5 Systemic Alarm Bells You Need To Know As Credit Suisse Fails

Originally posted on thepensivenugget.com

Credit Suisse has failed, and been rescued, over the course of a weekend. While this may have prevented an immediate global banking crisis, danger remains.

Here are five alarm bells that are currently ringing very loudly.

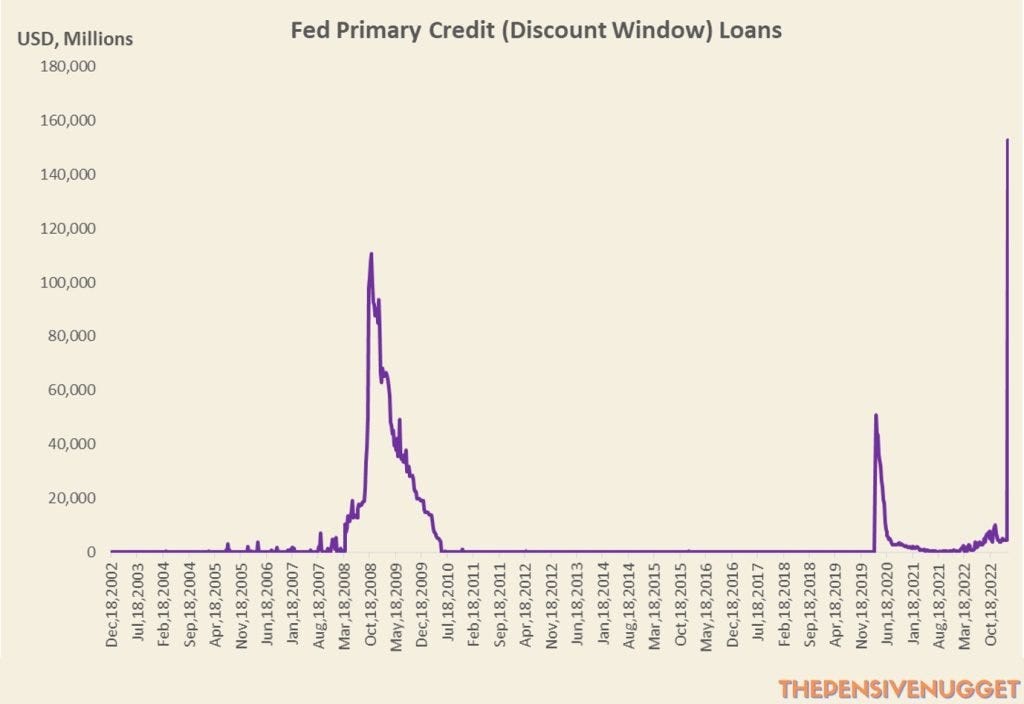

1. Use Of The Fed’s Discount Window Is Through The Roof

The Fed runs an emergency borrowing facility commonly referred to as the “Discount Window” (now formally known as the Primary Credit Facility). It exists primarily to ensure that banks in the US financial system can borrow bank reserves from the Fed in the event of emergencies.

In practical terms, it is the Fed’s lender-of-last-resort facility, and has a reputation of being so. Due to this reputation, a bank tends to only borrow from the facility out of desperation, as being known to have borrowed from the Discount Window casts a large shadow of doubt on its operations.

Since banks run on confidence, they naturally want to avoid situations which would cause their depositors, creditors, and transacting counterparties to question their fidelity. Which means not using the Discount Window unless absolutely necessary.

Note that the largest banks can be an exception to this, especially if they have large trading/dealing operations. During times of crisis, they can sometimes act as intermediaries; by borrowing from the Discount Window to lend at higher rates to smaller banks, pocketing the difference as profit.

As such, the amount of loans borrowed from the Discount Window is an important indicator of demand for emergency funding in the US banking system. The higher its usage, the higher the degree of systemic risk.

As of last Wednesday, the amount that banks have borrowed from the Fed’s discount window hit 152.8 billion, which, as you can see from the chart below, is higher than levels in both 2008 and 2020.

