XHB: Assessing Risks That Are Unique To The Trump Administration

- The 2024 Presidential Election outcome, with Donald Trump's re-election, led to a significant short-term boost in major stock market indices.

- Despite the market surge, the SPDR S&P Homebuilders ETF declined due to concerns over tariffs and economic policies impacting housing affordability.

- The XHB ETF offers diversified exposure to the homebuilding sector, including building products and home improvement retailers, which can mitigate sector-specific risks.

- Long-term prospects for the homebuilding market remain positive due to low existing home inventories and expected single-family permit growth, despite short-term uncertainties.

The Good Brigade

Regardless of your view of the outcome of the 2024 Presidential Election, one thing that I believe everybody will have to agree with is that the end result ended up being very bullish, at least in the near term, for the stock market and the investors with exposure to it. On November 6th, when it became clear that former President Donald Trump has been elected, for the second time, into office, major market indices shot up. The Dow Jones Industrial Average spiked the most, climbing by 3.57% for the day. The S&P 500 was the laggard with a 2.53% increase. And in the middle was the NASDAQ, rising by 2.95%.

Unfortunately, not everything and not everyone was a winner. The SPDR S&P Homebuilders ETF (NYSEARCA:XHB) actually declined by nearly 1%. This might seem odd. In general, when the market is rising rapidly, it is because there is the expectation that the economy will do better. And in a stronger economy, you would fully expect anything related to housing to do well. A stronger economy, after all, leads to stronger wages. And stronger wages and overall wealth creation should result in more demand for homes and more demand in the repair and remodeling industry. However, there is another angle to this. While it is possible that economic growth could do well, and it is possible that this would result in increased demand for housing, there are also factors that could negatively impact the homebuilding market.

Digging in

Federal Reserve

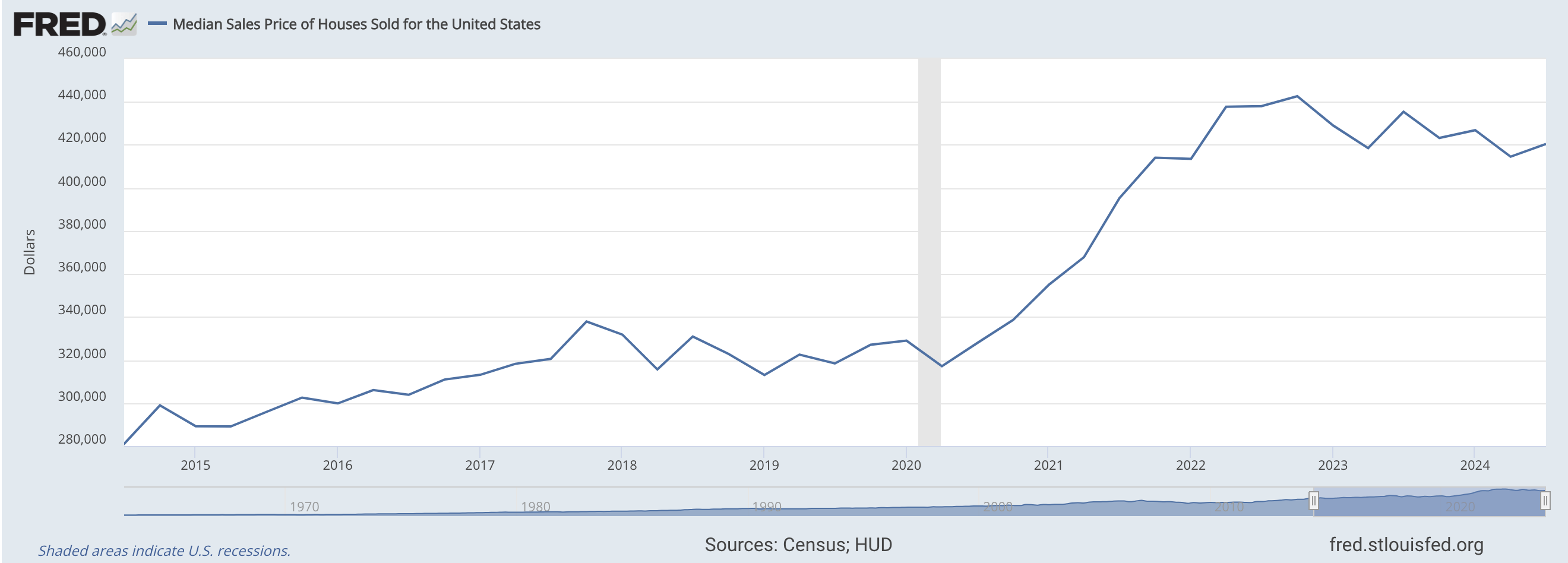

For starters, there are concerns about the economic impact associated with tariffs that President-elect Trump wants to put on other nations. Economists have estimated that this could negatively impact consumers by an average of between $2,600 and $3,000 per year. This would make it harder for many to buy homes in a market that has already priced out so many. After all, while home prices have dropped since their peaks, the average sales price of a house sold in the US in the third quarter of this year was a whopping $420,400.

