Adjustments to Options After Corporate Actions and Formation of Non-Standard Options

In option trading, corporate actions refer to major events occurring to listed companies, such as stock splits, reverse splits, special dividends, mergers and acquisitions, etc. These events affect the price, quantity, or structure of the underlying stock, requiring corresponding adjustments to option contracts to maintain the fairness and economic value of the contracts. According to the rules of the Options Clearing Corporation (OCC), option contracts usually undergo standardized adjustments after a corporate action, but some adjustments will cause the option to transform from a standard contract to a non-standard option. Below are the basic principles of option adjustments:

-

Standard Option Contracts: Usually based on 100 shares of the underlying stock, with fixed strike price and expiration date, and the deliverable is a standard number of shares.

-

Adjustment Trigger: After a corporate action occurs, the OCC will evaluate and adjust the option contract to ensure that the rights and interests of option holders are not diluted or amplified. Adjustments usually take effect on the next trading day after the corporate action takes effect.

-

Common Adjustment Types:

-

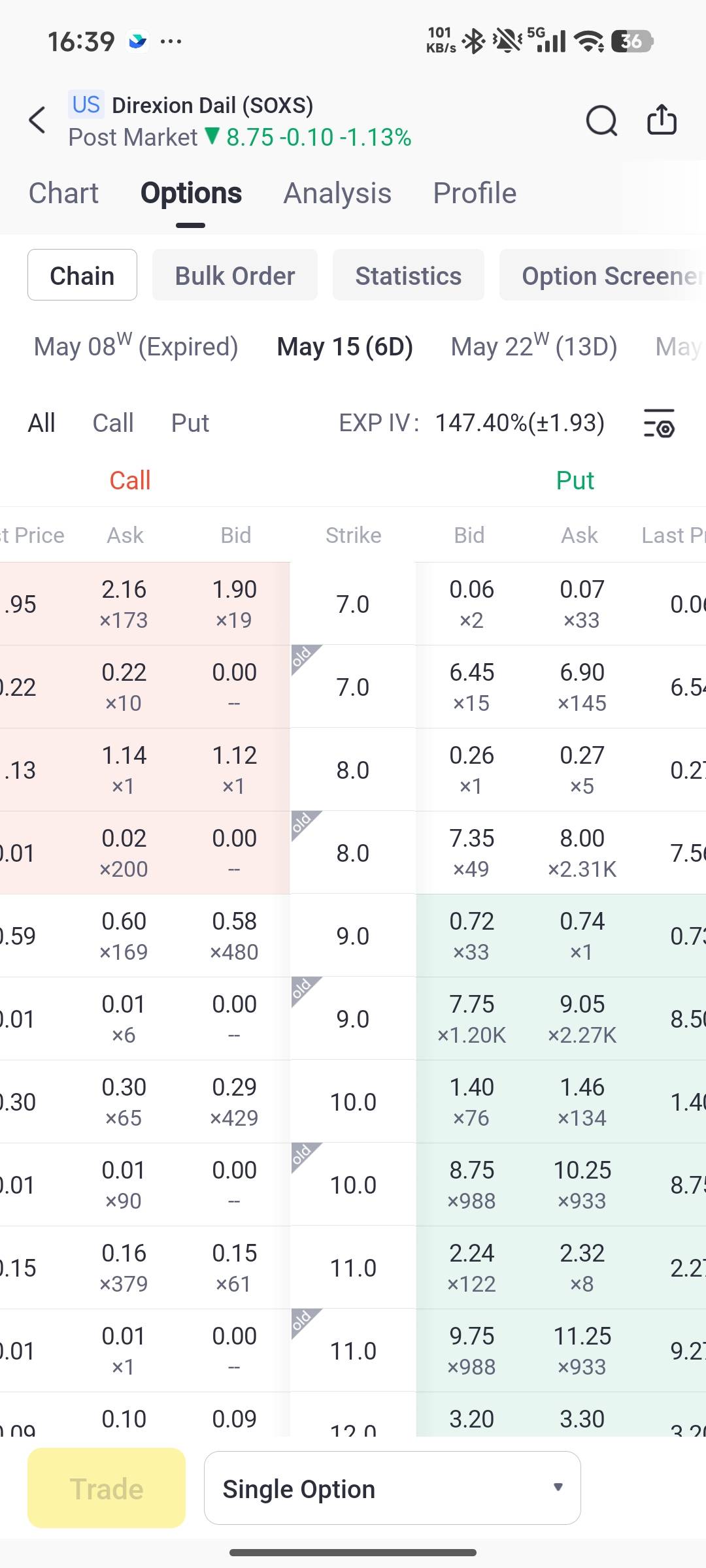

Stock Split (e.g., 1-for-2): If the underlying stock undergoes a forward split, the strike price of the option contract will decrease accordingly (e.g., original strike price $100 becomes $50), and the number of shares covered per contract will increase (e.g., from 100 shares to 200 shares). This makes the option a non-standard contract because the number of deliverable shares is no longer the standard 100 shares.