The failure of Silicon Valley Bank, and now Credit Suisse, although Credit Suisse had yet to “officially” fail last Wednesday, is clearly symptomatic of a broader problem — banks are struggling to fund themselves.

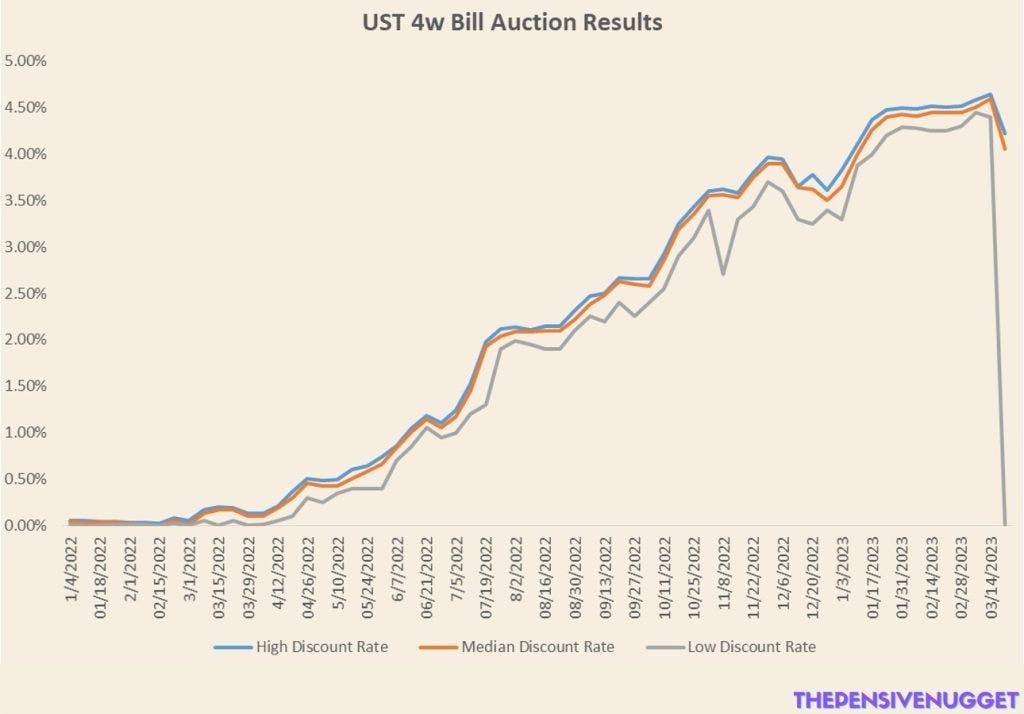

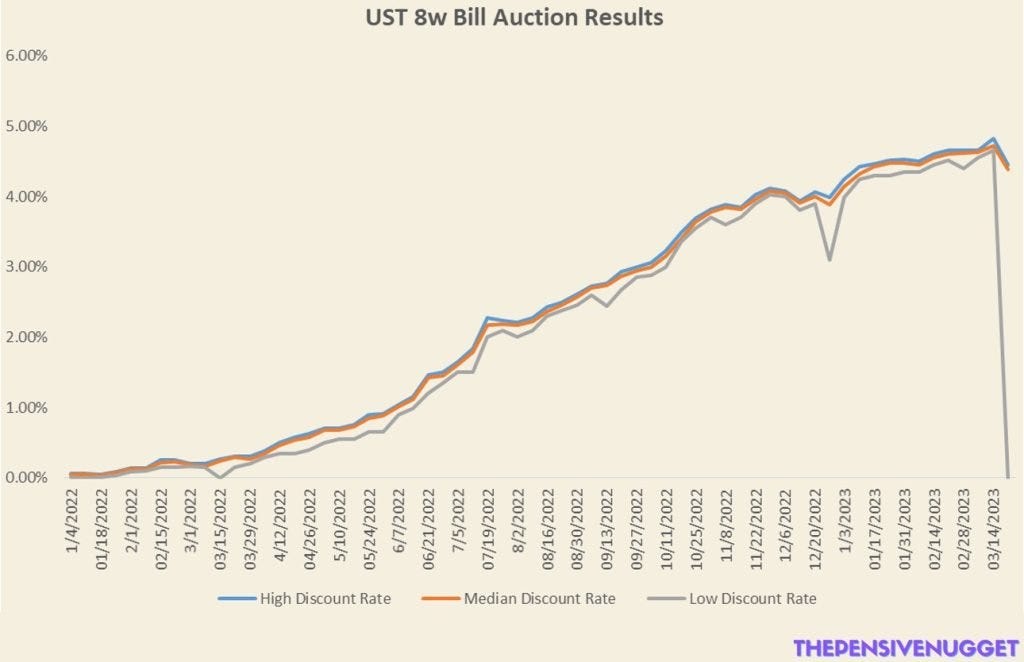

2. 0% Rates Are Making A Comeback

The auctions for 4 week and 8 week US Treasury (UST) Bills held at the end of last week saw the low discount rates for both hit 0%. Note that UST Bills are zero coupon instruments, hence the use of “discount rate” as opposed to “yield”; both terms reflect the rate of interest a buyer earns.

Sharp drop offs in low discount rates at these two auctions show that there are bidders willing to pay more than their peers in order to get their hands on both 4 week and 8 week Bills. Moreover, the 0% low rate also means that these bidders are willing to lend to the US government for no interest.

Why would anyone be so desperate to get their hands on UST Bills?

