Where is the bear🐻?

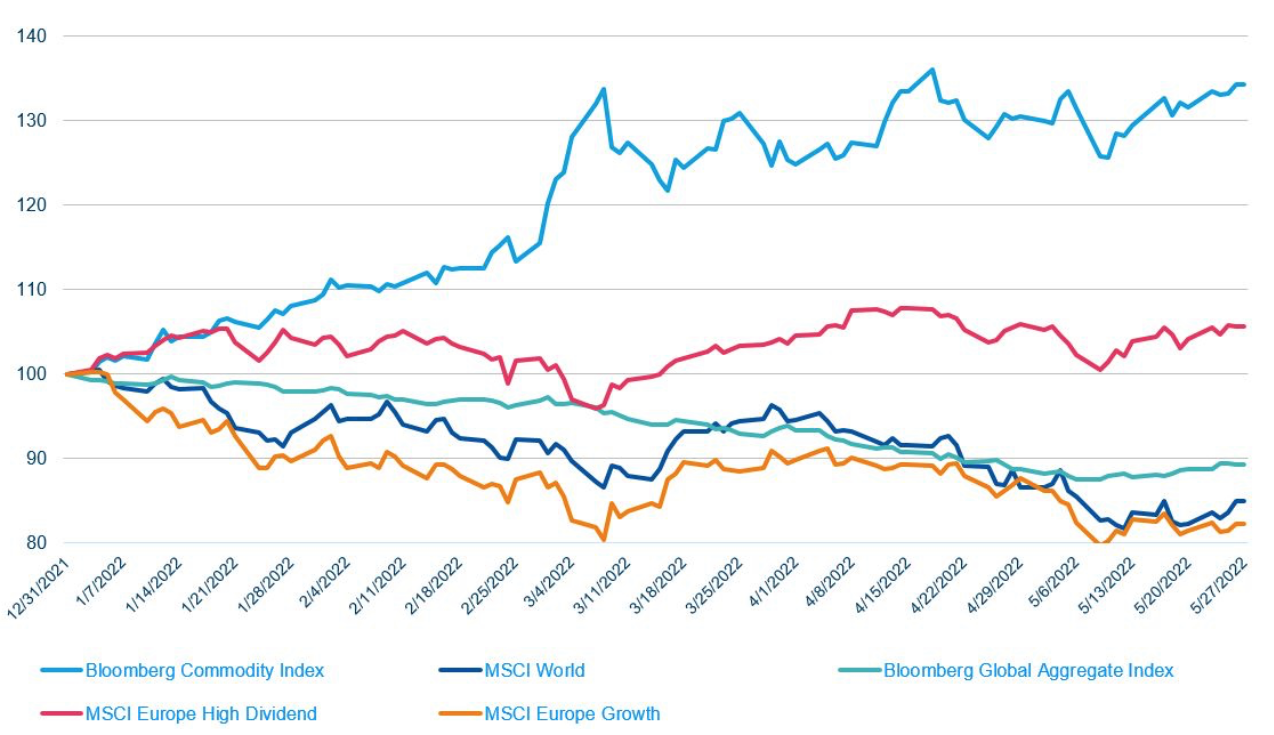

While the MSCI World$MSCI Inc(MSCI)$ is down around -15% YTD and the Bloomberg aggregate Fixed Income Index lost more than -10% YTD, Commodities (Bloomberg Commodity Index) are up 33% YTD. This shows how essential commodities are for a diversified, multi-asset portfolio.

However, not only active asset allocation can generate alpha. Single name selection pays off as well. European Growth Stocks (MSCI Europe Growth Index) are down -18% YTD. At the same time, MSCI Europe High Divided Index gained almost 6% YTD. It is the highest level of dispersion we are seeing in a long time. Diversification paid with active management gets crucial again.