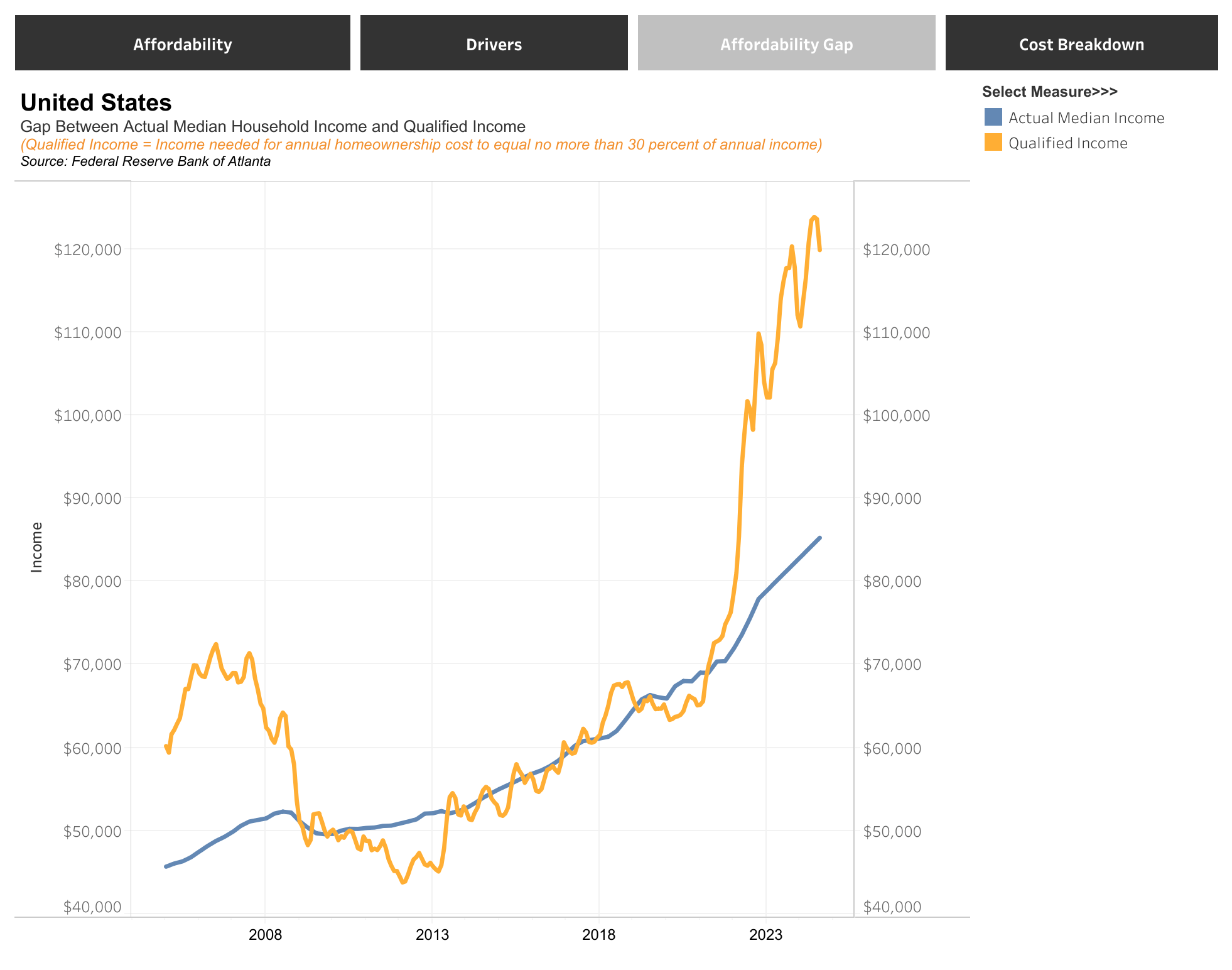

Federal Reserve

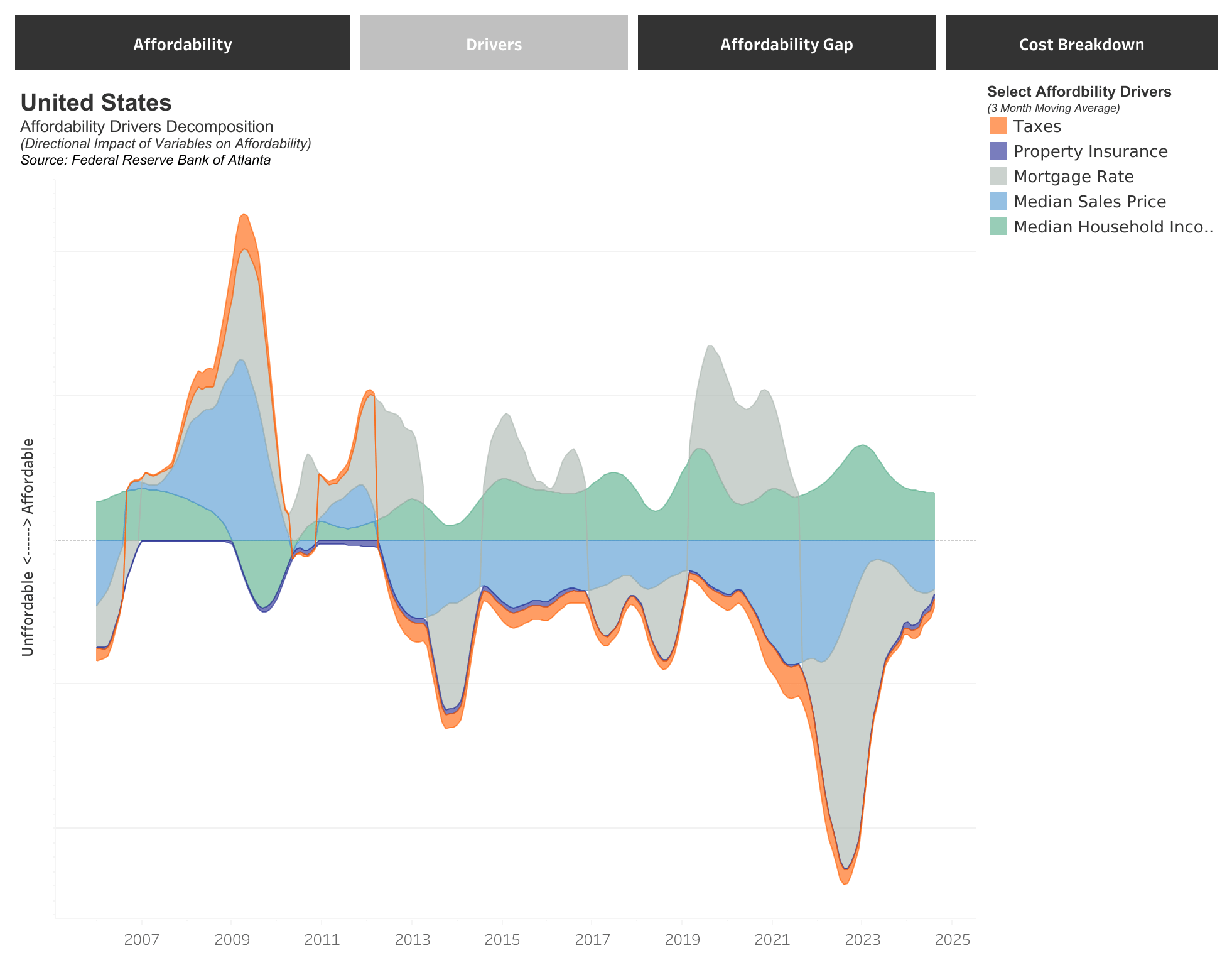

In the chart above, you can see the trend that has developed whereby homes have become increasingly unaffordable. The blue line shows the actual median household income in the US, while the yellow line shows how much income somebody would need in order to afford a home without spending more than 30% of their annual income to purchase the average home. In September of 2021, for instance, the median home was $320,667. At that time, the median household income was $70,413. And to avoid going above the 30% threshold, household income had to be $73,434. But by August of this year, the median home was $392,500. And even though annual income had increased to $85,255, the amount needed to afford the average home ballooned to $119,870. At the median income level, 42.2% of a household’s income would be allocated toward the cost of homeownership. The rise in the average home price certainly contributed to the affordability issues. But as the image below illustrates, a ton of damage has been done by rising interest rates.

Federal Reserve

Speaking of interest rates, the economic agenda of the President-elect could result in slower interest rate declines by the Federal Reserve. The fact of the matter is that policies such as tax reductions, higher tariffs, and pushing for the deportation of undocumented immigrants, could result in faster economic growth and a tighter labor market. Higher import costs associated with the tariffs would also prove problematic and would perhaps necessitate a moderation of monetary policy. It's not unthinkable that the Federal Reserve could even be forced to hike interest rates under certain circumstances.

