Albemarle: Navigating Stormy Seas With Limited Visibility

- Albemarle Corporation's stock remains a “Sell” due to declining revenue, profitability issues, and significant overvaluation despite a 17% price drop since January.

- Lithium prices have halved over the past year, leading to an oversupply and negative sentiment for Albemarle's upcoming earnings release on November 6.

- Valuation models [DDM and DCF] indicate substantial downside potential, with DDM suggesting a fair value of $35.24 per share, far below the current price.

Just_Super

Investment thesis

My initial bearish thesis about Albemarle Corporation (NYSE:ALB) aged well, as the stock became cheaper by around 17% since late January. Headwinds for lithium prices are poised to remain strong in the foreseeable future, which makes it difficult to expect positive earnings surprises on November 6. The company's revenue is declining rapidly, and profitability is melting down. Furthermore, various valuation approaches suggest that the stock is significantly overvalued. All in all, I reiterate my "Sell" rating for Albemarle.

ALB Q3 earnings preview

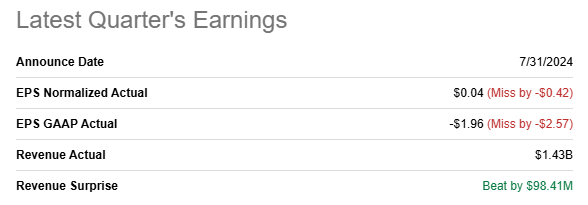

Albemarle released its latest quarterly earnings on July 31, when the company delivered a positive revenue surprise but showed a wide EPS miss. The Q2 revenue plunged by almost 40% YoY. The adjusted EPS declined year-over-year from $7.33 to almost zero.

Seeking Alpha

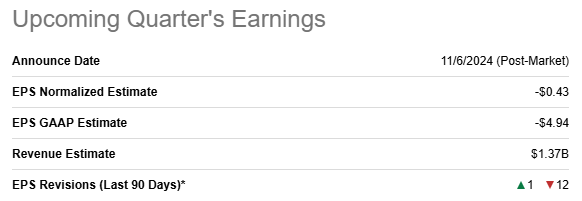

I would rather not focus much on the previous earnings release because the company releases its Q3 earnings on November 6 after the market close. Wall Street analysts expect quarterly revenue to be $1.37 billion, which will be around 40% lower on a YoY basis. The quarterly adjusted EPS is expected to go negative for the first time over the last several years.

Seeking Alpha

Wall Street's sentiment regarding the upcoming earnings release is predominantly negative, with 12 EPS downgrades. While such sentiment is rarely a positive indicator, there is another perspective to consider. Lower analyst expectations can make it easier for Albemarle to exceed them.

