Ralph Lauren: Attractively Priced As Margins Expand

- Ralph Lauren is an outlier luxury stock, with a double-digit price rise YTD, even as the sector struggles.

- Revenues continue to grow, even if slowly, particularly in the challenged China market. Margins are forecast to expand as well.

- While the stock's forward P/E is elevated compared with peers, it's still rather attractive compared to its own past average.

winhorse

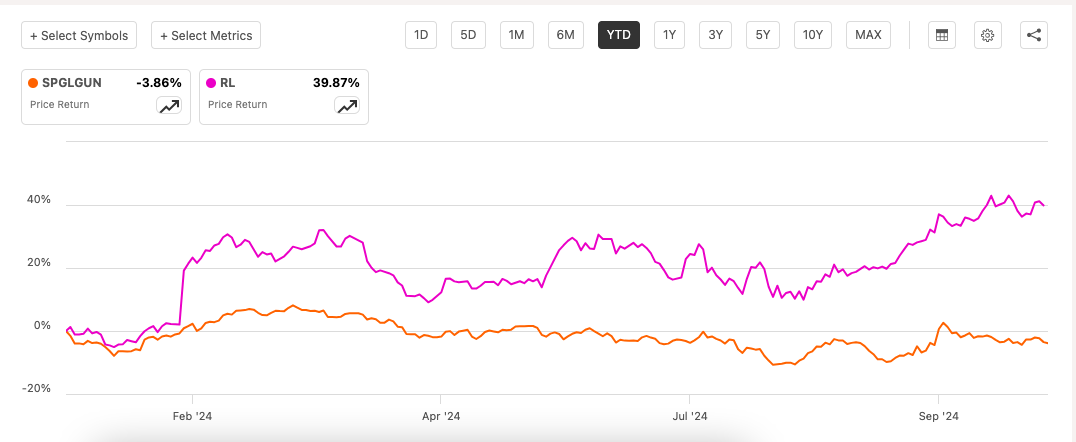

If there's any outlier luxury stock out there right now, it has to be Ralph Lauren (NYSE:RL). The S&P Global Luxury Index (SPGLGUN) is down by ~4% year-to-date (YTD), but in sharp contrast, RL is up by 40%.

Signs that it's undervalued were visible even when I last wrote about it over a year ago. However, the stock's continued progress despite a weakening luxury market calls for a closer look, especially with its second quarter (Q2 FY25, quarter ending September 2024) results due next week.

Price Returns (Seeking Alpha)

Still deeply undervalued, in some respects

It's not hard to see why RL has seen a steep price increase from purely the market multiples perspective. To estimate the stock's forward non-GAAP price-to-earnings (P/E) ratio, I first made a calculation for its FY25 earnings. The earnings forecast is based on the following assumptions:

- In line with the company's projections, reported revenues are assumed to grow by 1%.

- Similarly, the adjusted operating margin assumption is 13.6%, which is the midpoint of the company's guidance range.

- In line with 2023 figures, the ratio of adjusted net profit to adjusted operating profit is expected to be 83%.

Trading significantly below average...

They yield a net income of $756.5 million, which is a 10.3% YoY increase and translates into a 16.51x forward non-GAAP price-to-earnings (P/E) ratio. This is attractive for two reasons:

- It's significantly lower than the stock's five-year average of 30.8x. This is despite robust double-digit earnings growth in Q1 FY25 and FY24 of 15% YoY and 23.6% respectively.

- It's also a shade lower than the median P/E of 17.06x for the consumer discretionary sector.

...but highly-priced compared to the closest peers...

There is a catch, however. And that's the valuation comparison with its closest peers. For this analysis, I considered the four closest companies to it in terms of product category and market capitalization. Of these, only, V.F. Corporation (VFC) of brands like The North Face and Timberland trades higher at 47.3x.

The closest to RL by market capitalization, Tapestry (TPR), of brands like Coach and Kate Spade, trades at 10.8x. Smaller stocks in terms of market capitalization like Calvin Klein and Tommy Hilfiger owner PVH Corp. (PVH), and Versace and Jimmy Choo owner Capri Holdings (CPRI) trade even lower at 8.44x and 8.28x, respectively.

