Celestica: The Unsung AI Champion

- Celestica's stock has surged 50% in three months, driven by AI and data center tailwinds.

- Recent earnings report showed over 20% YoY revenue growth for three consecutive quarters, with record adjusted EPS of $1.04.

- The company's CCS segment, benefiting from data center investments, saw 42% YoY revenue growth, enhancing profitability and free cash flow.

- Despite a 191% stock rally in the past year, Celestica's valuation remains attractive, with a DCF model indicating a 141% upside potential.

JHVEPhoto

Investment thesis

My previous bullish thesis about Celestica's stock (NYSE:CLS) aged extremely well as the stock gained 50% over the last three months. The company demonstrates exceptional ability to absorb strong AI and data center tailwinds, which makes me remain bullish.

Trends in financial performance are positive, and the management looks confident regarding the company's ability to continue successfully riding the AI growth wave. Despite a massive rally since mid-August, the stock's valuation is still very attractive. All in all, I reiterate my "Strong Buy" rating for CLS.

Recent developments

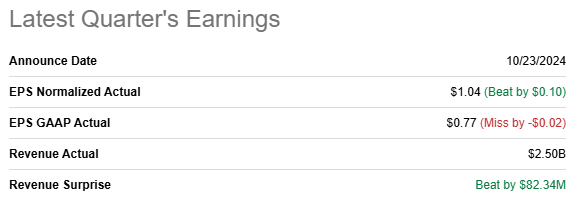

Celestica released its latest quarterly earnings on October 23, delivering positive revenue and adjusted EPS surprises. The YoY revenue growth was above 20% for the third consecutive quarter, indicating strong momentum. The adjusted EPS achieved record level of $1.04, which is significantly higher compared to $0.65 demonstrated during the same quarter last year.

Seeking Alpha

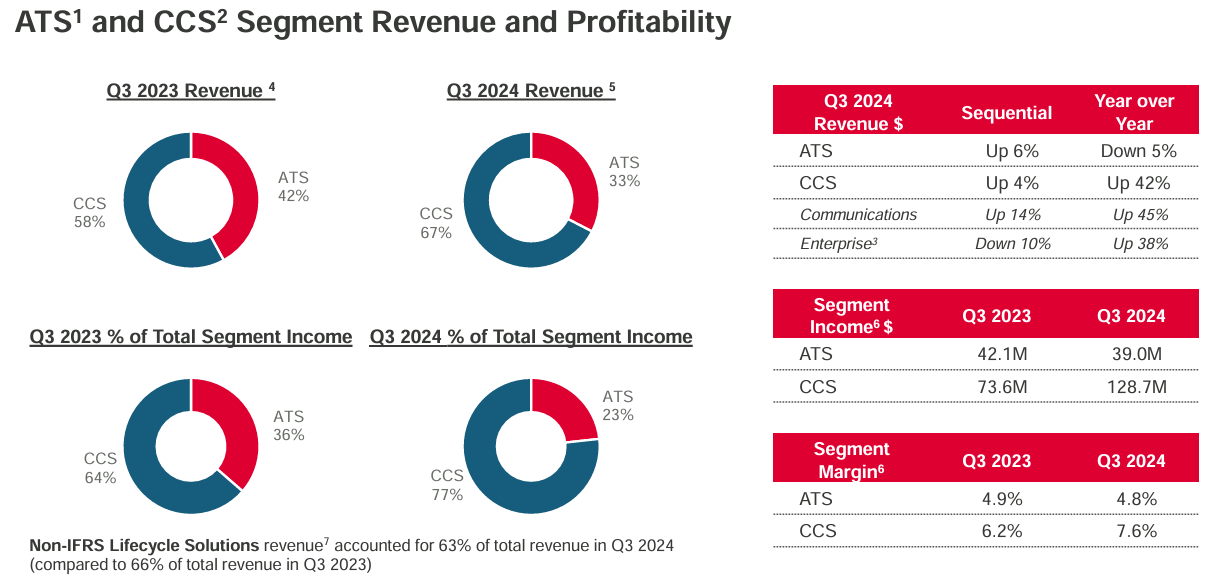

The company's revenue mix continues its aggressive shift towards the more technologically advanced Connectivity & Cloud Segment [CCS]. The segment capitalizes on aggressive data center spending from technological giants, and its revenue was up 42% on a YoY basis. Aggressive revenue growth in the CCS segment outweighed a 5% revenue decrease in Advanced Technology Segment [ATS].

