Option Focus | Institutions Build Long-Dated Tesla 650–660 Bull Call Spreads, While Hedge With December $350 Puts

$Tesla(TSLA)$ closed at $391.95 on Wednesday, rising 7.62% and extending its winning streak to five consecutive sessions, with cumulative gains exceeding 14%.

Recent activity in Tesla’s options market has been dominated by sizable block trades, בעיקר in longer-dated contracts such as June 2027 expiries. Institutional investors have constructed large-scale bull call spread strategies, positioning for significant long-term upside, while simultaneously purchasing long-dated put options as downside hedges—reflecting a constructive outlook paired with disciplined risk management.

Options Market Overview

Implied Volatility and Volume

Current implied volatility (IV) stands at 54.25%, with an IV percentile of 49.20%. This places IV in a historically neutral range, indicating that options are neither particularly cheap nor expensive.

The put-to-call volume ratio is 1.79, suggesting an overall bullish bias in trading activity.

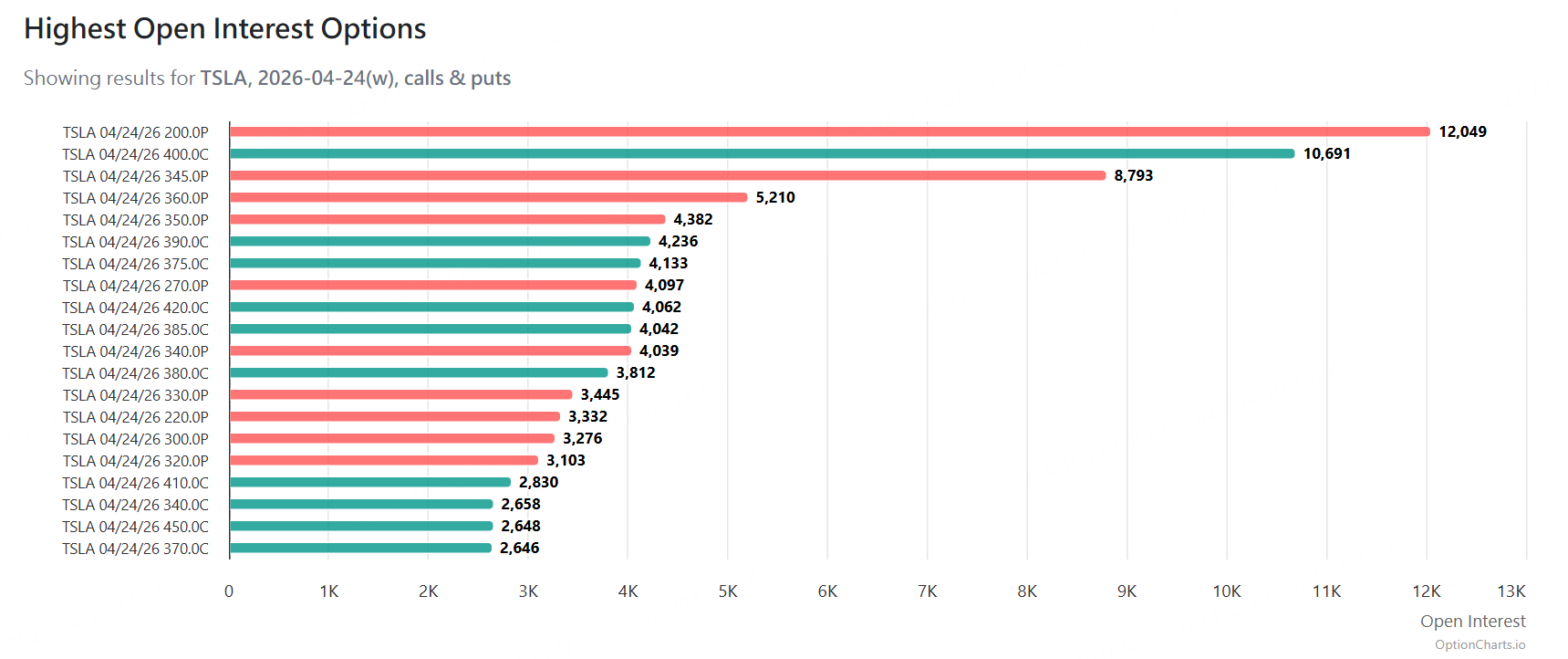

Open Interest Positioning

Based on the April 24, 2026 options chain, open interest is concentrated around several key strike levels:

-

On the call side, $400 (10,691 contracts), $390 (4,236 contracts), and $375 (4,133 contracts) have accumulated significant positions.

-

On the put side, $350 (4,382 contracts) and $360 (5,210 contracts) also show notable open interest.

Block Trades

-

Structured Strategy: Long-Dated Bull Call Spread

A notable institutional trade established a June 2027 bull call spread, involving the purchase of 6,001 $650 calls and the sale of 6,001 $660 calls. The position was initiated at a net cost of $1.05 per share, implying a total premium outlay of approximately $630,000.

$TSLA Vertical 270617 650.0C/660.0C$

This structure represents a leveraged but risk-defined bullish wager that Tesla’s stock could rise above $650 over a horizon of more than one year. By capping both potential gains and losses, the strategy reflects a cautiously optimistic long-term outlook.

-

Directional Trade: Long-Term Put Hedge

At the same time, another large transaction involved the purchase of 1,400 December 2026 $350 put options, with a total premium of approximately $5.26 million.

Such a position is typically interpreted as either “disaster insurance” for an existing long exposure or a direct bearish bet on a significant decline over the next six to twelve months. The relatively high premium underscores a strong emphasis on hedging tail risks.

Outlook and Strategy Implications

Signals from Tesla’s options market point to a mixed outlook. While some investors are positioning for continued upside through structured call spreads, others are allocating substantial capital toward downside protection. This combination often suggests expectations of elevated volatility with uncertain direction.

Key levels to watch include the $380–$385 range, where short-term call positioning is concentrated, and the $350 level, which aligns with longer-dated put interest and may act as a critical support zone.

For investors with a bullish outlook, the current moderate IV environment keeps outright call purchases relatively affordable. Alternatively, a bull call spread—such as buying a lower-strike call while selling a higher-strike call—can help reduce upfront costs while clearly defining the risk-reward profile.

$(TSLA)$Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.