How the Russian-Ukraine War Will Affect the Chinese Stock Market

The real tragedy is when two powers meet.

As the war rages on in Ukraine, a great chasm has erupted on the Chinese social media. The confusion brought by news from various unverified sources behind the wall threw fuel into the online fire. Amid such a cacophony of how the sanctions on Russia would be applied and what its scope would be, the weekend stock market in the heads of pundits has been rollercoastering through limit-ups and downs.

Such commotions online suggest that traders may have plunged back into stocks, probably lured by the epic intraday reversal in the US market last Thursday night. The trading volume on Friday once again surged to well over one trillion yuan. With new developments on the frontline over the weekend, where are China markets heading in the coming weeks?

Next week will be the important “Two Sessions”, during which the government will likely set the growth target for 2022 to be just above 5%. We should hear more on plans of important projects, updates on infrastructure investment, as well as the all-important property policy.

Early indications have so far been positive: the issuance of special-purpose bonds and local government bonds has accelerated; of the 11 provinces that have announced large investment plans, total project investment increases by more than 20%; “consumption” and “the digital economy” are some of the terms that have shown up frequently in the provincial plans. While infrastructure projects may have grand plans, early statistics on commodities consumed by such projects suggest that many projects have barely started, probably affected by the strict “dynamic zero-tolerance” policy as COVID experiences a resurgence.

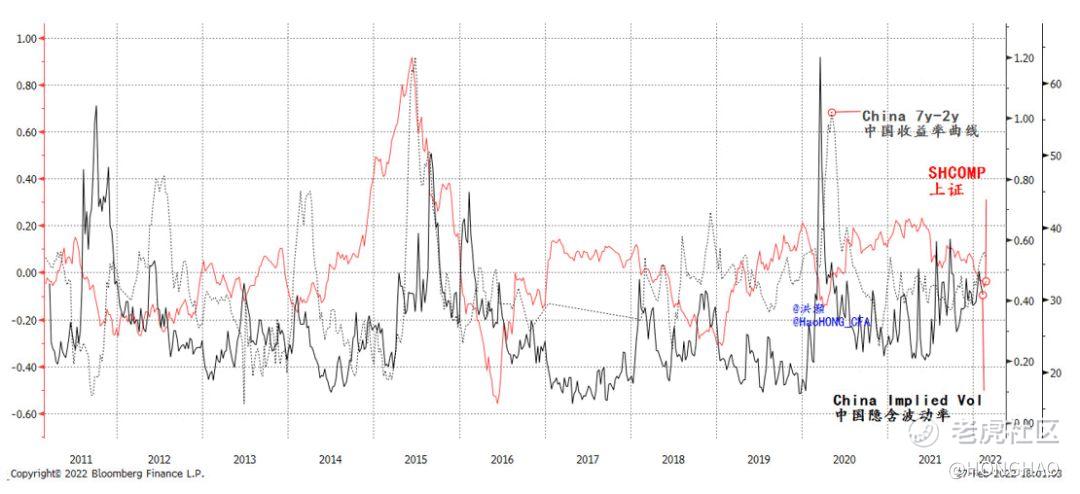

By now, the easing bias is firmly in the price. How else could we explain the implied China market volatility remains elevated, but not yet as high as it had been during previous crises (Figure 1)? Indeed, it is well below the levels seen during the European Sovereign Debt Crisis in 2011, the burst of stock market bubble in 2015 and the pandemic in 2020. As such, as external uncertainties are set to flare in the coming weeks’ trading, pressure on the stock market should still cloud. Till last Friday, sufficient liquidity has helped calm the market down amid epic market gyrations overseas. For instance, the PBoC injected RMB500bn via open market operations last Thursday and Friday.

Many believe that uncertainties in the foreign markets may compel the PBoC to ease even more aggressively. But the strengthening yuan to near the level seen just before the currency reform in August 2015 suggests that the central bank is moving at its own measured pace, probably preparing monetary leeway for contingencies. And if the PBoC does ease aggressively later as hoped, it should be considered an insurance policy to insulate the Chinese economy from external uncertainties. And if so, such easing is a red light of emergency, and will cushion the downside of the economy and hence the stock market, rather than goading for the upside.

