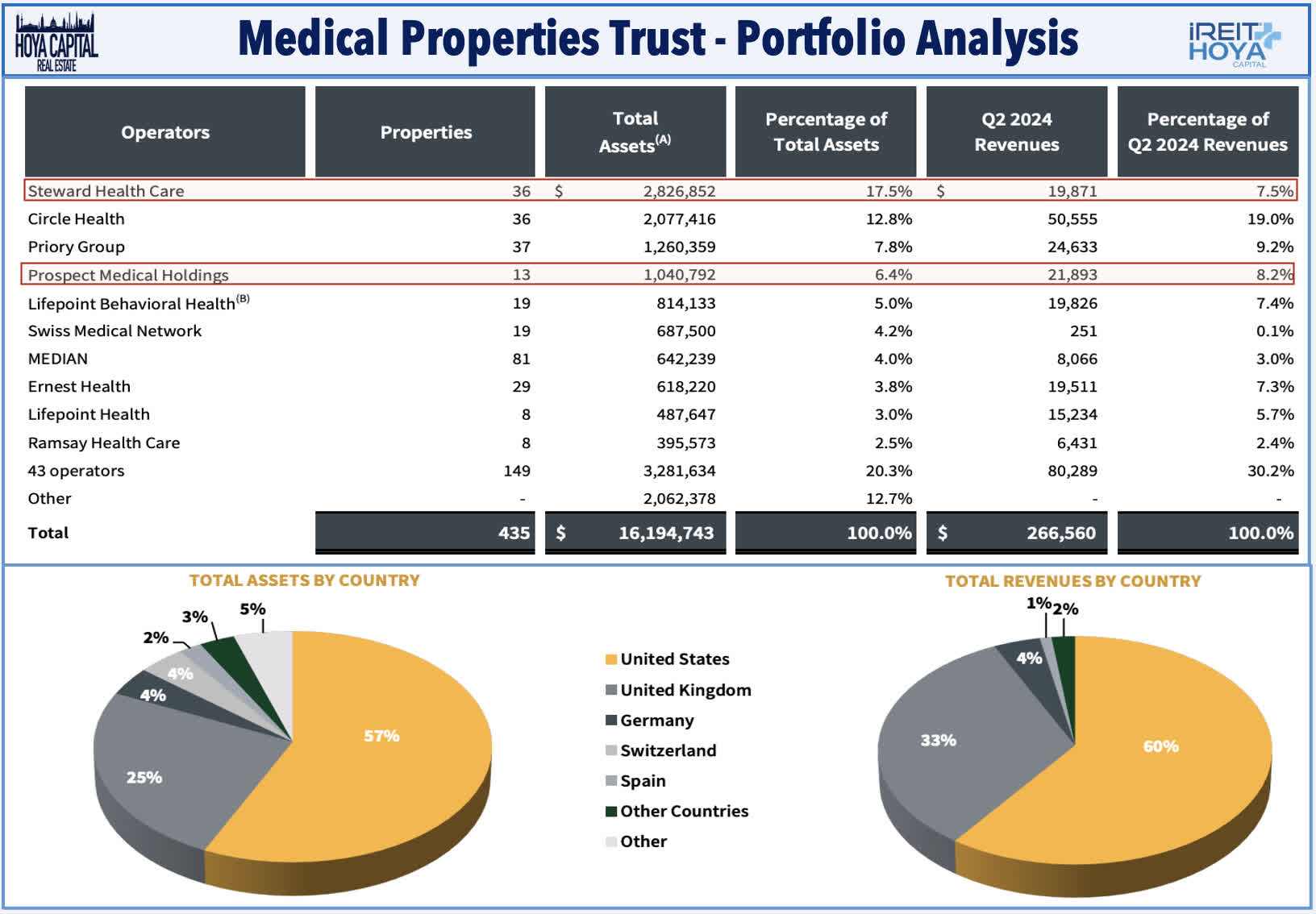

Healthcare: Sticking in the healthcare space, embattled hospital owner Medical Properties Trust (MPW) was little-changed this week despite signs of potential progress in resolving the ongoing messy saga related to the bankruptcy of its largest tenant, Steward Health Care. On Friday evening, Steward announced that it reached an deal to settle disputes over leasing claims by allowing MPW to take control of Steward's hospitals to allow for the transfer of hospitals to new interim operators. In exchange, MPW agreed to the release of all claims on secured lease obligations between them, "including the release of billions of dollars of claims held by MPW against Steward." Steward noted that it would seek bankruptcy court approval for the deal "as soon as possible." Earlier in the week, Steward announced an agreement to sell six of its hospitals in Massachusetts, which were among the eight Steward-operated hospitals that were owned by MPW. Earlier this month, MPW recognized a "full impairment" of its $550M equity ownership in the eight Steward-operated hospitals in Massachusetts after failed negotiations with state regulators, which MPW says would only agree to approve the transfer of the operating license - and by extension the real property - to an "in-state, not-for-profit operator." Using this leverage, Steward has been able to effectively take ownership of these properties from MPW, and it's unclear what recovery - if any - MPW would receive from the sale of these properties.

