How to Use Nvidia's Option Income ETF--NVDY?

$NVIDIA Corp(NVDA)$ ‘s earnings surge makes a good time to introduce its special option ETF, $YIELDMAX NVDA OPTION INCOME STRATEGY ETF(NVDY)$

ElevateShares, an asset management company, recently launched several ETFs targeting big-techs in the US market. It is option income-enhancing ETFs, including $YIELDMAX AAPL OPTION INCOME STRATEGY ETF(APLY)$ to $Apple(AAPL)$ , $YIELDMAX TSLA OPTION INCOME STRATEGY ETF(TSLY)$ to $Tesla Motors(TSLA)$ , $YIELDMAX INNOVATION OPTION INCOME STRATEGY ETF(OARK)$ to $ARK Innovation ETF(ARKK)$ and $YIELDMAX NVDA OPTION INCOME STRATEGY ETF(NVDY)$ to $NVIDIA Corp(NVDA)$

ETFs are publicly traded funds on the market, read their prospectus is necessary.

What is an option income ETF?

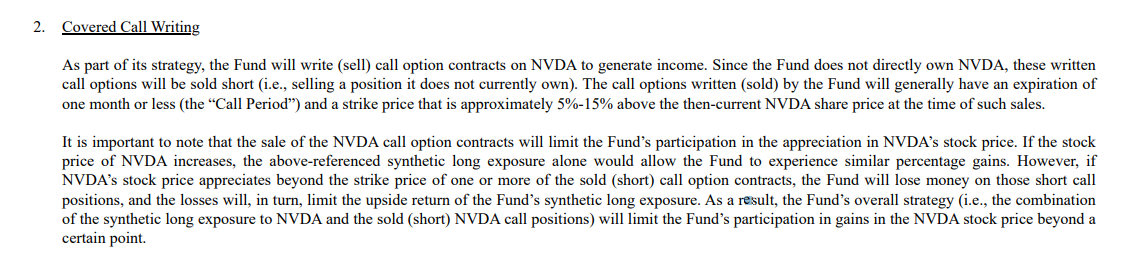

The ElevateShares' option income-enhancing fund for Nvidia stock is an actively managed fund that generates monthly income by selling NVDA call options ("covered call" strategy). Although the fund does not directly invest in NVDA, its intention is to attract investors by pursuing similar returns as underlying stocks through strategies while generating additional revenue.

This particular ETF provides investors with two sources of return: net asset value changes and premium income from selling options plus interest earned from cash invested in short-term government bonds.

What is its options strategy?

Covered calls.

