What is Baba's Intrinsic Value - With Valuation Model

Following my previous post which talked about the quick analysis on $Alibaba(09988)$ $Alibaba(BABA)$ and JD after both announced their earnings last night, I will go a little more in depth about each company’s valuation and see how much should we change with our valuation model.

We will start first with Baba, and then I’ll do another one in the next post with JD.

The goal here is to look at it objectively (rather than from a biased point of view because of vested position), so I’ll flex my objective thoughts and if you agree or disagree you are more than welcome to let me know your thoughts in the comment sections below (though please provide your reasoning so we can have a meaningful discussion).

Segmental Reporting:

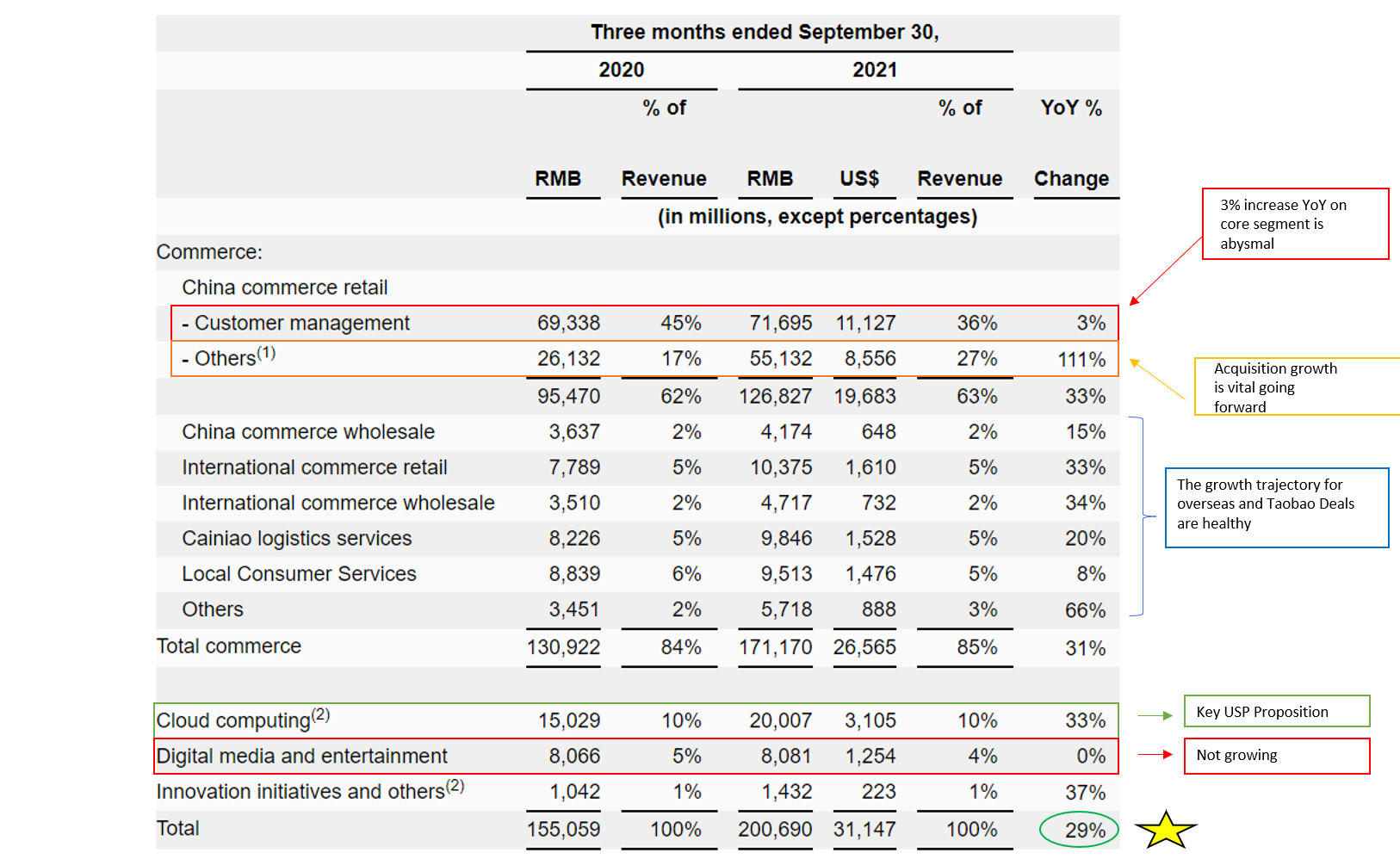

First, let us take a look at the segmental reporting of the business for this quarter which I think is key to understanding how the business have done in each of their respective segments.