Hoya Capital

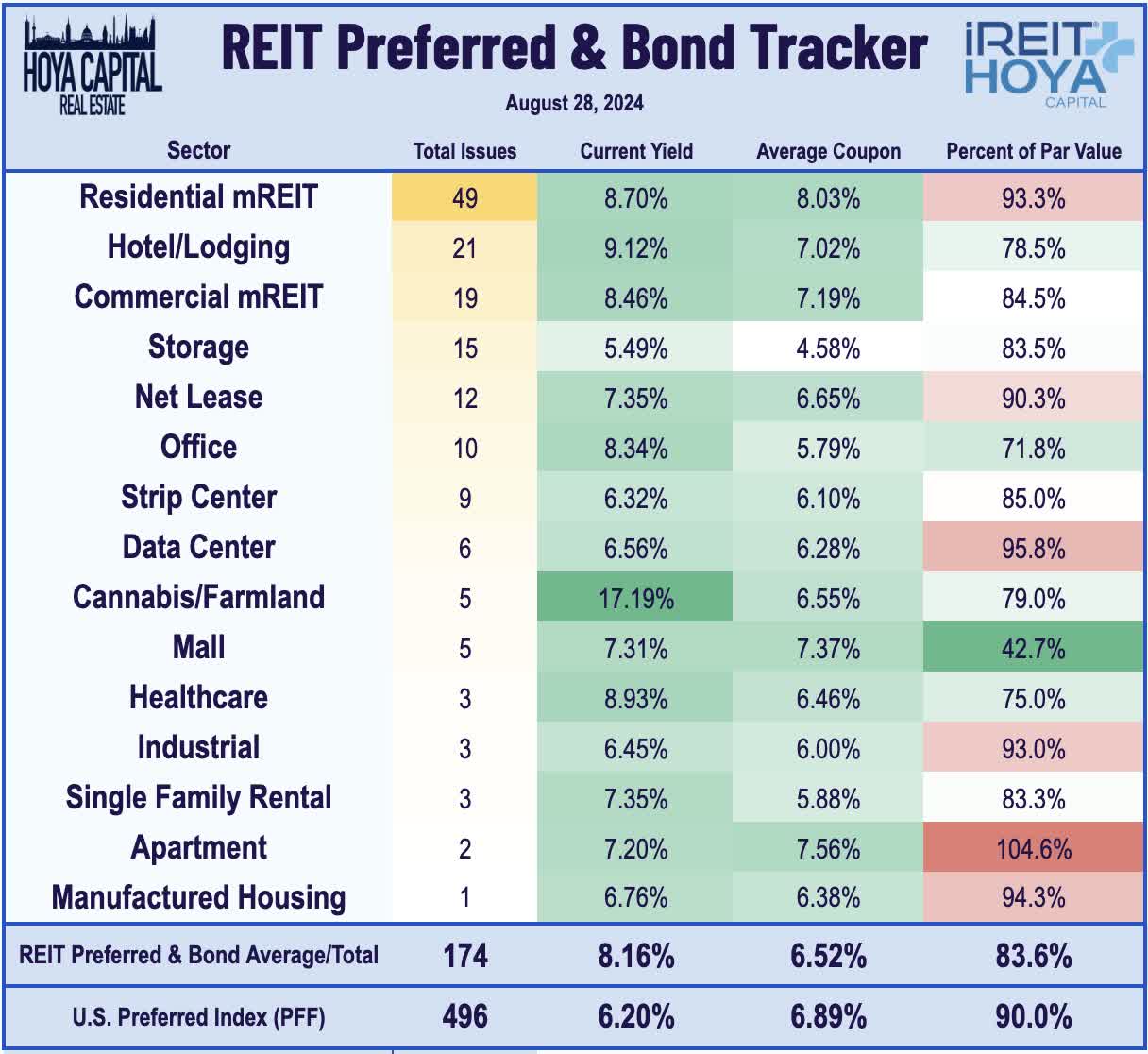

Net Lease: REITs remained busy on the capital raising and "capital recycling" front this week as well. Realty Income (O) - the largest net lease REIT - gained 2% this week after it announced that it raised nearly $1B in new debt capital and noted that it would redeem its lone outstanding preferred share class, which was a residual from the Spirit Realty merger in 2023. O raised a combined £700M ($933M) in debt, pricing a public offering of £350M of five-year notes due 2029 at a 5.00% interest rate, and £350M of seventeen-year notes due 2041 at a 5.25% interest rate. Concurrently, Realty Income announced that it would redeem all 6.9M outstanding shares of its 6.0% Series A Preferred (O:PR), formerly the Spirit Realty Series A Preferred. The shares will be redeemed at $25.00 per share, plus accrued and unpaid dividends to Sep. 30. The total payment will come to $25.375 per share. The shares had traded as low as $19.70 last October prior to the merger announcement. After the redemption, there will be 173 exchange-listed REIT preferred securities, which trade with an average current yield of 8.16%, and trade with an average discount to par value of roughly 15%.

