GSK: Earnings Confirm It's On Track To Meet Guidance

- GSK is on track to achieve its guidance for 2024, with its Q3 2024 and 9m 2024 results today.

- For 9m 2024, the company's turnover growth at 9% is at the upper end of the guidance range and core EPS growth of 14% exceeds it.

- While the numbers slumped in Q3 2024, this was expected, especially as reported earnings absorbed Zantac related payouts. They are unlikely to impact full year figures, however.

- In the meantime, the forward P/E is attractive and the dividend yield isn't bad either.

Wirestock

British pharmaceutical company GSK (NYSE:GSK) reported its third quarter (Q3 2024) and nine months 2024 (9m 2024) results earlier today, which indicate that it's on track to achieve the full-year targets. This is even as Q3 2024 figures showed softening. Here, I take a closer look at the latest figures and what they mean for the stock going forward.

Results on track to achieve full-year guidance

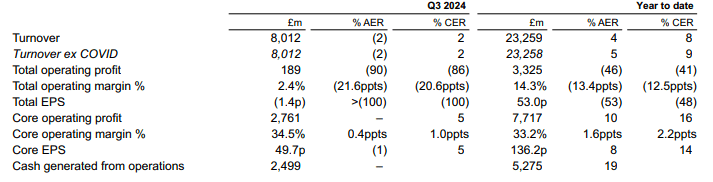

For 9m 2024, GSK saw turnover ex-Covid growth of 9% year-on-year (YoY) at constant exchange rates [CER] and core earnings per share [EPS] growth of 14% YoY (see table below). The turnover growth is at the upper end of the company's projection of a 7-9% increase for the full year 2024. Core EPS growth is even higher than anticipated, at 10-12%.

Financial Highlights, Q3 2024 (Source: GSK)

Where the weakness showed up

This continues to reflect progress for the company, even as there are pockets of weakness in the figures, as follows:

- Turnover growth softens in Q3 2024

Turnover growth slowed down to 2% YoY in Q3 2024, compared to 13% YoY in Q2 2024. But this was to be expected. Following the release of its first half (H1 2024) results in July, I had actually penciled in a contraction in turnover in H2 2024.

From that perspective, the number is actually better than expected so far. It would still be worrisome if the expected weakness were due to a lack of demand, which is true in the case of vaccines (discussed below). But more broadly speaking, the company has pointed out earlier, “the annualisation of product launches and stocking impacts" are seen as the reason for the softening.

- Reported earnings turn negative

Expectedly, the company's reported earnings were affected by the payout for Zantac related settlements. I had last written about GSK earlier this month, following news that it had finally settled a majority of the long-pending cases against its heartburn medication drug Zantac, which was alleged to be carcinogenic.

Positive as the development is for the long-term stability of GSK's stock price, in the short run, a pullback in earnings was expected. The company had said that Q3 2024 figures will reflect the settlement amount of GBP 1.8 billion (USD 2.3 billion).

So it's really no surprise that it clocked a minor loss during the quarter, even though this is a worse than my expectation of a small EPS of GBP 0.11 in the quarter. The estimate was based on the expectation of a GBP 0.55 of EPS in H2 2024, less, a GBP 0.44 per share hit from Zantac payouts.

What the strengths are

That said, there are notable positives in the latest earnings report too:

- Core earnings unaffected by Zantac payouts

I had also penciled in a hit to the core EPS figure from the Zantac payments, to cover all possibilities. But as it turns out, they weren't affected, resulting in a 5% YoY rise in the number Q3 2024 at CER and a 14% YoY increase for the corresponding figure for 9m 2024. As a result, the actual figure for core EPS at GBP 0.497 is significantly superior to the near nil figure I had factored in.

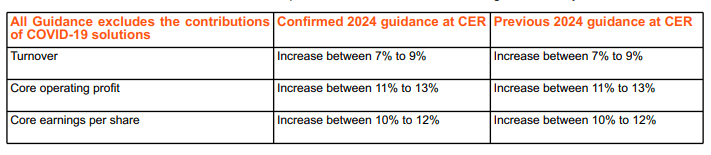

- Projections for 2024 sustained

Further, the company's guidance for core EPS for 2024 remains unchanged (see table below). In fact, with the growth rate exceeding the guidance range for up to 9m 2024, I think there could even be the possibility of an upside surprise to Q4 2024 earnings.

