Volatility in Chinese Stocks! How to Short with Options?

Recently, both Hong Kong and U.S. stocks with Chinese assets have seen significant adjustments, with noticeable outflows of funds from individual stocks.

Analysts from several fund companies noted that this rally has been quite sharp, with rapid volume expansion. This could lead to even greater market volatility going forward. Historically, after sharp gains across the board, the market often enters a cooling-off period.

Market Volatility After Sharp Rally

Despite the sharp drop in Chinese-related ETFs, the recent inflows of funds reflect strong optimism in the overseas market. The cost of short-term options for China-related ETFs in the U.S. also hit new highs on Monday, signaling strong bullish sentiment among investors. Some big traders have rolled their profit positions to higher prices, hoping to expand their gains if the rally continues.

However, signs are emerging that some “cautious” investors are setting up protections in case the rally fades. For instance, last week, more than $200 million was poured into $Direxion Daily FTSE China Bear 3X Shares(YANG)$ .

In the face of this volatility, investors might consider using option strategies like Bear Call Spread to short the market.

What is Bear Call Spread?

A bear call spread is an options strategy for when a trader expects the underlying asset’s price to decline in the near future. It allows traders to short the asset while keeping risk in a defined range.

Specifically, a bear call spread involves buying call options at a certain strike price and simultaneously selling the same number of call options at a lower strike price, both with the same expiration date.

Study Case: Shorting KWEB Example

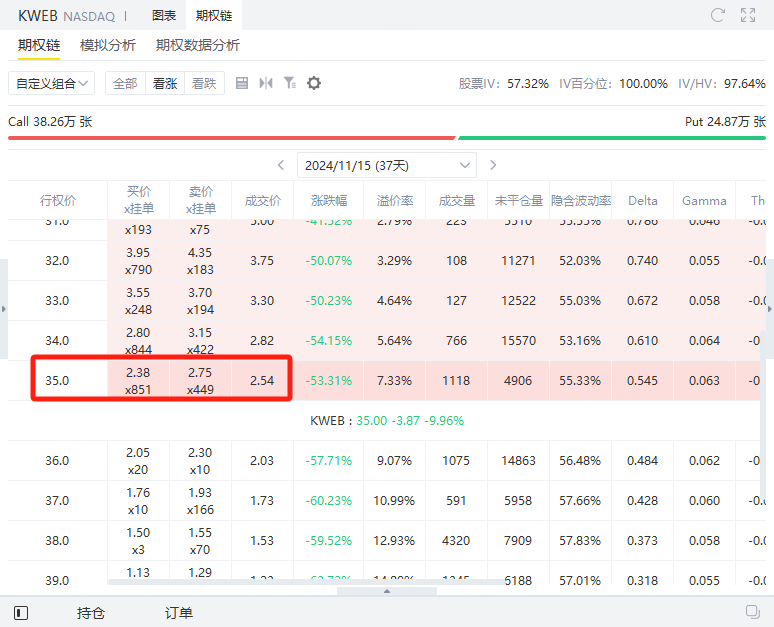

Let’s take shorting the $KraneShares CSI China Internet ETF(KWEB)$ as an example. KWEB is currently priced at $35. Suppose an investor expects it to drop to around $30 by November 15. The investor could use a bear call spread to short KWEB.

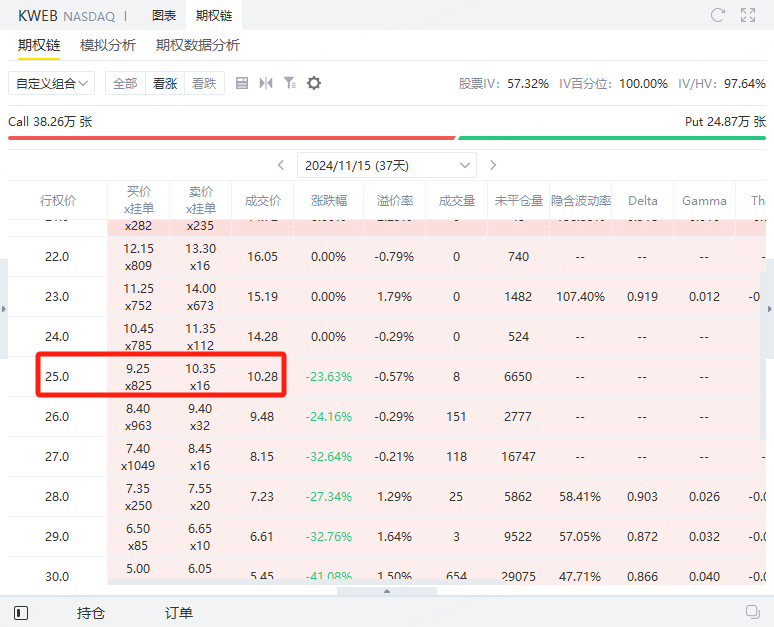

Step 1: Sell a call option expiring on November 15 with a strike price of $25, collecting $1,028 in premium.

Profit and Loss Analysis

- Max Profit: If KWEB’s price is below $25 at expiration, both options expire worthless, and you keep the net premium. Max Profit = $774 (no obligation to exercise)

- Max Loss: If KWEB’s price is above $35 at expiration, the $25 call option will be exercised. Max Loss = (Difference between strike prices, $35 - $25 = $10) * 100 contracts - Net premium = $1,000 - $774 = $226.

So, your Max Profit is $774 when KWEB is $25 or below, and your Max Loss is $226 when KWEB is $35 or above.

The beauty of a bear call spread is it reduces the risk of shorting (buying the higher strike call offsets the risk of selling the lower strike call). Shorting stocks directly has theoretically unlimited risk if the stock price surges, but with this spread, the risk is much more controlled.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.