Quite simply, for use as collateral in the repo market, which implies that this key global funding market is currently under severe strain. As repo is one of the most important, and liquid short term funding markets on the planet, a sharp drop in UST Bill rates, which are the best form of collateral, tells us that a good number of participants are rushing to buy as much collateral as they possibly can.

This could be due to them having an immediate need to meet collateral/margin calls, or that they are stocking up on collateral (UST Bills) in anticipation of the repo market seizing up in the near future. Either way, it speaks to a large negative change in the liquidity of the repo market, that is, people with cash are no longer lending it out easily.

You can learn more about the repo market, and collateral, here, and how low, or zero percent rates do not always mean that money is abundant here.

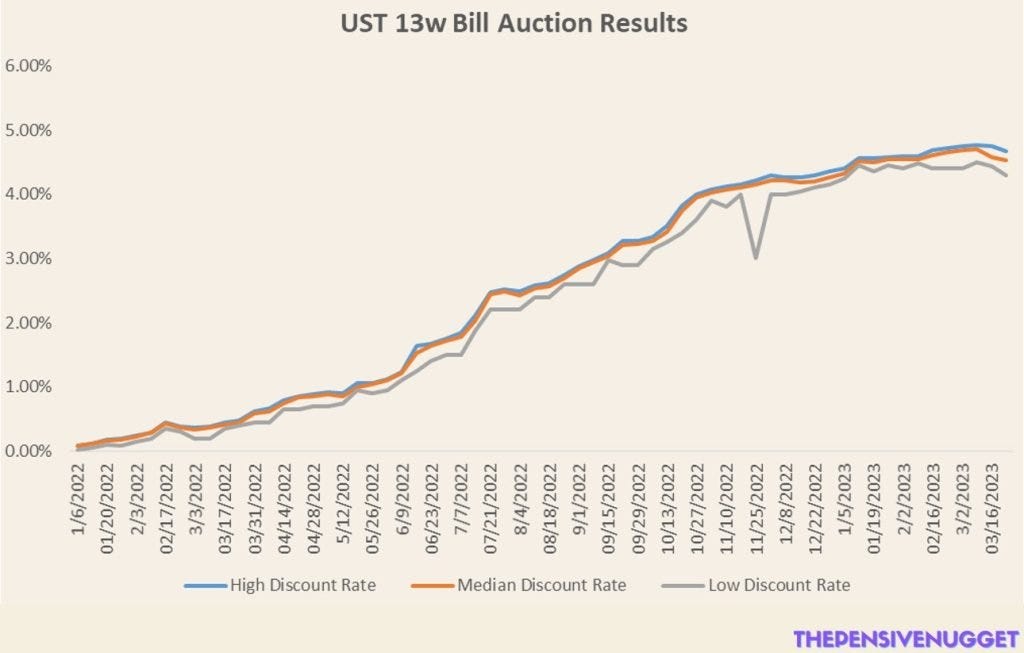

That being said, yesterday’s auction for 13 week Bills did not see a drastic change in its low discount rate. While high, median, and low rates for the auction did come down a little, no sharp drops in the manner of the 4 and 8 week Bills occurred.

