Powell Industries: Up 1,250% In 24 Months, But You Still Haven't Missed The Boat

- Powell Industries has experienced a 1,250% stock increase over the last 24 months due to strong demand for power distribution systems.

- POWL's financials show significant progress in sales, EPS, and margins, as the company has transformed from a breakeven outfit to a profitable mid-size firm.

- The company's valuation at 17x EV/EBITDA is reasonable, supported by energy & utility Capex, alongside a robust cash position with zero debt.

- We rate the stock a 'Strong Buy'.

real444/E+ via Getty Images

In case you've been living under a rock, Powell Industries (NASDAQ:POWL) has had one hell of a run.

Over the last few years, the small, mostly unheard-of firm has grown substantially off the back of significant demand for power distribution systems, the company's core product line.

While this may seem like a relatively 'sleepy' market, increasing investments into the U.S. grid (and energy infrastructure more broadly) have driven financial growth for POWL and huge share gains for investors.

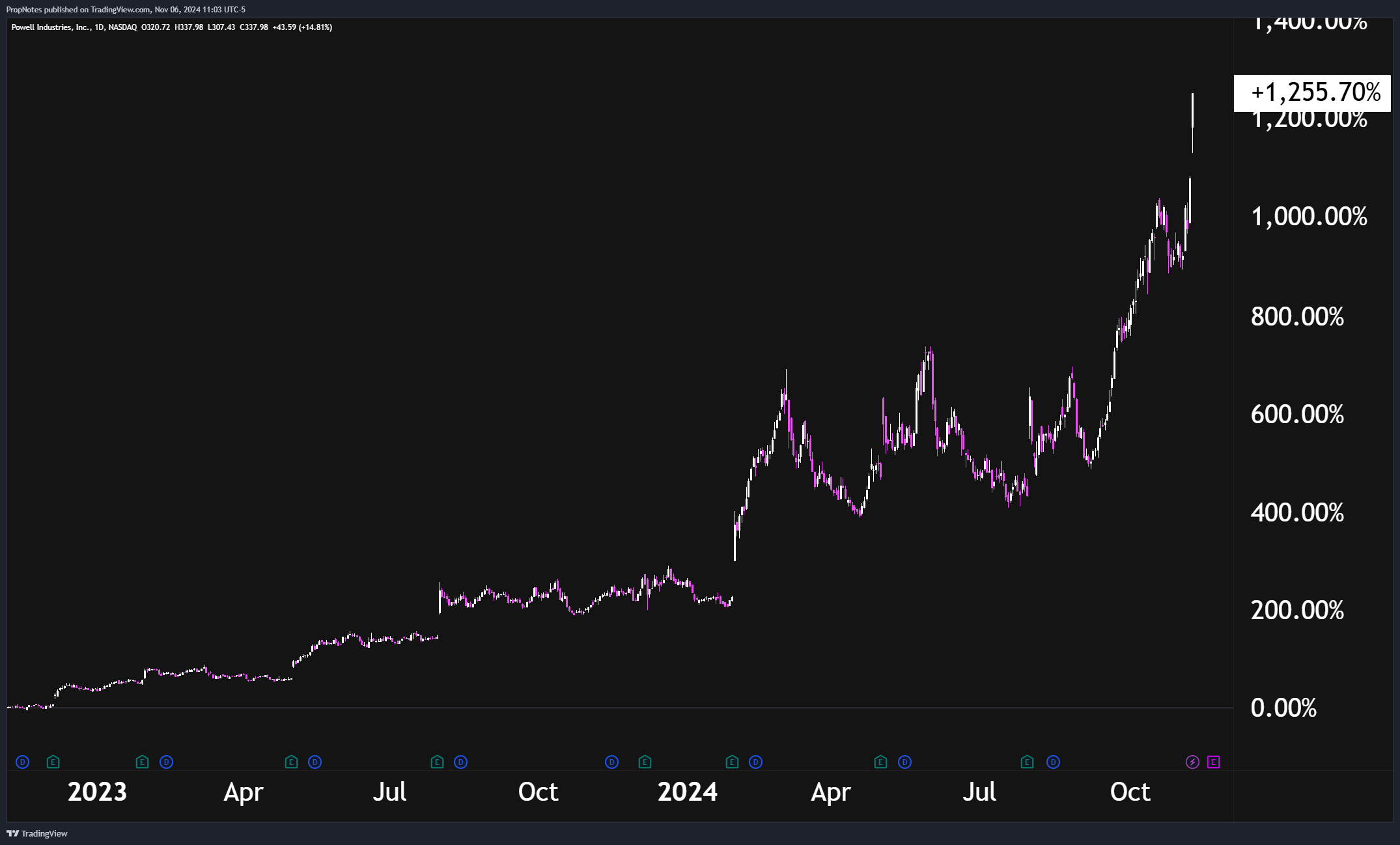

Over the last 24 months, the stock is up around 1,250%, which has absolutely dwarfed the return of the S&P 500:

