The financial market in 2022 is destined to witness more market miracles.

We have been distracted by all the talk about the Ukrainian-Russian military conflict, you may not know that the yen has quietly fallen to a century low, and now the decline may have just begun. . .

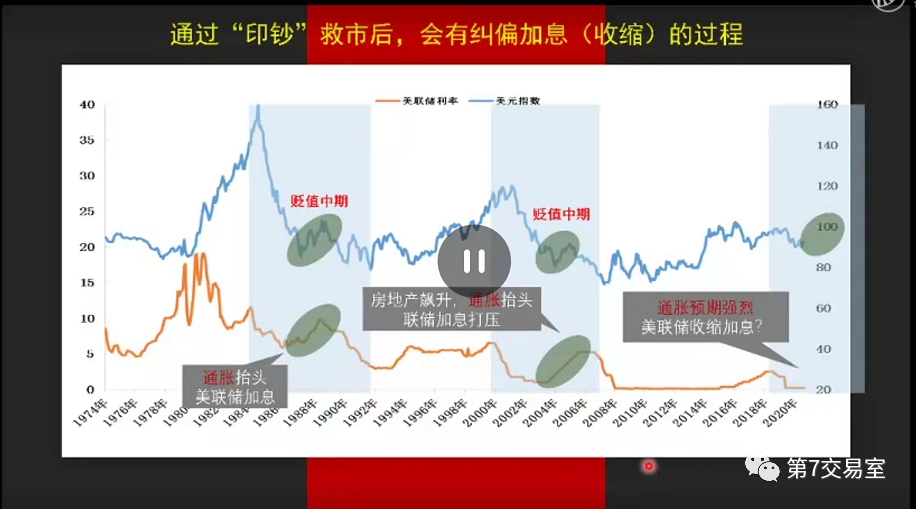

If you are an investment veteran, you will not be unfamiliar with the Plaza Accord. This ridiculous agreement signed in 1980s has become the most humiliating history in the history of modern Japanese economic development. It is also the first and last time that the Japanese yen and the US dollar have confronted each other head-on in the exchange rate market.。

Let's briefly review together:

At that time, it was the early 1980s, when the US fiscal deficit increased sharply and the foreign trade deficit increased. Therefore, the US Z government wants to increase its export competitiveness through the depreciation of the US dollar.

Under the leadership of the United States, on September 22, 1985, the United States, Japan, Germany, France and Britain held a meeting at the Plaza Hotel in New York, and reached an agreement: let the five countries jointly intervene in the foreign exchange market to induce the orderly depreciation of the exchange rate of the US dollar against major currencies.

After the signing of the agreement, the central banks of the five countries began to sell a large number of US dollars, and the US dollar depreciated sharply in a short time under the short-selling trend of the market. In less than three months, the dollar has fallen by 20% against the yen. In less than three years, the dollar has lost another 50% against the yen,,

The signing of the Plaza Accord is tantamount to giving international capital an official endorsement to speculate on the Japanese stock market and housing market. Once the market expectations tend to be consistent, the consequences will be terrible. In the five years after the agreement, the Nikkei index will grow wildly at a rate of 30% and the land price will increase at a rate of 15% every year, but the annual growth rate of Japan's nominal GDP in the same period is only about 5%.

When the asset bubble expands too violently and is far from the fundamentals, the overall collapse is not far away, and the flash collapse only needs some changes to puncture the bubble.

In 1989, In order to alleviate the soaring housing prices, the Japanese government implemented a tight monetary policy. In just a few months, the Japanese stock price and land price plummeted by more than 50%, the capital chain of banks broke, a large number of bad debts spread widely in the financial system, foreign capital began to flee, the yen plummeted against the US dollar, and the Japanese economy entered a recession period for more than ten years.

