Affirm: Surprisingly Solid Execution And Undervalued

Affirm (NASDAQ:AFRM) is one of the leaders in the Buy Now Pay Later industry. Customers use a Buy Now Pay Later service in order to spread out the cost for product purchases. Benefits for the customer includeincreased flexibility, control, and simplicity. For merchants, flexible payments mean a greater number of purchases and often a higher average order value (AOV).

Despite it being a competitive industry, Affirm has major partnerships with the likes ofAmazon(AMZN) and Walmart (WMT). Given ~50% of all e-commerce isthroughAmazon, Affirm is in a solid position. Rather than just going for the small merchants, Affirm has gone for the whales. This solid strategy has been the brainchild of founder and CEO Max Levchin a tech icon who was part of the "PayPal mafia" along with Peter Thiel, Reid Hoffman (LinkedIn founder), and Elon Musk.In this post, I'm going to break down the company's solid financial results for the most recent quarter, before calculating its valuation, let's dive in.

Growing Financials

Growing Financials

Affirm generated solid financialresultsfor the first quarter of the fiscal year 2023. Gross Merchandise Volume (GMV) increased by a rapid 62% year over year to $4.4 billion. If we exclude their largest Merchant in the prior year (Peloton) which is struggling currently, then GMV actually increased by 73% year over year. Affirm's GMV growth was driven by strong merchandise sales across large retail merchants in North America. For example, the Affirm platform isusedby the largest brick-and-mortar retail player in the U.S., Walmart. The platform can also be used at Target (TGT), Best Buy (BBY), Nike (NKE), Sony (SONY), and many more retailers. In 2021, Affirm scored a landmark deal with e-commerce giant Amazon to offer Buy Now Pay Later across its gigantic platform. The Travel and ticketing sector was also a key growth driver, with GMV increasing by 90% year over year, however it has declined by 17% since the last quarter due to a normal seasonal decline (end of summer). The sporting goods category underperformed (mainly due to Peloton). In addition, the Home and lifestyle category slowed to 15%, down from 18% year over year.

As a paymentplanprovider, Affirm makes its revenue from a percentage of Gross Merchandise volume which is sold through the platform. In this case, Revenue increased by 34% year over year or 46% if we exclude Peloton to $362 million.

Revenue as a percentage of GMV declined to 8.2% from 9.9% in the prior year. This was mainly driven by the shift to interest-bearing products, which generally recognize revenue over the same period of time as a loan. Funding costs were a headwind in the quarter, due to the rising interest rate environment.

Operating Income (Loss) was negative $287 million, which was worse than the negative $166 million generated in the equivalent quarter of the prior year. Ideally, over time, I would like to see losses narrowing as a portion of revenue, as the company benefits from increasing operating leverage. The good news is on an adjusted basis, operating income has improved its margin from negative 17% to negative 5%. However, this excludes stock-based compensation and non-cash expenses.

Management is seeing leverage on its G&A expenses and S&M expenses, on an adjusted basis. As you can see from the chart below, Sales and Marketing expenses were $41 million and made up 15% of revenue in FYQ1,22. Whereas, by this most recent quarter, its S&M expenses as a portion of revenue has declined to just 7% or $25 million. However, keep in mind this does exclude $100 million in extra expenses related to warrants granted to Amazon in Q4, 2021.

Technology and Data Analytics spending have continued to rise from $51 million to $84 million. Overall I don't believe this is a bad sign as companies that tend to invest more in product and R&Dtendto generate greater shareholder value over time. Also, I imagine the Amazon integration would be a major project, and ensuring this is reliable is vital.

