Disney's Losing Subs Again, Is Time To Bet On Bob Iger?

$Walt Disney(DIS)$ released its Q3 earnings, showing a rebound in overall revenue, although it remains below expectations.

The subscription count for its streaming service has once again declined, while the year-over-year losses have continued, albeit with a slight reduction in the extent of the losses.

Simultaneously, the offline theme parks have experienced a significant year-on-year increase, benefiting from the recovery in the Chinese market and poised to set a historical high.

However, the company's stock experienced fluctuations after trading hours, primarily due to news of a price increase for its streaming service.

Q3 Earnings Overviews

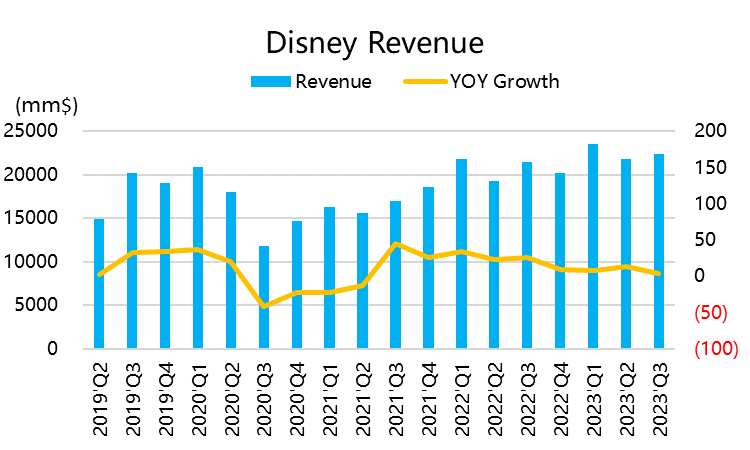

-Revenue reached $22.33 billion, marking a 4% year-on-year growth, which falls short of the market's expected $22.53 billion.

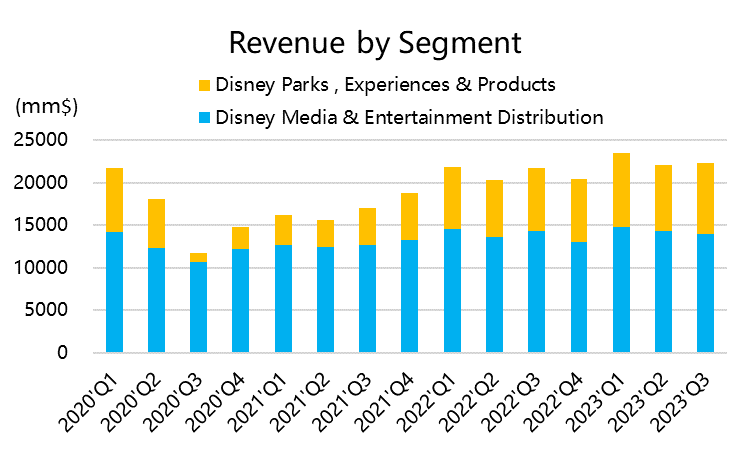

-Breaking down the segments, Media and Entertainment revenue was $14 billion, a 1% decline year-on-year, below the anticipated $14.3 billion. Meanwhile, Parks, Experiences, and Products revenue reached $8.33 billion, a 13% increase year-on-year, surpassing the market's expected $8.24 billion.

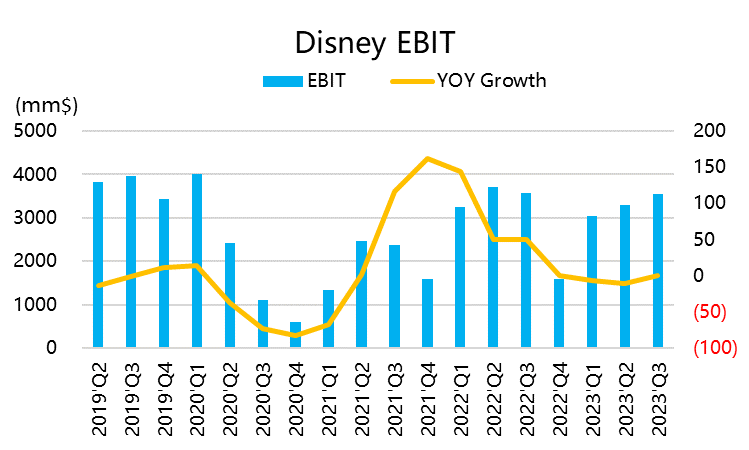

-In terms of operating profit, the overall adjusted EBIT was $3.56 billion, surpassing the anticipated $3.4 billion. The adjusted EPS also decreased to $1.03, but it exceeded the market's expected $0.97.

-Disney Media and Entertainment garnered $1.13 billion, down 18% year-on-year, yet exceeding the expected $1.05 billion. Disney Parks, Experiences, and Products profit reached $2.43 billion, a growth of 11% year-on-year, surpassing the expected $2.3 billion.

-Disney's theme park division has consistently witnessed double-digit revenue and operating profit growth, while Media and Entertainment have experienced contraction. This consensus is attributed to the company's cost-cutting measures.