What is even more frightening is that, These foreign capitals that originally speculated on Japan's stock price and land price, Escape from the top when a crisis occurs, After the crisis, when the stock price tended to be flat, it came back in the name of saving the market, and comprehensively acquired a large number of excellent assets in Japan. At that time, a large number of enterprise controlling shares and lot ownership were grabbed by foreign capital. Since then, Japan has become a country with inflated sovereign debt, long-term fiscal deficit and absolute dependence on foreign capital.

It is no exaggeration to say that the yen may repeat its original plunge. The Japanese government is difficult to control the spread of the crisis, more importantly, the collapse of the yen on the Asia-Pacific markets and emerging markets brought a very serious impact.

Inflation sweeps across the world, and countries begin to compete for endurance

The yen is likely to crash before the euro

It is hard to say that the conflict between Russia and Ukraine is coming to an end. Russia has not even got the absolute control of the East Barton region. After more than a month of conflict, the Russian army only engaged in some seesaw battles on the periphery of Ukraine, which is in the psychology of protecting civilians. The Russian army has not yet achieved absolute occupation of Donetsk and Luhansk, the two most controversial regions.

When the situation in Ukraine and Russia is delayed, the United States starts the process of raising interest rates again. For other economies in the world, there will be two huge threats

One is the re-reign of a strong US dollar. How to maintain the stability of the exchange rate of the local currency in the foreign exchange market and prevent a large amount of foreign capital from returning to the US dollar is the most important thing.

Second, when inflation sweeps across the world, causing global bond yields to increase and bond prices to plummet, how to control inflation and bond yields on the basis of ensuring economic and stock market stability, or more directly, without imposing austerity policies, is also a headache for leaders of various countries.

We probably underestimated Biden, an old man who is nearly 80 years old,

As far as American is concerned, his policy of letting America reap profits is timely and ruthless. At present, the Fed's expectation of raising interest rates this year has risen to nine times, and the yield of US 2-year bonds has reached a high of 2.6 after taking into account the interest rate increase of more than 200 bps.

From the historical trend of the US dollar, the US dollar will rise for several months after the start of interest rate hike. As far as the current trend of US bond yields is concerned, the rise of the US dollar is only the beginning

Under the suppression of the strong US dollar, all countries have the pressure of foreign capital returning, which is most obvious from the performance of the foreign exchange market. As a freely convertible low-interest currency, the Japanese yen has long been used by various funds as the base currency for borrowing.

That is to say, A lot of money invested in the Asia-Pacific region is borrowed in yen first. And then reinvest in other monetary assets, To earn the difference,

The most popular form of trading is to borrow yen to invest in RMB assets or Australian dollars. Canadian dollar assets, Or just holding foreign currency to earn interest margins, In recent years, this way of cross-market arbitrage has made a steady profit, because Japan has reduced its interest rate to the lowest after experiencing the impact brought by the Plaza Accord. For a long time, Japan has kept its real interest rate at 0 or even negative, so the interest rate cannot fall, and it has naturally become the first choice for hedging and borrowing.

However, the current market situation has undergone tremendous changes. After the Ukrainian-Russian war started, the Federal Reserve also announced that it would insist on raising interest rates, which gave an official expectation that the US dollar would continue to appreciate.When the market expectations tend to be consistent, the scenes of forcing short or forcing long will be repeated, which we call "corn risk"

Imagine what you would do if you knew that Japan could not raise interest rates and that the US dollar would definitely appreciate in the future. Of course, it is to follow the trend of selling yen and buying dollars. It will lead to a short market in the US dollar and a long market in the Japanese yen. Now, before the rise of the US dollar has started, this push has already happened on the Japanese yen