The Positives:

Let’s start off with what we see as the positive signs.

First, as highlighted in yellow, the company is continuing to acquire and in this quarter, they have consolidated the Sun Art’s earnings into this Group’s earnings to give a better picture of what they are. You can see that this segment reported a 111% increase year on year and Sun Art has contributed quite a good significant increase in the overall.

In fact, without the Sun Art’s consolidation, total commerce will only grow by 16% instead at the 31% we are looking right now. This will remain a key pillar for growth for years to come.

The company continued to invest in their key strategic pillars – with the likes of Ele.me, Taobao Deals as well as international commerce segments which include the likes of Lazada and Trendyol. While Lazada and Trendyol are reporting a strong 80% year on year growth performance in their respective segments, Taobao Deals and the likes of Cainiao have not been monetized just yet. At this moment, they are still trying to build the right infrastructure to provide long term value creation for both the merchants and customers.

Cloud computing is the big elephants in the room that hardly anyone in the earnings call have talked about it just yet.

And it is rightfully so because we are still looking at a small base number of only RMB 20b.

However, the 33% growth is considered good and if they can maintain this growth trajectory rate over the next 5 years, it will end up at more than $80b by 2026, which has surpassed the CMR segment which is today bringing them the most. In other words, this will become the big elephants in the room for the much longer term to come.

The company is still building the right infrastructure and investment for cloud computing, which includes the recently announced design of the new chips which they can monetize in the future. For now, this is a negative ROI investment (even though they have turned positive EBITDA recently for this segment) but the ROI for the longer term is immensely powerful (just look at Amazon’s AWS).

The Negatives:

The CMR core segment only grows at 3% year on year and that is a big disappointment.

This can boil down to two factors – either the management is executing poorly or the regulation rules which includes the removal of the walled garden are impacting them. Or it can be due to a mixture of both.

This segment also faces the most intense competition from the likes of the smaller players like JD and PDD and the goal of common prosperity is likely going to benefit the smaller players – although we can argue that in the long run if middle income GDP increases nationwide, every players are going to eventually benefit.

Digital Media & Entertainment segment also disappoints. I think annual subscriber for Youku and Ali Pictures have not really taken off yet so they are not growing at all and will likely remain weak.

Growth Guidance FY22 & Beyond:

Management has guided for approximately 22-24% growth going forward for full year FY22.

If we do the maths behind, their first half exhibits a higher growth of around 29%, which means to say that their 2H will be much worse than what we are seeing today.

2H growth could come in at between 14-19% and the market could be disappointed further.

Still, if we look objectively at the overall growth of between 22-24%, it’s still a very respectable growth for that size of overall business.

While the management has not given a longer term growth prospect, I think we can sort of project based on our own guestimate.

Valuation:

Let’s flex a bit of muscle what this means from a valuation points of view.

It’s going to be a little complicated than the usual straightforward DCF we did in the past so please bear with me.

