3 Reasons To Bet On Flutter's 'License To Print Money'

- FLUT's strong revenue growth, driven by FanDuel and expanding markets, positions it for continued top-line expansion, potentially reaching $20 billion by FY 2028.

- Operational improvements and margin expansion are expected to boost profitability, with operating margins projected to grow significantly, enhancing shareholder returns.

- Despite FLUT's breakeven status over the last twelve months, the company's future growth potential makes it an attractive investment.

- We rate FLUT a 'Strong Buy'.

Michael Blann/DigitalVision via Getty Images

In the world of business, a Gambling License is often referred to as a 'license to print money'.

While the exact origin of the term remains unknown, the idea behind this saying is straightforward - offering gambling products to the general public, especially when there's a built-in house edge, virtually guarantees strong, recurring revenues over time.

Tilt the tables in your favor, and gambling turns from, well, gambling, into a highly profitable business model. As they say - 'The House Always Wins'.

In this article, we wanted to examine Flutter (NYSE:FLUT), a leading gaming / sportsbook company with operations and brands all over the globe. While the company's largest and fastest growing market is the US, the company also does significant business in the UK, Australia, Italy, Ireland, and elsewhere.

As the digital gaming opportunity continues to grow domestically alongside more mature markets internationally, we thought it would be a good time to take a look at FLUT and give our thoughts on whether we think the stock is a Buy, Sell, or Hold.

Today, we'll dive into the company's financials, explore the valuation, and explain 3 key reasons we think the time is right to bet big on this global gambling behemoth.

Sound good? Let's dive in.

1) The Growth Opportunity

Let's start by taking a look at FLUT's financial results over the last few years.

While the company has only recently listed itself publicly in the United States (on NYSE), FLUT has been a public company in the UK for a long time, so we actually have a relatively robust set of financials to review.

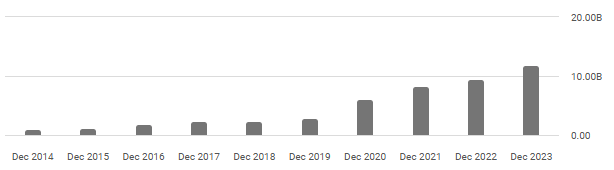

Here's a look at FLUT's revenues over the last decade:

Seeking Alpha

As you can see, sales have grown substantially, from $1.1 billion in 2014 to $12.8 billion over the last twelve months.