Hoya Capital

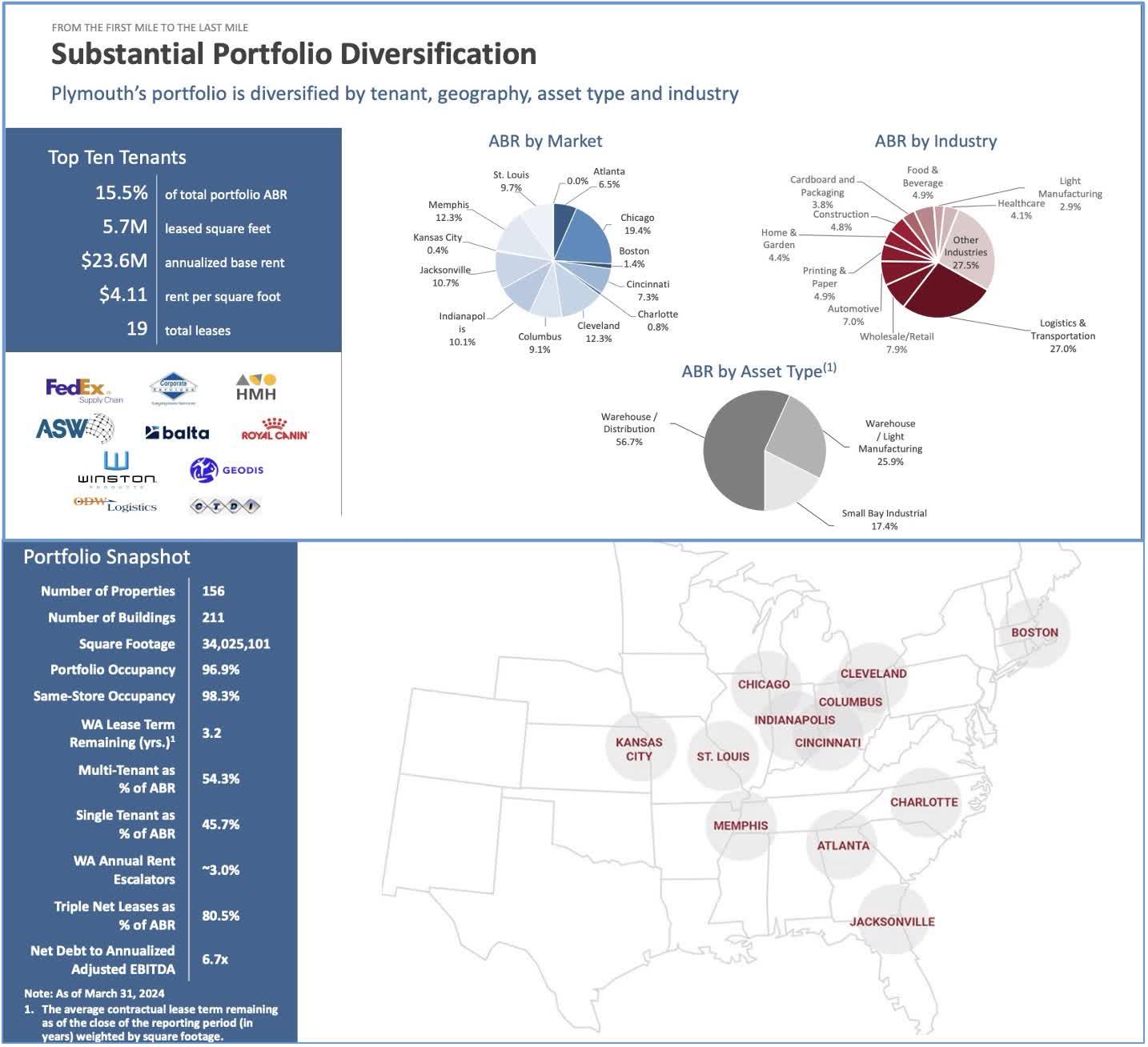

Industrial: Small-cap Plymouth Industrial (PLYM) - which we own in the REIT Dividend Growth Portfolio - was little-changed after it announced a strategic agreement in which private equity firm Sixth Street will provide $500M in capital "to accelerate earnings growth and scale the platform in key industrial markets." The total includes $250M of capital in the form of a 65% joint venture ownership of Plymouth’s Chicago portfolio and non-convertible preferred equity investment at a 7% yield. Plymouth will contribute its 5.9 million-square-foot Chicago-area properties to the joint venture at a 6.2% capitalization rate - a healthy valuation implying a gross asset value of $356M - and will retain 35% ownership of the portfolio. PLYM intends to use the proceeds to partially fund its recent $100.5M acquisition of an industrial portfolio in Memphis at an 8.0% cap rate. Plymouth noted that the capital provided by Sixth Street would "fund additional growth on a leverage-neutral basis without exclusive reliance on the public equity markets." Not uncommon for small-cap REITs, Plymouth has a Debt-to-EV Ratio of roughly 45%, which is well above the industrial sector average of around 20%. PLYM also affirmed its previously issued 2024 Core FFO full-year guidance range of $1.88 to $1.90 per share, implying full-year growth of around 3%.

