Walmart UP and Target Down, How's the trend in supermarkets?

After $Wal-Mart(WMT)$ 's Q3 earning super surge, $塔吉特(TGT)$ pivoted differently, with a plummet over 13%. Why Wal-Mart can survive from cost issue while TGT not?

Q3's concern, is downturning profits.

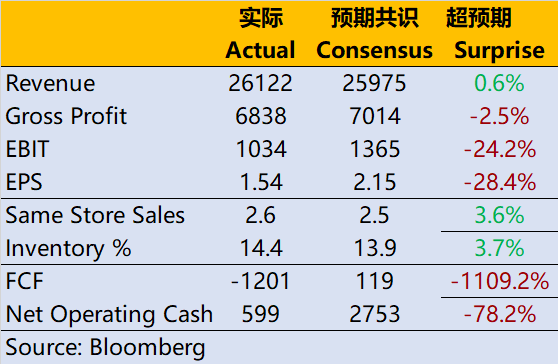

- The overall revenue was US $26.12 billion, a year-on-year increase of 3.29%, and remained in low single digits for three consecutive quarters, exceeding the market expectation of US $25.97 billion;

- Same-store sales increased by 2.7%, down 78% year-on-year, and also exceeded the market expectation of 2.5%.

- The gross profit margin was 24.7%, although higher than the low point of last quarter, it still fell by 12% and was also lower than the market expectation of 25.6%;

- The growth rate of inventory is 14.4%, which can be seen that it has dropped a lot from the level higher than 30% in the first few quarters of last year, and the market expectation is 13.9%.

- As management and sales expenses rose 7.4% year-on-year, further eroding profits, the final EBIT was $1.03 billion.It fell by 48% year-on-year, and fell far short of the expected $1.36 billion.

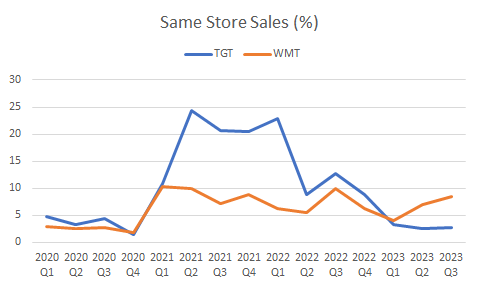

Obviously, the market has different views on retailers. Perhaps the news delivered by WMT was more positive before, and Q3's performance exceeded expectations, so the market took it for granted that TGT in the same industry could also create good results. From the key data-There is also a gap in the growth rate of same-store sales, which is 8.5% in WMT, 8.2% in North America, and only 2.7% in TGT

As a result, TGT told us the profit margin not controlled, and the gross profit margin from the source was less than expected. Not only did the previous high cost continue to consume gross profit margin, but the marketing expenses were soaring due to promotional activities, and the extra management costs caused by the tight supply chain were still there. Therefore, the overall profit margin is far less than the market expectation.

Compared with Wal-Mart's upward adjustment of Q4 performance, Target also lowered its forecast for Q4 shopping season, arguing that gift products will not sell well in this shopping season, and the whole non-essential consumer goods will not sell well. But optional consumption accounts for almost half of TGT.

This is very interesting. Is it a TGT problem or an industry problem? If it is an industry problem, the goal set by WMT may be somewhat radical? If it is a problem of company management and the difference between different advantageous categories between supermarkets, the two companies may drift away.

It should be differentiated until the reveal of next report.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- st16·2022-11-18thanks for sharing4Report

- Dionysius·2022-11-19cos target is perceived to be more expensive right?2Report

- Svengers19·2022-11-19Thanks for sharing2Report

- chloe1021·2022-11-25[Speechless]LikeReport

- szesze23·2022-11-20OkLikeReport

- 小泉闯股海·2022-11-19谢分享LikeReport

- shreyas_kp·2022-11-19👍LikeReport

- gary9535·2022-11-19wowLikeReport

- huaer8497·2022-11-19❤️LikeReport

- nightson·2022-11-19[smile]LikeReport

- cowsmile·2022-11-19MmkLikeReport

- katgoh·2022-11-19okLikeReport

- BB88·2022-11-19谢谢分享LikeReport

- henryxie1688·2022-11-19okLikeReport

- boonk·2022-11-19OkLikeReport

- 茁壮成长的韭菜儿·2022-11-19kLikeReport

- DMTrader·2022-11-19kLikeReport

- CheeWee79·2022-11-19thanksLikeReport

- WayneSing·2022-11-19ok1Report

- liverpool777·2022-11-19good sharing2Report