State Street Global Advisors

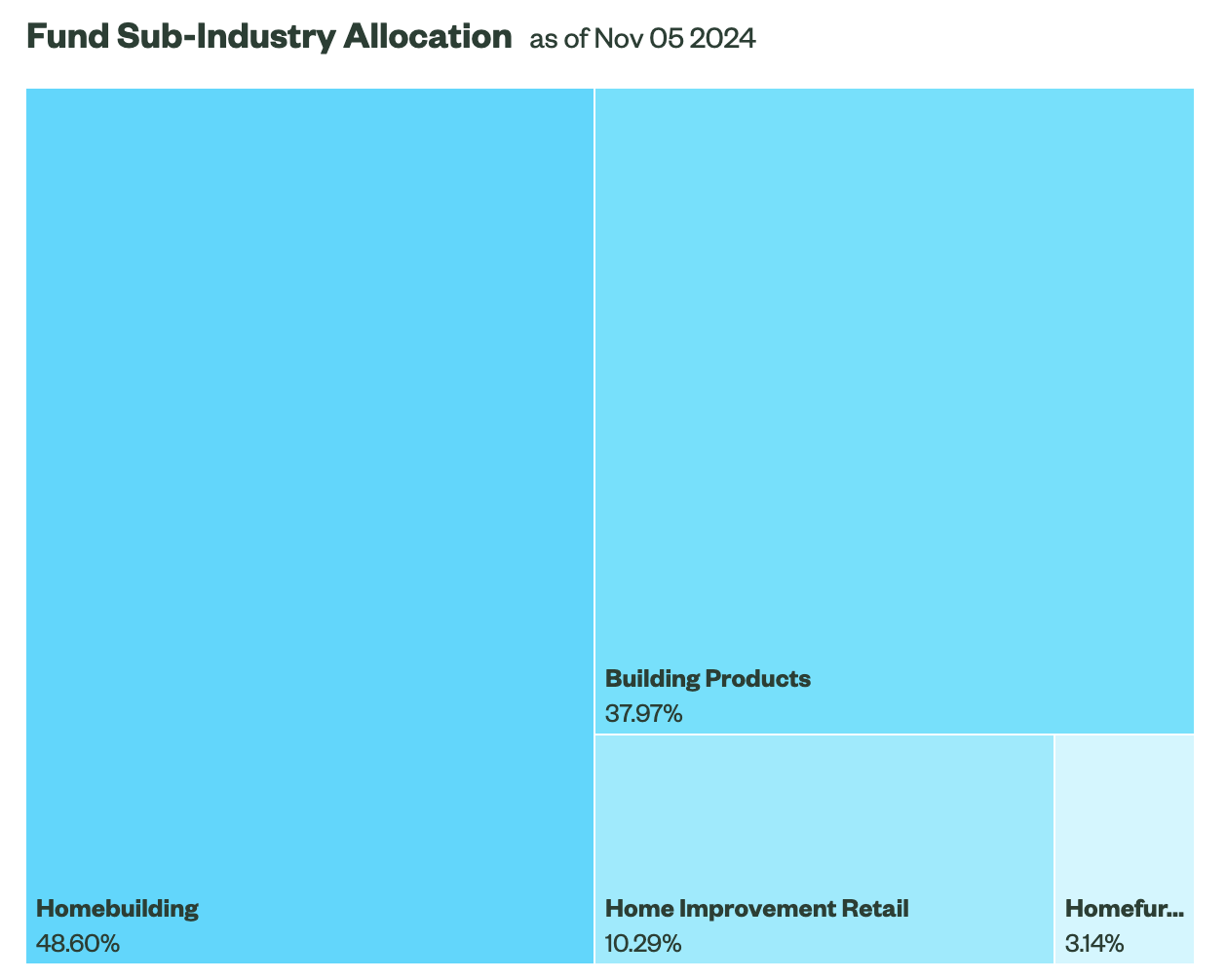

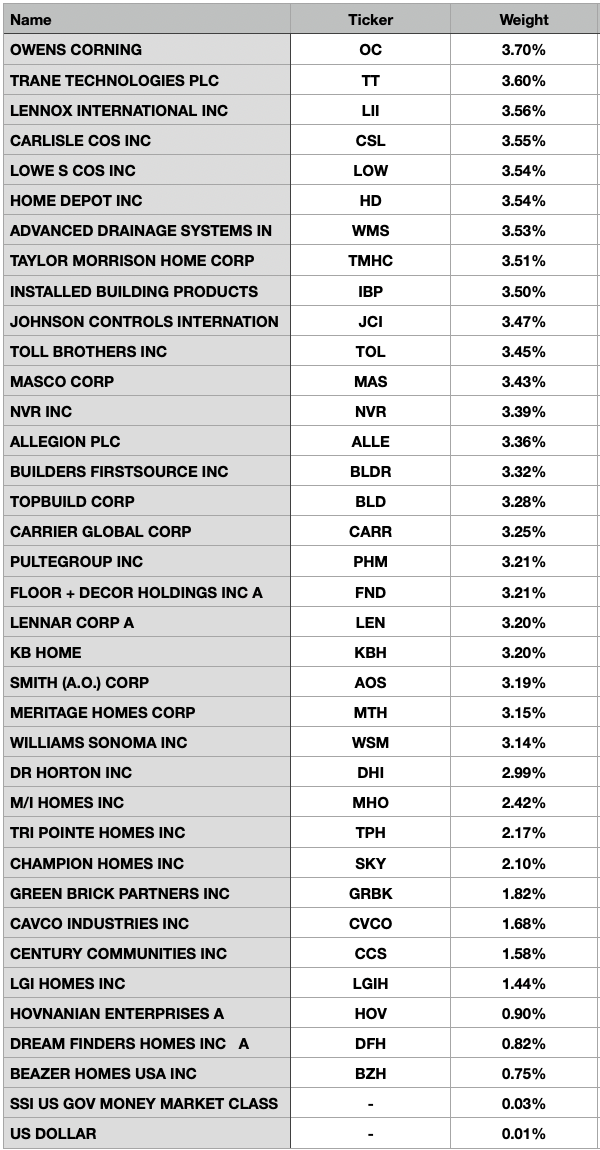

Given these issues, it wouldn't be a surprise to me to see companies in the homebuilding industry experience certain challenges. But of course, not all of the companies in the XHB ETF will face challenges equally. Even though it is called the SPDR S&P Homebuilders ETF, only 48.6% of the assets in the ETF are homebuilding companies specifically. Another 37.97% involves building products. 10.29% involves home improvement retailers. And the remaining 3.14% involves home furnishing retail. In all, there are 35 different companies within the ETF.

Author - State Street Data

Interestingly, none of the seven largest holdings in the ETF are actually homebuilders. It's the 8th largest, Taylor Morrison Homes Corporation (TMHC), at 3.51% exposure, that is the largest homebuilder. Obviously, the other players that are larger than it, do have a lot to do with the homebuilding market. For instance, the largest holding, Owens Corning (OC), has historically generated much of its revenue from producing and selling insulation, roofing, and composites for housing. Earlier this year, the company completed its purchase of Masonite International Corporation in exchange for $3.9 billion. That added the production and sale of doors and related products to its list. Tied for 5th and 6th place at 3.54% each is The Lowe’s Companies (LOW) and The Home Depot (HD). These companies do have exposure to homebuilding directly. But they are also major players when it comes to repair and remodeling work.

For investors looking for an opportunity that is dedicated solely to the homebuilding market, XHB ETF is clearly not the best candidate to consider. However, the diversity that the company offers in the space has some major benefits. For starters, it's an easy way to get exposure to 35 different businesses that should all benefit from strength in the homebuilding industry. Then again, those same businesses will likely also suffer if the market is right and there is weakness in this space moving forward. Another advantage to this diversity is that while there can be strength in some aspects of the housing market at some points in time, there can be weaknesses elsewhere.