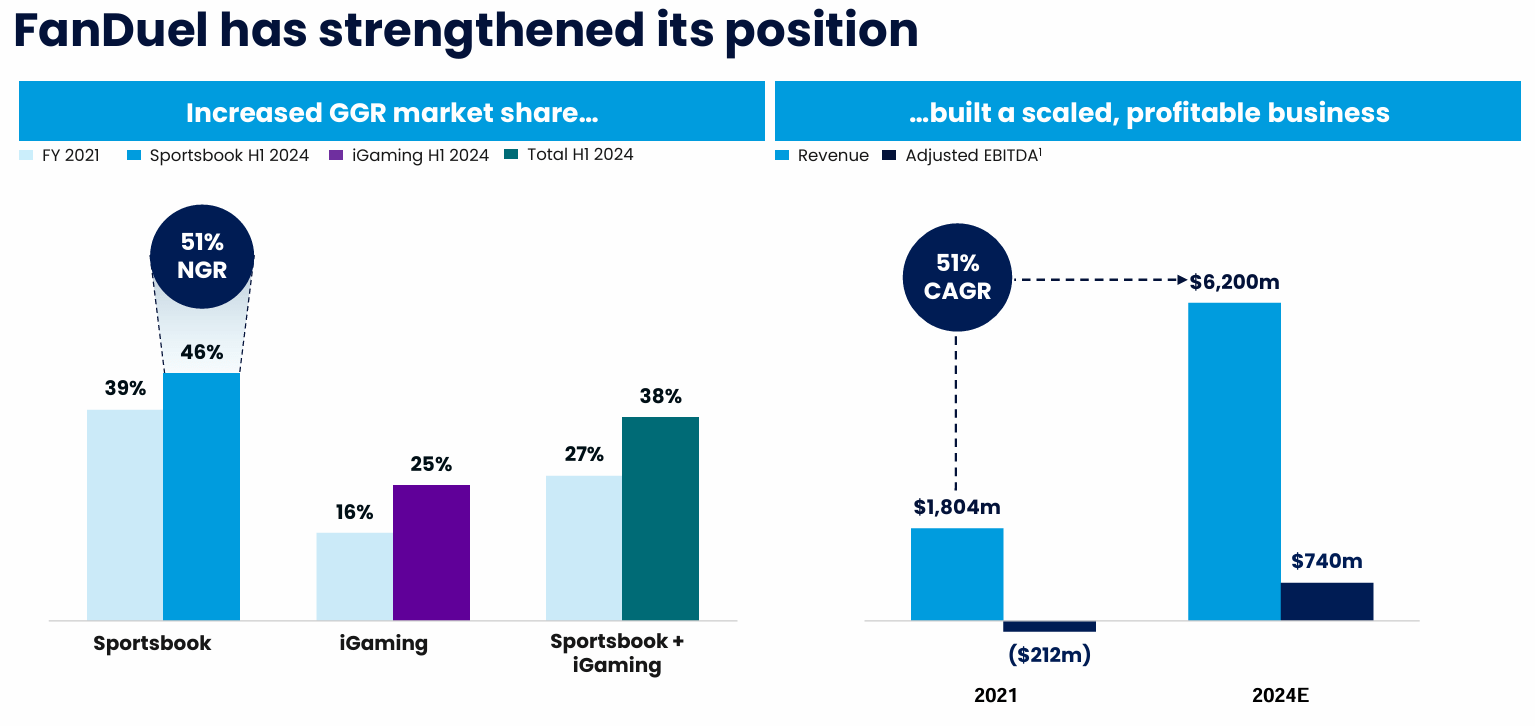

This '10x' sales expansion is due to a number of factors, but the majority of this growth is from FanDuel, the company's premiere sportsbook asset operating in the US:

IR

On the first chart, you can see how FLUT's revenue began growing rapidly between 2018 and 2020 following the US Supreme Court's 'legalization' ruling, and the pandemic, which saw unprecedented retail flows into sports betting in all jurisdictions.

Within the US, FanDuel has been able to capture a lot of this business on an ongoing basis, and growth between 2021 and 2024 has remained robust.