-

Reverse Split (e.g., 2-for-1): The strike price will increase (e.g., original $50 becomes $100), and the number of shares covered per contract will decrease (e.g., from 100 shares to 50 shares), also leading to non-standardization.

-

Special Dividends or Cash Dividends: If the dividend exceeds a certain threshold (usually 10% of the stock price), the strike price will be adjusted downward (subtracting the dividend amount), but the number of shares per contract remains unchanged. If cash delivery is involved, the option may transform into a non-standard form delivering cash or other assets.

-

Mergers or Restructuring: Options may be adjusted to deliver based on the new company's stock, cash, or other securities. For example, if a company is acquired, the option may be converted to a cash-settled contract or a contract for new stock, leading to changes in the strike price and deliverables.

-

Other Situations: Such as stock symbol changes or company spin-offs, the option chain may be migrated entirely to the new symbol and parameters adjusted.

-

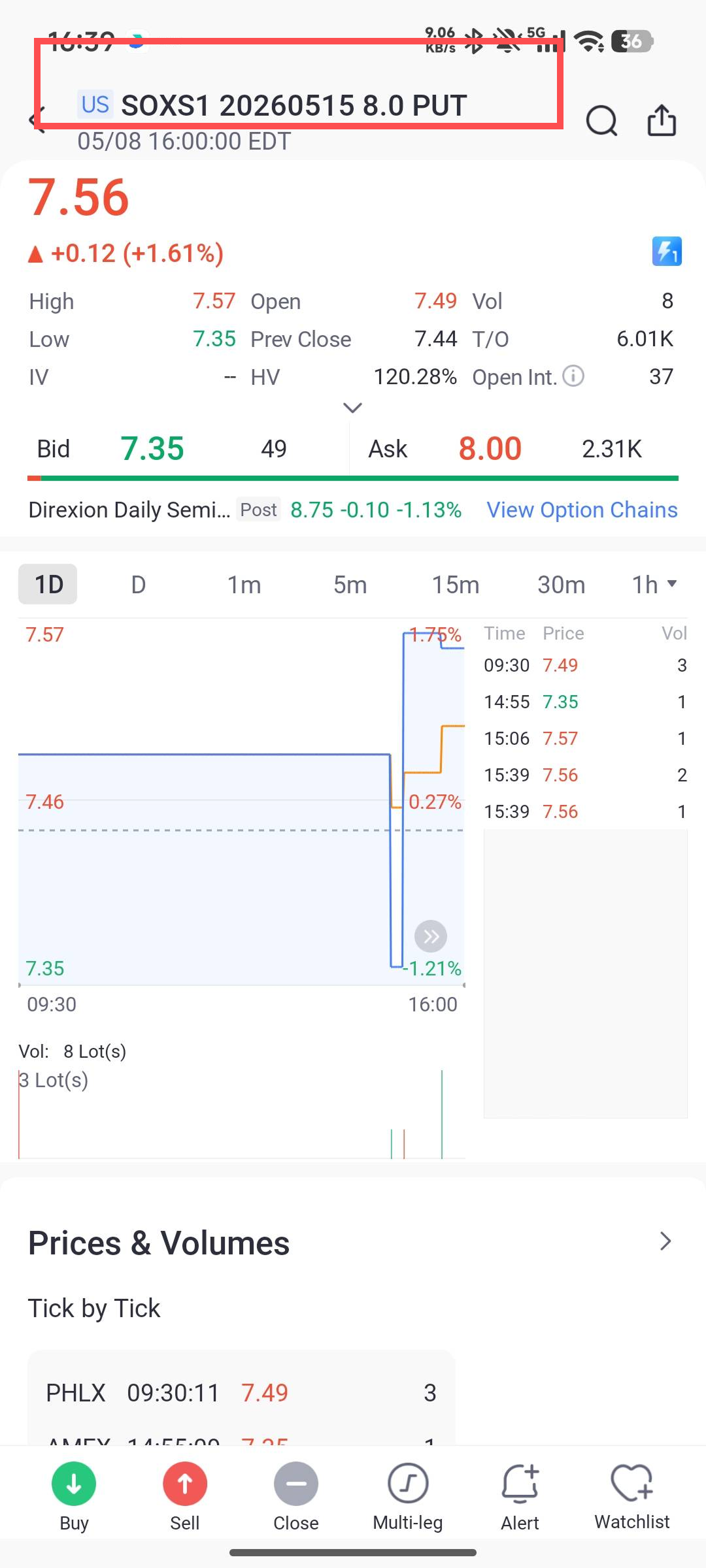

After these adjustments, the symbol of the option contract usually adds a suffix (e.g., ".1" or ".2") to identify its non-standard nature, and the original option chain may be marked as "Non-Standard Option" or "Old Option." Non-standard options are still tradable on exchanges (e.g., CBOE), but their terms (such as the number of deliverable shares, strike price multiple) are different from standard options, leading to more complex pricing models and risk management. Users are strongly advised to avoid trading these non-standard options as much as possible to reduce potential risks. Below are the main reasons:

-

Low Liquidity: Due to their unique contract terms, non-standard options usually have much lower trading volumes than standard options. This leads to a wider bid-ask spread, and users may find it difficult to trade at a reasonable price, or even unable to close positions in time during market fluctuations, increasing holding costs and opportunity losses.