Celestica's Q3 earnings presentation

Revenue shifting between the two segments positively affects the bottom line because CCS is a notably more profitable segment with a 7.6% segment margin compared to 4.68% generated by ATS. I also want to emphasize that the CCS segment demonstrates the economies of scale effect as its segment margin was 6.2% in Q3 2023. Such a trend indicates that investors can expect further margin expansion if the top line continues delivering growth.

Celestica's Q3 earnings presentation

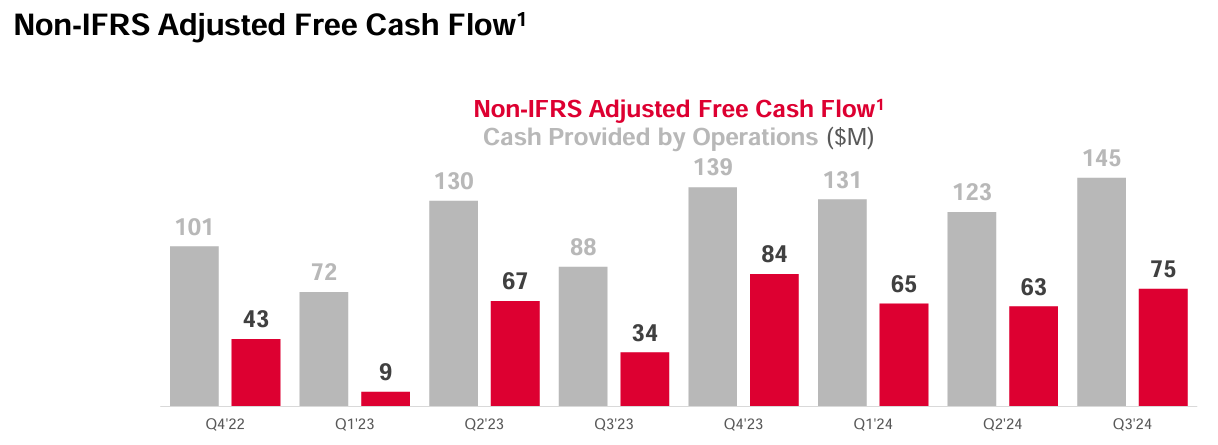

For me as a long-term investor the company's ability to convert growth into increased free cash flow is crucial. It is vital because even secular tailwinds will cool down over time and a successful company needs to ensure that it accumulated enough resources during the "super-cycle" to reinvest in new growth drivers. Therefore, the fact that Celestica's operating and free cash flow has significantly improved in Q3 on a YoY basis, is another big positive sign.