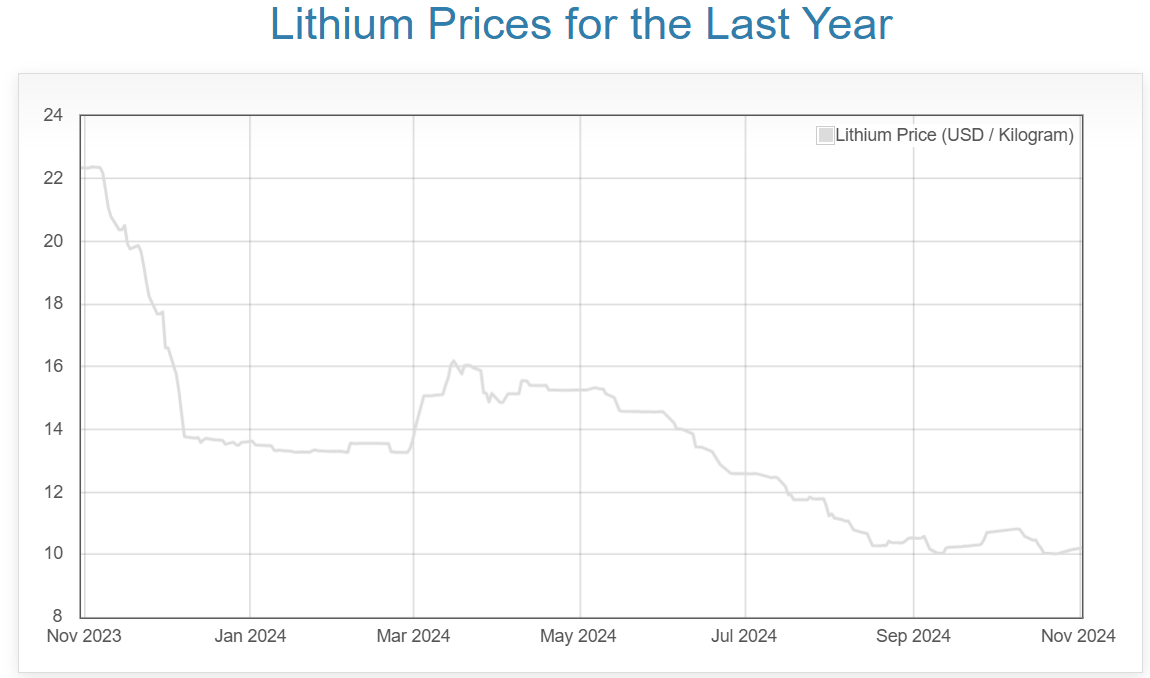

While it appears that strong secular trends in EVs are beneficial for the lithium industry, the foreseeable future for large lithium producers looks cloudy. Lithium prices more than halved over the last twelve months. The picture looks much worse if we compare current lithium prices to all-time highs. As shown below, the current price is around $10 per kilogram. The historical record was achieved in late 2022 and the price was above $80 per kilogram.

dailymetalprice.com

The significant spike in lithium prices following the pandemic can be attributed to Tesla, Inc.'s (TSLA) soaring EV deliveries during the pandemic and through 2022. Additionally, the shock in oil markets after the onset of the Russia-Ukraine war contributed to a FOMO effect in lithium prices, as EVs became more attractive compared to internal combustion engine cars amid rising gasoline prices. However, gasoline prices did not remain high for long, as the Fed's aggressive monetary tightening adversely affected demand for Tesla's EVs. This was because most purchases were financed with debt instruments, making monthly car payments less attractive for consumers. As a result, the lithium market currently experiences substantial oversupply. According to Clean Energy Associates, lithium prices can remain through 2028.

Seeking Alpha

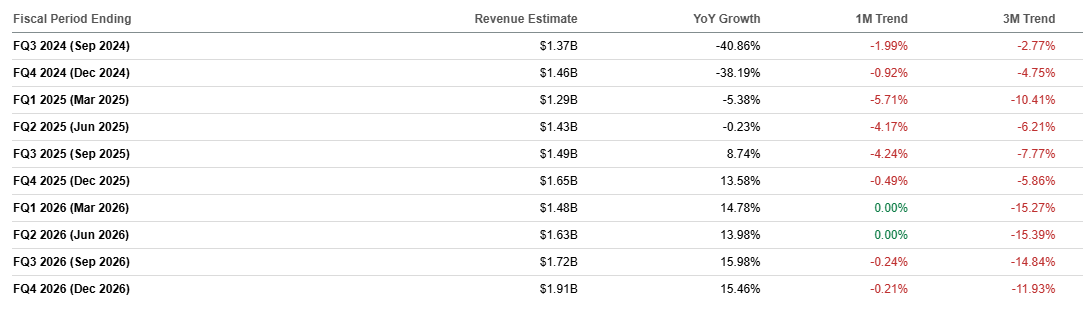

When a company faces such headwinds, it is difficult to expect miracles from the upcoming earnings release. The situation with the oversupply looks complex, and it is reflected in recent trends in ALB's quarterly revenue revisions. All changes are mostly in red, and the extent of downgrades also appears notable.

