Japan Tobacco: The Vector Group Acquisition Impact

- Japan Tobacco Inc.'s YTD gains are unsurprising, given its muted profit outlook, high market multiples, and lower dividend yield compared to peers even towards the start of the year.

- Its recent acquisition of Vector Group raises concerns further about Japan Tobacco's future sustainability as it focuses more on traditional tobacco than next-generation products.

- The acquisition's cost can also significantly impact earnings, raising the forward P/E ratio and potentially impacting dividends.

BalkansCat/iStock Editorial via Getty Images

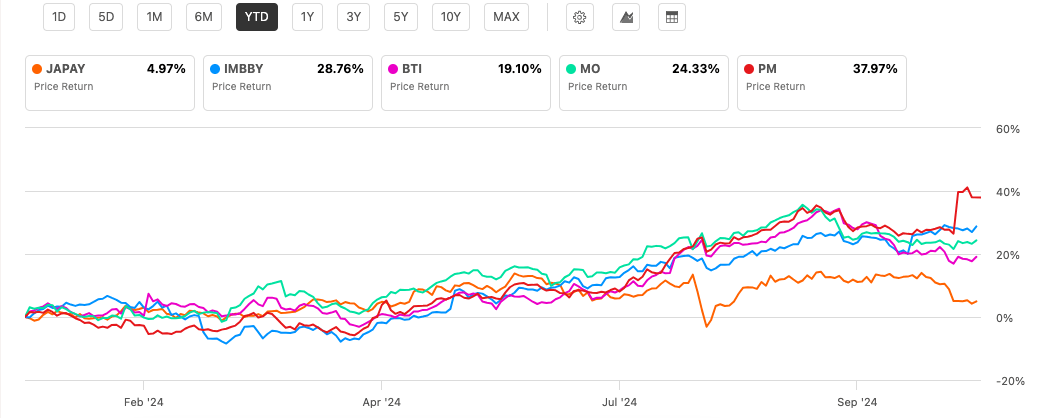

Japan Tobacco Inc. (OTCPK:JAPAF, OTCPK:JAPAY) has seen disappointing developments in its stock market fortunes this year. It has clocked the smallest gains among the five biggest tobacco stocks by market capitalization (see chart below). This is in stark contrast with last year, when it was ahead of the rest and saw a whole 25% price rise.

That said, when I wrote about it in February, the signs of future stalling in price were already there. The company expected profits to contract a bit in 2024, its price-to-earnings (P/E) ratio was elevated and its dividend yield wasn't competitive compared to peers.

Price Returns YTD for JAPAY, IMBBY, BTI, MO and PM (Source: Seeking Alpha)

Admittedly, though, it has been a while since the update. Much has happened for Japan Tobacco since, which further explains why investors are shying away from it.

Further expansion into traditional tobacco

In the biggest news for the stock this year, it recently completed the acquisition of the US-based Vector Group [VGR]. With VGR focused solely on cigarettes, along with a small interest in real estate investments. At a time when the pivot to next-generation products is crucial for tobacco biggies, this appears to be a step back for Japan Tobacco.

To be fair, the company outlines good reasons for the acquisition as follows:

- It allows expansion into the big US market, since VGR is the fourth-largest tobacco manufacturer in the US. The company anticipates to increase its market share in the country from 2.3% to 8%.

- It also stands to become a bigger company, though by a small margin. VGR had a market capitalization USD $2.36 billion before delisting. Added to JAPAY's market capitalization, that pushed it up to over USD $50 billion, even as its position as the fourth-biggest tobacco stock remains unchanged.

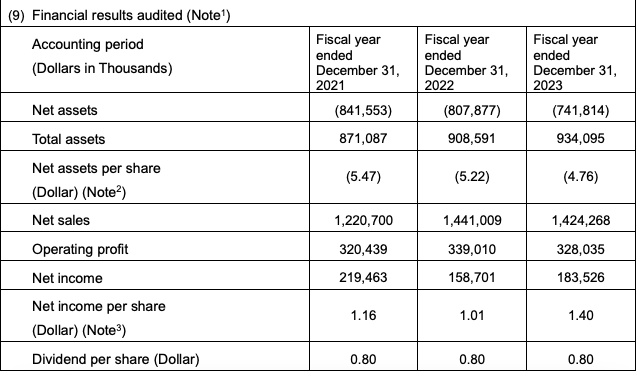

- Similarly, the acquisition stands to add to the company's financials, albeit in a limited way. VGR had net sales of USD $1.4 billion and a net income of USD $183.5 million in 2023. This bumps up Japan Tobacco's revenue by 7.6% and net profits by 5.8%.