Hoya Capital

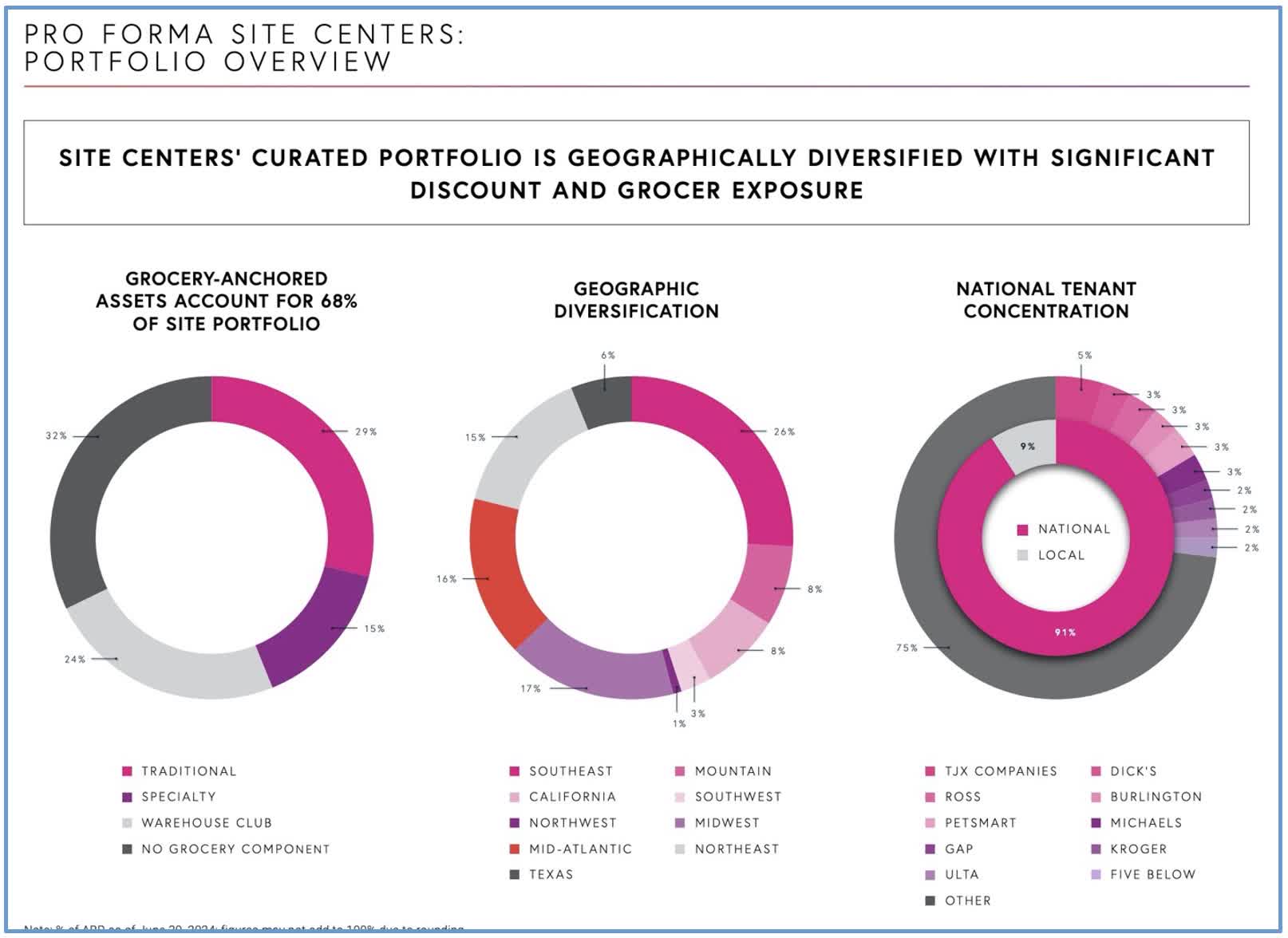

Strip Center: SITE Centers (SITC) slipped 1.5% this week after it provided a business update showing that it has remained active on the capital recycling front ahead of its planned spinoff of its convenience store portfolio into a separate public REIT - Curbline Properties - which is expected to be completed in early October. SITC reported that it has sold 11 properties thus far in the third-quarter for a total of $552.7M in proceeds, while it acquired four convenience shopping centers for a total of $88.0M. Earlier this month, SITC reiterated that it remains on a "dual path" in its shareholder value maximization strategy, which includes the spinoff of the Curbline portfolio and through one-off property dispositions. As of June 30, the Curbline portfolio includes 72 wholly-owned properties, and at the time of the spinoff, is expected to have no debt and $600M of cash. Following the spin-off, SITC will own approximately 50 wholly-owned strip centers - 68% of which are grocery-anchored - with a concentration along the Sunbelt and East Coast. Elsewhere in the strip center space Regency (REG) announced the opening of Oakley Shops, a new Safeway-anchored ground-up development in Oakley, CA, marking Regency's first development in the Northern California submarket.

