Why Luckin Still Has 42% Upside Potential?

Beverage industry in China is undoubtedly thriving, and in this environment, the Q2 earnings of $Luckin Coffee Inc.(LKNCY)$ surprisingly achieved a record-breaking profit.

Despite the scandal of falsifying financial data two years ago, the company has moved from the main board to the OTC market and settled legal disputes. However, it still lacks coverage from mainstream investment banks. As a result, Luckin can only compare its performance against its own past achievements, as there are no "market expectations" to be compared with.

In the past year, growth stocks have faced immense pressure, especially in the restaurant industry, which has been struggling. Surviving the pandemic period was already commendable, not to mention facing massive market competition. Therefore, Luckin's high growth rate has become a driving force for continuous investor interest.

After the Q2 financial report was released on August 1st, the company's stock price soared by nearly 14%, bringing its total market value to $9.589 billion, reaching 75% of the peak market value of $12.9 billion on January 17, 2020. However, judging from the current valuation level, Luckin still has a 42% upside potential.

What makes Q2 so extraordinary?

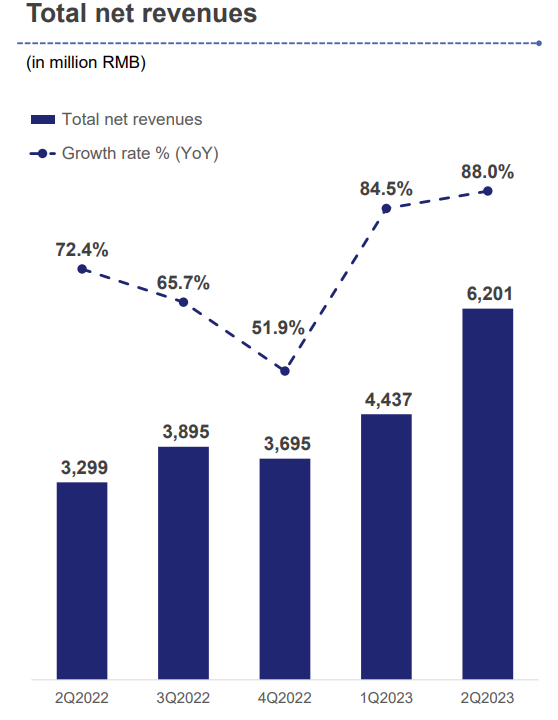

the company's revenue reached CNY 6.201 billion, a year-on-year increase of 88.0%. Among this, revenue from self-operated stores was CNY 4.495 billion, up 85.2% year-on-year, and revenue from franchised stores was CNY 1.486 billion, up 91.1% year-on-year.

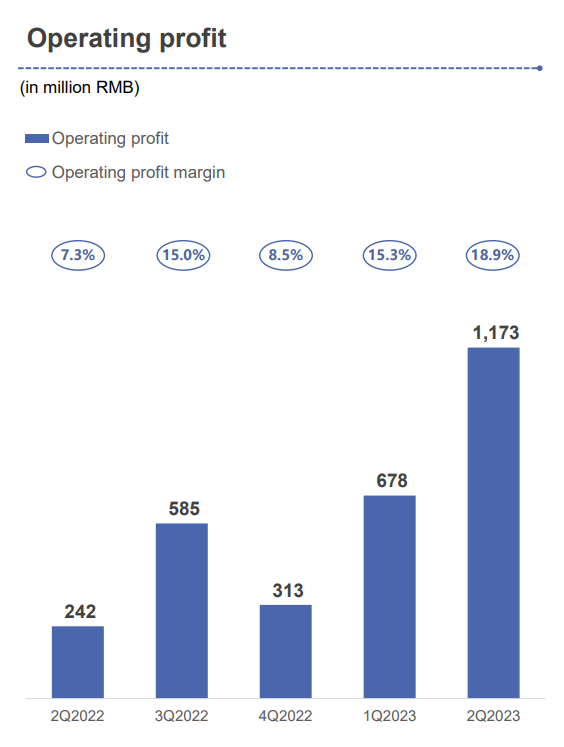

The net profit was CNY 998.7 million, compared to a loss of CNY 114.7 million in the same period last year. GAAP operating profit was CNY 1.173 billion, a significant increase of 385% year-on-year, with a profit margin of 18.9%, significantly improved from 7.3% in the same period last year.

