Covering Analysts Reiterate Confidence in OUE REIT Following Robust 1Q 2026 Performance

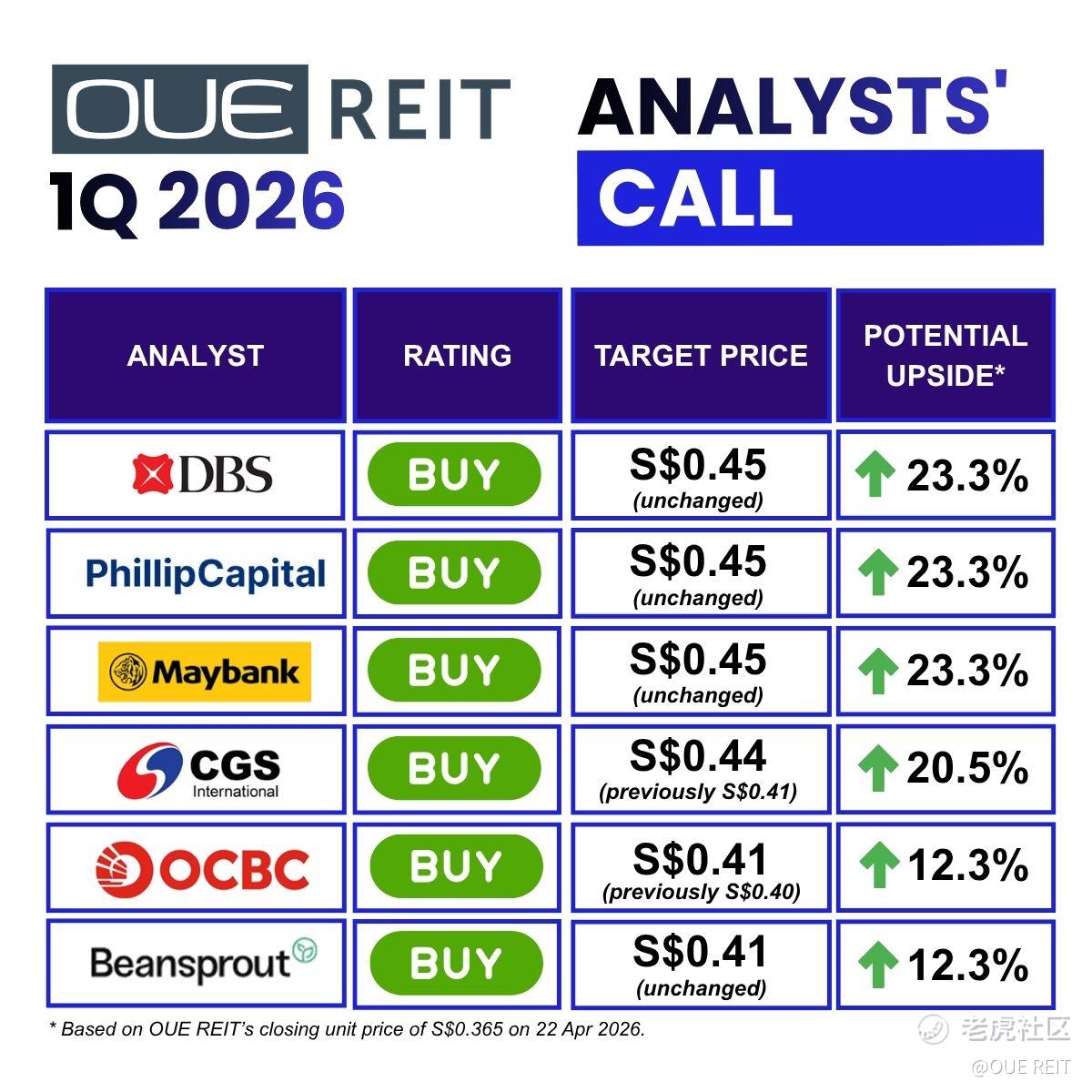

Following our robust 1Q 2026 performance, we are pleased to see covering analysts reiterate their confidence in OUE REIT in their latest reports and maintained their “BUY”/“ADD” ratings.

CGS International and OCBC raised their target prices to S$0.44 and S$0.41 respectively and increased their FY 2026 DPU forecasts after factoring in the acquisition of a 19.9% interest in 180 George Street and potential upside upon the completion of OUE Bayfront’s Level 17 space conversion.

Meanwhile, DBS, Maybank, PhillipCapital and Beansprout highlighted OUE REIT’s strong 1Q 2026 performance, supported by broad-based portfolio growth, a clear recovery in hospitality performance, and a more efficient capital structure with upside from easing interest rates.

𝐊𝐞𝐲 𝐕𝐢𝐞𝐰𝐬 𝐟𝐫𝐨𝐦 𝐀𝐧𝐚𝐥𝐲𝐬𝐭𝐬:

[你懂的] 𝐏𝐡𝐚𝐬𝐞 3 𝐕𝐚𝐥𝐮𝐞 𝐂𝐫𝐞𝐚𝐭𝐢𝐨𝐧 𝐉𝐨𝐮𝐫𝐧𝐞𝐲

-

Active capital reallocation in action with the strategic acquisition of 19.9% interest in 180 George Street, providing high-quality exposure to Sydney’s core precinct

-

Proactive asset enhancement with OUE Bayfront securing planning approval to create more than 22,600 sf of prime office space and is expected to deliver a stabilised ROI exceeding 11.0%

[你懂的] 𝐒𝐭𝐫𝐨𝐧𝐠 𝐫𝐞𝐛𝐨𝐮𝐧𝐝 𝐢𝐧 𝐭𝐡𝐞 𝐡𝐨𝐬𝐩𝐢𝐭𝐚𝐥𝐢𝐭𝐲 𝐬𝐞𝐠𝐦𝐞𝐧𝐭

-

Hospitality revenue surged 15.1% YoY and NPI jumped 16.8% YoY, supported by proactive revenue management, refreshed offerings and a stronger MICE pipeline versus the same period last year

-

Encouraged by the positive trajectory and guided that forward bookings for the hospitality segment remained resilient as at end April

[你懂的] 𝐋𝐨𝐰𝐞𝐫-𝐭𝐡𝐚𝐧-𝐞𝐱𝐩𝐞𝐜𝐭𝐞𝐝 𝐟𝐢𝐧𝐚𝐧𝐜𝐞 𝐜𝐨𝐬𝐭𝐬

-

Financing costs declined by c.18% YoY, providing an upside surprise

-

Among the key beneficiaries of a declining interest rate environment in Singapore within the mid-cap REIT space, with steady QoQ interest savings likely to continue

[你懂的] 𝐑𝐞𝐬𝐢𝐥𝐢𝐞𝐧𝐭 𝐜𝐨𝐦𝐦𝐞𝐫𝐜𝐢𝐚𝐥 𝐨𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐩𝐞𝐫𝐟𝐨𝐫𝐦𝐚𝐧𝐜𝐞

-

Rental reversions for the Singapore office portfolio moderated but remained robust at +6.0%, while committed occupancy for Mandarin Gallery was stable with rental reversions of +3.8%

-

Expect margins to remain stable, underpinned by long-term utilities contracts in Singapore and cost pass-through to tenants in Australia

Read more here:

-

The Business Times “Off to a good start’: Analysts expect OUE REIT to unlock further value from assets after strong Q1 showing”: https://lnkd.in/gxPH4zBN

-

The Edge Singapore “OCBC, DBS, CGSI maintain positive views on OUE REIT”: https://lnkd.in/gUWaRZU9

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.