Federal Reserve

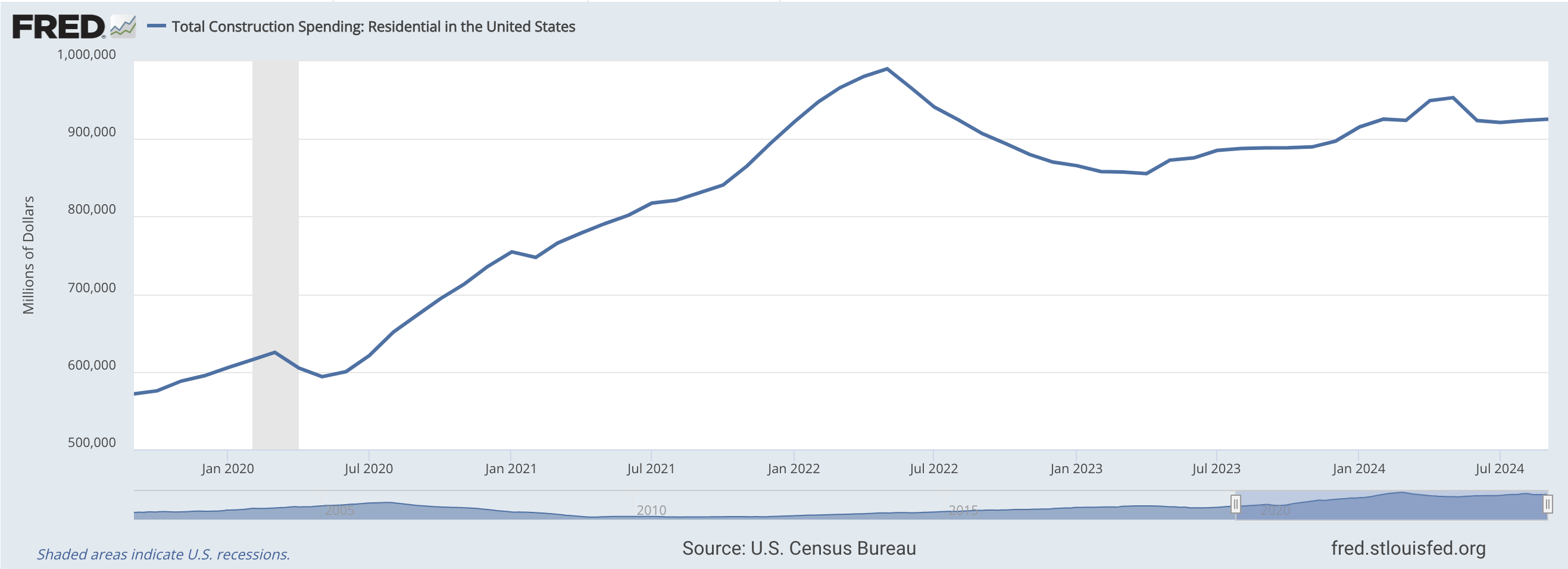

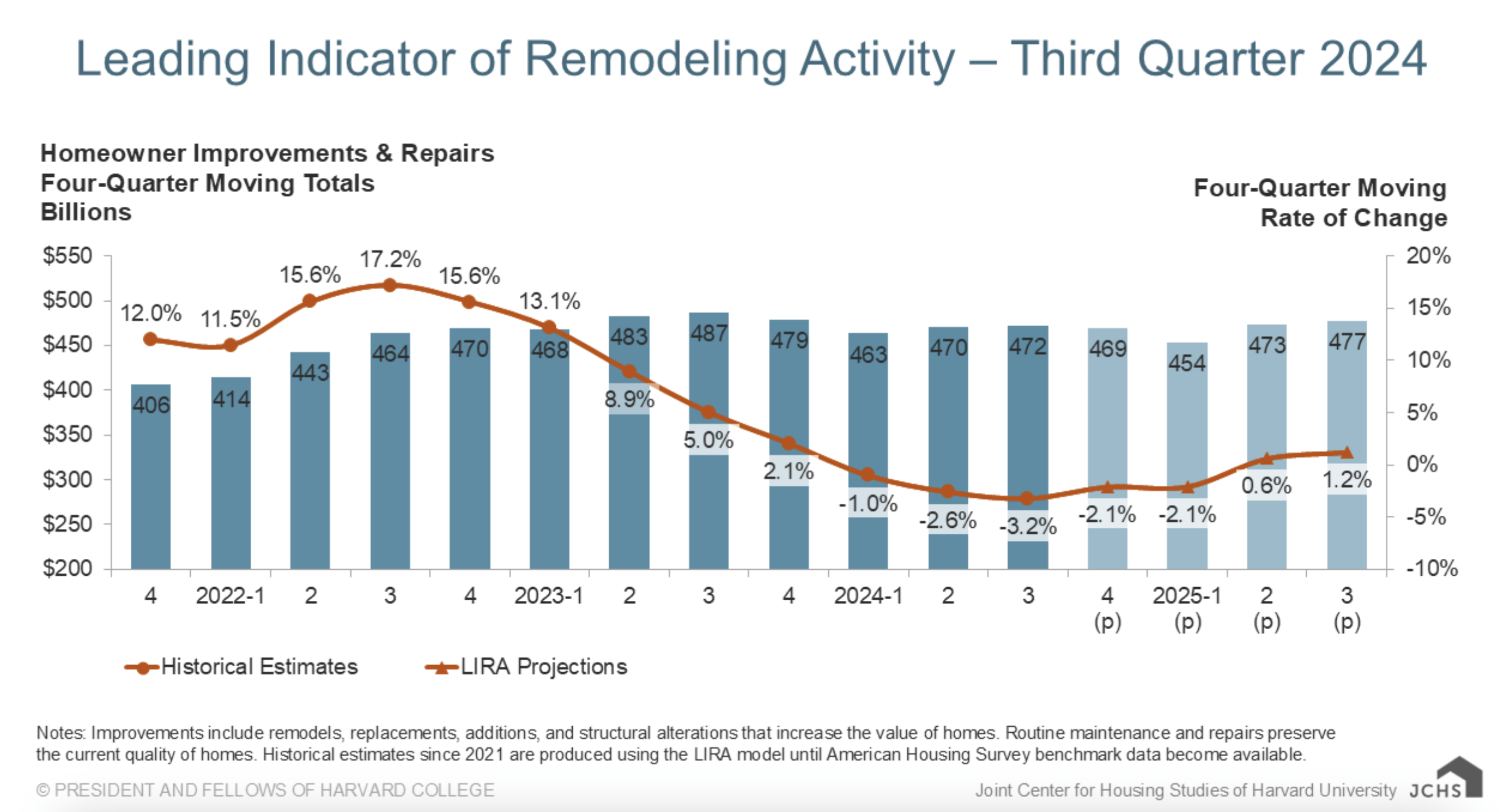

Repair and remodeling work does not always go hand in hand with residential construction spending. In the chart above, you can see the last five years of residential construction spending as provided by the Federal Reserve and the US Census Bureau. From the second quarter of 2022 until around the middle of 2023, there was a rather substantial decline in spending. But in the image below, you can see that, during this time, the four quarter moving average spending for homeowner improvements and repairs actually increased. So while one aspect of the market might be doing poorly, another might be doing well.

