Jobs Report Sends Mixed Signals, But Another Rate Cut Is Still Very Likely

- In an unusual labor market report, the unemployment rate stayed steady while payroll figures took a nosedive in October, which is explained by estimation differences.

- With temporary reasons affecting payroll figures, though, a big rate cut from the Fed is unlikely, although there's still good reason for one.

- With a fairly strong macro-picture in place right now, investors might stand to gain from making some braver, though still careful, choices.

David Ryder/Getty Images News

The October jobs report released earlier today reflected mixed signals, with the unemployment rate remaining unchanged on the one hand and a dramatic drop in non-farm payroll increases on the other. Factors like Boeing's (BA) strike action and the two hurricanes, Helene and Milton, impacted the readings differently.

Whichever way we interpret the numbers, though, a more comprehensive view of the economy indicates a strong likelihood of another rate cut in the Fed's November meeting, though not a big one. The cut can make the environment even more conducive for investors, calling for a still careful, but braver spirit.

Labor market gives mixed signals

As anticipated, temporary factors affected the labor market report for October. The impact was limited to the payroll figures. The details are as below.

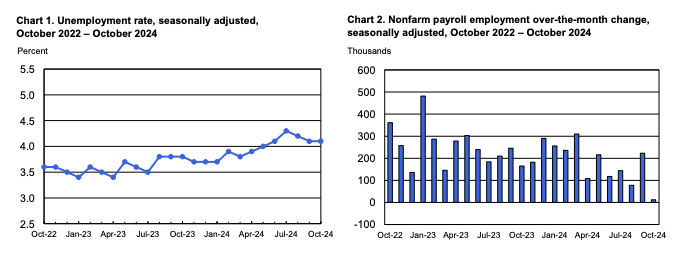

- The unemployment rate remained unchanged from the previous month at 4.1%, in line with expectations. The number is also the modal value for 2024 so far now, with the rate being observed in three of the past 10 months. The mean unemployment rate is a bit lower at 4%, however.

- Non-farm payroll increases were at just 12,000, however, a sharp decline, which makes it the worst reading since April 2020, when the figures contracted due to the onset of the pandemic and the subsequent lockdowns. The latest numbers are also a dramatic drop from the initial estimates of 254,000 gains in September and a 93.8% drop from the average monthly gains of 194,000 over the past year.

- Downward revision in earlier non-farm payroll gains was also observed. The August number was revised downwards by 81,000 to 78,000, while the September figure is now down by 31,000 to 223,000. Note that these figures were below the monthly average gains over the past year even earlier, now they are even more so.

-

Average hourly earnings grew 0.4% MoM in October, same as the initial estimate for September. The figure for September was also revised upwards to 0.5%. Interestingly, growth remained slightly higher than the forecast of 0.3%, much like last month.

Key Labor Data\ (Source: Bureau of Labor Statistics)

Why are payrolls weak and not unemployment numbers?

On the face of it, it doesn't make sense that the unemployment rate should stay unchanged while the payroll figures sink. The answer is found in the methodology for estimating the numbers. While the unemployment data is based on the household survey data, payroll numbers are based on the establishment survey data. The payroll estimation process considers strike activity as a loss of jobs, unemployment estimates don't.

Strike action drags payrolls down

In my last update on the labor market, I had mentioned the risk to unemployment numbers this month. For reasons of estimation method, Boeing's strike was expected to impact the numbers only to the extent of the spillovers of industrial action on suppliers. Clearly, that wasn't a significant figure, as the household survey shows.

With no less than 33,000 workers participating in the strike, the establishment data reflects the impact completely, in the numbers for manufacturing activity. A total of 46,000 manufacturing jobs were lost during the month. Of these, 44,000 were on account of the industrial action that affected transportation equipment manufacturing. If it weren't for these losses, the total payroll figure would have instead increased by 56,000. That, too, is a come-off from the 78,000 figure for September, but to a far smaller extent.

Hurricanes add to the woes

Additionally, the hurricanes impacted the figures as well, though that's a less straightforward exercise. It's possible that the impact was limited though, considering that the hurricane-hit state of North Carolina, in particular, contributes to a relatively small 3.1% of the total employment, though Florida, the other impacted state, has a far bigger 6.1% contribution.