Keep a close eye on UST auctions, especially for how low discount rates come in at the short end. As long as they continue to stick at, or close to 0% for the 4 and 8 week Bills, demand for collateral remains high, and by extension, funding markets remain stressed.

Should low discount rates in 13 week Bills plummet towards 0%, that would imply increasing demand for collateral, and hence higher levels of stress in funding markets. This in turn would imply a higher probability of further selloffs in global markets, possibly even violent ones.

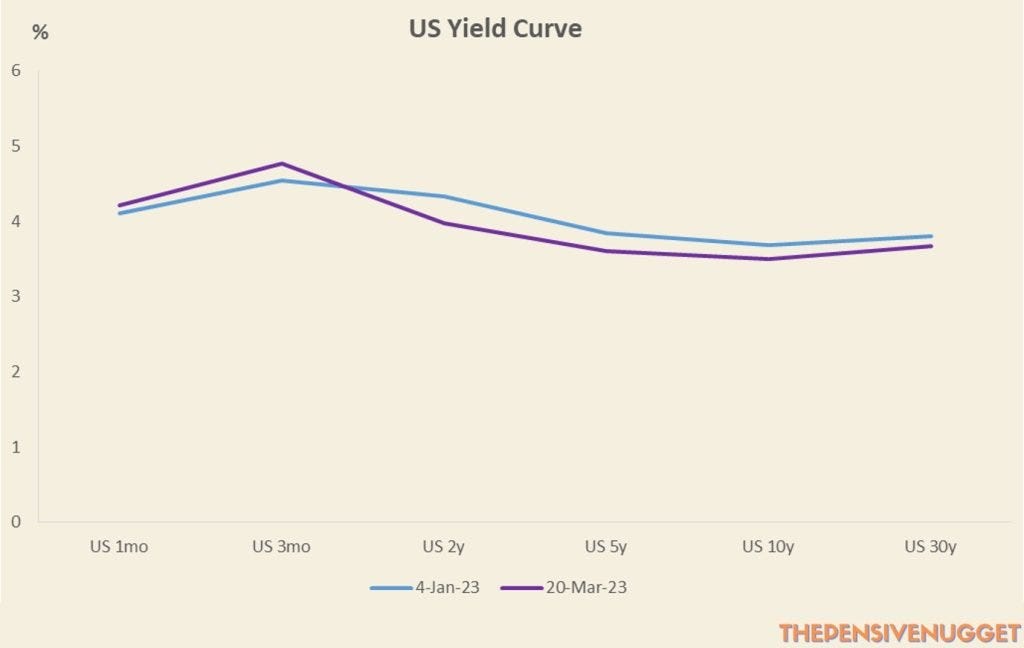

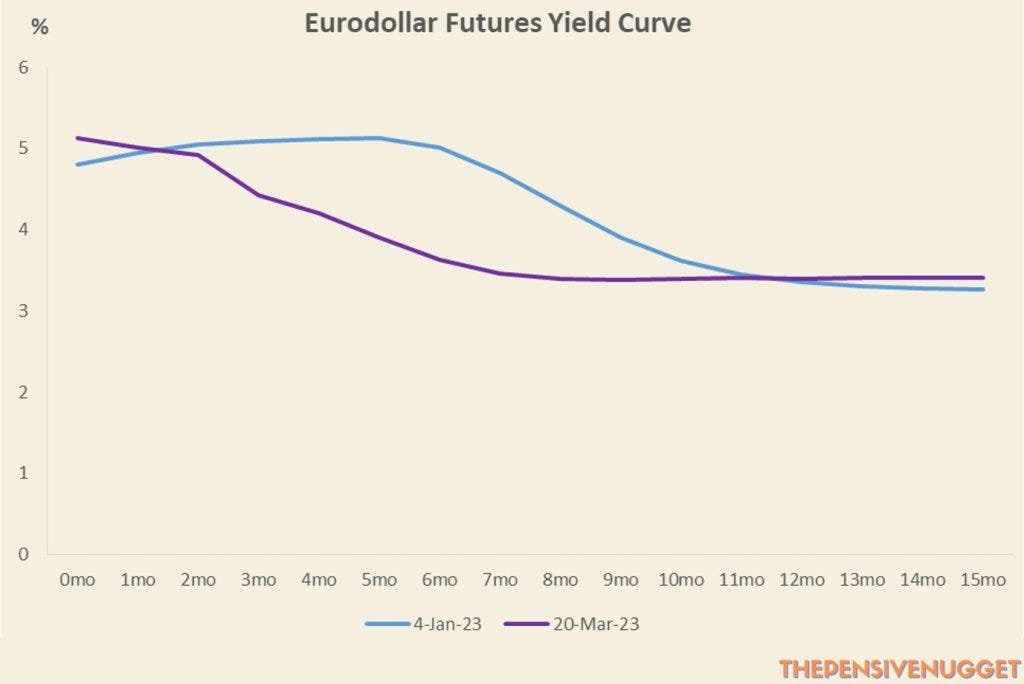

3. Yield Curves Have Spasmed

Both the UST and Eurodollar yield curves have changed dramatically over the past week, and not in a good way.

Looking at the chart of the UST yield curve above, a few things are immediately apparent. Rates from 1 month to 3 month Bills have risen, but yields after that point have fallen. This naturally means that the curve has grown more inverted, especially between the 3 month Bill and 10 year Note.

Higher rates at the short end reflect higher funding costs than in January, although they have fallen quite a bit from where they were just 2 weeks ago, in response to the banking crisis. This fall points towards stresses in funding markets like repo, as explained previously.

On the long end, lower yields are a result of the market quite clearly pricing in lower levels of growth-driven inflation, which really does not bode well for the economy.

The curve has also steepened a little between the 2y and 10y tenors since January, although not by much. While this might seem to be cause for some kind of optimism, since if a flattening curve implies trouble, a steepening one should imply the opposite, this isn’t the case, as a lot depends on other circumstances.

In the current environment, the steepening between the 2y and 10y is largely driven by a sharp fall in 2y yields. This is an occurrence that hints at growing trouble in the financial system, which is an accurate reflection of current circumstances given the failure of Silicon Valley Bank and a few others in the US, and Credit Suisse in Europe. Lower yields at the 2y mark means that the market is pricing in lower rates, which reflects expectations of Fed rate cuts, and/or participants rushing to purchase collateral.