Hoya Capital

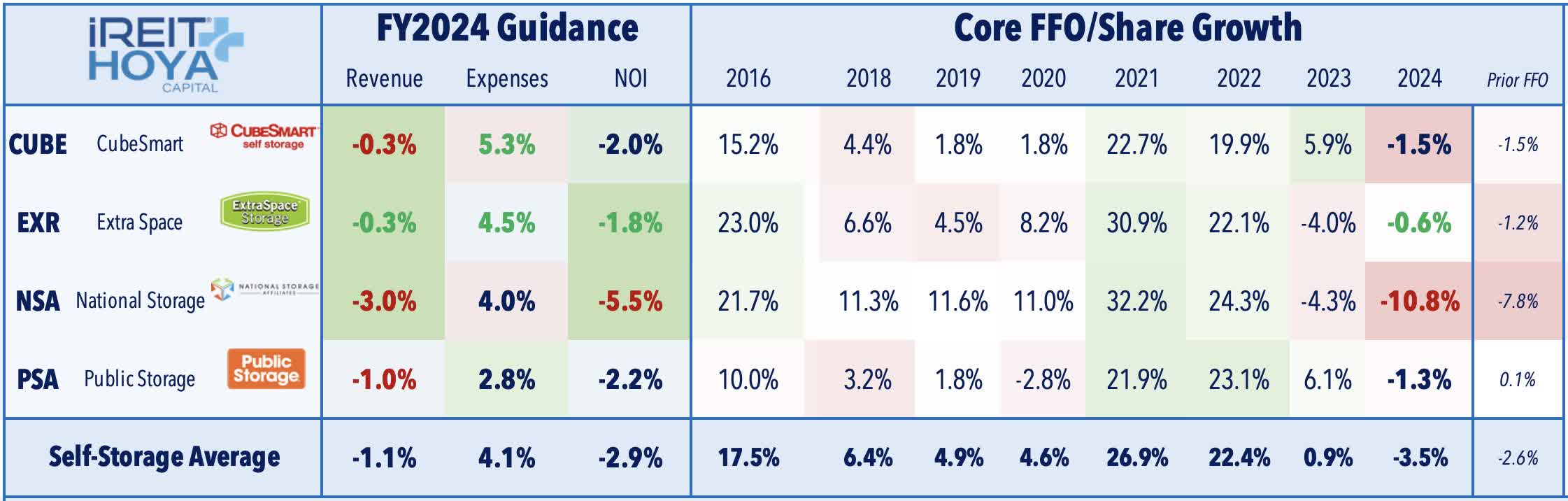

Self-Storage: National Storage (NSA) - the fourth-largest storage REIT - gained 2.5% this week after it announced a deal with Solar Landscape to develop 100 megawatts of solar capacity on up to 1,000 of its rooftops. Solar Landscape will develop, own, and operate the projects and make monthly lease payments to NSA. Development on the first sites has already begun, and the projects require no capital expenditure by NSA. Other self-storage REITs - as well as REITs across the industrial and retail sectors with ample rooftop square footage - have employed similar programs and partnerships in recent years. Public Storage (PSA) noted earlier this month that it has now equipped more than 500 of its facilities with solar, and plans at least 500 additional installations over the next several years. PSA noted that these solar installations were partially responsible for the 8% decrease in same-store utility costs last quarter. Extra Space (EXR) commented earlier this month that it has been "quite aggressive on the solar side for a lot of years," with 50% of its facilities now equipped with solar. EXR also credited these installations with a favorable improvement in expense trends, and that it "continues to look for [solar] opportunities with a good yield."