On Affirm's balance sheet, it has Cash and Cash Equivalents of $1.5 billion at the end of the quarter. Its short-term investment portfolio also has $1.2 billion in assets which are available for sale. If I combine these two metrics, we get a total liquidity position of $2.8 billion. Assessing its debt levels is challenging as the company is similar to a bank in that it has many complex loans on its balance sheet. As an indication, the Seeking Alpha Balance sheethighlights~$4.1 billion in total debt, however, I believe not all of this is traditional debt. Details include; $1.7 billion in Convertible Senior Notes which could be called traditional debt. However, the business also has $1.7 billion in Notes issued by Securitization Trusts and $792 million related to funding debt. "Securitization" is the process of packaging up financial instruments such as loans. Therefore, I don't believe this to be "real debt" for the company, as it is related more likely to its consumer loans. For context, Affirm isn'ttechnicallya bank but "rents balance sheet" from its partner banks Celtic Bank and Cross River Bank.

A great way to assess the health of Affirm's Credit Portfolio is to track 30+ day delinquencies. This is the number of customers who have missed payments and are past 30 days due. Generally, during a recession, we would see a spike in 30-day delinquencies (DQ) for most financial companies. In this case, Affirm's portfolio has held up well with its FY 2022 DQ rates (dark grey line) slightly higher than pre-pandemic levels of 2019, and is at ~2.5%. However, there is a slight uptrend which should be noted and monitored, especially as we enter a recessionary environment.

Advanced Valuation

In order to value Affirm, I have plugged the latest financials into my advanced valuation model, which uses the discounted cash flow method of valuation. I have forecasted 30% revenue for next year, as I forecast recessionary headwinds and lower payment volume, as consumers curb spending. However, in years 2 to 5, I have forecasted a 35% per year revenue growth rate, which is the equivalent growth rate achieved in the most recent quarter.

In order to increase the accuracy of the valuation of Affirm, I have capitalized the business R&D expenses. In addition, I have forecasted the company to increase its operating margin to 15% over the next 6 years as the company benefits from increased operating expenses across its Sales, Marketing and G&A expenses.

Given these factors, I get a fair value of $18 per share, the stock is trading at $15 per share at the time of writing and therefore is ~17% undervalued.

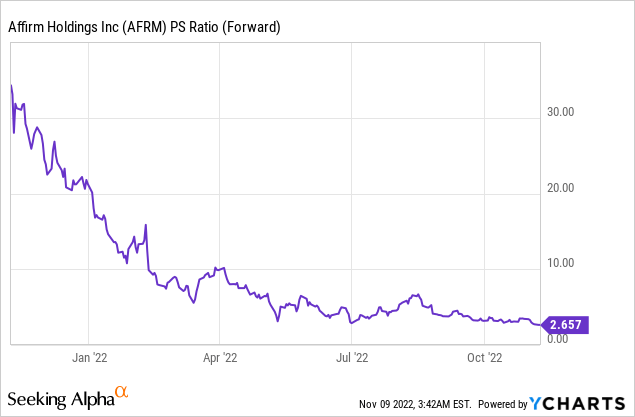

As an extra datapoint, Affirm trades at a Price to Sales ratio = 2.7 which is significantly cheaper than its prior levels of over 30.

Risks Competition

Risks Competition

The buy now pay later industry is heavily saturated. We have Klarna in Europe, Afterpay (recently acquired by Block (SQ)), and even PayPal has launched its own BNPL product. Therefore, it is safe to say that the business doesn't really have a moat or solid barrier to entry. However, in my past posts, I forecasted that the winner's in the BNPL space will be those that scale the fastest and get the biggest partnerships. In this case, Affirm's partnerships with Amazon and Walmart say it all.

Recession/Lower Payment Volume/Loan Risk

As mentioned prior, thehighinflation and rising interest rate environment have caused many analysts toforecasta recession. Recessionary environments tend to cause lower payment volume and a greater number of loan delinquencies. This is a short-term risk for the business, which investors need to be aware of.

Final Thoughts

Affirm is a leading BNPL company that has a strong founder and a number of elite partnerships. The company has grown its revenue strong and is performing well, especially given the macroeconomic environment. I do expect some volatility in the short term and growth rates to dip, due to the "recession". However, longer-term Affirm is poised to be the King of the BNPL industry.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Agree