Singapore REIT Monthly Update (Aug 07 – 2021)

Technical Analysis of FTSE ST REIT Index (FSTAS351020)

FTSE ST Real Estate Investment Trusts (FTSE ST REIT Index) increased slightly from 868.08 to 882.31 (+1.64%) compared to thelast month update. Currently the Singapore REIT index is still trading with a range between 816 and 890.

- As for now, Short term direction: Sideway and Up.

- Immediate Support at 816, followed by 775.

- Immediate Resistance at 890.

Previous chart on FTSE ST REIT index can be found in the last post:Singapore REIT Fundamental Comparison Tableon July 4, 2021.

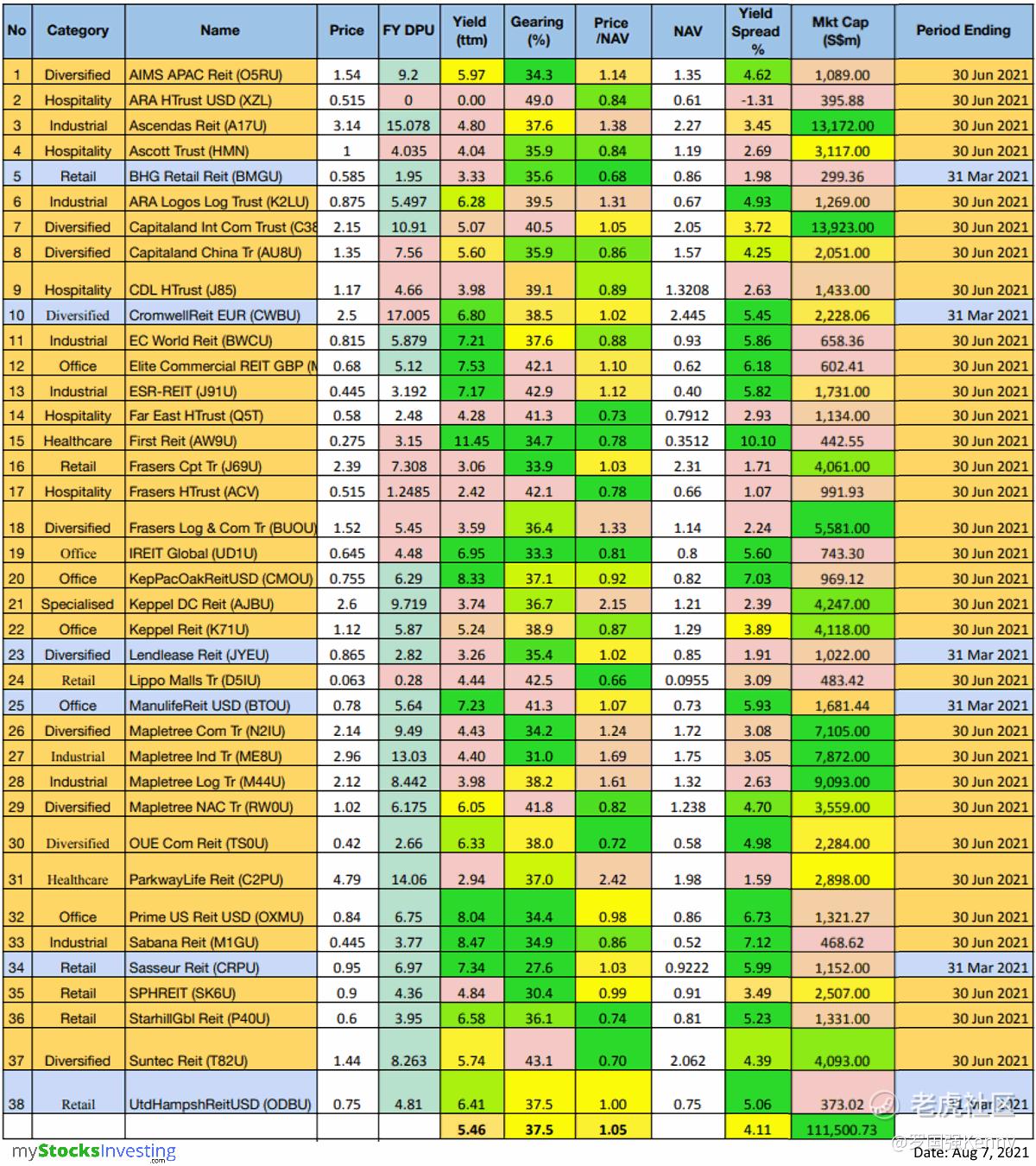

Fundamental Analysis of 38 Singapore REITs

The following is the compilation of 38 Singapore REITs with colour coding of the Distribution Yield, Gearing Ratio and Price to NAV Ratio.