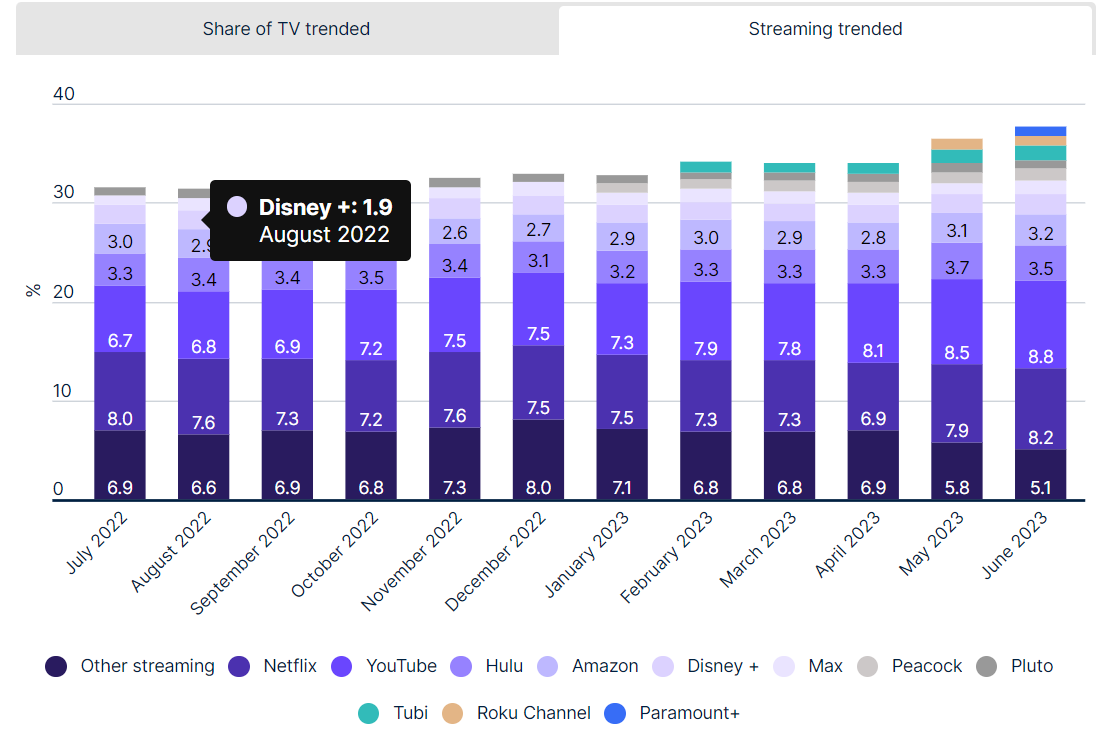

-The company's operational metrics for this quarter were somewhat disappointing, with Disney+ streaming subscriptions decreasing to 146.1 million, significantly below the expected 154.8 million. This marks the third consecutive quarter of decline. Among these figures, the core membership of Disney+ grew by 1% to 105.7 million, while Hotstar's subscribers dropped by 24% to 40.4 million. The streaming service ESPN+ of ESPN, Disney's largest division, maintained stability at 25.2 million subscribers, albeit falling short of the expected 25.8 million. Hulu's subscription count was at 48.3 million, below the anticipated 48.7 million.

Investment Highlights

Under Bob Iger's leadership, one of the key focuses has been the strategic optimization of streaming services to cut costs and enhance efficiency. As he articulated, the primary objectives have revolved around restructuring the company, bolstering operational efficiency, and reinvigorating creativity at the core of our endeavors. The company not only surpassed its initial target of saving $5.5 billion but also managed to elevate our DTC (Direct-to-Consumer) business revenue by approximately $1 billion over three quarters.

Although there has been a decline in streaming subscriptions, the momentum of price hikes remains unaltered. The ad-free version of Disney+ is set to see a 27% price increase, rising from the current $11 to $14 starting October 12th. Similarly, the ad-free version of Hulu will experience a 20% price surge, reaching $18. The minimum prices for Disney+ and ad-supported Hulu will remain unchanged. Disney has also introduced bundled packages for ad-free versions of Disney+ and Hulu, available at a monthly rate of $20. Subscriptions with advertisements will be adjusted from $13 to $15 per month. Additionally, Disney launched an ad-supported version of its Disney+ service in various European markets and Canada in November. This marks the second price adjustment in less than a year, all in the pursuit of profitable streaming operations.

Taking a page from Netflix's playbook, Disney is taking measures to combat password sharing. While this move might yield short-term effects, its long-term success still hinges on the quality of the platform's content. Considering the 39% YoY revenue decline in the film business, as seen in the recent quarter's performance of Paramount Pictures (a subsidiary of Disney), the development of certain new intellectual properties (IPs) for Disney's films might not be proceeding as smoothly as hoped. Even established IPs are experiencing some degree of fatigue.

In terms of content diversity, Disney falls short of $Netflix(NFLX)$ offerings. To a significant extent, Disney's dedicated audience consists of families with children and devoted Marvel enthusiasts, among others. These demographics often subscribe based on the rhythm of specific content releases. Fluctuations in subscriptions may occur when content quality diminishes or due to seasonal shifts (like post-summer).

Currently, with the resurgence of outdoor activities worldwide, the performance of Disney's park segment is expected to continue strengthening, potentially surpassing pre-pandemic levels.

Summary

Bob's cost-cutting and efficiency-improvement actions are welcomed by investors and bring good news for long-term shareholders. However, in the short term, they might lead to increased downside risks.

Nevertheless, Disney's stock price has shown weakness this year, especially with its recent downturn, which has resulted in a decline in its valuation multiple to some extent, reflecting investor sentiment.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

They just keep killing the the brand and driving customers away. None of the issues were adressed in the call.. you cant expect already unhappy customers to come back by raising prices, lol

Just keep doubling the price of Disney Plus every year to offset the loss of subscribers.. Sounds like a great plan! I think it isn't going to happen when they are trying to come up with the cash to buy Hulu in 2024.

How the heck is this w*ke garbage up pre market when they report half a billion loss. Until they stop this left wing rubbish then this will bearish all day long

When & how much Div is DIS will be paying?

Disney lost 11.7 million subscribers!