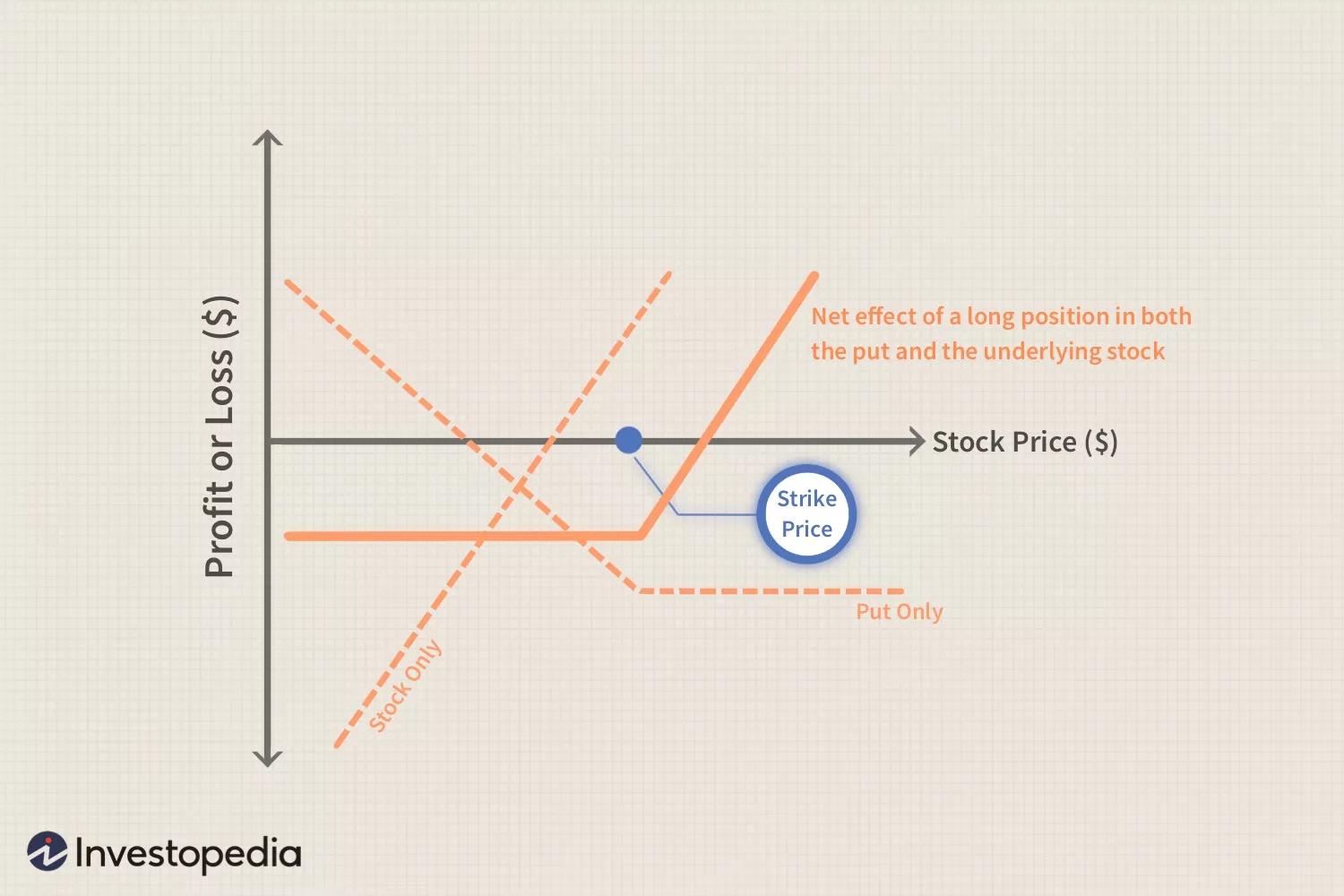

Traditional covered calls involve buying shares of stock and then selling equivalent positions of out-of-the-money call options. However, this particular ETF uses synthetic covered calls instead.

This means they do not purchase actual shares but rather buy at-the-money call options while simultaneously selling at-the-money put options to create a simulated long position. They also sell equivalent positions of out-of-the-money call options.

The benefit of synthetic covered calls mainly lies in reducing capital requirements; however, the synthetic position may experience greater volatility.

Since this ETF aims to generate additional income, the saved capital can be used to purchase short-term government bonds (such as US Treasury 3 Month Bill ETF (TBIL) and iShares 0-3 Month Treasury Bond ETF(SGOV)) for extra returns. Nvidia also regularly distributes these additional cash earnings.

What is the risk of covered calls?

Nvidia announced a strong Q1 financial report that caused its stock price to surge by 24%, reaching an all-time high. This is last thing what NVDY's managers want to see.

The biggest risk for covered calls is not necessarily a drop in underlying asset prices because even with some loss, they can still outperform underlying assets due to their call option premiums. The real problem lies when underlying assets rise significantly beyond the strike price of sold call options; this means that this strategy cannot benefit from further gains.

We found that Covered CALL prices are about 5-15% higher than ATM Call prices among NVDY's top ten holdings. Currently, the highest Covered CALL price is only $335 compared to NVDA's post-market price of $385 - a difference of $50!

In other words, if Nvidia's stock jumps more than 15%, then this strategy will not keep up with it. Most of NVDY’s Underlying assets price are between $285 to $300, makes it harder to benefit from the surge.

Even buying higher-priced Calls on May 25th would have been futile in hedging against such risks.

Is there arbitrage opportunity in NVDY's?

In theory, yes! According to NVDY’s prospectus, its covered options can only cover situations where Nvidia rises less than or equal to 15%. Therefore any increase above that level will not be reflected in NVDY’s net value growth rate.

However, after-hours trading saw NVDY follow NVDA and rise nearly by almost 26% ($26). In theory, its net value should only be around $24, which means there is a premium of $2.

If NVDY has enough liquidity, then in the long run, its net asset value will not maintain a premium of more than 10%. Without off-market arbitrage opportunities, investors can use an equal position to buy NVDA stocks and short NVDY to achieve arbitrage.

However, liquidity is also a significant issue. Emerging ETFs often lack sufficient trading volume and may experience prolonged premiums.

What does that mean to investors?

Firstly, it must be said that covered calls are undoubtedly a good strategy. In most cases, they generate returns higher than holding actual shares. The reason why this asset management company dares to promote such an ETF is that they believe long-term returns can beat low-probability events; furthermore, they have done extensive backtesting to prove that this strategy works effectively.

Secondly, synthetic covered calls are even better in high-interest rate environments because they reduce capital requirements while generating additional income. Currently US short-term bond rates exceed 4% annually - definitely worth considering!

Furthermore, after the small probability event of Nvidia's surge of more than 15%, the tail risk of this kind of small probability event happening again has actually decreased, and covered call strategy can be arranged.

After all, Nvidia's bulls must also be happy to see another post-market surge of 15%.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Many EV and AI Sector stock Investors Ignoring the Noise and Filling the Dips in Tsla and others in May for Life- changing Future Gains.

Ford has sold a handful of mach-e’s, so tesla should come out great on the deal.

Why do emerging ETFs often lack sufficient trading volume and experience prolonged premiums? 🤔

How can investors use an equal position to buy NVDA stocks and short NVDY to achieve arbitrage?

Will NVDY's net asset value maintain a premium of more than 10% in the long run?