Option Focus | ARM Volatility Spikes to a Record 95%; Block Trade Builds $220/$227.5 Call Position for Upside Bet

$Arm Holdings(ARM)$ is set to report its latest quarterly results on May 6, 2026, after the U.S. market close, with investors closely watching its growth momentum amid the ongoing AI boom. Consensus estimates point to revenue of $1.471 billion for the quarter, up 19.4% year-on-year, while adjusted earnings per share are expected to come in at $0.58, marking a 10.83% increase from a year earlier.

Options positioning around the earnings window

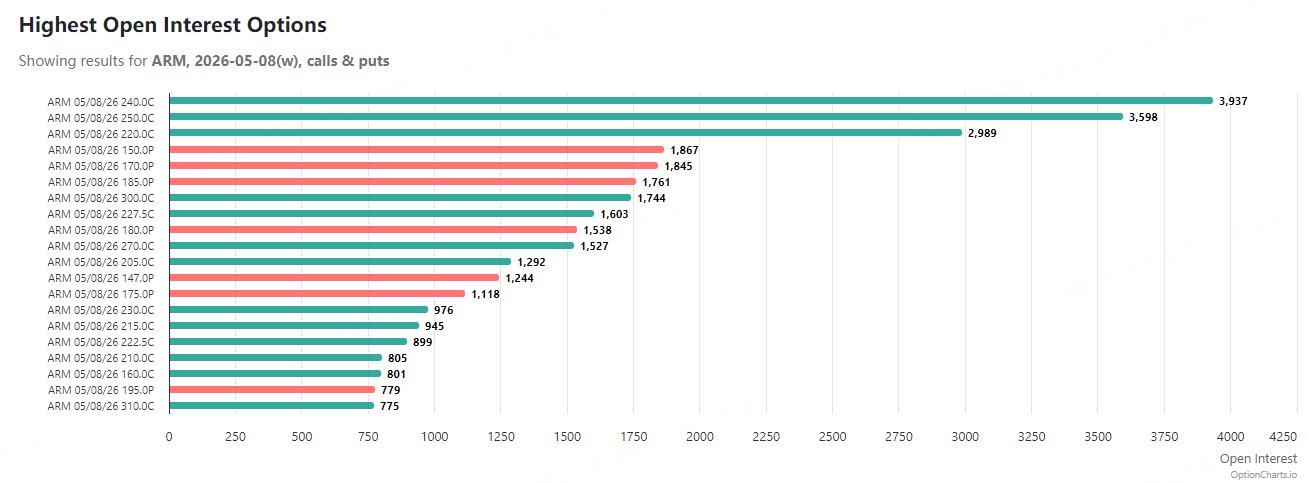

1. Notable open interest concentrations

Based on options expiring May 8, 2026, contracts with relatively high open interest include:

-

$240 strike calls: 3,937 contracts

-

$250 strike calls: 3,598 contracts

-

$220 strike calls: 2,989 contracts

Interpreting recent block activity

Over the past three trading sessions, options flows suggest a buyer-dominated positioning combining short-term bullish exposure with medium- to long-term hedging, against a backdrop of elevated implied volatility (IV percentile at 95.22%).

1. Near-term bullish bet: double-long call structure

-

Trade structure: Simultaneous purchases of May 8, 2026 $220 and $227.5 strike calls, with a net premium outlay of $2.6786 million.

-

Interpretation: This represents a directional bullish wager that the stock could break above $227.5 shortly after earnings.

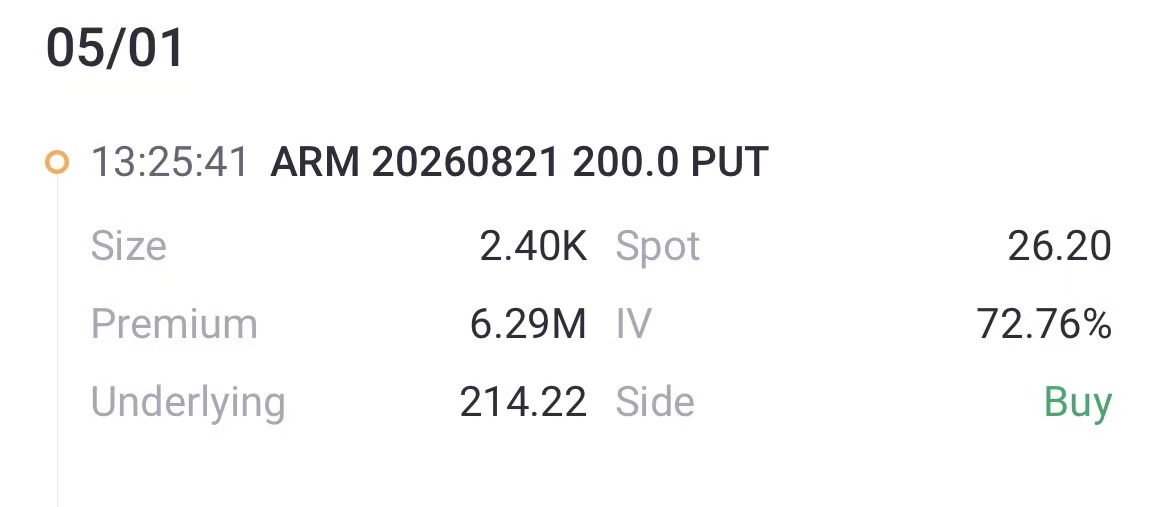

2. Medium- to long-term downside protection: longer-dated puts

-

Largest single trade: Purchase of August 21, 2026 $200 strike puts, with notional turnover of $6.288 million—typically viewed as either downside protection or a directional bearish position over the medium term.

-

Tail-risk hedge: Buying deeply out-of-the-money January 15, 2027 $100 strike puts, with a premium of $540,000, aimed at guarding against extreme downside scenarios at relatively low cost.

Takeaways and strategy considerations

Positioning suggests the market is bracing for heightened volatility and potential upside in the near term, while simultaneously adding longer-dated put protection as portfolio insurance.

For option sellers, the current elevated implied volatility presents an opportunity to collect rich premiums. However, outright selling of out-of-the-money options (e.g., calls above $235 or puts below $185) entails substantial risk exposure. Investors seeking defined risk may instead consider spread strategies—such as iron condors or butterflies—to cap both downside and upside while monetizing elevated volatility.

$(ARM)$ $(ARMG)$ $(ARMW)$ $(ARMU)$Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.