TradingView

While current investors are likely happy with their position, new investors coming to the story at this point in the cycle may be wondering whether or not they 'missed the boat'.

This is a reasonable fear, given how far the stock has come in such a short span.

Here's the thing, though - with a massive order backlog, strong economic tailwinds, and a new administration coming in that has promised to 'drill baby drill' (which should materially benefit POWL for the foreseeable future), we anticipate that the company will continue to grow earnings significantly over the coming years.

Given the POWL's somewhat reasonable valuation at roughly 26x blended P/E and 3.5x blended P/S, we think the stock remains a solid long-term capital allocation for patient traders.

Today, we'll dive into POWL, explore the company, and explain why we think the stock is a reasonable 'Buy', even following the massive growth we've seen up to this point.

Sound good? Let's dive in.

POWL's Financials

As always, let's start with POWL's financials.

At its core, POWL is focused on making power distribution technology for a few different industries, but primarily the energy and utility sectors:

We develop, design, manufacture and service custom-engineered equipment and systems that distribute, control and monitor the flow of electrical energy and provide protection to motors, transformers and other electrically powered equipment.

We are headquartered in Houston, Texas, and serve the oil and gas and petrochemical markets that include onshore and offshore production, hydrogen, carbon capture, liquefied natural gas (LNG) facilities and terminals, pipelines, refineries and petrochemical plants.

Additional markets include electric utility, light rail traction power, and commercial and other industrial markets that include end markets such as data centers, mining and metals, and pulp and paper.

Most of the firm's products are custom-made, and focus on breakers, switches, grounding tools, chargers, and industrial-scale electrical management hardware:

www.powellind.com

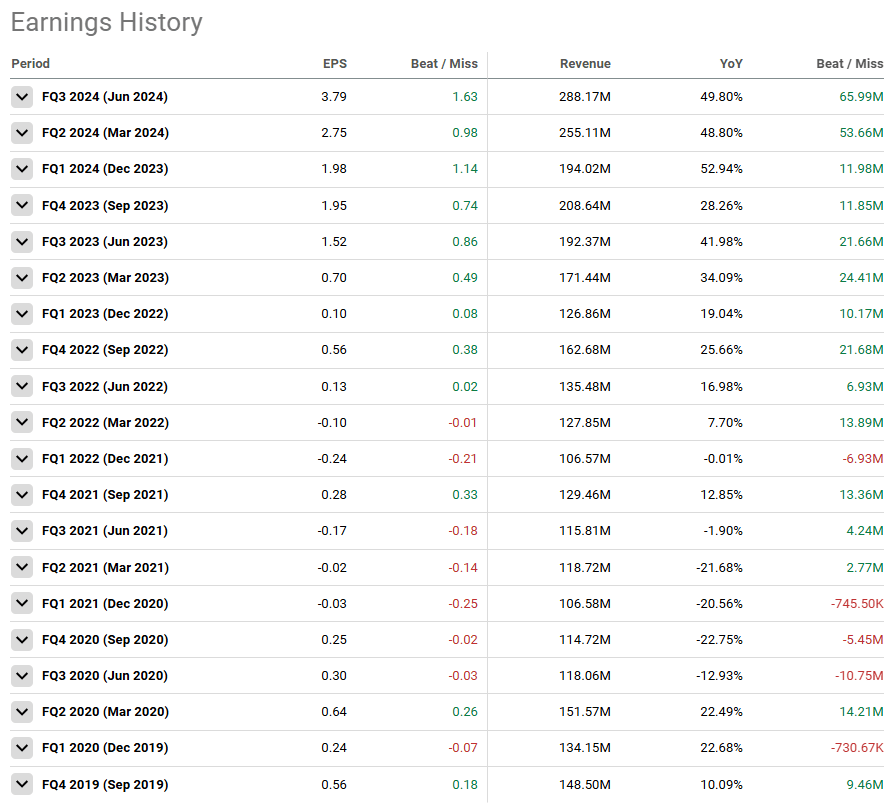

For the longest time, POWL's business has been choppy, but in recent quarters, the company has seen substantial growth. You can see below how in the years of 2019 - 2022, POWL reported mixed (and sometimes negative) EPS, alongside breakeven top-line growth figures:

Seeking Alpha

Only in recent years has POWL begun to grow top-line sales, and the company has now clocked significant YoY sales growth in the 50%~ range for the last few quarters.