Vector Group, Key Financials (Source: Japan Tobacco)

While the acquisition can open the doors for more in the market, for now, the renewed focus on traditional tobacco products rather than making further inroads into next-generation products isn't the most encouraging development.

Limited gains for RRPs

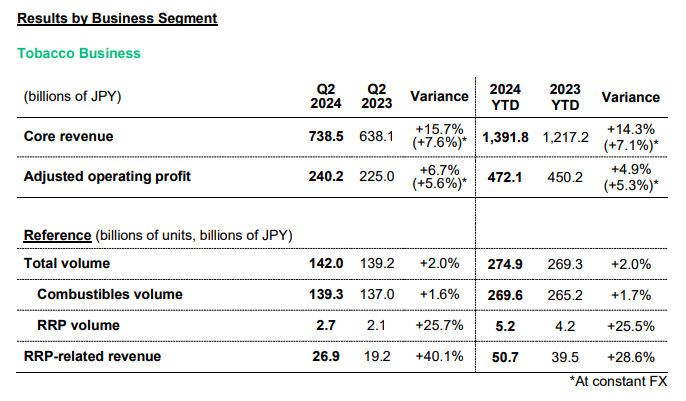

This is especially as the company is already lagging on newer nicotine products. In the first half of 2024 (H1 2024), its reduced-risk products [RRPs], contributed to just 3.6% to tobacco revenues. Further, with the addition of VGR's tobacco revenues to its own, the share of RRPs is set to reduce even further.

In defense of the company, this is a slight improvement over the 3.3% share in 2023, due to RRPs higher revenue growth. They grew by 28.6% YoY in H1 2024, a far bigger increase than the 14.3% YoY seen for overall tobacco revenues during the period. Their volumes also saw double-digit increases (see table below).

Further, the company's heated tobacco products under the Ploom brand have expanded to 21 countries, from 13 in 2023. And this is just halfway through the company target of selling in 40 countries.

Source: Japan Tobacco

Earnings set to be impacted

Further, it's fair to expect that the acquisition will impact Japan Tobacco's earnings this year. Even after upgrading its forecasts for 2024 along with the release of its H1 2024 results, it still expected a small contraction of 1.5% YoY in profits. But the acquisition price at JPY 378 billion (USD $2.4 billion), it can be reduced by almost 80% of this forecast (see table below).

This will bring the profit figure to just JPY 79.6 billion, an 83.5% YoY decline. If VGR's financials get reflected in Japan Tobacco's earnings from next earnings release itself, there would be a smaller drag on profits. But it won't be significant, going by its limited expected contribution, as noted above.

Stock metrics

- Market multiples

To estimate JAPAY's forward P/E, however, here I assume only the negative impact of the acquisition on the full year 2024 profits. As would be expected, this reflects a big jump in the ratio to 91.5x from the 15.4x based on the company's latest profit projections, since they pre-date the acquisition.

Even looking into 2025, the P/E remains unconvincing. To estimate the profits for next year, I assumed that it will clock JPY 475 billion in profit next year, which was expected for this year. VGR is assumed to see a net profit growth of 15.6% in both 2024 and 2025, much like it did in 2023. This brings its contribution to JPY 38.3 billion.

In total, Japan Tobacco's profit is then at JPY 513.3 billion (USD $3.35 billion) for 2025. This results in a forward P/E of 14.2x. Only Philip Morris (PM) has a higher ratio for the next year, 18.3x, but then it offers an advantage in that made the biggest gains in pivoting towards next-generation products, so some premium on the stock is warranted. All the other big tobacco stocks are trading at sub-10x P/Es for 2025.

- Dividends

JAPAY's forward dividend yield at 4.97% already doesn't compare well with peers either. Again, it's higher only than that for PM, which has a 4.14% yield, but PM is in a league of its own right now. The average yield for the big five tobacco stocks is at 6.5%. With the VGR purchase, dividends could be impacted as well, considering that the company has maintained a payout ratio of 70-75% in the past three years.

What next?

The Japan Tobacco story looks far less encouraging now than it did when I last checked on the stock. Its acquisition sets it back on the contribution of newer nicotine products, even as it expands the company's footprint in the big US market. The purchase will also impact its financials for the year. JAPAY's forward P/E was already high compared with peers, and now it's sky-high.

It can subside considerably by 2025, though. But along with the muted Japan Tobacco Inc. dividend yield compared with peers, I don't see any particular gains coming in the next year. In fact, there's a chance its dividends can be cut. At this point, however, it's best to wait for its Q3 2024 earnings release due on October 31, which could carry updated forecasts. I'm retaining a Hold rating.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.