Zoom Video: Normalization Gone Bad

Summary

•Zoom beat FQ2'22 analyst targets, but the size of quarterly beats continues to trend downwards.

•The company forecast FQ3'22 revenues to decline sequentially in further signs of a slowdown in business.

•The stock headed into the quarter trading at 20x forward sales, while the future growth rates don't warrant this valuation.

A lot of individual investors didn't want to listen, but $Zoom(ZM)$ faced nearly impossible comps due to pulledforwarddemand. Inaddition, the recent deal to acquire $Five9 Inc(FIVN)$ is exactly what companies do in order to replace stalling growth. My investment thesis remains very Bearish on the stock not correctly priced for the new normalized, post-Covidphase.

End Of The Growth Phase

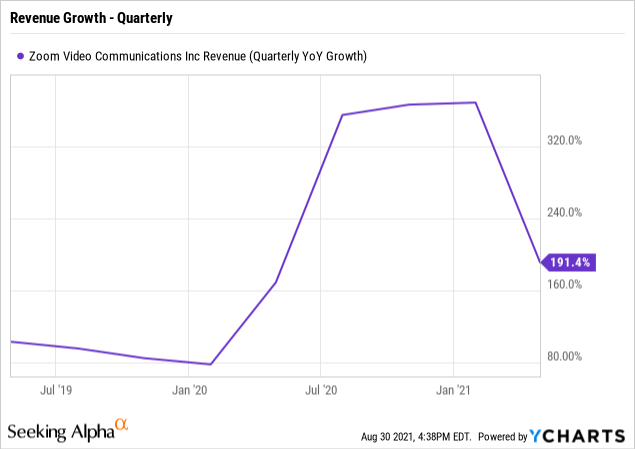

For the quarter ending July 31, Zoom reportedrevenue surged 54% YoYto top $1 billion for the first time. The cloud communications company had guided to quarterly revenues of$990 millionjust months ago.

Clearly, investors need to take into account Zoom beat originally guided FQ2'22 revenues to upwards of $31 million. The company ended up reporting revenues of $1.021 billion.

More important to the stock was guidance. Zoom guided to FQ3'21 revenues of $1.015 billion to $1.020 billion. The cloud communications company actually guided revenues down sequentially.

This number is crucial considering Zoom reported FQ1'22 revenue of $956 million and guided up to FQ2'22 revenues of $990 million. Very notably, the company expected revenues to grow $34 million sequentially and ended up growing by $65 million QoQ.

This revenue trend is not the friend of shareholders considering the valuation of the stock. Zoom beat analyst estimates by $30 million in the quarter, but the company has seen the beats substantially decline as revenues have soared from just $328 million back in FQ1'21 to over $1 billion now. The quarterly beats were over $100 million as Covid demand ramped up.

As seen in another light, revenue growth has now collapsed from over 300% to 54% now. The guidance has revenue growth at around 31% in FQ3'22 with a path to limited growth in FY23 and beyond.

Customer Peak

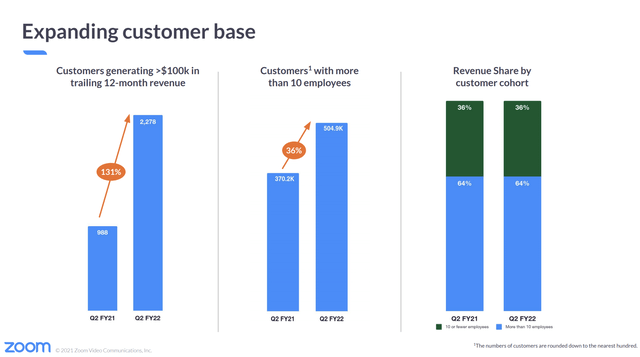

The customer growth rates have been a solid indication that Zoom would run into growth struggles this year. For the quarter, customers with more than 10 employees only grew 36% to 505K.

At some point, Zoom was going to quickly run out of customers to add. The company hit 497K customers in FQ1'22 and only grew the base by 8K sequentially. The prior quarter saw the customer base grow 30K sequentially from 467K.

The implication here is that the reopening play could even lead Zoom to see a decline in customers. Enterprises might no longer need cloud communication solutions with the preference to in-person meetings, or customers might just scale back usage.

All along, this was the problem with paying a massive $150+ billion market cap for Zoom at the peak. The company hasn't made the case for massive sustained growth rates anytime soon.

At best, Zoom will return to strong growth after a 12-18 month consolidation phase considering the unexpected growth surge in the last 18 months. The question is where the stock will be valued about 18 months from now with an extended period of constrained growth.

The stock trades at ~20x forward sales estimates of $4.8 billion while one has to question whether Zoom can grow by 20% in FY23. The company isn't expecting any revenue growth in the current quarter and the customer account isn't expanding anymore. Investors shouldn't expect the net expansion rate of 130% to remain anywhere close to those levels as most customers expanding substantially during the lockdown could easily pull back on spending.

Zoom is reporting massive profits and cash flows here, so investors need understand the difference between a great company and a bad stock. The company outlook for FY22 forecasts net income of $1.5 billion with an EPS slightly below $5 per share with ~308 million shares outstanding. The company generated $468 million in operating cash flows leading to impressive FCF of $455 million. These numbers are impressive for a company, but not so much for a stock still worth $100 billion heading into the quarterly report.

With the massive growth, Zoom was able to leverage the cost base without related spending on SG&A and product enhancements. The shift to cloud communications happened so fast that the company will now need to spend aggressively in an attempt to recapture growth and maintain market share. The lack of revenue growth and higher spending will lead to relatively flat EPS numbers in the next year or so.

Takeaway

The key investor takeaway is that investors should question whether Zoom can grow revenue next year, much less achieve the 20% analyst target. Under such a scenario, the stock shouldn't even trade at 10x forward sales.

Zoom is trading down $30 in after-hours and investors should expect the recent lows below $300 to be at risk here.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.