Next, despite the softening in Q3 2024, GSK has sustained the guidance for 2024. With the YTD growth in turnover at 9% YoY, even with a small pullback in Q4 2024, the company could achieve its target.

Source: GSK

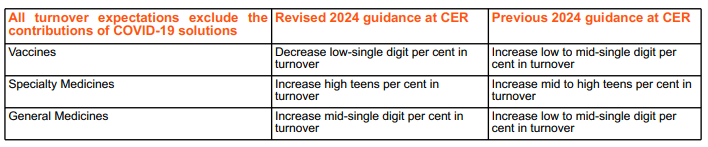

- Specialty medicines and general medicines support growth

The improved forecast for both specialty medicines and general medicines support the turnover guidance, even as the outlook for vaccines has taken a turn for the worse. In my article in July, following the H1 2024 earnings, I had pointed to the weak trend in the sales of Arexvy, the company's vaccine for respiratory infections, as something to watch out for.

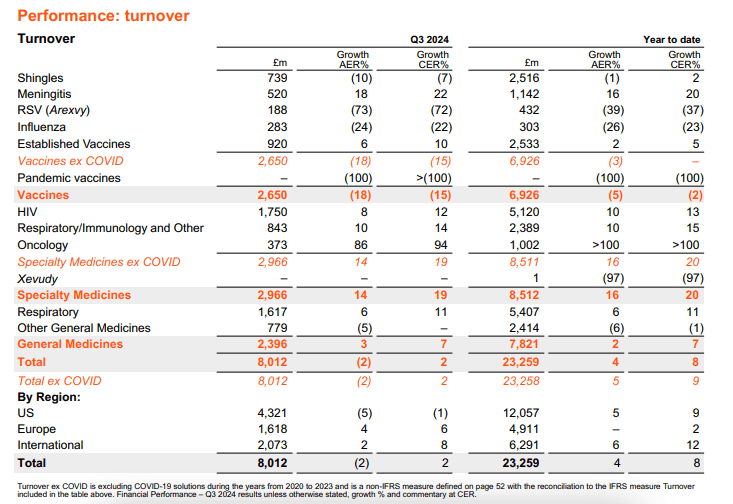

Launched in Q3 2023, the vaccine was an instant success, bringing in over 20% of the revenue for the vaccines segment. But the number quickly started dwindling and a year later, in Q3 2024, it has contributed to just 7.1% of the revenues for vaccines. The company attributes this to current restrictions on its usage in the US, along with a priority for Covid-19 vaccinations over the others.

At the same time, the growth in specialty medicines, of 19% YoY in Q3 2024 and 20% in 9m 2024 is notable. As a result, it has now become the biggest contributor to GSK's turnover with a ~37% contribution in 9m 2024, on a broad-based increase across its sub-segments (see Table 2 below) and seen an upgrade in forecast (see Table 1 below).

Table 1: Forecast by segment (Source: GSK )

Table 2 (Source: GSK )

What the results mean for stock metrics

Even after penciling in a possible reduction in core EPS earnings due to Zantac payouts, the stock's forward non-GAAP EPS at 12.3x was somewhat competitive compared to its five-year average ratio of 12.84x.

Now, with no impact expected on core earnings, the ratio looks even better at 8.5x, assuming that the earnings come in at the midpoint of the guidance range for 2024. Further, analysts estimates anticipate another 15.4% increase in EPS in 2025, which puts the ratio at an even lower 7.4x for next year. This suggests that by next year, the stock has the potential to rise significantly from current levels.

The company has maintained its dividend levels at GBP 0.60 per share, which puts the forward yield at 4.1%. This might be lower than the stock's five-year average levels of 4.65%, but it's still higher than the healthcare sector's average of 1.47%.

What next?

The big picture for the GSK story remains unchanged. While Q3 2024 figures showed the expected softening in turnover growth and weakness in reported per share earnings, the outlook remains unchanged. Core earnings, for one, were unaffected by the big Zantac payout that was absorbed in the latest quarter. And the robust growth in the company's specialty medicines division can continue to drive turnover forward, even as the vaccines segment is impacted.

The stock's metrics look rather attractive, especially now that there's not much more Zantac related uncertainty, and continued expected earnings growth confirms this further. I'm retaining a strong buy on GSK. This can change, if the guidance for 2025 turns out to be softer compared to current expectations, though.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.