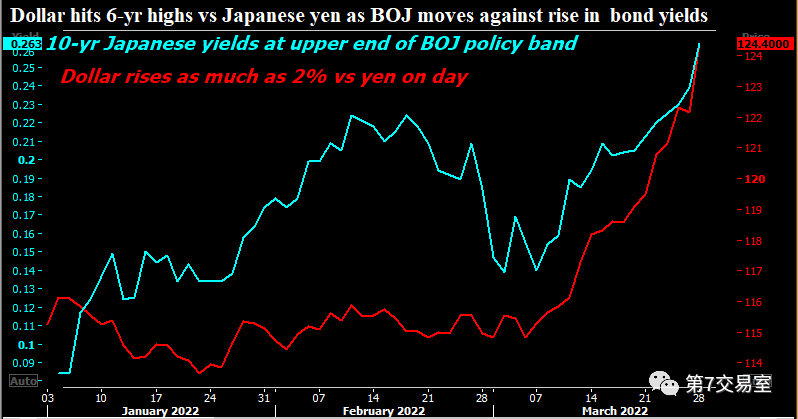

Since the beginning of this year, the yen has fallen by more than 7% against the US dollar (red line), which is already quite serious in the exchange rate. With the improvement of domestic inflation expectations, the yield of Japanese 10-year government bonds (blue line) has also risen sharply.

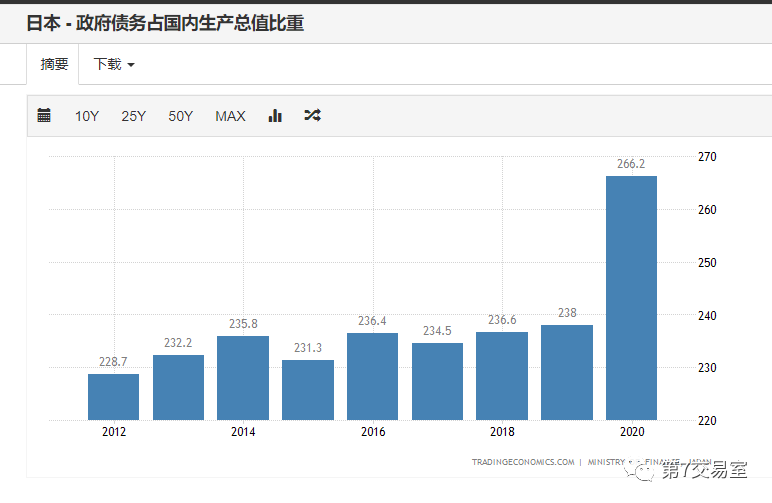

This scares the Japanese government, which has long been known for its debt finances, with its debt-to-GDP ratio at 238%

The increase in the yield of national debt means the increase in interest and the further expansion of fiscal deficit, and the benchmark yield of 0.25% of 10-year Japanese debt is also the bottom line for a large number of foreign investors to hold Japanese debt.

Therefore, in order to maintain the yield of Japanese debt, the Japanese central bank has started an unlimited bond purchase strategy, which is a very dangerous action, which will only make the yen depreciate even more.

Since the beginning of this week, the Japanese central bank has purchased more than 2.5 billion US dollars of bonds, but the price of Japanese government bonds has hardly risen, and Japanese bonds have been continuously sold off for five years. It seems that this policy of carrying faggots to put out fires will continue in the next few weeks. The depreciation of the yen is only the beginning.

Let's look at the dilemma facing the government next day:

At present, the nominal interest rate in China has been reduced to negative, and there is a large deficit in trade, which means that high-priced raw materials and energy commodities will exert imported inflationary pressure on Japan. The current account and government budget are both negative, and both foreign trade and finance are in deficit! This has almost decided that Japan will not be able to protect itself from the coming storm of a strong dollar and high prices.