Celestica's Q3 earnings presentation

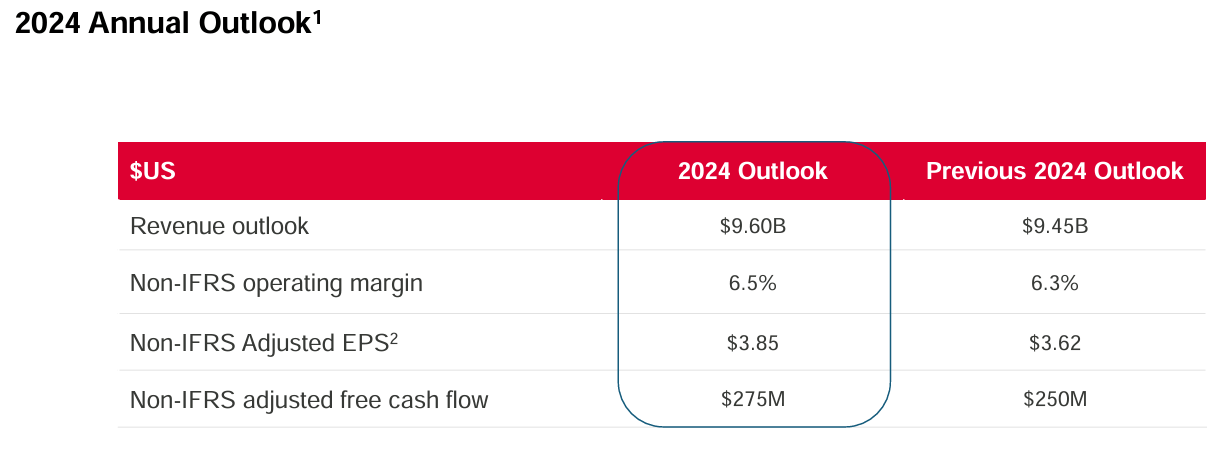

The management considers that industry tailwinds are poised to remain strong through the end of 2024. As a result, they released a more optimistic 2024 annual outlook with more optimistic forecasts across the board.

I think that the guidance upgrade is fair because there are no signs of the AI and data center mania cooling down. I already got used to tech giants announcing their multi-billion data center investments across the world almost every week. The recent trend is that new data center investors from various domains are appearing. Asset management firms are apparently very rich investors, and some of the prominent names in the industry are quite aggressive. KKR (KKR) recently entered into a $50 billion strategic partnership to boost artificial intelligence technology. According to Blackstone (BX), it has over $70 billion worth of data center assets, with another $100 billion in the pipeline. BlackRock (BLK), the world's, by far, largest asset manager, is also in the race.

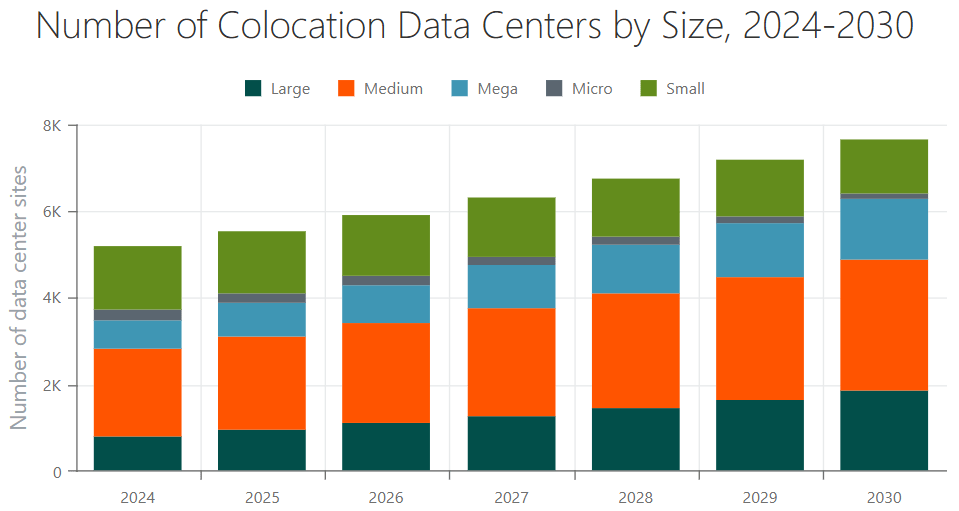

ABI Research

According to ABI Research, the number of data centers is expected to grow from around 5.7 thousand to almost 8 thousand between 2024 and 2030. The expected growth pace is quite aggressive, and this is a big tailwind for CLS.