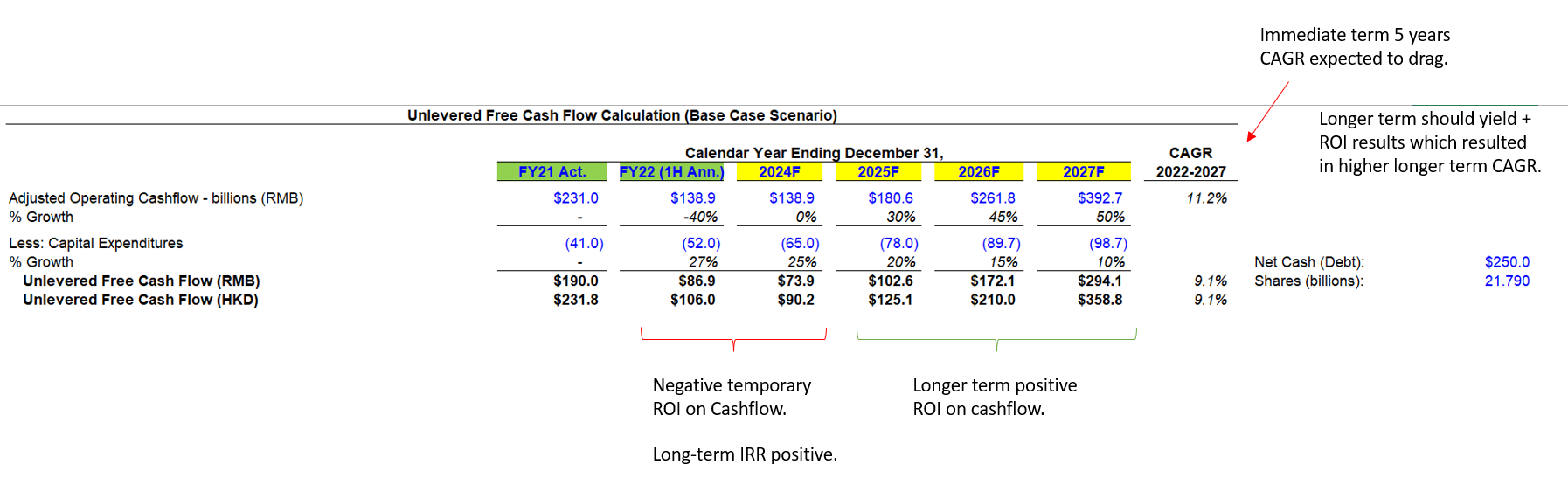

Let’s rewind a bit when the company reported its full year FY21 results.

The company had a great FY21 growth trajectory as compared to the previous year in FY20 and operating cashflow was at RMB 231b and analysts were tweaking their financial modeling to reflect the higher base and higher growth trajetory.

Then Q1 results came, and then another Q2 results last night.

In both the earnings result, the company exhibits a negative cagr on its operating cashflow as the company ramped up its spending on capex to build their key strategic pillars for both overseas and cloud computing.

As a result, 1H operating cashflow was down by a negative -40% as compared to the 1H of the previous year. At this point, the company is in a high spending mode and one might argue DCF might not be the most best options available in order to value the company. I’ll explain why.

The company reported an operating cashflow in Q1 FY22 of RMB 33.6b and in Q2 FY22 of RMB 35.8b. If we annualize this over the full year, this would come up to about $138.9b for the year.

In my model above, I have projected their “high capex spending” on their strategic pillars to last for another 6 more quarters (2H FY22 + FY23-24).

The ROI will then start to kick off from FY2025 onwards where cashflow > capex, resulting in a higher Free Cash Flow over the longer term.

This doesn’t bode well for the company in the short term as spending continues to pressure their EBITDA margin until the “investment” turns ROI positive.