Harvard University

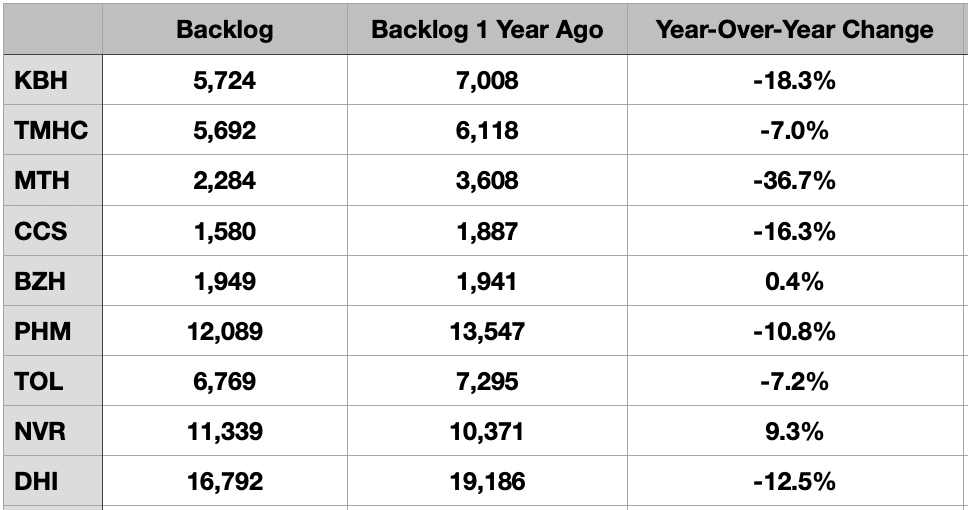

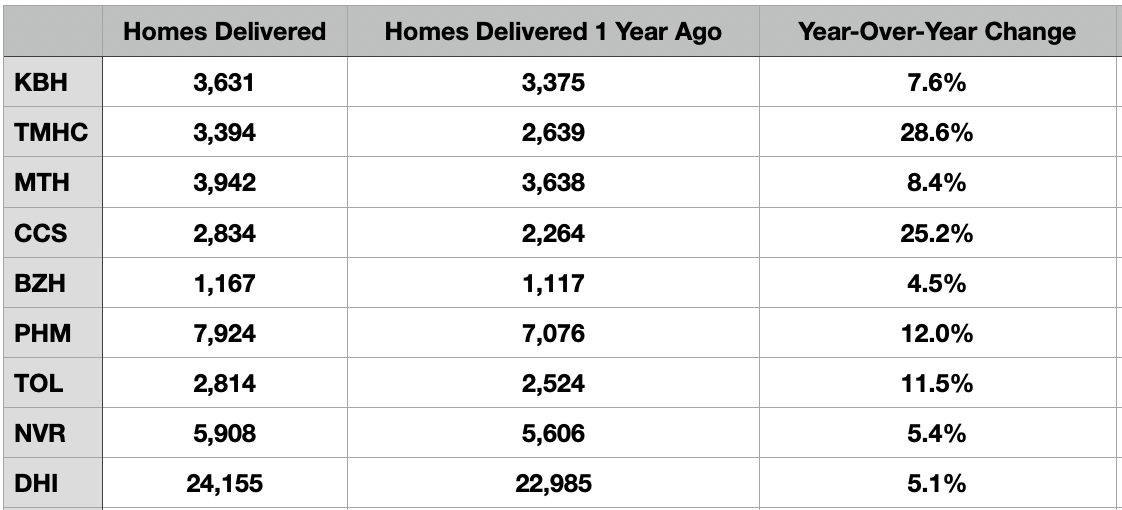

Given that the largest chunk of the XHB ETF is focused on the homebuilding industry, I decided to look at recent data involving nine publicly traded homebuilders (all of which are part of XHB). What I have seen here is something of a mixed bag for investors that are interested in the homebuilding industry. For starters, year over year, backlog for these companies is a bit low. Across the nine companies, backlog totals 64,218 homes. That's down 9.5% compared to the 70,961 homes that were in backlog the same time last year. In fact, only two of the five companies have experienced improvements in backlog during this window of time. The other seven have seen declines, with the worst one dropping 36.7% year over year.

Author - SEC EDGAR Data

This indicates that orders for these properties have been weak. But it doesn't mean that financial performance for these firms has, individually, been bad. In articles here and here, I give examples of how well some of these businesses are doing and how cheap their shares are. And a lot of that stems from an increase in the number of homes delivered.