EPS has also been transformed from being mixed / negative, to growing substantially & crushing analyst estimates.

Margins have also improved, with gross margins going from TTM 14% to TTM 25% over the last few years, and net margins going from TTM 0%~ to TTM 13% in that same span.

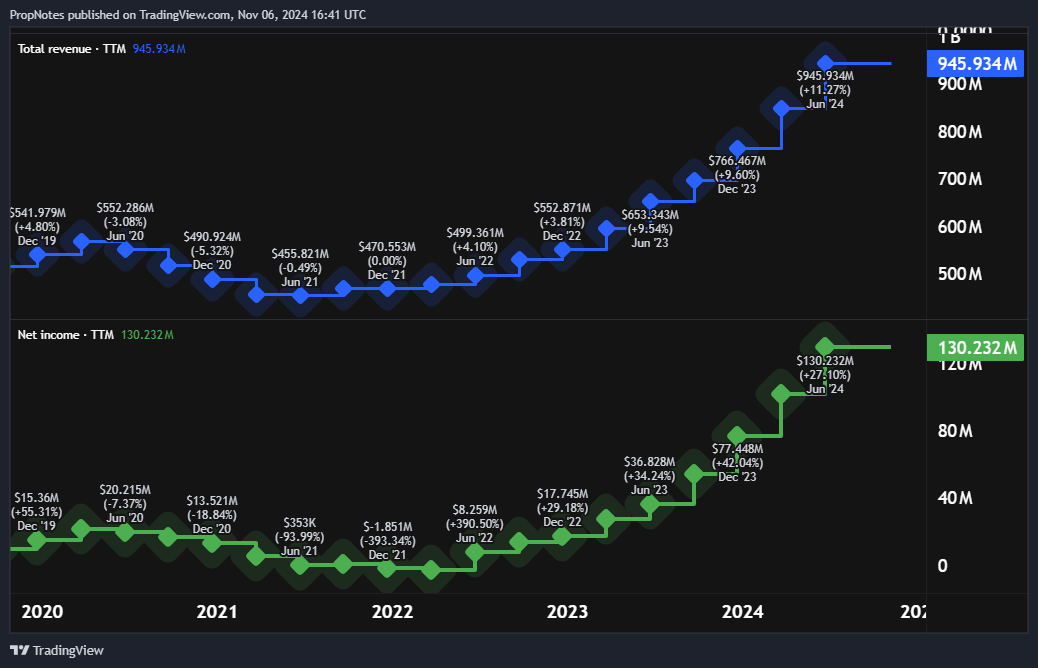

Zooming out, this is what the company's top and bottom-line results look like:

TradingView

Not bad, right?

The real unlock for shares in this case has been the company's transformation from a small, breakeven company to a mid-size firm producing substantial net income ($100 million+) on a TTM basis. Small breakeven companies are simply valued differently than profitable firms with nearly $1 billion in revenue, thus the explosive re-valuation in the share price.

Looking forward, we expect the company's performance will continue due to three main reasons: secular infrastructure trends, Trump, and the company's balance sheet.

Let's start with Trump.

In short, a large percentage of the company's focus is on the oil & gas industry, as drilling firms often need large, custom-designed electrical distribution systems to power drills, sensors, motors, and more.

In their 10Q, POWL management state that the company has a lot of exposure to oil and gas drilling activity:

Within the industrial sector, specifically oil, gas and petrochemical, the demand for our electrical distribution solutions is very cyclical and closely correlated to the level of capital expenditures of our end-user customers as well as prevailing global economic conditions.

With a Trump White House on the way in 2025, we remain bullish on POWL's prospects. Trump and allies have consistently promised to reduce regulations to incentivize more domestic American energy production, which should trickle down to much higher Capex, and thus, business for POWL. This is a huge driver, and probably why the stock is up a lot today on election news.