...for good reasons though

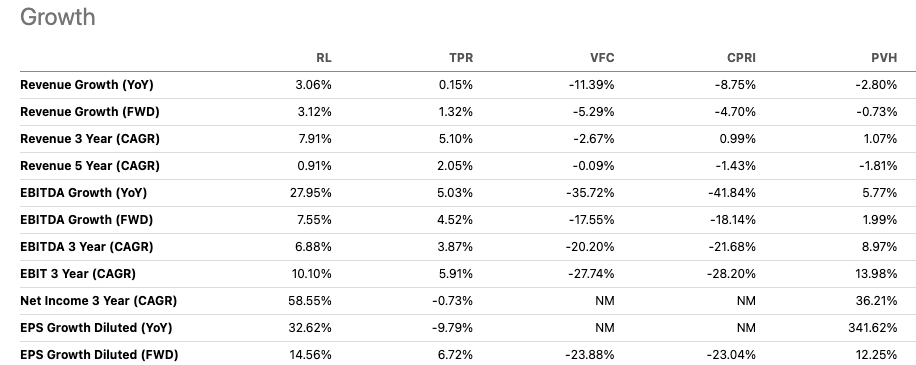

There are good reasons for a premium for RL, though. As the table below shows, it has performed much better overall in terms of both revenues and earnings. Specifically, the three-year compounded annual growth rate (OTC:CAGR) for revenues is at 7.9%, compared to the average of the five stocks at 2.5%. Similarly, the CAGR for EBIT is also good at 10.1%, second only to PVH at 14%.

Financials, Comparison with Peers (Seeking Alpha)

Revenue growth seen in Q2 FY25 and FY25

The company's prospects for FY25 aren't too bad either, considering the state of the luxury market, which can continue to justify its premium valuations. Its revenue is expected to continue growing, even as growth itself is expected to soften, as follows:

- RL forecasts revenues at constant currency (CC) to grow by 2-3%, which is a small decline at the midpoint from the 3% growth seen in FY24.

- So far, though, it's performing relatively well. In Q1 FY25, revenue growth was at 3% YoY, which is the top end of the guidance range. And they are expected to grow by 3-4% in Q2 FY25, which is 0.5 percentage points higher than the 3% increase seen in Q1 FY25 and also above the full-year guidance range.

This revenue growth is nothing great, but besides the fact that some of the biggest luxury companies are seeing an even bigger slowdown, RL still stands out for two reasons:

#1. Growth despite unfavorable exchange rate impacts

It's notable that despite an unfavorable currency translation effect of ~1.5 percentage points expected in FY25, it will still see around 1% reported revenue growth, even as it's down from 3% in FY24.

The foreign exchange impact already became visible in Q1 FY25, with exactly 1% reported revenue growth. In Q2 FY25, though, this can improve with a forecast of 1.9% YoY.

#2. Europe and Asia hold up revenues

Further, RL is growing despite continued weakness in its biggest market, North America, which brings in 40% of its revenues. In Q1 FY25, the market contracted by 3.7% YoY. Reported revenue growth still continued to be positive because of support from Europe, which saw a 6.3% YoY increase.

Surprisingly, Asia, which has been a challenge for luxury companies recently owing to soft trends in China's consumer market, also saw a 3.5% YoY increase. In fact, RL points to the fact that demand in the Chinese market grew in "high-single digits" in reported terms during the quarter.

Ralph Lauren

Margin expansion to continue

Margin expansion is expected to continue too. The gross profit margin at CC is expected to increase by 0.5-1 percentage points in FY25 to 67.5% from 66.8% in FY24.

Owing to gross margin expansion and softening in some pockets of operating expenses, the operating margin at CC is also seen expanding by 1-1.2 percentage points in FY25. This will drive it up to 13.6%, at the midpoint, from 12.5% last year. Incidentally, this is an even bigger margin expansion compared with the 0.5 percentage point rise seen last year.

In Q2 FY25, too, the operating margin is expected to expand YoY, albeit to a lesser extent than that for the full year. With a forecast 0.8-1.2 percentage point increase from the 10.5% in Q2 FY24, the number comes to 11.5% at the midpoint.

What next?

The key takeaway from the discussion is that there are clear reasons for RL's continued uptick this year. Its revenues are still growing, and are expected to continue doing so in FY25. Growth in the company's China market, in particular, is both surprising and heartening.

Margins are expanding, and with profit growth expected this financial year, its forward P/E is still justifiable. Not only is it slightly lower than that for the consumer discretionary sector, but it's also lesser than the stock's five-year average. Even the premium over its closest peers can be justified due to superior performance.

The only challenge for RL right now is the big but weak North American market. While there's nothing in the US economy's growth so far that suggests concern, a soft landing for it can affect the company's growth going forward. I'm retaining a Buy rating, but if things take a turn for the worse in its key markets, this can change.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.