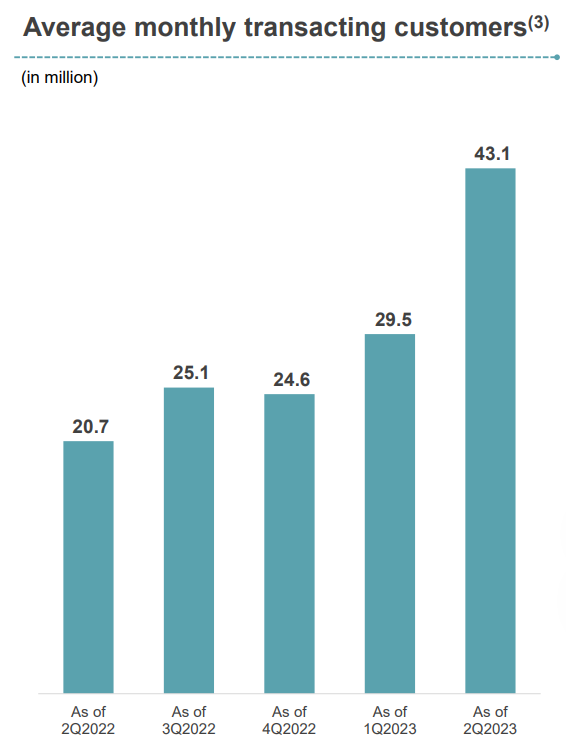

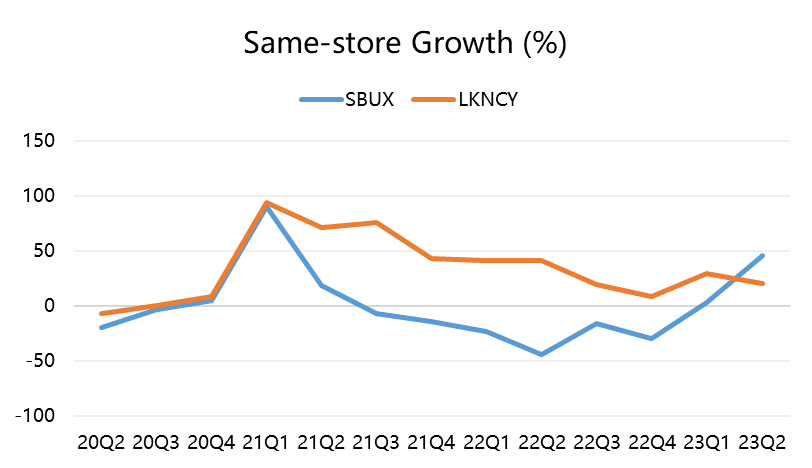

The same-store sales growth of self-operated stores was 20.8%, slightly lower than the 41.2% in the previous year, but still outstanding. The average monthly transactional customers increased by 107.9% year-on-year, reaching 43.1 million.