Still, estimates from Bank of America indicate that along with strike actions, the hurricanes were responsible for lowering the job count by 50,000 in October. With 44,000 of the losses due to strike activity, this indicates a far smaller 6,000 losses due to the hurricanes.

Implications for the FOMC rate decision

However, despite the dramatically weak payroll figures, the Fed is unlikely to be moved into making a big rate cut in the November meeting. Here's why:

- Boeing workers could be close to a deal with the company's management, which will relieve some of the pressure on upcoming payroll figures anyway.

- While long-term employment losses from hurricanes can affect labor market data over time, reconstruction work can play its part in creating some balance. It's estimated that some 1.4 million jobs will be created as a result of the recent hurricanes, which is just shy of 1% of the total employed workforce.

- With the first of the unemployment rate figures for Q4 2024 now released, the figure would have to average at 4.55% in the next two months to come in at the Fed's forecast rate of 4.4%. This appears unlikely, as the economy is in a robust place. The advance estimates for Q3 2024 GDP growth show an above-trend 2.8% growth.

The cut might not be big, but the latest inflation data makes a case for a cut nevertheless. The Fed's target inflation measure, the Personal Consumption Expenditure (PCE) inflation for September came in at 2.1% YoY, which undershoots the reserve's forecast of 2.3% in Q4 2024.

Core PCE inflation remains slightly higher at 2.7% compared to the target of 2.6%, though. But even this figure is close enough. Further, after seeing a rise for two weeks starting in the last week of September, crude oil prices have also subsided, which can support inflation as well.

Where to invest

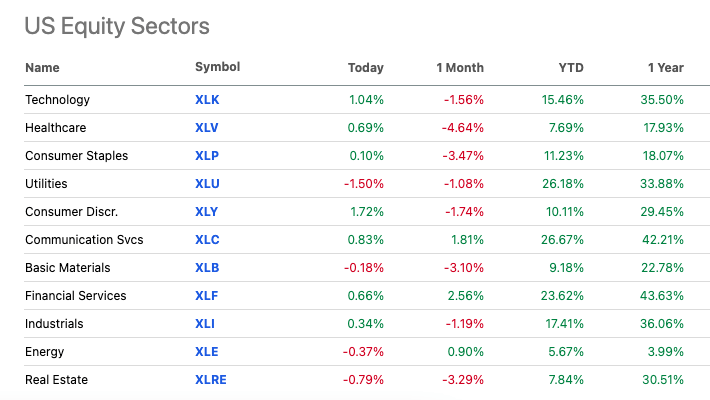

Stock markets have responded well to the labor market report. The NASDAQ 100-Index (NDX, QQQ) has seen the biggest rise of 1.2%, followed by the Dow Jones Industrial Average (DJI) with a 1% increase and S&P 500 (SP500, SPX, SPY) with an increase of 0.8%. With the economy still looking strong and inflation has softened to comfortable levels, this is unsurprising.

It would ideally be a time to get braver and look beyond traditional defensives now that there's much improvement in the macro data. Except that there are still risks of a growth softening in the US going forward and global factors, like weak Chinese growth, can impact the outcomes for cyclicals like commodities and consumer discretionary goods, which have seen relatively muted increases year-to-date (YTD) anyway (see table below).

Source: Seeking Alpha

At the same time, there are still promising stocks among cyclicals, though they need to be picked carefully. Two that I liked recently are the luxury fashion stock Ralph Lauren (RL), which has been an outlier in a sagging market this year. The other one is Norwegian Cruise Line (NCLH), which benefits from the still ongoing recovery from the pandemic.

In conclusion

As always, the stock markets continue to throw up investing opportunities. While the latest drop in payroll figures is nothing to take lightly, it could be more due to temporary factors than anything else. This indicates that the labor market could well continue to stay strong. Along with the above-trend GDP, subdued inflation rate, and the likelihood of a rate cut, cyclicals may well, if selectively, start shining soon enough.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.