Both of these are reasons which do not translate into economic bullishness.

The Eurodollar yield curve has also shifted drastically from the beginning of the year, reflecting the same reality as the UST one, and is now fully inverted over the next 8 months or so.

This shift indicates a large shift in financial market participants hedging against a sharp fall in rates over the next few months, which implies that they expect more funding stress in repo, Fed rate cuts, and a slowing economy.

4. The Fed’s USD Swap Lines

The Fed announced over the weekend that it would be increasing the frequency of its USD swaps with a handful of other central banks, which is a major sign of stress in global USD funding markets (which are closely tied to collateral and repo).

After all, why make more USDs available to international counterparts if they are plentiful and easily available in the global financial system?

There are some issues here, the first of which is that only a few central banks are involved, whereas the USD is needed globally, especially in China (whose central bank wasn’t included). In order to truly avert a global crisis, Dollars must be made available to every financial system on the planet that transacts in USDs, which in current times is the vast majority of them.

In addition, the Fed making more USD swaps available does not mean that everyone who needs them will get them. Only banks with the needed collateral and creditworthiness will be able to access these USDs from their own domestic central banks.

In turn, only the most creditworthy customers will be able to access these Dollars from the banks who are able to get them in the first place. Bear in mind that the Fed’s USD swap lines are only used in times of global USD scarcity. This means that economic and financial conditions are so poor that banks aren’t willing to step up to make Dollar loans to other banks and their customers. Naturally, in such an environment, banks will only make loans to those which are most likely to pay them back.