- Note 1: Eagle Hospitality Trust has been removed.

- Note 2: The Financial Ratio are based on past data and there are lagging indicators.

- Note 3: This REIT table takes into account the dividend cuts due to the COVID-19 outbreak. Yield is calculated trailing twelve months (ttm), therefore REITs with delayed payouts might have lower displayed yields, thus yield displayed might be lower.

- Note 4: REITs inorangehave been updated with Q2 2021 business updates/earnings. REITs inblueare still using Q1 2021 values.

(Source: https://stocks.cafe/kenny/advanced)

Price/NAVdecreasedto 1.05

- Decreased from 1.06 in July 2021.

- Singapore Overall REIT sector is slightly overvalued now.

- Take note that NAV is adjusted downward for most REITs due to drop in rental income (Property valuation is done using DCF model or comparative model)

TTM Distribution Yieldincreasedto 5.46%

- Increased from 5.16% in July 2021.

- 9 of 38 (23.7%) Singapore REITs have distribution yields of above 7%.

- Do take note that these yield numbers are based on current prices taking into account the delayed distribution/dividend cuts due to COVID-19, and post circuit breaker recovery.

Gearing Ratiodecreasedfrom37.50%

- Decreased from 37.68% in July 2021.

- Gearing Ratios are updated quarterly.

- In general, Singapore REITs sector gearing ratio is healthy but increased due to the reduction of the valuation of portfolios and an increase in borrowing due to Covid-19.

Most overvalued REITs (based on Price/NAV)

- Parkway Life REIT (Price/NAV = 2.42)

- Keppel DC REIT (Price/NAV = 2.15)

- Mapletree Industrial Trust (Price/NAV = 1.69)

- Mapletree Logistics Trust (Price/NAV = 1.61)

- Ascendas REIT (Price/NAV = 1.38)

- Frasers Logistics and Commercial Trust (Price/NAV = 1.33)

- ARA LOGOS Logistics Trust (Price/NAV = 1.31)

Most undervalued REITs (based on Price/NAV)

- Lippo Malls Indonesia Retail Trust (Price/NAV = 0.66)

- BHG REIT (Price/NAV = 0.68)

- Suntec REIT (Price/NAV = 0.70)

- OUE Commercial REIT (Price/NAV = 0.72)

- Far East Hospitality Trust (Price/NAV = 0.73)

- Starhill Global REIT (Price/NAV = 0.74)

- Frasers Hospitality Trust (Price/NAV = 0.78)

Highest Distribution Yield REITs (ttm)

- First REIT (11.45%)

- Sabana REIT (8.47%)

- Keppel Pacific Oak REIT (8.33%)

- Prime US REIT (8.04%)

- Elite Commercial REIT (7.53%)

- Sasseur REIT (7.34%)

- Manulife US REIT (7.23%)

- Reminder that these yield numbers are based on current prices taking into account delayed distribution/dividend cuts due to COVID-19.

- Some REITs opted for semi-annual reporting and thus no quarterly DPU was announced.

Highest Gearing Ratio REITs

- ARA Hospitality Trust (49.0%)

- Suntec REIT (43.1%)

- ESR REIT (42.9%)

- Lippo Malls Retail Trust (42.5%)

- Elite Commercial REIT (42.1%)

- Frasers Hospitality Trust (42.1%)

- Mapletree North Asia commercial Trust (41.8%)

Total Singapore REIT Market Capitalisationincreasedto S$111.5 Billion.

- Increased from S$108.4 Billion in July 2021.

Biggest Market Capitalisation REITs:

- Capitaland Integrated Commercial Trust ($13.92B)

- Ascendas REIT ($13.17B)

- Mapletree Logistics Trust ($9.09B)

- Mapletree Industrial Trust ($7.87B)

- Mapletree Commercial Trust ($7.11B)

- No change in ranking compared to March-June 2021 update.

Smallest Market Capitalisation REITs:

- BHG Retail REIT ($299M)

- United Hamsphire REIT ($373M)

- ARA Hospitality Trust ($396M)

- First REIT ($443M)

- Sabana REIT ($469M)

- All 5 REITs were also the Smallest Market Capitalisation REITs in the March-June 2021 update.

