Can Amazon's Q2 Earning Be The Savior?

$Amazon.com(AMZN)$ Q2 earnings seems truly remarkable, making a big splash.

Summary

Core e-commerce business performed exceptionally well despite the inflationary environment, surpassing market expectations and regaining growth momentum. Particularly noteworthy was the impressive performance of the third-party retail segment, which shone even brighter after price adjustments, and the offline stores crossed the $5 billion mark for the first time.

Similar to $Alphabet(GOOG)$ and $Meta Platforms, Inc.(META)$ , Amazon's advertising business also performed exceptionally well, exceeding expectations and surpassing $100 billion in revenue for the first time, becoming the fastest-growing segment among its major businesses.

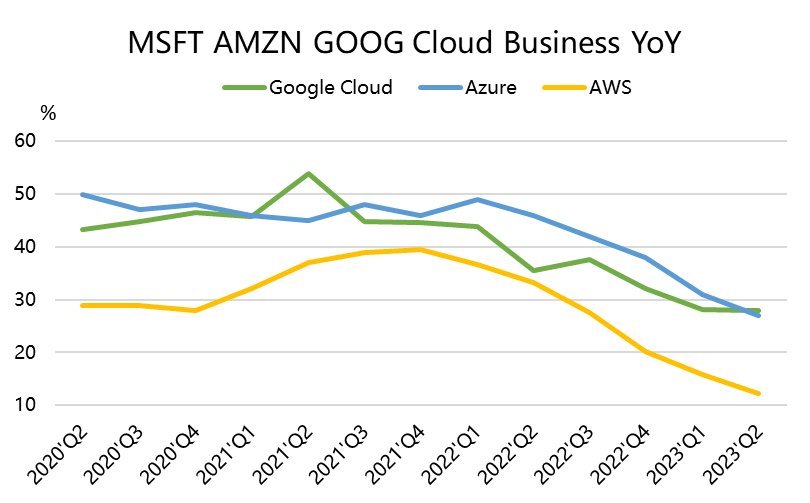

The growth rate of AWS cloud services continued to decline, in line with the trend seen in $Microsoft(MSFT)$ , but it still maintains its position as the market leader. In the AI era, Amazon places great importance on data, and AWS is becoming an essential foundation.

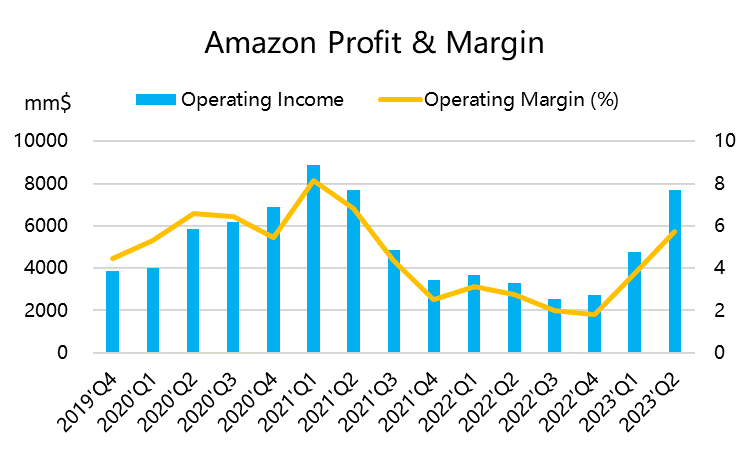

As different business segments experienced varying growth rates, the gross profit margin increased significantly. Moreover, cost-cutting measures have shown effectiveness, with the operating profit margin returning to 5.7% after seven quarters, providing a basis for further improvement in future profit margins.

The market had previously incorporated strong recession expectations, fearing that inflation might significantly impact Amazon's performance. However, these concerns proved to be somewhat excessive, and the company's strong Q3 performance guidance further demonstrated the continued recovery of its retail business, enhancing its valuation.

Financial Highlights

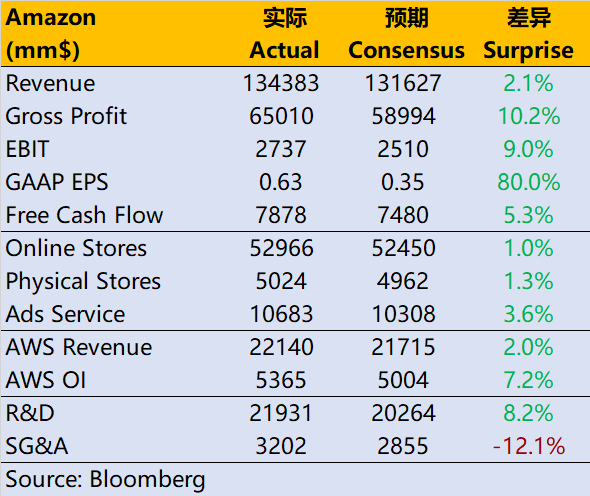

- Total revenue: $134.38 billion, exceeding market expectations of $131.63 billion (11% YoY growth).