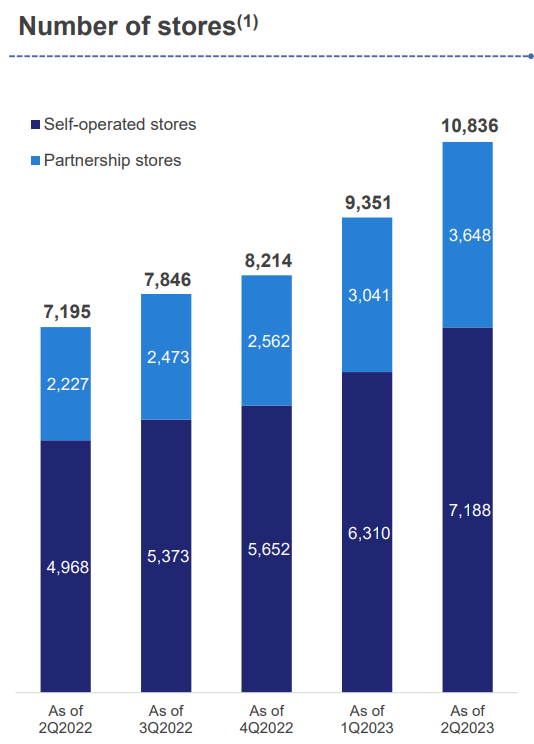

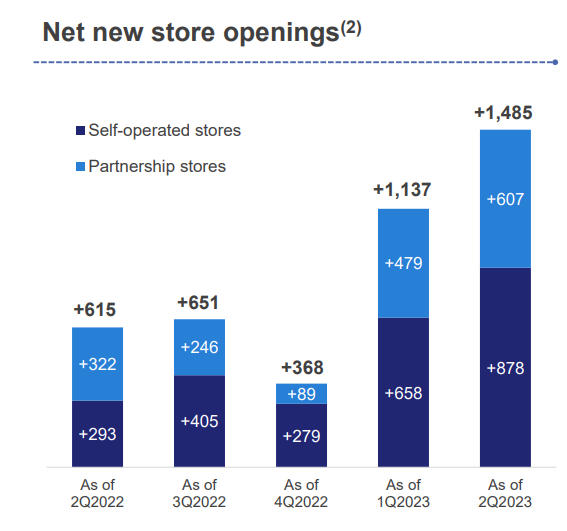

A total of 1,485 new stores were opened, including 5 in Singapore, with a quarter-on-quarter growth rate of 15.9%.

As of the end of the second quarter, the total number of stores was 10,836, including 7,188 self-operated stores and 3,648 franchised stores.

Why does Luckin Coffee seem similar to $Pinduoduo Inc.(PDD)$?

The company's continuous expansion of new stores has been driving its growth. Luckin already boasts an impressive number of over 10,000 stores, a remarkable achievement for a chain enterprise.

While the year-on-year growth may be due to a low base effect last year, the surge of over 40% in revenue from the previous quarter is the result of new store openings after the pandemic. Self-operated stores still account for a larger proportion, but franchised stores have shown greater growth both on a quarter-on-quarter and year-on-year basis.

After surpassing the ten-thousand-store milestone, the potential for growth through "newly added stores" may be limited, and the company might focus more on same-store growth. This could involve promoting sales through promotional activities and then adjusting pricing strategies to improve marginal income.

The "price war" dominated Q2. With the aggressive low-price strategy of "Cotti Coffee" by one of the co-founders, Lu Zhengyao, Luckin was initially thought to be significantly impacted. However, even with the introduction of 9.9 yuan coupons, and the number of paid users surpassing 50 million in June, the same-store sales growth rate reached 20.8%, and the store profit margin reached 29.1%, both returning to the levels of Q3 2022.

Comparing this with $Starbucks(SBUX)$ ' performance in recent quarters, although Starbucks achieved a same-store growth of 46% in the just-concluded Q2, it relied heavily on price promotions, resulting in a decline in the average ticket. This also confirms the fierce competition in the domestic beverage industry.

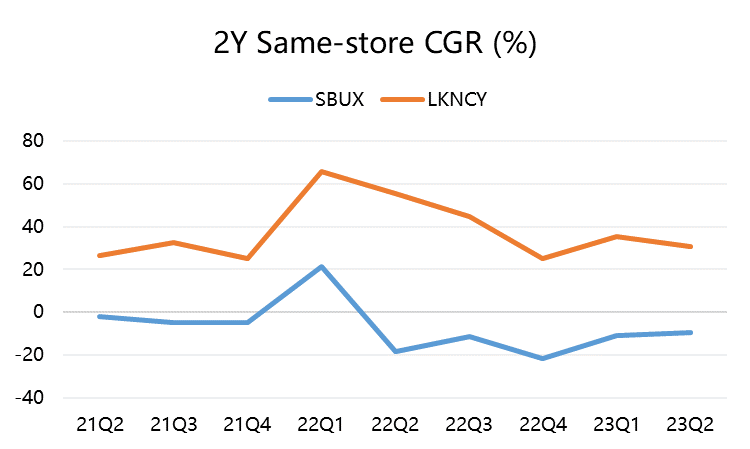

If we compare the two-year compound growth rates, Luckin Coffee's same-store growth has consistently outperformed Starbucks by a significant margin.