Commodities

Commodities

Commodities remain strong, reaching new highs. This performance is mainly driven by Energy and to some extent Agricultural. Base Metals have been consolidating in May and lost close to 3%. Trend-following models continue to capitalize on this opportunity. The media is full of justifications for why commodities are trending higher: rising demand, tight supply with supply chain disruptions, and geopolitical risks are just a few. However, commodities started their uptrend in late 2020 — long before geopolitical risks were on the agenda.Precious Metals are in their uptrends despite the 12% drawdown Gold just went through. Gold and Silver have not been delivering the returns many observe have been expecting, especially when inflation is on the rise. Nevertheless, Precious Metals perform an important part in a portfolio: they provide relative stability when other asset classes struggle.

Stocks and Bonds continue to be under pressure and both are trading in intermediate-term downtrends. Although the last days of May have shown some relief (bear market rallies), the main trend is down. “Risk off” remains the name of the game.

Stocks and Bonds continue to be under pressure and both are trading in intermediate-term downtrends. Although the last days of May have shown some relief (bear market rallies), the main trend is down. “Risk off” remains the name of the game. Where is the bear?

Where is the bear?

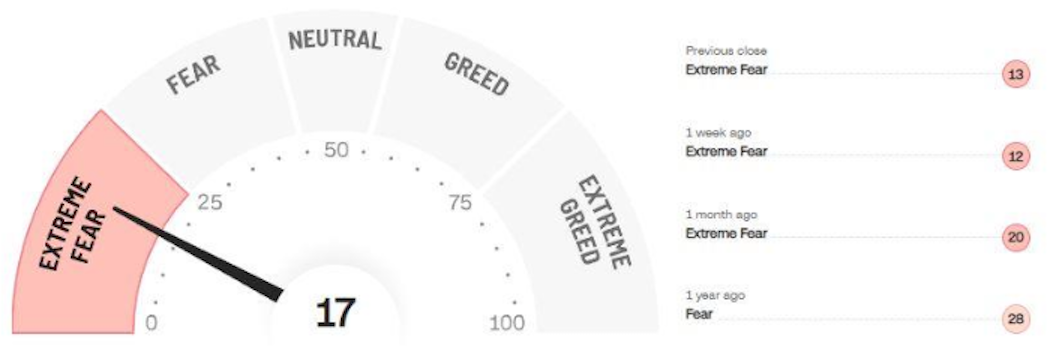

According to many popular sentiment indicators, we are in a period of extreme fear. But despite the sell-off in Bonds, the weak performance in (technology) Stocks, and these bearish sentiment indicators, it does not seem that the market is in panic mode. Buy the dip still seems to be the chosen strategy for investors. Research from Bank of America shows that private clients’ stock market allocation remains close to record highs (at 63%). Capitulation looks different and the short-term fear does not match where investor put their money. There is still a long way toward capitulation. Where is the bear?