Author - SEC EDGAR Data

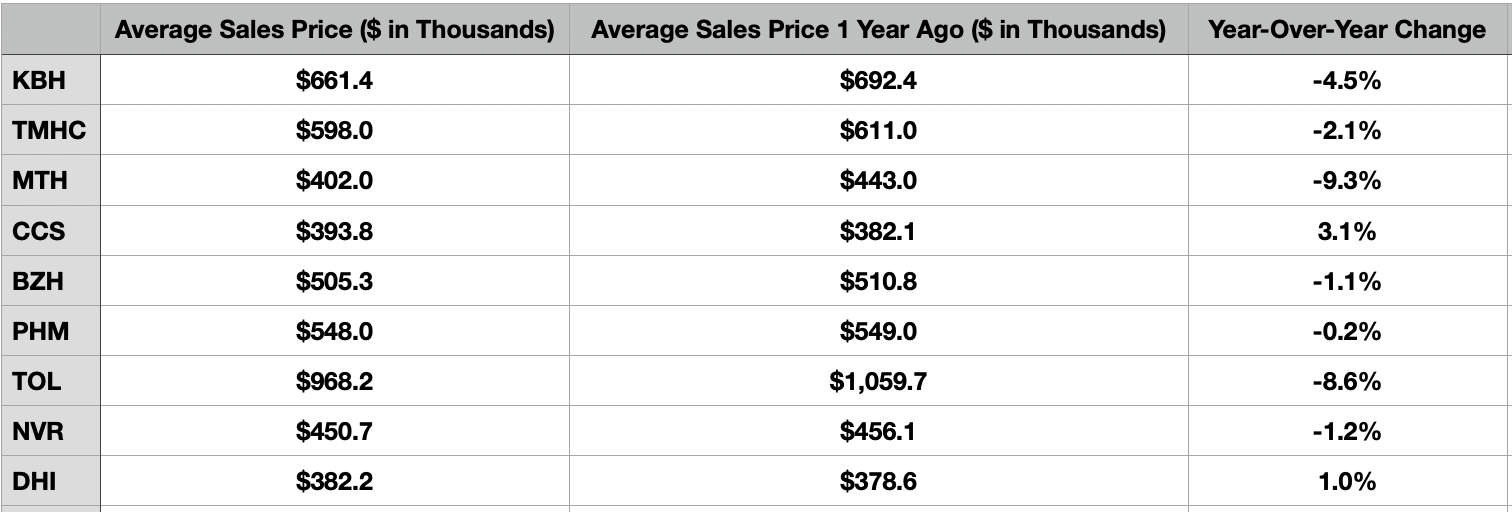

Year over year, these homebuilders increased the number of homes delivered by 8.9% from 51,224 to 55,769. This occurred because they were trying to grow their revenue and profits leading up to what they thought might be difficult times because of declining backlog. However, the average price of the homes delivered did drop during this time. Collectively between the nine companies, it dropped by 1.2% from $484,400 to $478,459. Some of the businesses actually saw an increase in the price of a home delivered. But others experienced declines as much as 9.3%.

Author - SEC EDGAR Data

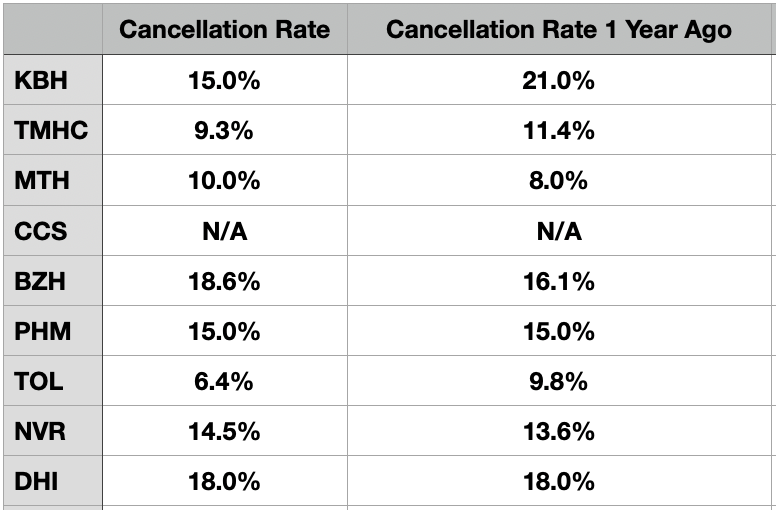

If we take a moment and step back, we can see the interesting picture that this paints. We have a declining backlog that has been exacerbated by a jump in the number of homes being delivered. But another element to this has been the cancellation rate. In the table below, you can see the cancellation rate for eight of these nine firms. One of the companies does not provide a breakdown for investors. Even though there has been weakness from a pricing perspective and a backlog perspective, both of which indicate weakening market conditions, the cancellation rate for three of the eight companies showed signs of improvement, while another remained flat year over year. This leaves another four businesses with cancellation rate increases. So this indicates something of a mixed picture.

Author - SEC EDGAR Data

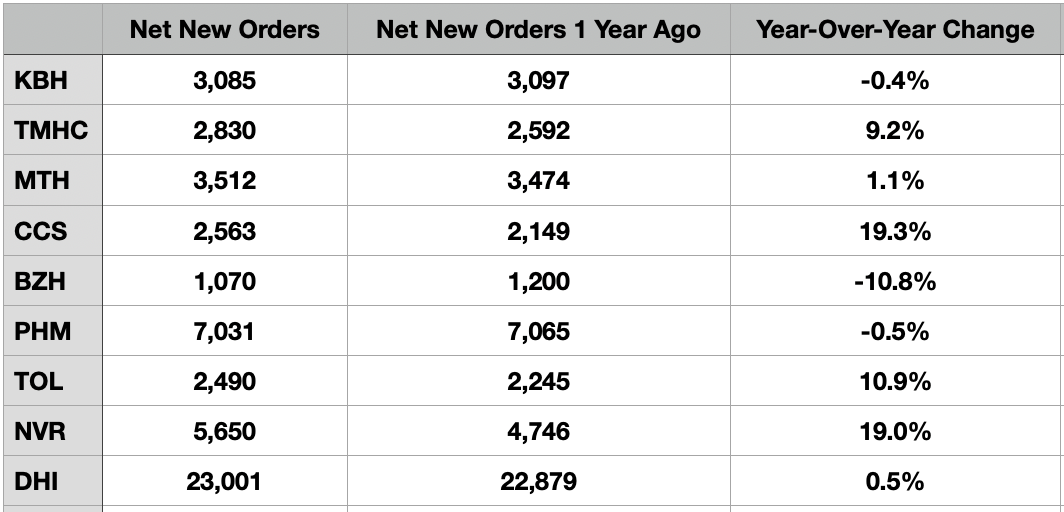

Fortunately, there has been some evidence that there is strength in the market. And this comes from new homes that are being ordered by customers. During the most recent quarter, these companies had combined net new orders, which are net of cancellations, of 51,232. This is actually 3.6% above the 49,447 homes ordered at the same time one year earlier. This is obviously not a huge increase. But it does show that the market has been experiencing a bit of a recovery on a year-over-year basis. And with other data showing that housing permits for the first nine months of this year are down 2% year over year, it looks as though this strength will be limited or might have even been short-lived.