TrendSpider

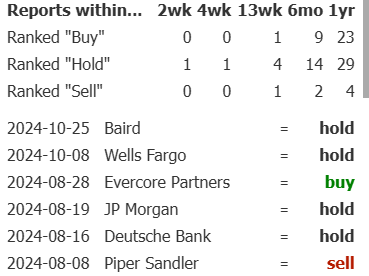

Consequently, it is not surprising that Wall Street analysts rarely recommend buying the stock with mostly "Hold" ratings.

Valuation update

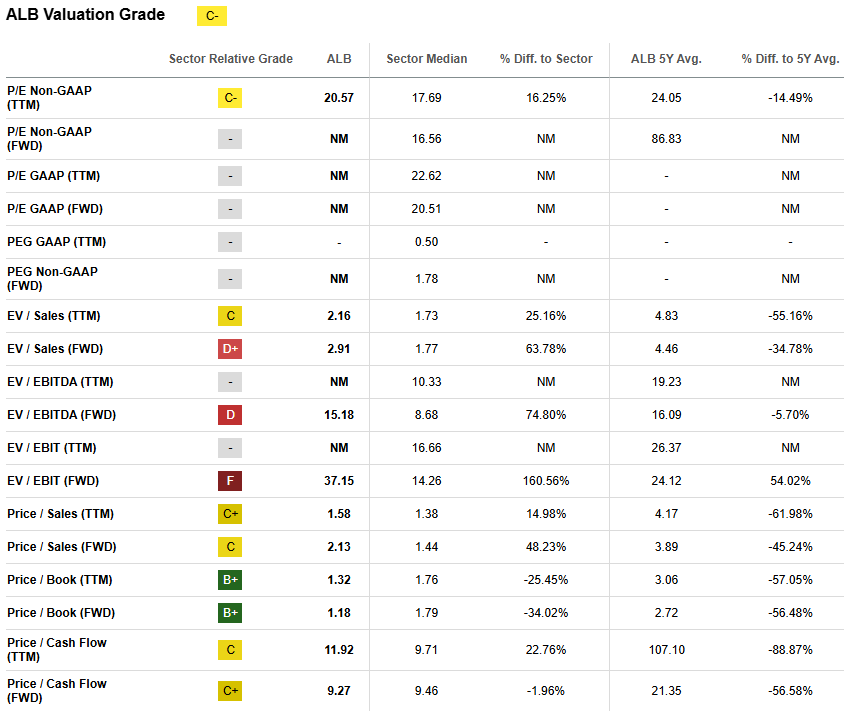

ALB declined by around 15% over the last 12 months, substantially lagging the broader U.S. stock market. Performance so far in 2024 is even worse, with a 30% YTD plunge. ALB's valuation ratios look reasonable compared to the sector median. I prefer to ignore comparisons with ALB's historical averages because expectations around lithium demand growth were likely too high during the pandemic craze.

Seeking Alpha

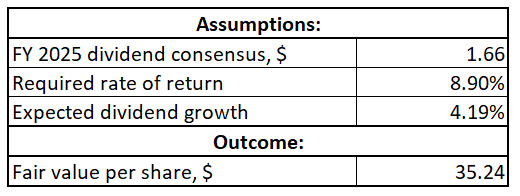

Albemarle's dividend consistency is solid. Therefore, the dividend discount model [DDM] is a sound valuation approach to proceed with. The FY2025 dividend consensus estimate is $1.66. ALB's cost of equity is 8.9%, which is my required rate of return assumption. The last decade's dividend growth CAGR is 4.19%, which is the third key assumption for my DDM calculations.

Author's calculations

The suggested DDM fair value per share is $35.24. This is almost three times lower compared to the current share price, which makes me doubtful about the suitability of the DDM to value ALB.