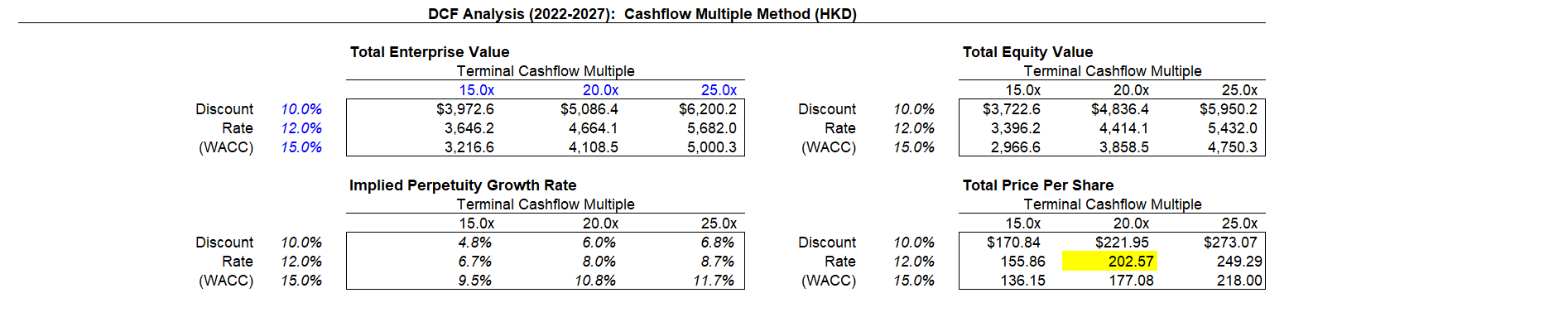

Using this model with a short term (2021-2027) CAGR of 11%, the company is worth at about ~HKD$202 in today’s price (after accounting for discount rate of 12%). This is about 30% margin of safety from what the shares are trading at right now.

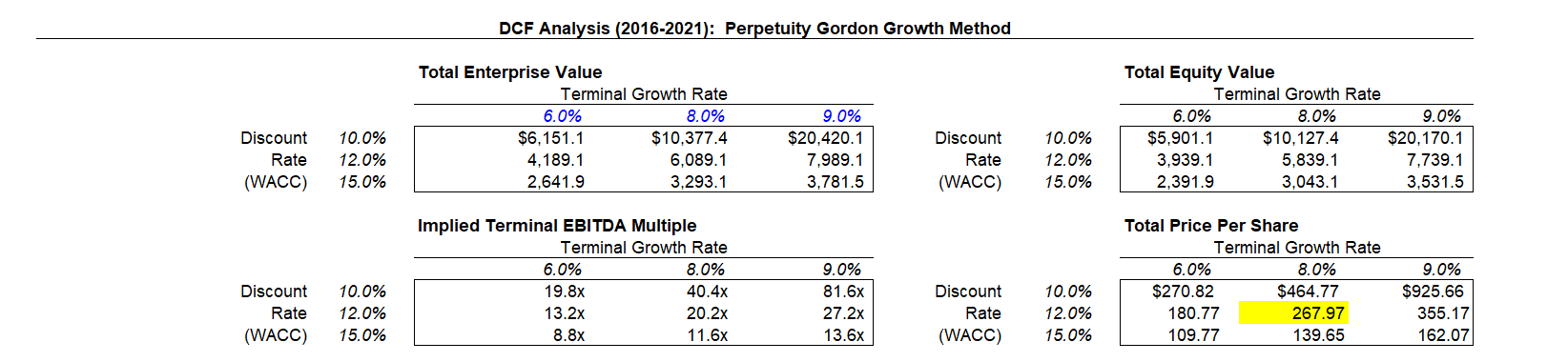

I did another type of model where I used the perpetuity growth method of valuing the company.

If we just ignore the short term fluctuations and think ok the company is going to grow at a perpetuity rate of 8% after accounting for inflation and discount rate, the company would be valued at about ~ HKD$267.

If the company remains a market leader in the industry, I think that’s quite a respectable amount of long term growth rate, and do note that we are talking about cashflow and bottomline growth here, so not just revenue topline.

Conclusion:

Based on the fundamentals alone, I think Baba would struggle for a while as they are back to the heavy capex spending stage where it is currently not yielding them any positive ROI on their cashflow. This will only yield results in the longer run where the infrastructure and platforms become more matured.

In the meantime, I think their China commerce segments will continue to struggle and lose market share to the smaller players and because of this, Baba would only be suitable for someone who had a much longer term view of its business (especially when cloud computing revenue starts to dominate in 5-6 years time). In the short term, the likes of JD and PDD would be a much better play if you are looking for exposure in this sector.

For me, I’ll likely just continue to hold my positions for now and have enough exposure in this sector (including JD) unless there is a further margin of safety which the market is giving me to add on. In the meantime, I’ll continue to monitor and provide further updates to the modeling after the next earnings call.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

for such a big coy to transform, it will not be easy, but such huge cash flow, its just a matter of time.

选择大于努力,远离中概,尤其是baba

哈哈