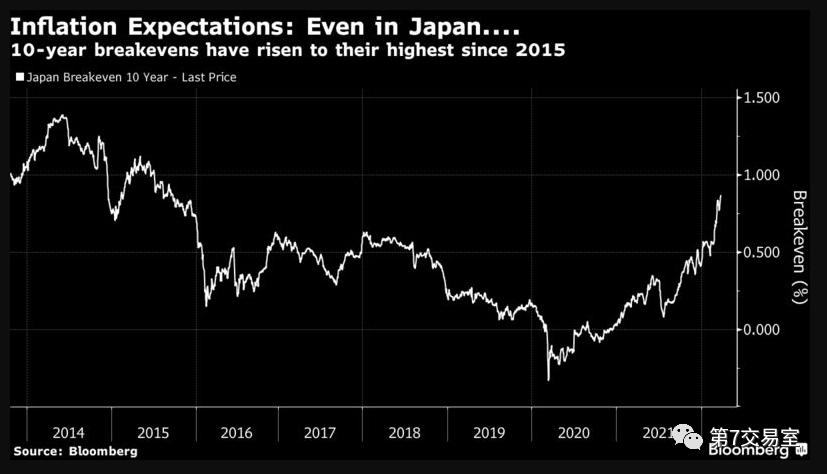

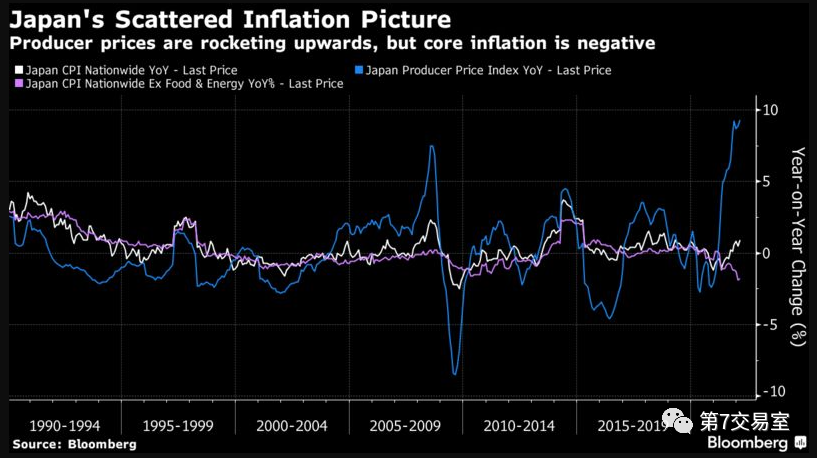

Let's look at Japan's 10-year levelingThe inflation rate index has reached a high level since 2015, indicating that inflation expectations are still expanding.

Japan's domestic consumer goods prices (white line) have not yet changed, and PPI raw material prices have soared (blue line) below

If it is impossible to raise interest rates, what awaits Japan is an unsustainable way to continue its life. Next may be: prices continue to rise, and foreign capital will accelerate its flight.

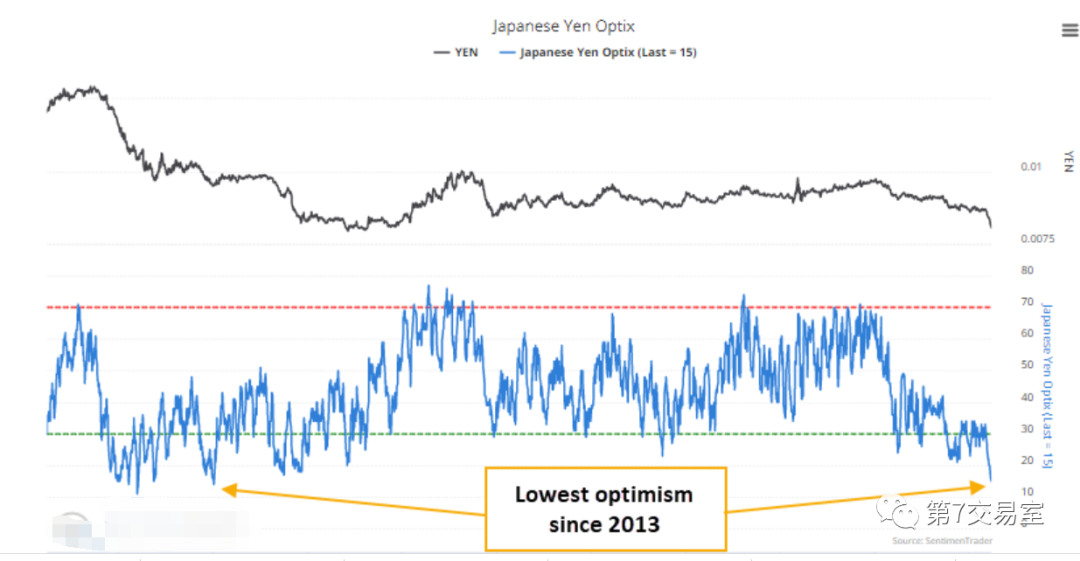

Shorting the yen is becoming more and more popular

First of all, we tracked the yen optimism index to the lowest level in 2014, indicating that a large number of short positions have been pressed against the yen.