Aside from Trump, there are other drivers impacting POWL's financials.

On the economic side, POWL has begun diversifying somewhat away from purely servicing the energy industry, which means that the company has more exposure to the surging infrastructure build out surrounding the projected 2030 electricity supply gap.

Alongside data centers, POWL is a clear beneficiary from recent high-tech advances seen from the Mag 7 group:

Activity within our commercial and other industrial market also remains attractive, which includes activity within the data center market. As we outlined on our second quarter call, we believe the strong growth that we have seen so far in this market for Powell has a larger potential as we continue to qualify more of our products and services for the future of this important end market.

Lastly, the outlook for our utility market remains very positive, supported by our recent return of new generation work in addition to Powell's leadership and utility distribution substations. We've been very pleased with both the volume of projects coming to market as well as our win rate on the orders we have booked thus far.

Thus, POWL has exposure to supplying power distribution systems for two key economic trends that we expect will continue in coming years.

Finally, the company's balance sheet should allow POWL management to capitalize on this opportunity.

With zero long-term debt and >$350 million in cash on the balance sheet, management has done a good job investing internally for IRR, recently acquiring land to expand manufacturing capacity:

The previously announced expansion of our electrical products factory in Houston is also progressing as planned. This $11 million factory addition is expected to be completed in the middle of fiscal 2025 and coincides with our initiative to release new products in support of our future growth across the customers and markets we serve.

Most recently, in early July, we acquired nine acres of property neighboring our Houston headquarters location for a total consideration of $5.5 million. We are currently undertaking some minor remediation work to get the space prepared for productive use and we expect this additional property to contribute incremental revenue in fiscal 2025.

On top of this, a lack of interest payments & debt should lend itself well to countering the swings inherent in the company's end markets, while also providing exactly zero drag from FCF.

The company reports earnings in just under two weeks, and we're expecting another strong quarter.

We'd be very happy with $300 million in revenue, gross margins in the 27% - 30% range, and net margins above 15%. These numbers are based on a continuation of financial trends the company has produced recently.

Past that, the potential benefit from increased energy & drilling Capex shouldn't hit until early next year, which means that there's further runway for top and bottom-line results to move higher in coming quarters. This is important for the stock moving forward.

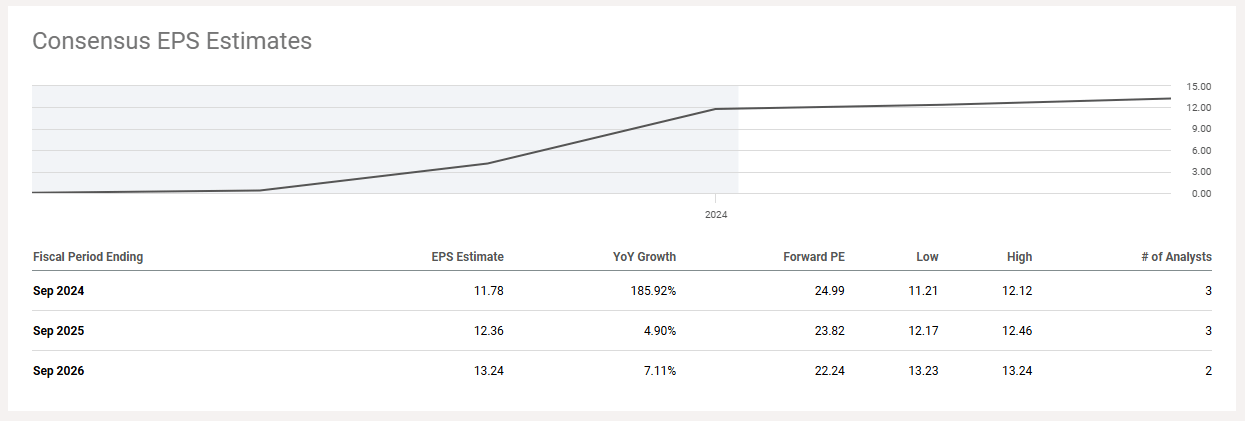

Analysts aren't as bullish, showing slowing growth in coming years despite mounting catalysts:

Seeking Alpha

Thus, we're materially more bullish on POWL's organic results than the analyst community, which is a core element of our view on the stock.

Overall, we're incredibly excited about POWL's financial results, given the strong underlying trends and competent management execution.