- E-commerce revenue breakdown:

- Online store revenue: $52.97 billion (4.2% YoY growth).

- Physical store revenue: $5.02 billion (6.4% YoY growth).

- Third-party seller services revenue: $32.33 billion (18% YoY growth).

- Subscription services revenue: $9.89 billion (14% YoY growth).

- Advertising revenue: $10.68 billion (22% YoY growth).

- AWS revenue: $22.14 billion (12% YoY growth).

- Gross profit : $65 billion (margin 48.38%).

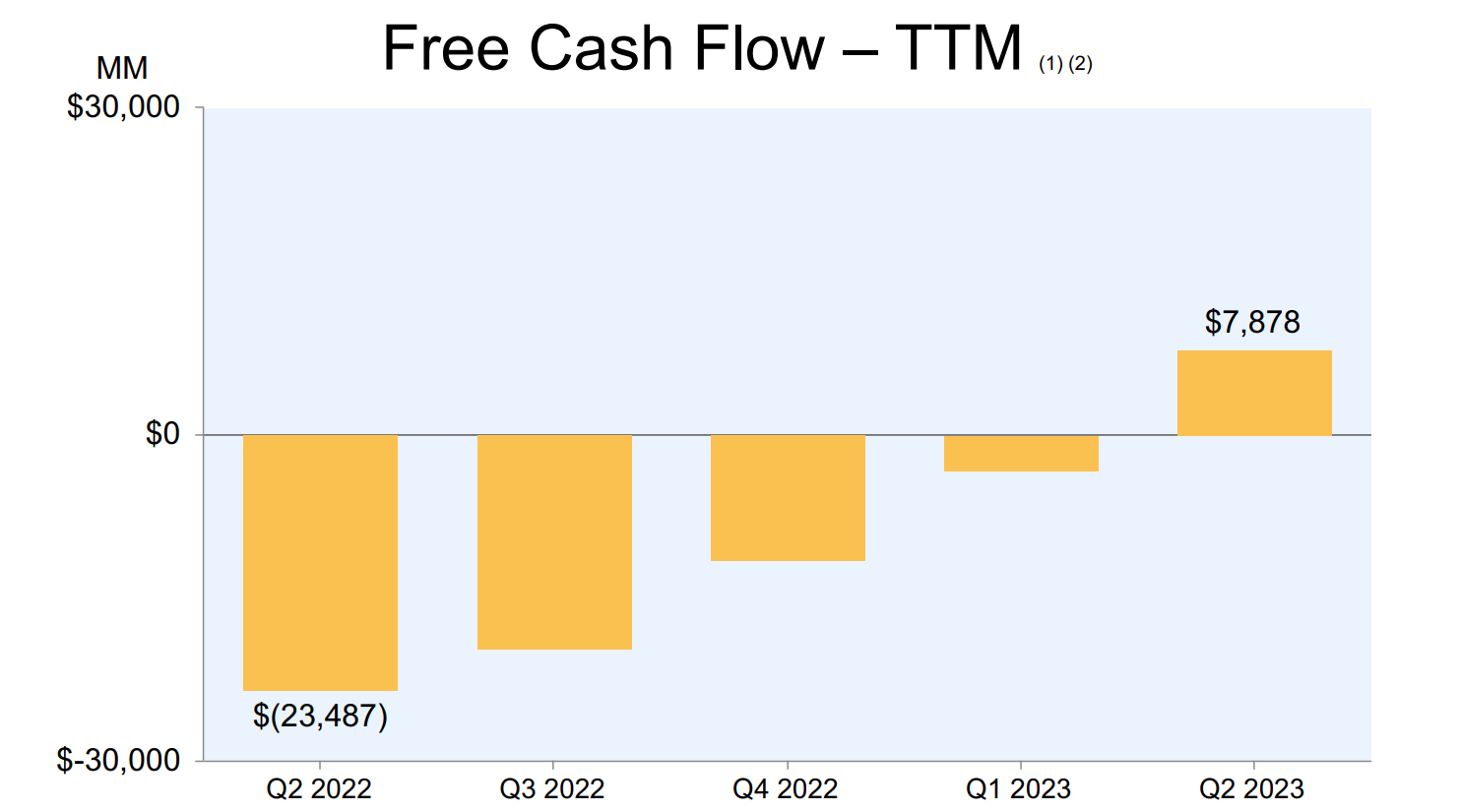

- Operating profit: $7.68 billion (margin 5.7%).

Looking ahead, Amazon projects Q3 revenue to be between $138 billion and $143 billion, surpassing the consensus estimate of $138.3 billion. Operating profit is expected to be between $5.5 billion and $8.5 billion, exceeding the consensus estimate of $5.4 billion.

Investment Highlights

Overlooked retail business. Amazon's main online store experienced a decline in four out of the past five quarters, but in Q2, the growth rate rebounded, and the offline store growth remained in the mid-single digits.