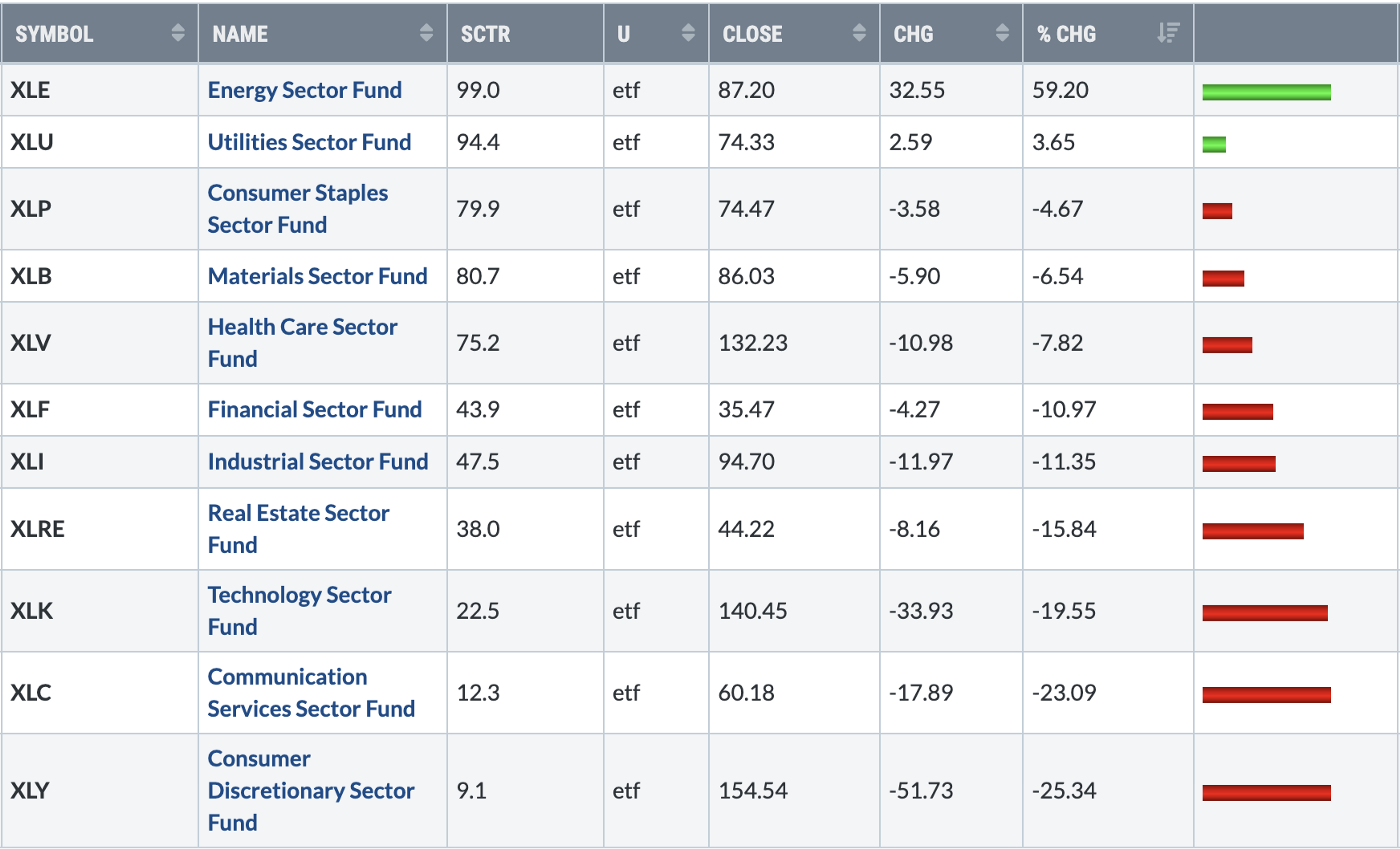

Research from Bank of America shows that private clients’ stock market allocation remains close to record highs (at 63%). Capitulation looks different and the short-term fear does not match where investor put their money. There is still a long way toward capitulation. Where is the bear? Per definition, a bear market starts when an index drops 20% or more. Applying the same logic to sectors, only technology, communication services, and consumer discretionary dropped 20% or more. Energy and Utilities are the positive outliers while all remaining sectors trade -4% to -15%. This also shows that the recent sell-off was more concentrated than broad-based.

Per definition, a bear market starts when an index drops 20% or more. Applying the same logic to sectors, only technology, communication services, and consumer discretionary dropped 20% or more. Energy and Utilities are the positive outliers while all remaining sectors trade -4% to -15%. This also shows that the recent sell-off was more concentrated than broad-based. The Great Rotation