Hoya Capital

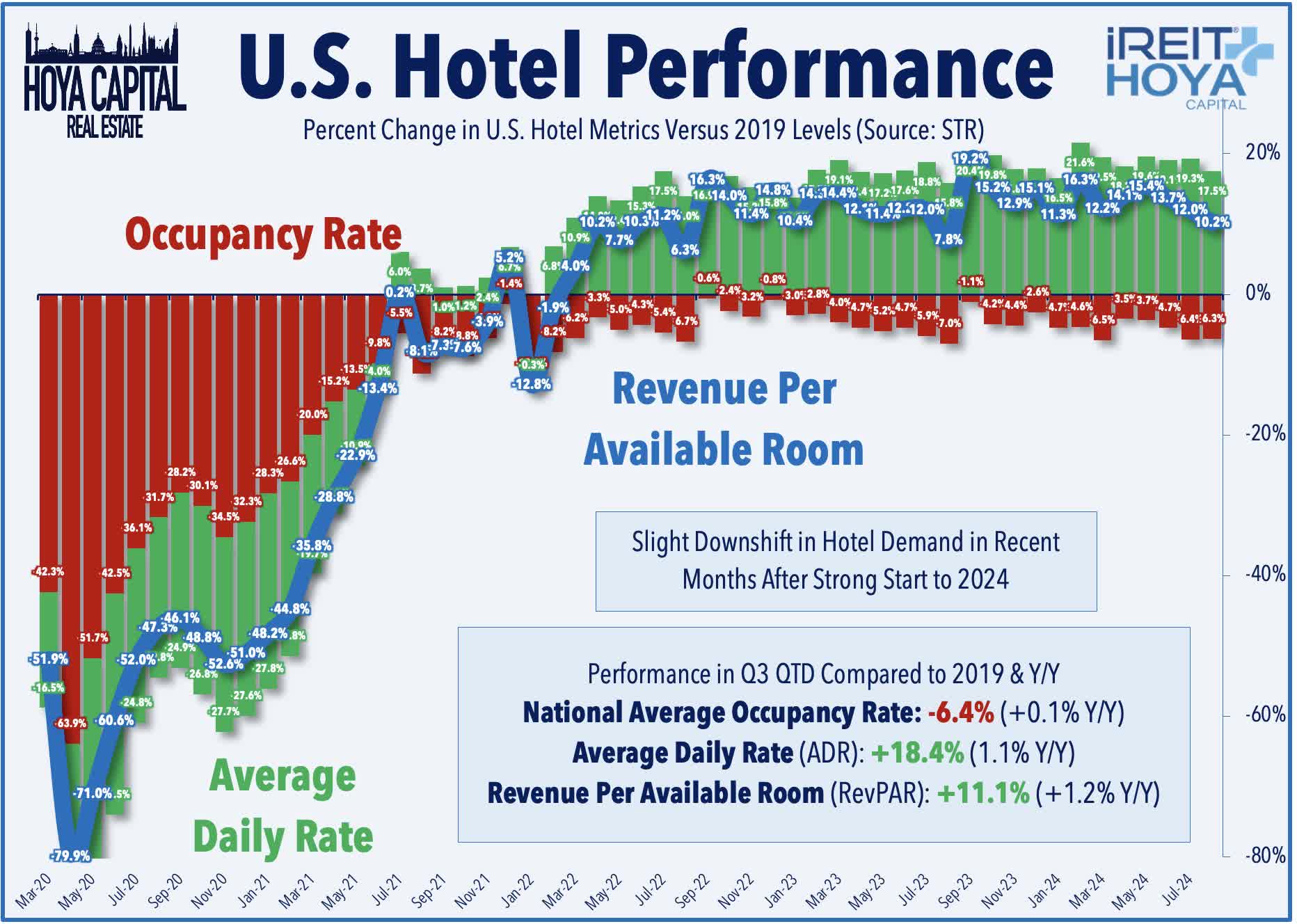

Hotel: Park Hotels (PK) advanced 1% this week after it reported that its two Hawaii-located hotels "sustained no material damage" from Hurricane Hone, a Category 1 hurricane that impacted the Hawaiian Islands last Sunday. Hotel data provider STR reported this week that industry-wide Revenue Per Available Room ("RevPAR") was flat on a year-over-year basis in July, continuing a trend of moderation in recent months after a strong start to 2024. This level of RevPAR was 12.0% above pre-pandemic 2019-levels, however, as cumulative room rate inflation (Average Daily Rates) of nearly 20% during this time has helped to offset a 6% drag from lower occupancy rates. Recent weekly data indicates that August is shaping up to be a stronger month, with RevPAR trending to be 2.4% above last year. TSA Checkpoint data shows similar trends of softness in July followed by a rebound in August. Domestic throughput cooled to around 4% above 2019-levels in July - the softest month since mid-2023 - but has rebounded thus far in August to roughly 8% above 2019-levels. Hotel REITs were among the "losers" of REIT earnings season, as ten of the eleven hotel REITs lowered their full-year RevPAR outlook.