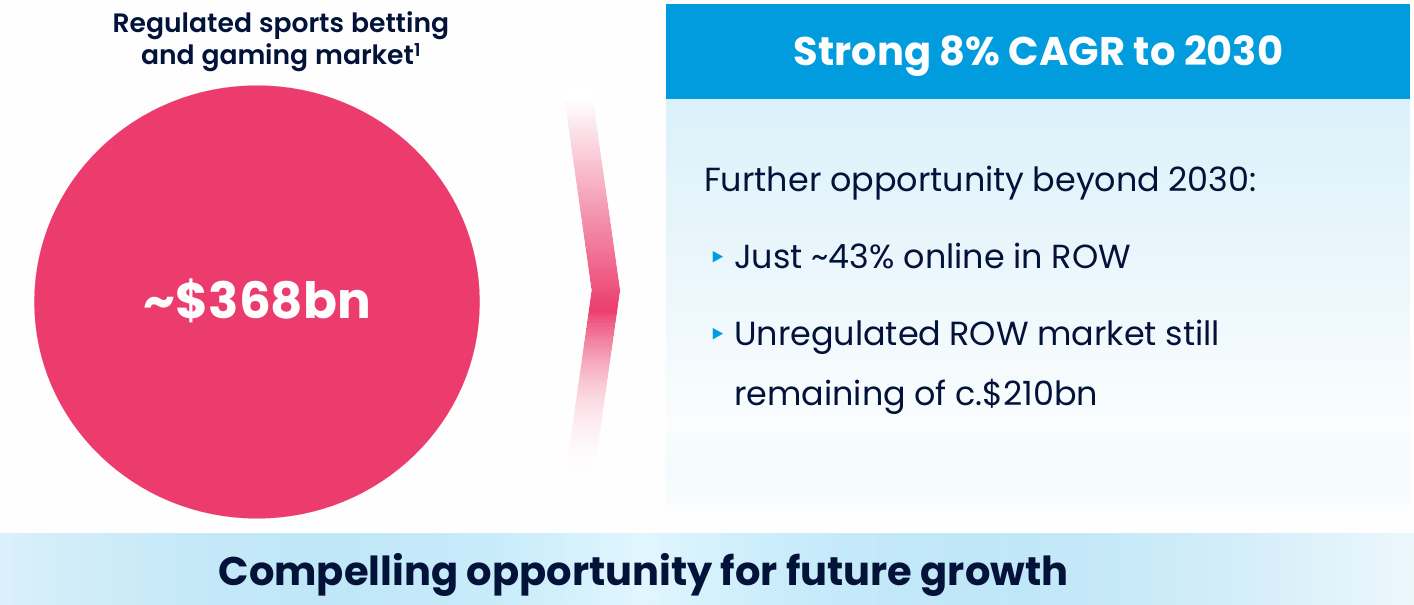

While these explosive rates of expansion are likely behind FLUT to some degree, there's still a significant amount of market to take in other developing markets, where betting is under-penetrated by digital players:

IR

Plus, there's still a long way to go in terms of building on the US opportunity.