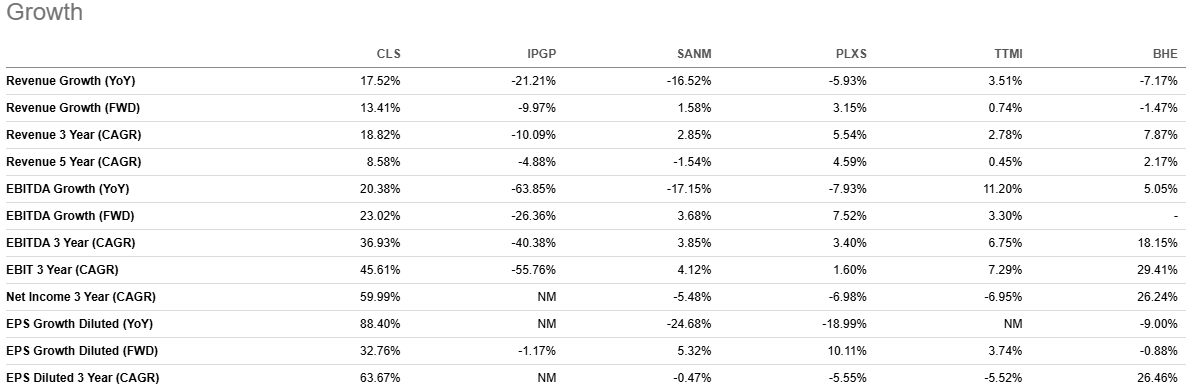

In the early paragraphs of the analysis, I have emphasized that trends in Celestica's financial performance suggest that the company is efficient in absorbing the positive effect of AI and data center tailwinds. I also want to emphasize Celestica's strength in capitalizing on positive industry trends by looking at the growth demonstrated by competitors. Celestica represents the Electronic Manufacturing Services [EMS] industry. According to the peer comparison provided by Seeking Alpha, we can easily compare all Celestica's key metrics to competitors'. As we can see, none of the company's peers demonstrate comparable growth across key financial metrics.

Seeking Alpha

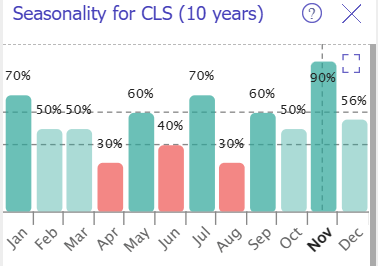

Seasonality trends also look quite positive for the stock. According to the below bar chart, November is historically the most successful month for CLS investors. December has also been mostly positive over the last decade.

TrendSpider

To conclude, the set of positive catalysts looks robust, which includes both strong industry tailwinds and company-specific strengths.