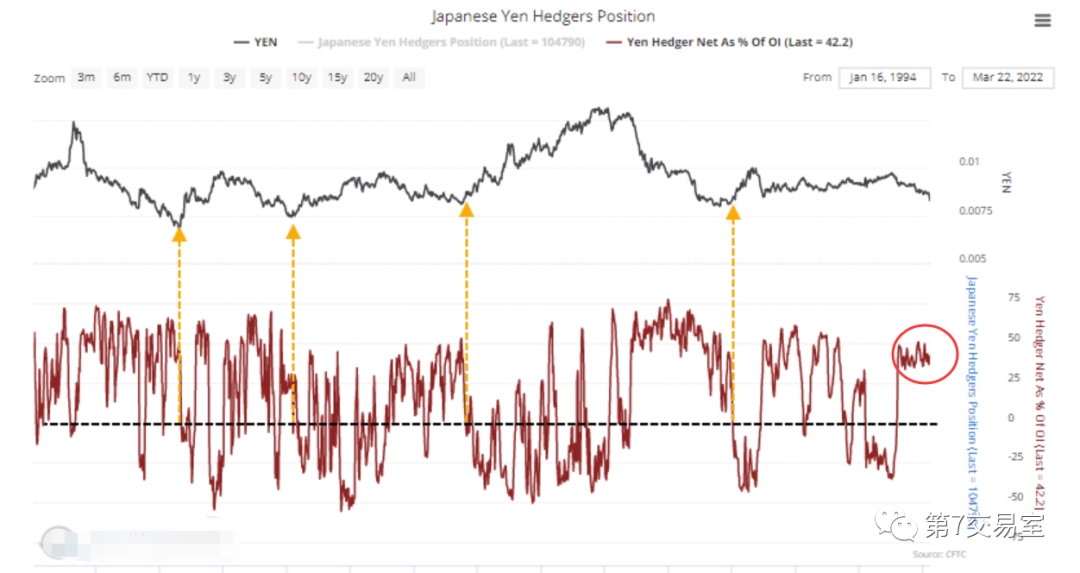

From the perspective of hedging index, the hedging index of Japanese yen has shown a high net long position for more than two years,

Don't be surprised, the net excess on the hedge means the net excess on the base, and this short position will be even larger. At present, the yen has reached the lowest level in 2016, so it seems that there is still much room for the yen to fall

Although I shared several major sectors worth bargain-hunting in A shares a month ago, including real estate stocks,

In the recent period of time, real estate stocks have also soared. I believe that if you follow our installments for a long time, you have already made some profits. However, as far as the current trend of the yen is concerned, you should always pay attention to stopping the profits, because the selling of the yen as the basic borrowing fund will trigger the linkage selling of these foreign capitals with leverage. Simply put, if you borrow yen to buy AG, if there is something wrong with yen, do you have to sell it before you can exchange it for yen and return it?

If it is too sensitive, I won't say much. After all, the content of the community still needs some awareness of risk prevention and control, unlike the personal site of private public accounts. In short, the short yen may be an opportunity, and real estate stocks should pay attention to stopping profits recently, don't you think?

$Japanese Yen - main 2206(JPYmain)$ $E-mini Nasdaq 100 - main 2206(NQmain)$ $E-mini Dow Jones - main 2203(YMmain)$ $Gold - main 2206(GCmain)$ $Light Crude Oil - main 2205(CLmain)$

Comments

[Happy]