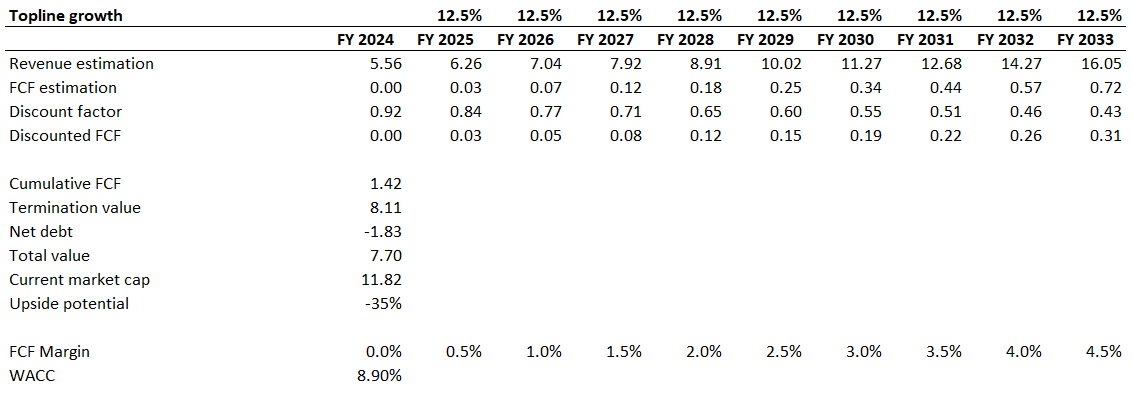

Therefore, let me also simulate the discounted cash flow [DCF] model. I use the same 8.9% discount rate. I rely on a consensus revenue estimate for FY 2024 and apply a 12.5% revenue CAGR for the next decade. Albemarle's TTM FCF margin is negative, but the company's liquidity metrics are solid. Therefore, I implement a zero FCF margin for the base year and expect a steady 0.5 percentage point yearly growth.

Author's calculations

The company's valuation looks much better from the DCF perspective, but there is still a 35% overvaluation. As two out of three valuation approaches indicate substantial downside potential, I can conclude that ALB is still notably overvalued.

TrendSpider

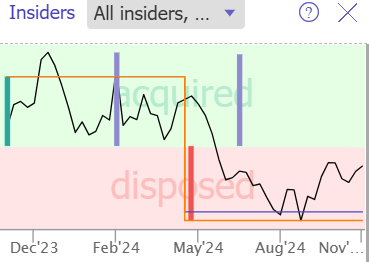

Insiders also might believe that the stock still has room to tank as the last time insiders bought the stock was 52 weeks ago. On the other hand, it is also fair to mention that there was no aggressive insider selling either.

Risks to my bearish thesis

Despite saying that my initial bearish thesis aged well, and the stock is now cheaper than it was on January 30, there were moments when my initial thesis did not look that good. The share price was around $121 when I shared my previous call, but it rallied to above $142 by the end of February. Therefore, there might be rallies during some periods which will make my bearish thesis look bad.

The Fed started cutting interest rates in September, and if it maintains an aggressive pace of monetary easing, this might be a big positive catalyst for EV demand. As a big driver of lithium demand, the potential spike in the production of new EVs might spur lithium prices, which will be beneficial for ALB.

The company recently announced that it is transforming its operating structure to increase agility and deliver significant cost savings. During the earnings call the management might indicate their expectations around cost savings amounts, and this might spur investors' optimism even if Q3 performance will not be impressive. Significant cost reductions might positively affect the EPS outlook for the foreseeable future, which might increase interest in the stock among investors.

Bottom line

To conclude, ALB remains a "Sell" in my opinion. Despite solid growth potential over the coming decades, the foreseeable future looks cloudy. The oversupply is a big problem that can keep lithium prices low for the next few years. Moreover, the stock looks significantly overvalued based both on the DCF and DDM.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.