The most eye-catching aspect is the revenue from third-party merchant services, which is a result of its price increases and also demonstrates that there is currently no other highly active app competing in the retail business. Even TikTok, a popular short video platform, still faces challenges in converting its traffic into e-commerce revenue in the North American region. Additionally, the advantage of Prime membership further enhances Amazon's online retail dominance.

In another survey focusing on online retail

Among those subscribed to Prime, 11.8% found it difficult or very difficult to cancel their subscriptions. Furthermore, only about one-third of former Prime users said they intentionally subscribed to Prime, which is positive from a company perspective, but it also raises concerns about potential future legal disputes and antitrust issues.

Amazon and Walmart are the only regular shopping platforms, while the rest are more likely to have respondents who make occasional and irregular purchases.

Occasional shopping platforms often require specific triggers. For example, $Etsy(ETSY)$ shoppers mention handmade or personalized items, jewelry, or custom-made products; $Wayfair(W)$ customers mention furniture or home goods; Temu $Pinduoduo Inc.(PDD)$ customers are seeking affordable items, while Shein customers are interested in clothing or inexpensive goods.

This suggests that users' shopping habits are relatively stable, and they form inherent impressions of a platform, which determines its growth ceiling. As a comprehensive shopping platform, Amazon's scale advantage is also more prominent.

As inflation begins to slow down, retail platform activity is expected to increase again. This is one of the important reasons why Amazon is boldly raising its Q3 performance guidance. The company's recent activities, including Prime Day, have further confirmed this trend.

The ignored Aadvertising business. This quarter, advertising showed the highest incremental growth among all businesses, with a single-quarter revenue of $10 billion. Advertising has become a driving factor for future growth, with revenue improving sequentially for several quarters.

However, it is not clear if Q2's rebound signifies a new trend, but at least it did not follow the decline seen in Q1.

Currently, Amazon's online advertising has become a profitable business, accounting for approximately 7.3% of the global digital advertising market. This further confirms that economic activity is stronger than expected. The company's robust demand for advertising services allows advertisers to customize ad placements and create interactive experiences for consumers.

The favorable aspect is that the high-profit margin of the advertising business contributes to the overall profitability of the company. However, the potential risk lies in the high monetization rate of commission advertising. The future incremental growth may still come from the overall advertising business, which can be cyclical.

Cloud services are entering a mature stage, and profit indicators will become crucial. Q2's AWS revenue growth was only 12%, returning to the level seen in 2015. While its growth rate lags behind Google's, it remains in line with Microsoft's trend. Although AWS continues to dominate the market, its massive scale also indicates that it is entering a mature stage, and future profit margins in the cloud business will be critical for evaluation.

In this quarter's financial report, the market did not focus too much on the deceleration of the cloud business, as future AI needs are expected to contribute positively.

There is still room for cost reduction and efficiency improvement. The continuous decline in operating profit over the past two years has been a significant factor constraining Amazon's stock price, making it one of the least impressive performers among major tech companies.

Q2's profit margin returned to 5.7% after four quarters, nearing the level of mid-2021. With further improvements in cost reduction and efficiency, the company sees more opportunities to enhance cost efficiency in the future.

Meanwhile, capital expenditures decreased by 27% YoY to $11.6 billion, mainly due to a YoY decline in transportation capital. This indicates that its logistics chain is currently maturing, and more investments will be directed towards AWS and AI-related endeavors.

Regarding AI, Amazon believes that data is the core of artificial intelligence. Large-scale language models in generative AI have three crucial levels, and AWS is heavily investing in them. The bottom level involves training basic models and performing computations required for inference or prediction, and the supply in the market is scarce. The middle level focuses on services with large language models. Developing these models requires billions of dollars and several years, which most companies prefer not to invest in and instead want access to these models to customize them with their own data—this is where AWS finds its opportunity.

Although Amazon is still in the very early stages of adopting and successfully using generative AI, consumer applications are just one layer of the opportunity.

Conclusion

Amazon's Q2 performance marks the beginning of a new era, and the market's almost 10% after-hours surge is well deserved.

With a strong retail business, incremental growth in advertising, and a solid foundation for cloud services in the AI era, Amazon is poised to improve its profitability and valuation. Additionally, Amazon's performance serves as a reliable indicator of economic trends.

At the current dynamic P/E ratio of 80, there is potential for the stock to return to around 30 times earnings in 2024.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

I brought Amazon at $142 any chance it will go back up. I can’t afford to lose my rent money. Every stock analyst on the planet told me I should invest my money in that company and I did, now I’m in fear of it dropping drastically.

Amazon has the ability to become a two trillion dollar company by end of year. Believe it or not Jassy has the ability to move Amazon into the stratosphere and the products and services to do that. Also don’t be surprised if they do a second prime day for the holidays since they killed the first one of the year.

Maybe its time for AMZN to shine we been waiting a log time