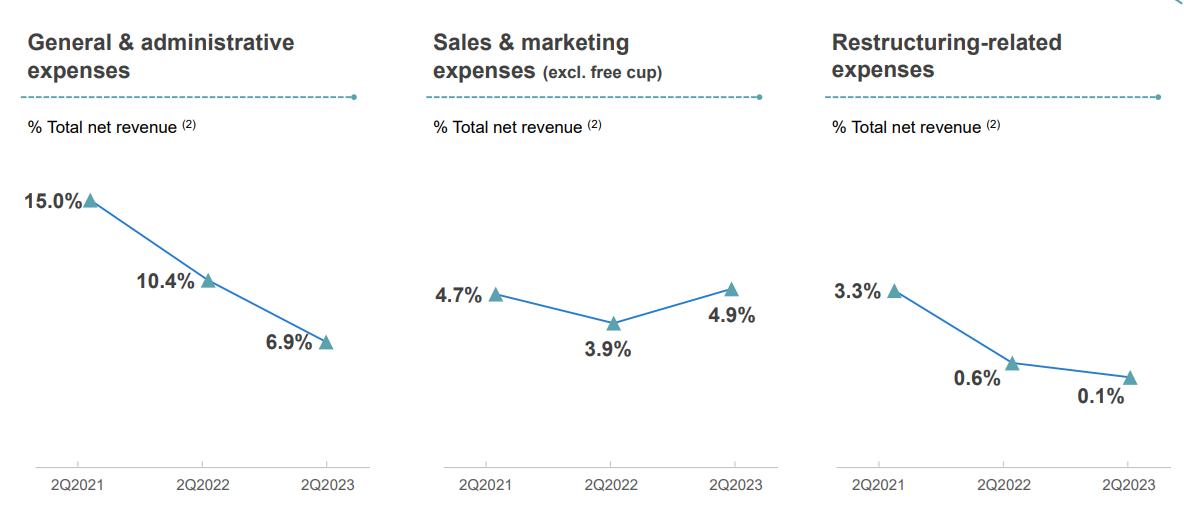

In terms of the management approach, Luckin shares some similarities with "profitable Pinduoduo." With economies of scale, cost reduction, increasing marginal income, and a gradual decrease in restructuring costs, the company has achieved a "leap" in profit margins this quarter.

The general management expense ratio improved by 3.5 percentage points year-on-year, but the market expenses still remain relatively high. If Luckin can build brand appeal similar to Starbucks and create customer loyalty, the pressure on marketing expenses may be alleviated. However, if the "price war" continues unabated, controlling marketing expenses might be challenging in the short term.

At present, Luckin has captured a significant portion of the coffee market priced below 20 yuan, but whether it can further challenge Starbucks' price range through new products will depend on market demand, brand influence, and market entry timing.

Why Luckin still has a 42% upside potential?

In comparison, Starbucks, which just released its financial report, currently has a TTM dynamic price-to-earnings ratio of 30.7 times, a forward PE of 29 times for the 2023 fiscal year, and an estimated PE of 24.8 times for the 2024 fiscal year, which is slightly higher than the overall average of the US restaurant industry.

Looking at the EV/EBITDA, Starbucks' expected EV/EBITDA ratio at the end of 2023 is 19.8 times, and 16.7 times for 2024. Luckin's trailing twelve months' EV/EBITDA is also 19.8 times.

However, considering its much faster revenue and profit growth compared to Starbucks, Luckin's valuation increase should at least reflect its EBITDA growth relative to Starbucks.

If we consider an EV/EBITDA of around 18 times for 2024, based on Luckin's current revenue level, assuming a growth rate of 20% in 2024 and a profit margin of around 18%, the share price could reach $47, still providing a 42% upside potential.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Great company. Combined with strong growth, many scaling effects are a great advantage now and in the future! In the long run, the share price will be 3 to 8 times higher...

After reviewing them in detail, the numbers on the earning release are REALLY strong. Not only did they show solid growth, but were able to do so with very positive profitability numbers, amazing same sales growth, and excellent free cash flow.

There will be profit taking ? normal for people that are a little insecure or get their money back ! Investors will be holding this cup🤎☕

LKNCY is a rocket that got re-fueled and re-launched. Any pullback now is a STRONG BUY.🍻🍻🍻

There are a lot of Coffe companies in China, LK will be # ☕🤎1