Consequently, the Fed making more USDs available to central banks will not avert a crisis. It may help to lessen global bank failures and ease the pressure off the largest businesses, but Dollar swap lines are ultimately a tool that tends to only benefit the strongest entities.

For everyone else in dire need of Dollars, it’s sink or swim. The more who sink, the higher the risk of negative cascading effects on the economy.

Note that the Fed also has a permanent Dollar swap facility for their central bank counterparts, the Foreign and International Monetary Authorities Repo Facility (FIMA), set up in 2021. You can learn more about it, and why it isn’t the solution the Fed believes it to be, here.

5. China Cuts Its RRR

In a surprise move, the People’s Bank Of China (PBOC) cut their reserve requirement ratio (RRR) at the end of last week. Most narratives tend to take RRR cuts as a positive for risk assets, believing them to be expansionary and good for growth.

However, such thinking ignores two very important facts. The first being that bank reserves, whose availability to banks increases when the RRR cut, are not lent out. This necessarily means that RRR cuts (or QE for that matter) are not actually expansionary, since bank reserves do not get pushed out to the broader economy. Banks making new, and more, loans is what matters, and their willingness to do so is not affected by having more bank reserves on their balance sheet.

At best, having more bank reserves available to them means that banks will be more able to meet daily transaction requirements, which could help ease pressure on those which are facing large deposit withdrawals. While this would be helpful in preventing possible bank runs, it isn’t expansionary at all.

Secondly, central banks don’t need to increase levels of bank reserves during good times, simply because the economy is growing, banks are lending freely, and the financial system as a whole is confident. In short, liquidity is plentiful and easily available for anyone needing to borrow.

Liquidity only tightens when financial actors become risk averse and reluctant to lend to counterparties. In other words, the system fails, or at least starts to exhibit signs of failure. This is when central banks step in. When they enact steps like rate cuts, RRR cuts, QE, USD swap lines, or whatever other emergency measures they can conjure, it means that the financial system and broader economy is taking a turn for the worse.

Pay Attention To Macro Markets, Not Equities

While most narratives will be focused on how the equity markets are performing, especially UBS stock, macro markets are the truest indicator of systemic risk.

Keep a close eye on developments in US rates, especially at the front end of the curve, with the understanding that volatility in short term rates is not a good development, even if rates on 1 month and 3 month UST Bills move sharply higher. A healthy rates market is one where movements are relatively small and incremental; large moves demonstrate high levels of uncertainty.

If you can, also pay attention to how Eurodollar futures are performing, as they give meaningful insight into how participants in the global financial system are hedging interest rate risk.

In addition, don’t forget to monitor the USD’s performance in the weeks and months ahead. A stronger Dollar would demonstrate rising scarcity of the world’s reserve currency, which directly translates into banks cutting back on USD lending. Nothing positive happens in the global economy when USDs grow scarce, which is the primary reason for the Fed moving to make its USD swap lines available on a daily basis over the weekend.

Should equities rally while interest rates and the USD continue to trade in a manner indicative of systemic weakness; that is, lower rates, both at the short and long end, and a steady or stronger Dollar, be very wary of narratives proclaiming that the crisis is over.

Finally, it is entirely possible for global markets to calm down substantially in the immediate future, with large rallies in equities and Dollar selling possible. This, however, does not necessarily mean that systemic pressures have been fully alleviated. Crises in global funding markets, like repo, tend to resolve themselves in their own time, more often than not after a massive deleveraging and selloff in markets.

In short, regardless of how positive stocks and the accompanying narratives may or may not be, now is not the time to be complacent.

Do you want to make money trading a crisis? Check out our course on how to do so. And don’t forget to sign up for our FREE course on how to create a trading plan!

5 Systemic Alarm Bells You Need To Know As Credit Suisse Fails was originally published in InsiderFinance Wire on Medium, where people are continuing the conversation by highlighting and responding to this story.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Woww