- Eagle Hospitality Trust has been removed

Disclaimer: The above table is best used for “screening and shortlisting only”. It is NOT for investing (Buy / Sell) decision. If you need help to start building your own investment portfolio, or want a portfolio review,book a consultation with Kenny now! First consultation is free.

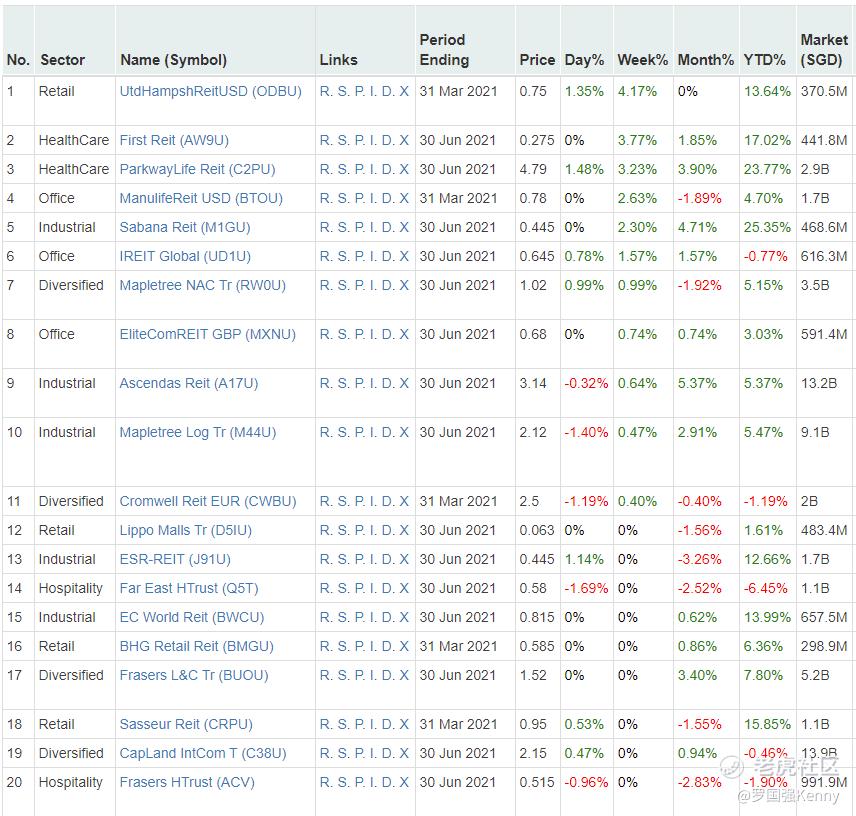

Top 20 Performers of the Month (Source: https://stocks.cafe/kenny/advanced)

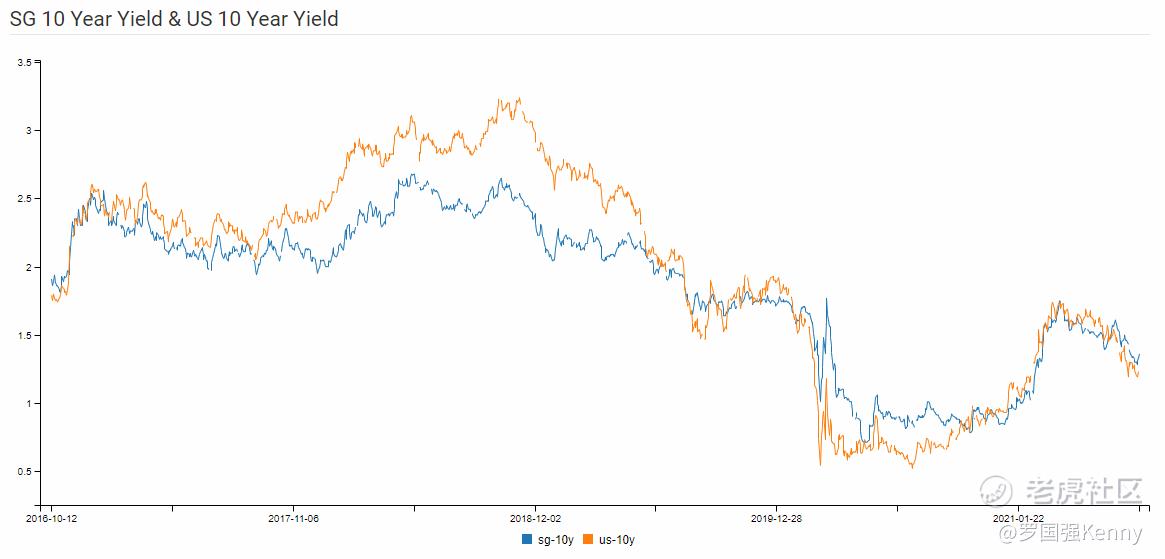

SG 10 Year & US 10 Year Government Bond Yield

- SG 10 Year: 1.36% (decrease from 1.539%)