Author - SEC EDGAR Data

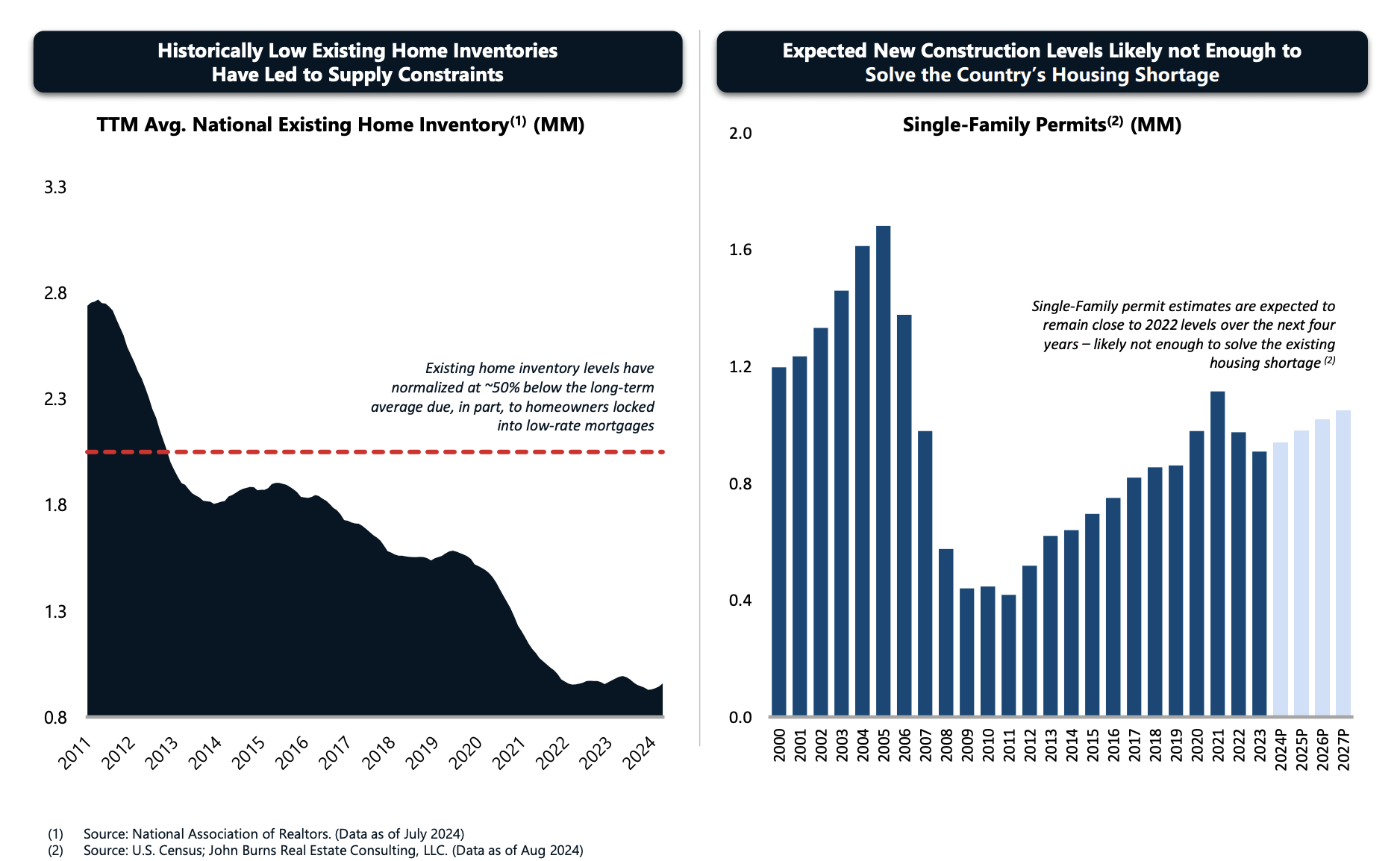

In the short term, there is no telling what could happen. But at some point, it is all but certain that there will be strength in this market. The question is how long we could have to wait for that to happen. And based on the market's reaction to the Presidential Election, there does appear to be a real risk that the Trump Administration will not be friends with the homebuilding industry. The reason why I say that the picture will eventually change is because, in addition to the US population growing, there has been a trend toward low existing home inventories for several years now. And even American Homes 4 Rent (AMH), citing data provided by the US Census Bureau, expects there to be at least single-family permit growth for the next few years. Obviously, this could be stifled depending on economic policies implemented by the incoming Administration. But that is something that investors will have to watch closely.

American Homes 4 Rent

Takeaway

Based on all the data presented throughout this article, I would make the case that there's a lot of uncertainty regarding the homebuilding industry specifically. Personally, I am a fan of picking individual homebuilders. But a lot of investors prefer to be more diversified with their money. Even though it would be giving them exposure to aspects outside of just the homebuilding market, expanding it to things like maintenance and repair, homebuilding retail, and more, the XHB ETF might very well be worth considering. Of course, because of uncertainty regarding political matters and the impact those could have on the economy, things might not pan out in the kind of timeframe that investors reading this article might want them to. But with a favorable the picture that points to weak existing home inventories and the government, at least up to this point, forecasting single family permit growth for the next few years, a positive trajectory will eventually develop. Those who don't mind waiting might very well be handsomely rewarded.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.