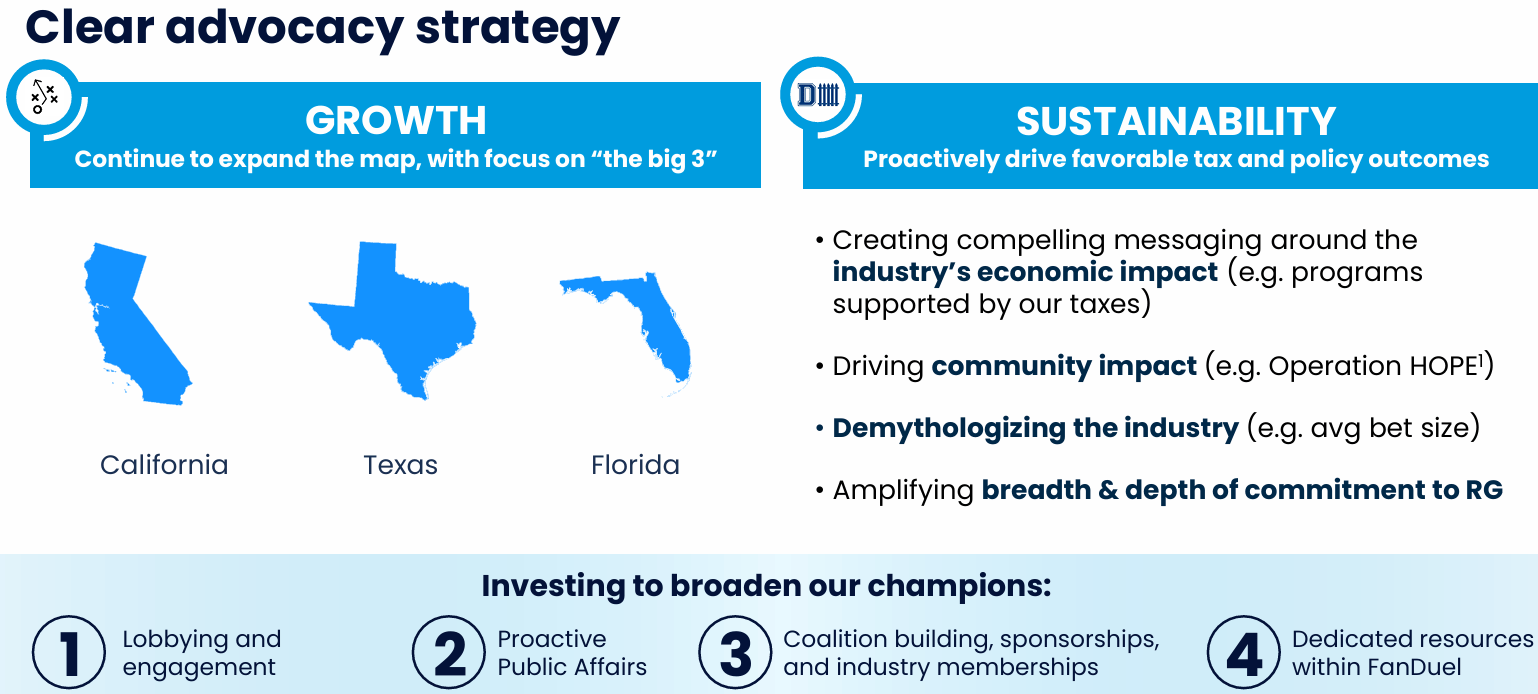

On the 'states' front, only a portion of U.S. states have currently legalized gambling, and many key regions remain untapped, like Florida, Texas, and California. The company is actively pursuing these opportunities with lobbying and other efforts:

IR

If legalized, these markets could add significant further revenue growth potential for FanDuel inside the U.S.

Additionally, on the growth front, FLUT has room for take rates to improve as competition becomes less fierce over time:

10Q

10Q

10Q

10Q

As you can see above, in the UK, Australia, and Internationally, FLUT enjoys take rates in the ~13%+ range. Over the last few months, FLUT brought in a 10% rake in the US, which means that as the domestic market matures, there's still significant room for expansion on both the net revenue margin side (30%+) and on the organic expansion side (more states and more betting in existing markets).

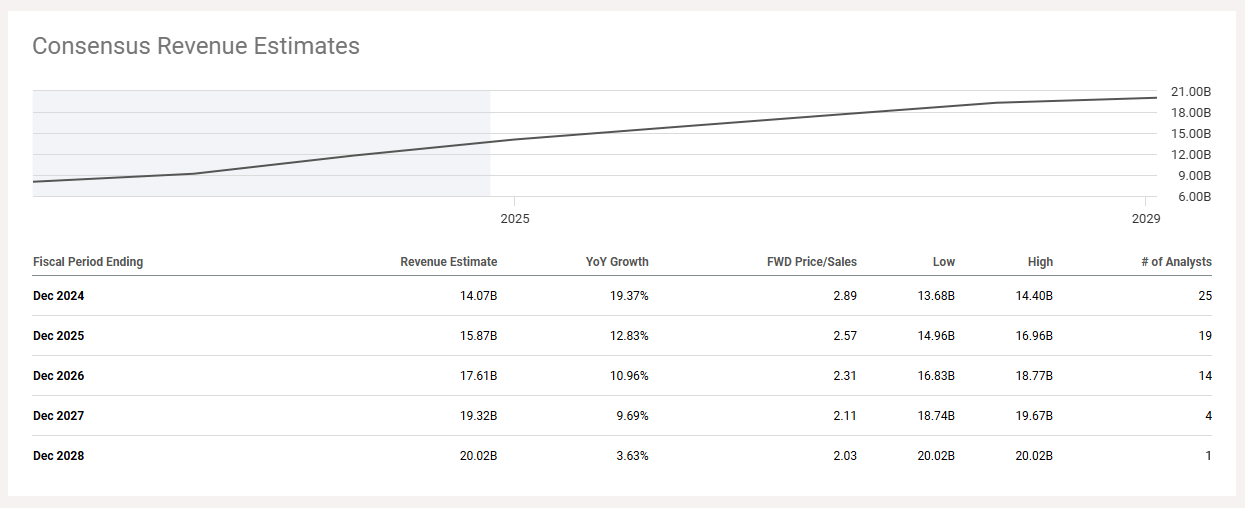

Net-net, we see FLUT's revenue growing quickly towards $20 billion over the next few years:

Seeking Alpha

Analysts are expecting this milestone to be hit by FY 2028, which seems reasonable, if perhaps a bit slow, to us.