- US 10 Year: 1.23% (decrease from 1.446%)

Summary

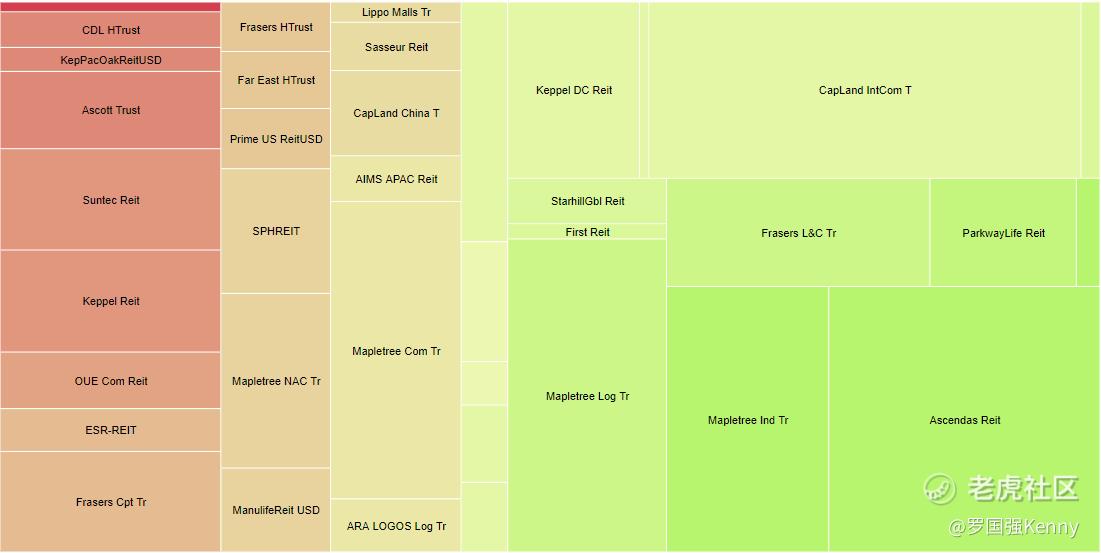

Fundamentally, the whole Singapore REITs landscape is slightly overvalued now based on the average Price/NAV value of the S-REITs. Below is the market cap heat map for the past 1 month. Unlike last month, where Small to Mid Cap REITs are the leaders in performance, in this update, Large Market Cap REITs generally are better performing.

(Source: https://stocks.cafe/kenny/overview)

Yield spread (in reference to 10 year Singapore government bond of 1.36% as of 6th August 2021) decreased slightly from4.11% to 4.10%.However, the risk premium is still attractive to accumulate Singapore REITs in stages to lock in the current price and to benefit from long-term yield after the recovery. Moving forward, it is expected that DPU will increase due to the recovery of global economy, as seen in the previous few earning updates. NAV is expected to be adjusted upward due to revaluation of the portfolio.

Technically the REIT Index is still trading in a sideways consolidation waiting for a breakout (upside bias). Currently the REIT index is testing the resistance zone at 880-890. Breaking this resistance zone will bring the bull back into Singapore REITs sector. Current macro factors such as a low-interest rate environment, aggressive M&A for future DPU growth, wider roll out of the vaccination and recovery of global economic support the bullish breakout. In addition,Singapore is entering the 4 Stages Reopening with high vaccination rate which also supports the bull case.

Note: This above analysis is for my own personal research and it is NOT a buy or sell recommendation. Investors who would like to leverage my extensive researchand years of Singapore REIT investing experience can approach me separately for a REIT Portfolio Consultation.

Kenny Loh is a Senior Consultantand REITs Specialist of Singapore’s top Independent Financial Advisor. He helps clients construct diversified portfolios consisting of different asset classes from REITs, Equities, Bonds, ETFs, Unit Trusts, Private Equity, Alternative Investments, Digital Assets and Fixed Maturity Funds to achieve an optimal risk adjusted return. Kenny is also a CERTIFIED FINANCIAL PLANNER, SGX Academy REIT Trainer, Certified IBF Trainer of Associate REIT Investment Advisor (ARIA) and also invited speaker of REITs Symposium and Invest Fair.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Thank you for sharing [开心][开心][开心]