Hoya Capital

2024 Performance Recap

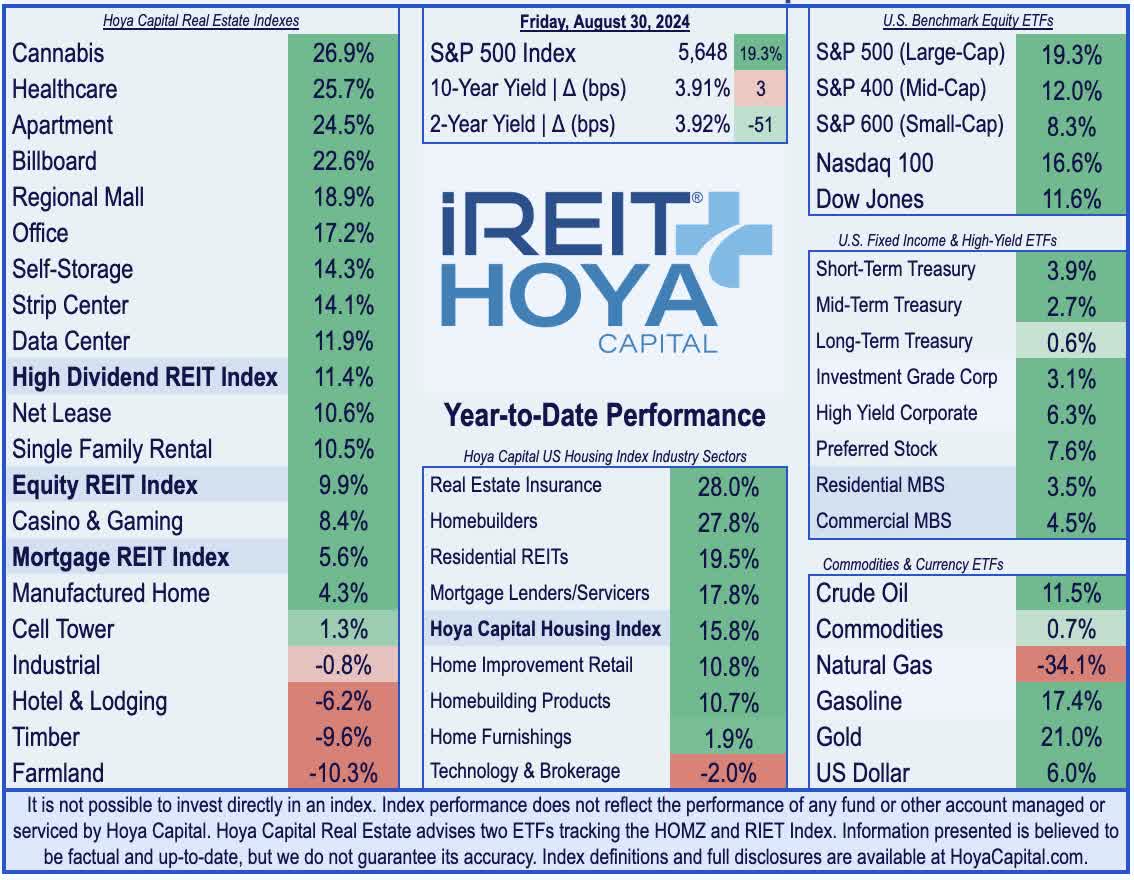

Performance trends have shifted dramatically over the six weeks, as the long-underperforming real estate sector has closed some of the historically wide gap with other segments of the equity market amid a sharp pull-back in benchmark interest rates. At the end of August, the Equity REIT Index is now higher by 9.9% this year, while the Mortgage REIT Index is higher by 5.6%. This compares with the 19.3% gain on the S&P 500, the 12.0% gain for the Mid-Cap 400, and the 8.3% gain for the Small-Cap 600. Within the REIT sector, 14 of the 18 property sectors are higher for the year, led by Healthcare, Residential, and Retail REITs - while Farmland, Timber, and Hotel REITs have lagged on the downside. At 3.91%, the 10-Year Treasury Yield is now higher by 3 basis points on the year, while the 2-Year Treasury Yield has dipped by 51 basis points to 3.92%. The aggregate Bloomberg US Bond Index is now higher by 3.1% this year. WTI Crude Oil is higher by 11.4% this year, while the broader Commodities complex is higher by just 0.7% on the year as higher oil prices have been offset by a dip in Natural Gas prices.