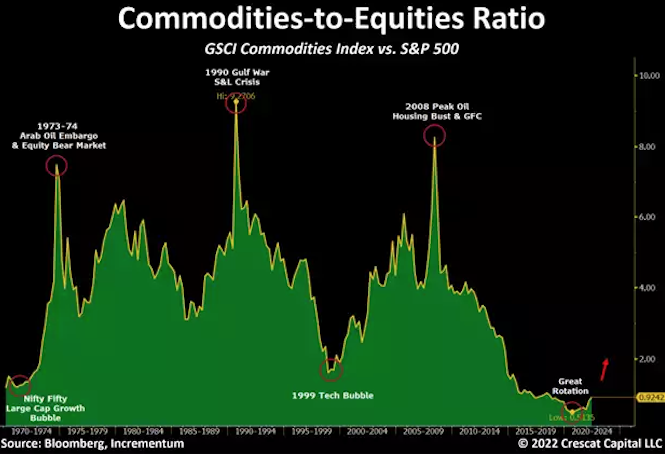

The Great Rotation

One question we hear often is: How much further can Commodities run? Looking at Commodities in comparison to Stocks (GSCI vs. S&P 500$S&P 500(.SPX)$ ), Crescat Capital thinks that it is still very early in the rotation cycle out of overvalued growth equities and low-yielding fixed income securities into commodities. While there remains a lot of downside risk in the broad stock markets, it is important to realize that there is a lot of value, growth, and upside potential in smaller sub-segments, such as commodity producers. Active management should also pay off here. The Global Hiking Cycle is Starting

The Global Hiking Cycle is Starting

Interest rates are rising rapidly in the most widespread tightening of monetary policy for more than two decades, according to the Financial Times. Central banks around the world have announced more than 60 increases in the past three months. This is the largest number since at least the start of 2000.

The recent change in monetary policy comes as inflation has reached multi-decade highs in many countries, fuelled by soaring energy and food costs since Russia invaded Ukraine in February. It is hard to forecast how long this cycle will last. As long as we have rising rates coupled with falling stocks and bonds, capital preservation and capturing trends in alternative assets remain our “risk-off” strategy. Regime Change: 60/40

Regime Change: 60/40

We have been writing about the danger of a traditional 60/40 stocks/bonds portfolio for some time (here). However, we are not alone with this thesis. More and more institutions are starting to rethink their traditional allocations. The latest in the row is KKR.

They just published their paper Regime Change: Enhancing the ‘Traditional’ Portfolio. It suggests enhancing Stocks and Bonds with Real Estate, Infrastructure, and Private Credit. So they transform the 60/40 into a 40/30/30 portfolio. What drives this recommendation? A balanced portfolio should deliver three things:

- Growth (capital appreciation)

- Income

- Diversification

In the current environment, a 60/40 cannot deliver these three requirements anymore. So the shift to a low growth/high inflation environment marks a regime change. According to KKR:

The market is entering a new environment for investing with rising interest rates, higher levels of inflation, and heightened geopolitical risks in combination with slower real economic growth.

After decades of declining interest rates, the trend starts to change (bond yield up, price down)

Stocks seeing signs of turbulence after a decade-long bull market

Public equities yielded negative real returns in inflationary environments, while private real assets have shown higher resilience

We think the message is clear: investors need to do more than simply buy-and-hold Stocks and Bonds. Private assets are great diversifiers (as we argued before here). In addition, this makes also a strong case for trend-following strategies. Not many strategies have been delivering constant returns coupled with exceptional crisis alpha. In markets like these, active management should shine.

https://medium.datadriveninvestor.com/where-is-the-bear-d91d53a435f0

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- hh488·2022-07-01Because most investors have wisen up. Why sell away good shares to opportunistic buyers? After every sharp fall, mkt always rebound strongly.LikeReport

- JohnMitchell·2022-06-29For investors do more day trading if you can. Dont put too much money long or short1Report

- Timothylwong·2022-07-01When will it end1Report

- jojoang·2022-06-30Ogjgkfjfjr1Report

- vic27·2022-06-30here is bear1Report

- WendyDelia·2022-06-29It is already in a bear market1Report

- Veldora·2022-06-29Bear [Spurting]1Report

- ChyeTan·2022-07-01Wow alot of good infoLikeReport

- meltb·2022-07-01Great ariticle, would you like to share it?LikeReport

- Lely84·2022-07-01kill the bearLikeReport

- boonluan·2022-06-30the bear went to hibernation1Report

- 桂圆酱·2022-06-30[微笑] [微笑]LikeReport

- Zhaoxiang·2022-06-30like plsLikeReport

- Masamune891·2022-07-01sheeshLikeReport

- frin·2022-07-01okLikeReport

- jerryteojr·2022-07-01wow interestLikeReport

- BLWM·2022-07-01Buy!LikeReport

- oneXwork·2022-07-01wowLikeReport

- CMY8602·2022-07-01👍LikeReport

- Jialatsia·2022-07-01MeepLikeReport