Figure 1: China’s implied volatility is elevated, but not at levels consistent with previous crises; pressure on the SHCOMP has yet to dissipate

The US market’s epic intraday reversal suggests that it believes the Ukraine war to be a transient, one-off hit. If so, why would the market also expect a less hawkish Fed based on market volatility, as seen in the falling implied rate hikes by treasury futures? After all, one of the few certainties out of this still unravelling war is that oil price will likely head higher. Commodities, too, as a hedge against inflation from supply chain disruptions. Inflation at its current level is definitely not consistent with the Fed’s policy target of price stability, while employment is strong.

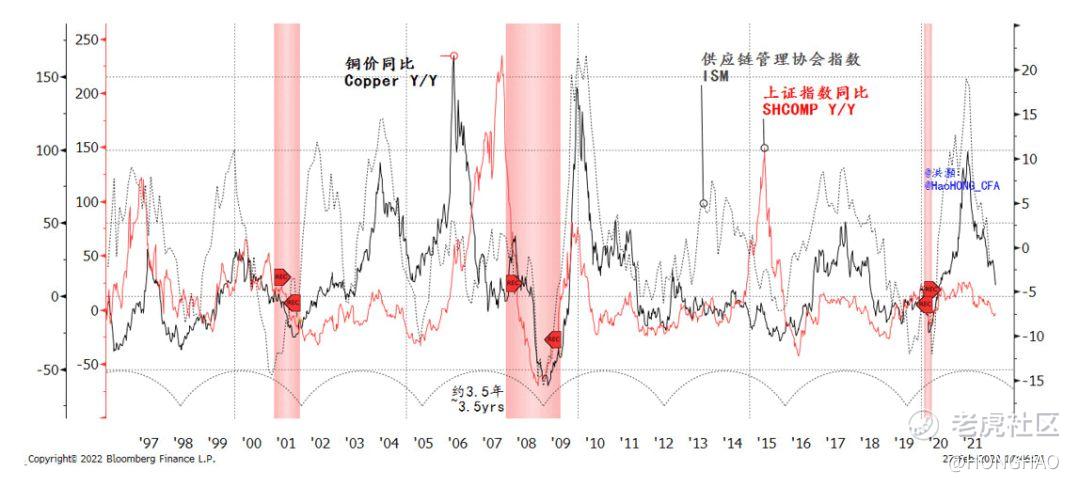

In our recent reports, we have repeatedly warned the biggest risk that the global economy is confronting is Fed tightening even as the US economic cycle starts to decelerate rapidly (Figure 2). The US economic cycle is slowing, as confirmed by the plunging ISM and copper cycle, while the China economic cycle is stuck at its trough. The cycles of the two major economies intertwine every three to four years. At such junctures, they will together conjure up significant confluences on the global scene.

Momentous historical events tend to happen around these junctures, and they are no coincidences. Otherwise, we would have to explain why such historic events tend to crowd around the periods when the US economic cycle collides with China’s. Last time we saw a similar episode was in 2018, when we called against consensus a dramatic market turmoil amid the trade war (Figure 2, please refer to our report“The Colliding Cycles of the US and China” on 2018-09-03). As such, the Ukraine war is one of the many manifestations of the end of the economic cycle, as well as the conflicts between the US and China’s cycles. It is now a particularly volatile period not conducive to risk taking.

Figure 2: Global economic cycle is plunging into a deceleration phase

In sum, the Ukraine war will continue to unravel and pile on uncertainties, at a juncture when the US cycle is decelerating rapidly while China’s cycle is stuck at its trough. The implied China market volatility is elevated, but at levels well below previous crisis episodes. As such, traders may have plunged back into the market too soon last Friday, and pressure on China’s markets will persist.

The war will mean higher oil and commodity prices, and thus higher inflation pressure will give little excuse for the Fed not to tighten according to plan. A strong yuan suggests that the PBoC may not be easing aggressively as hoped, leaving leeway for monetary insurance should the uncertainties from the war spill over. The “Two Sessions” will likely set the growth target at 5%, not deviating from consensus.

The war is one of the many manifestations of the end of the cycle. As we have repeatedly warned recently, this juncture is particularly volatile and not yet conducive to risk taking. Historic events tend to occur at the final phase of cycles, especially with the confluences between the US and Chinese economies. At the time when we sounded our warnings of impending risks, the gunshots of the Ukraine war had not been fired (“What the Tiger Year Means for Chinese Stocks”, 2022-02-07). The narrow difference between audacity and rashness is patience. As the “Two Sessions” start, we will have a better compass to navigate the troubled waters.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

👍🏻👍🏻