Hoya Capital

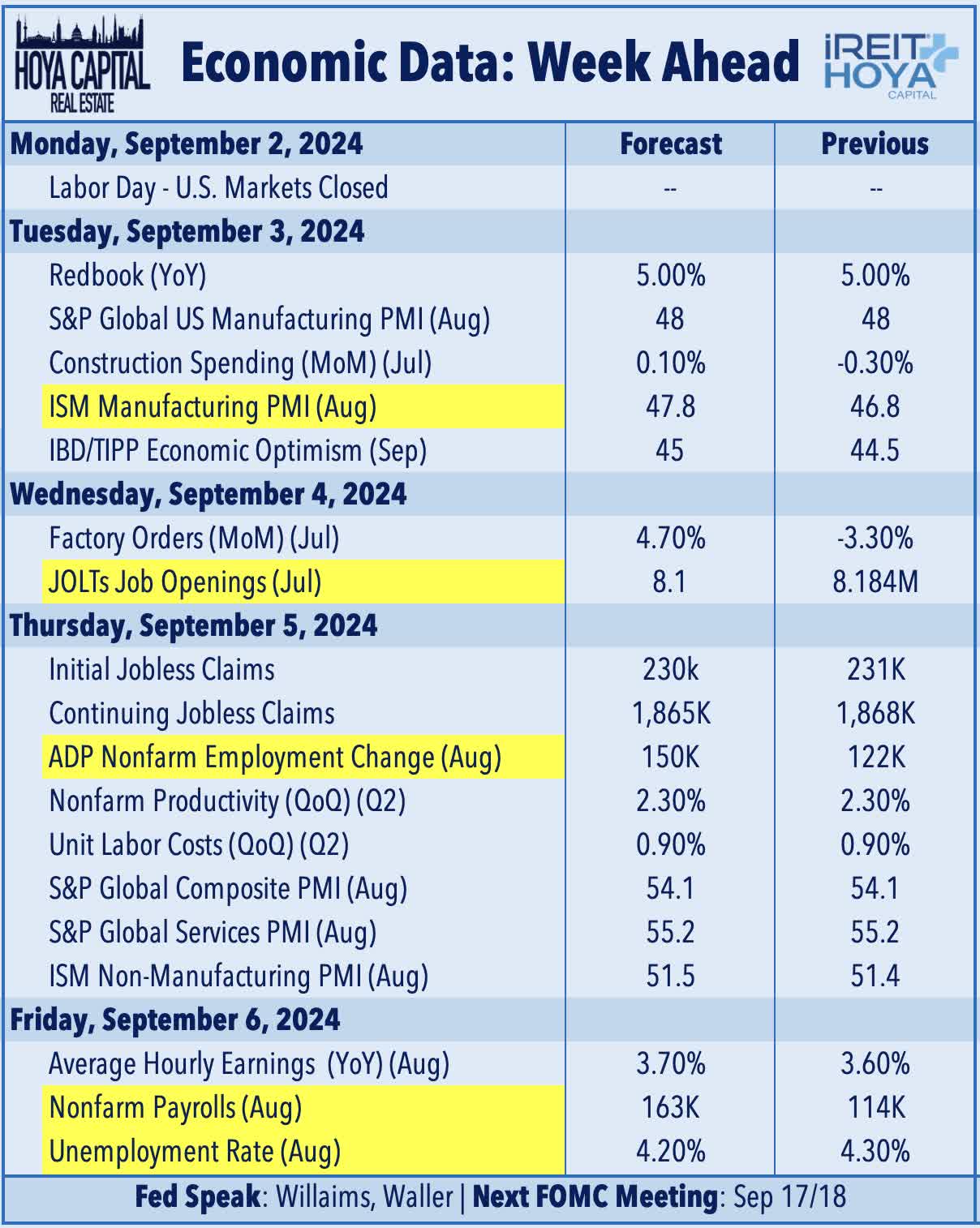

Economic Calendar In The Week Ahead

A critical slate of employment data highlights the economic calendar in the holiday-shortened week ahead, with the Job Openings & Labor Turnover Survey ("JOLTS") on Wednesday, ADP Payrolls and Jobless Claims data on Thursday, and the key BLS Nonfarm Payrolls on Friday. Economists expect job growth of roughly 163k in August on the "headline" Establishment Survey, which follows a notably weak print last month of 114k jobs. The stakes are high ahead of the Federal Reserve's rate decision on September 18th, as last month's report provided the most decisive evidence of weakening labor market conditions and has been perhaps the most significant contributor to the recent pivot in monetary policy expectations. The Household Survey - which is used to calculate unemployment metrics - has exhibited weaker trends in recent months, which has lifted the unemployment rate to nearly three-year highs. The Average Hourly Earnings series within the payrolls report - the first major inflation print for August - is expected to show that annual wage growth accelerated slightly to 3.7% from 3.6% last month. We'll also be watching a handful of PMI surveys throughout the week, headlined by the ISM Manufacturing PMI report on Tuesday, and ISM Services PMI on Thursday. U.S. equity and bond markets will be closed on Monday for Labor Day.

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.