2) Expanding Margins

While FLUT's potential top line growth is key to the durability of FLUT's business, operational improvements and margin expansion are core to the company's 'shareholder returns' story as time goes on.

While the company has 10x'd revenue, gross margins have come down dramatically and marketing costs have increased as the company has attempted to win new global share.

This effort has largely been successful, but as a consequence operating margins have suffered, and on an operating basis, if you include D&A, FLUT has been sitting at roughly breakeven since Covid.

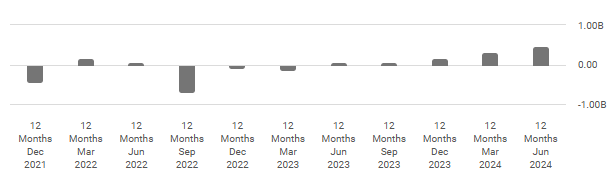

Thankfully, recently, operating margins have begun to expand, which shows how FLUT has been taking its foot off the gas in terms of user growth to instead prioritize margins:

Seeking Alpha

These operating margins haven't yet become meaningful, hovering around the low 3-5% range on a TTM basis, but we expect that the company has significant room to boost profitability looking forward due to the following factors:

- Less required promotional cost due to the company's cemented market position,

- Slower relative growth in marketing expenses (which we're already seeing), and;

- Improved operational efficiency in R&D, Tech, and SG&A.

Add these up, and against a growing top line, it appears as though FLUT has a lot of room to boost margins.

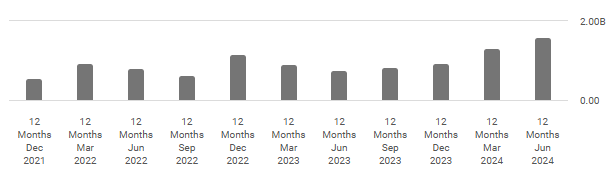

On a 'cash' basis, the company is also highly cash generative, which shows that the company has a lot of space to expand GAAP EPS over time:

Cash From Operations (Seeking Alpha)

With about $1.6 billion in cash from operations, FLUT enjoys a ~12% cash margin.

On $20 billion in '28 revenues, if operating margins can expand towards EBITDA, then we're looking at nearly $2.4 billion in GAAP net income.

This would be a huge step in the right direction and represent massive bottom-line growth for the gambling behemoth.

When it comes to FLUT's upcoming Q3 earnings report, expected next week, we expect a continuation of the current revenue growth and margin expansion trends discussed here.

We're looking for revenue growth in the 15%+ range, operating margins in the 8%+ range, and net income of more than $200 million.

In our mind, if the company can hit these targets, then we'd argue that FLUT is on the trajectory we're hoping for.

These metrics might not materialize, but we're confident in the company's execution up to this point, which makes us confident going into this earnings report.

This is doubly true given that a quarter of the NFL season's impact will likely be included in the results.

3) The Price Tag

So, to recap - we see FLUT's top-line growth continuing strongly into the future, alongside expanding margins across the income statement.

If the company can meet analyst estimates for revenue in FY '28, then $2.4 billion in GAAP net income seems probable, if not highly achievable.

Given that the company currently trades for roughly $40 billion, that puts the firm's valuation at around 16.5x '28 P/E.

We're not fans of valuing a company like this - so far out into the future - but it shows what kind of a value you get in a stock like this, just for holding.