POWL's Valuation

The real question here is the price.

We like the company, but does an expensive valuation spoil the investment case?

In our view - no, the valuation is reasonable.

This may be hard to believe given how far the stock has come as of late, but POWL's 'core' valuation, at roughly 17x EV/EBITDA (which we're using to take into account the company's robust cash position and zero debt) appears to be entirely reasonable.

The company's expanding margins, growing revenues, EPS growth, and small float all mean that shares could be headed higher - much higher. We see a valuation ceiling for POWL in the 22x - 25x range, based on comps from other, larger companies like Eaton Corp (ETN).

This is doubly true if the company keeps growing apace and can handle the huge backlog of work coming their way.

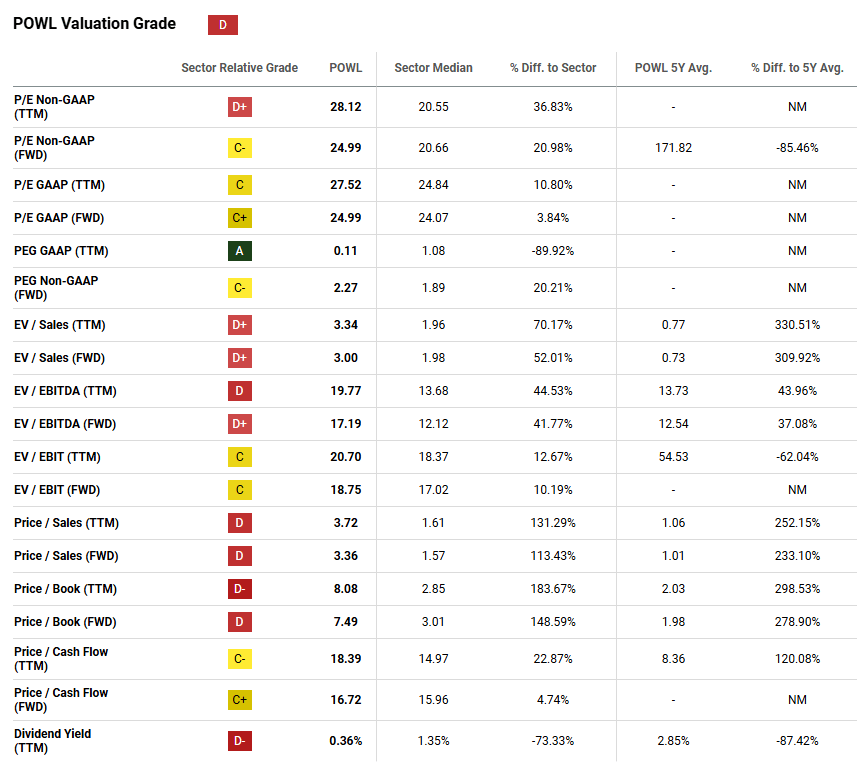

Seeking Alpha's quant system gives POWL a 'D' valuation score, which, we think, is unreasonable:

Seeking Alpha

Sure, the company's current multiple looks a bit extended on a TTM basis, but if you look at the GAAP PEG number (which takes into account POWL's growth), then you're looking at a much more reasonable number.

All in all, between POWL's business drivers, capital discipline, and valuation, this stock appears to be a highly attractive proposition for investors.

Risks

There are some risks that come with an investment into POWL.

First off, the stock is massively 'overheated' from a technical standpoint. Fundamentally, there's no reason that POWL can't move higher, but we wouldn't be surprised to see the shares dip in the next few months simply due to profit taking on the part of traders who have enjoyed gains up to this point.

The weekly RSI, a measure of momentum, is at around ~77, which is a high, 'overbought' reading.

Thus, short-term price action and a suboptimal entry could present a risk.

Additionally, the company has earnings coming up in ~12 days. As stocks run up into earnings, pressure mounts on a company to produce excellent results.

As we've laid out, we're bullish on POWL's upcoming report, but if the report suggests weakness or a slowing in the trend, then POWL's aggressive pricing could take a hit.

Summary

Overall, though, we like POWL and the underlying value proposition.

The company has a number of trends supporting strong, continued earnings, and the valuation, at 17x FWD EV/EBITDA appears highly reasonable.

While there are some risks around upcoming earnings and the potentially overheated stock, we think POWL should perform well going forward.

Thus, our 'Strong Buy' rating.

Cheers!

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.