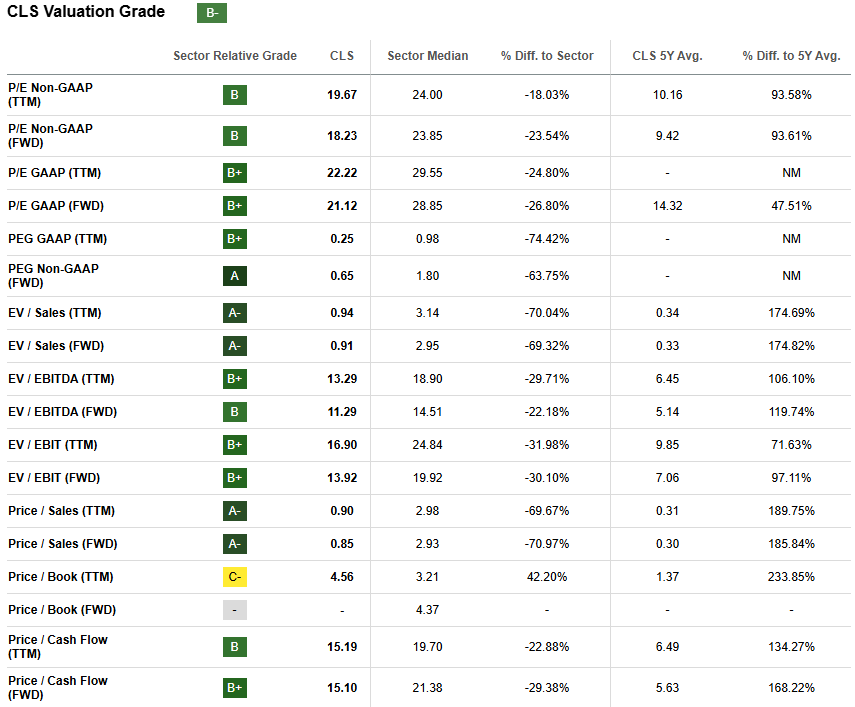

Valuation update

CLS soared by 191% over the last 12 months, way ahead of the broader U.S. stock market. The YTD performance is also unparalleled, with a 147% rally. Despite the share price skyrocketing over the last year, Celestica's multiples are still reasonable and most of them are significantly lower compared to the sector median.

Seeking Alpha

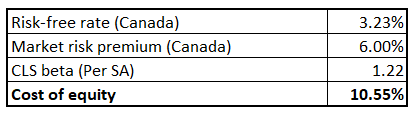

The discounted cash flow [DCF] approach is always a useful tool when we speak about companies experiencing strong revenue and profitability growth momentum. I use cost of equity as a discount rate, which is calculated below under the CAPM approach. I do not use WACC because Celestica's reliance on debt is quite insignificant. All variables for the CAPM formula are easily available on the Internet and Celestica's cost of equity is 10.55%.

Author's calculations

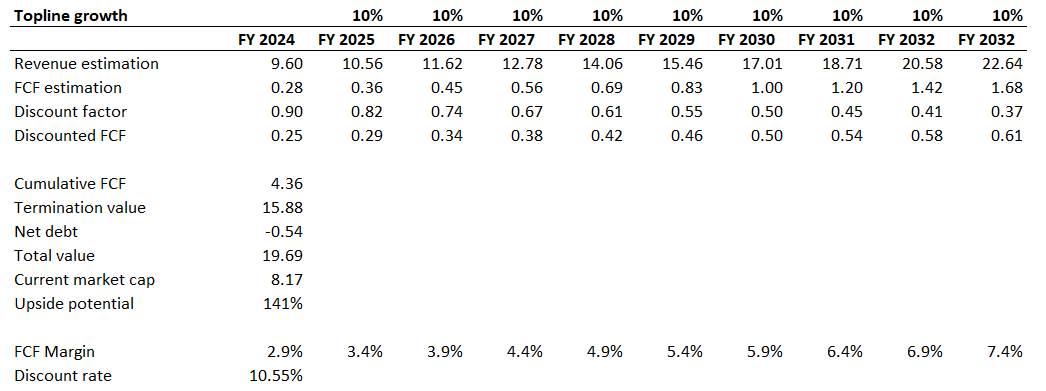

The base year $9.6 billion revenue assumption is the management's fresh FY 2024 revenue guidance presented above. For the next decade, I incorporate a 10% top-line growth rate because the EMS industry is projected to compound with a 9.7% CAGR, and we see that Celestica is quite strong in outperforming its peers. I use a 2.9% free cash flow [FCF] margin, which is also based on the management's fresh guidance. I expect a 50 basis points yearly expansion in the FCF because we see that the CCS segment is gaining momentum and there are indications that there is a solid potential to deliver economies of scale.