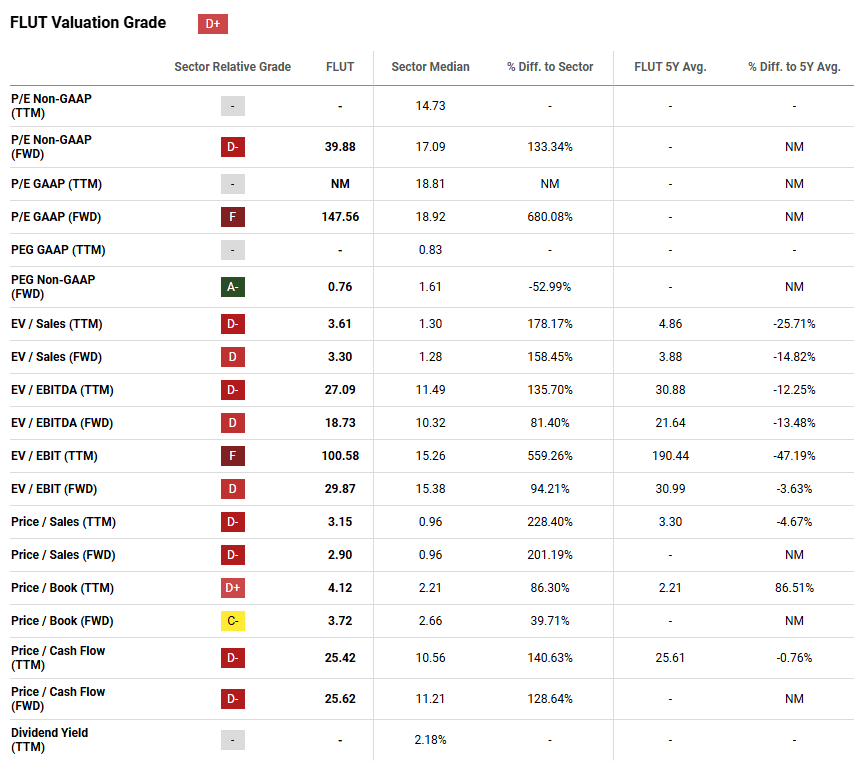

Viewed differently, Seeking Alpha's quant rating system gives the stock a 'D+', which is probably somewhat deserved:

Seeking Alpha

FLUT doesn't produce much in the way of earnings at present, has no dividend to speak of, and has a 'lean' book that doesn't support the multiple.

However, once you factor in FLUT's potential growth, then all of a sudden, the stock looks a lot more attractive. On the FWD PEG, FLUT scores an 'A-' from SA, which more accurately encapsulates our feelings on the valuation.

As the multiple expands and sales continue to grow, we're fans of buying this digital gambling behemoth on somewhere between 30x FY '25 and 16x FY '28 earnings.

Risks

That said, there are some risks when it comes to investing in FLUT:

Regulatory Issues & Taxes: FLUT operates in a tightly regulated industry, and any new taxes or rules—like recent UK tax chatter—could materially impact profitability.

Plus, some of our thesis is wrapped up in continued U.S. expansion, and if this doesn't materialize, then FLUT's multiple could come under pressure.

Market Competition: FLUT operates in a competitive environment, with competition from companies like DraftKings (DKNG), MGM (MGM) and Caesars Entertainment (CZR) domestically, and tens, if not hundreds of competitors internationally.

Intensified competition could lead to increased marketing expenditures and pressure on take rates, which would affect growth and margins.

Summary

FLUT's business is highly 'engaging' (and to some degree, addictive), which means that we expect a high level of recurring revenue from one-time subscriber acquisition costs. In short, this makes for a compelling business model, and explains why people call a gambling license a 'license to print money'.

Taken together, we think FLUT presents a compelling package to investors at the current price point.

Thus, our 'Strong Buy' rating.

Stay safe out there!

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.