-

Complex Pricing and Valuation: Standard options can be easily valued using standard tools such as the Black-Scholes model, but non-standard options involve adjusted share counts, strike prices, or deliverables (e.g., partial cash + stock), which can easily lead to valuation errors, especially for retail investors, increasing the risk of misjudging market direction.

-

High Risk Management Difficulty: The behavior of Greeks (e.g., Delta, Gamma) of non-standard options is different from that of standard options, making hedging strategies (such as Delta hedging) more difficult to implement. During market fluctuations, the price of non-standard options may fluctuate more violently, leading to unexpected losses. In addition, if the deliverable involves non-integer shares or mixed assets, users may face additional tax or settlement complexity when exercising the option.

-

Potential Regulatory and Compliance Risks: Non-standard options sometimes involve legal uncertainties from corporate actions (e.g., merger lawsuits), and long-term holdings may be adjusted again due to further corporate actions, increasing uncertainty.

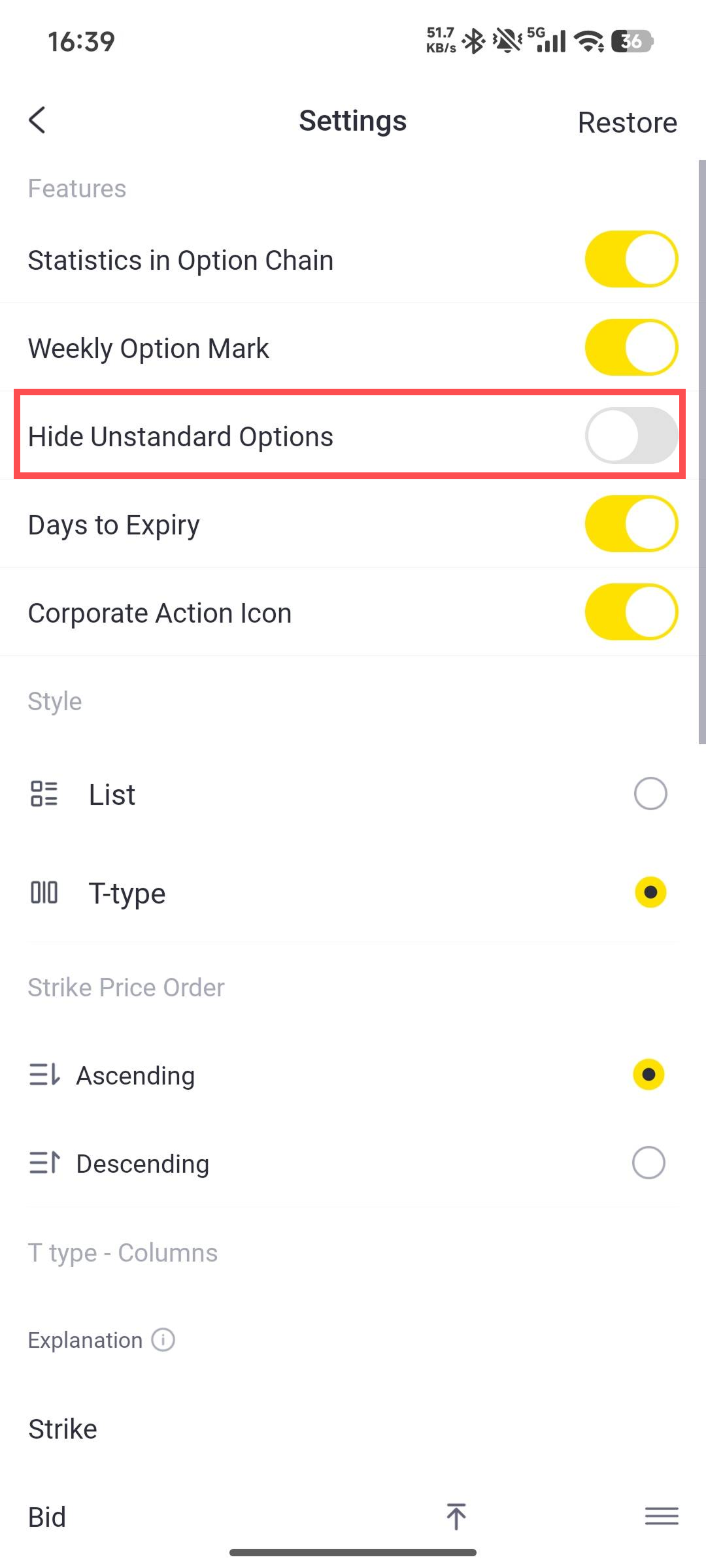

In conclusion, it is recommended that users prioritize standard option chains for trading. If it is necessary to involve options related to corporate actions, please close positions before the action or consult a professional advisor. Our platform will remind users of these changes through notifications and labels (e.g., "Old Option") to enhance user experience and risk awareness. If you still wish to trade these non-standard options, you can set a switch in the option chain settings to view them.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Great article, would you like to share it?