Author's calculations

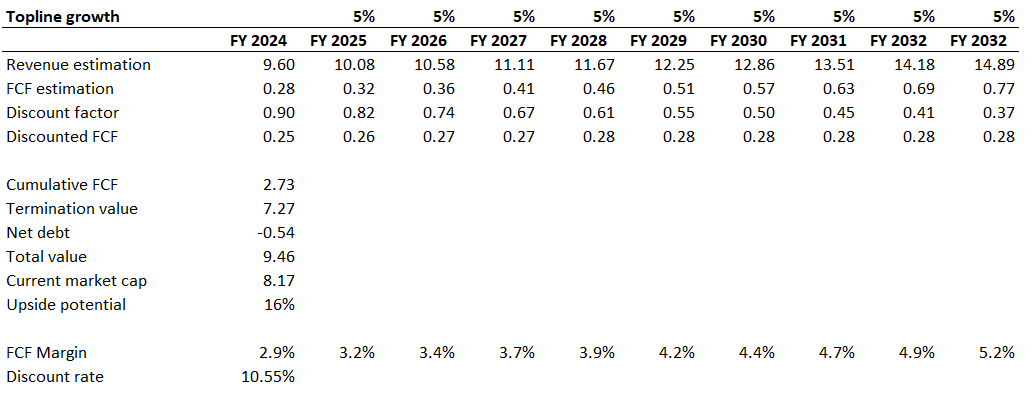

My DCF model suggests that the company's fair value is close to $20 billion, meaning that there is still a 141% upside potential. This might look unrealistic for some readers, but CLS is indeed very cheap compared to its growth potential. To understand this, in the below spreadsheet, I demonstrate that the stock is notably undervalued even when I implement a 5% revenue CAGR and 25 basis points FCF margin expansion.

Author's calculations

Risks update

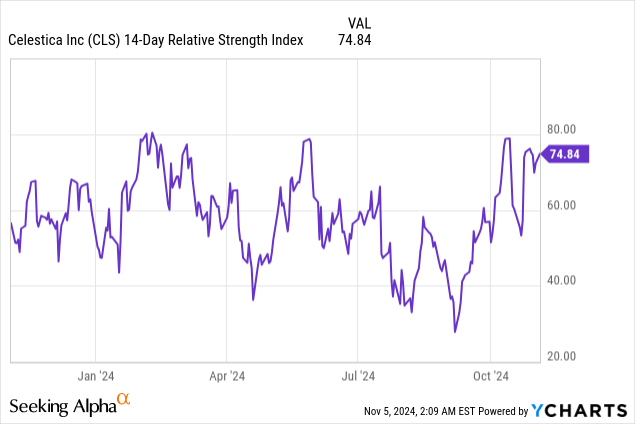

The stock's technical setup does not look quite good. The RSI indicator is close to its peak levels, meaning that there might be a temporary pullback before CLS continues its growth. Moreover, there are always substantial risks that after the share price almost tripled over the last twelve months, investors might start taking profits which will lead to a sell-off.

Data by YCharts

Data by YCharts

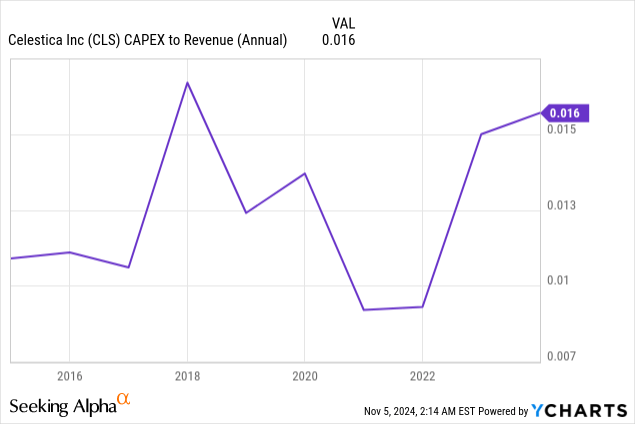

Celestica's proportion of revenue reinvested in CAPEX looks quite low, which means that entry barriers for potential new competitors are not that high. Therefore, even though we see that CLS confidently outperforms its peers, there is a risk that a new strong player might appear in the industry.

Data by YCharts

Data by YCharts

Bottom line

To conclude, CLS is still a "Strong Buy". The company is very strong in absorbing favorable industry trends, which we see both comparing to the company's historical performance and to peers' performance. There are multiple indications that AI and data center tailwinds are not cooling down.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.