Bad news is no longer regarded as good news.

The US stock market closed slightly lower on the first trading day of August, but the signal was huge-bad news was no longer regarded as good news, which was a huge change in market sentiment.

Look at other markets:

-The US dollar index fell for four consecutive trading days, falling 1.71 or 1.73% in the past four trading days

-In the bond market, the yield of 30-year US bonds fell below 2.92% for the first time since April. The 10-year yield was 2.605%, down from 2.642% last Friday (down sharply from the closing high of 3.482% hit in June). Meanwhile, the yield on the 2-year Treasury note was at 2.909%, continuing the upside-down yield curve seen as a key predictor of the recession. Recently, the focus of the market shifted from inflation to the deterioration of economic growth fundamentals, which pushed the yield of US bonds to continue to fall.

-Bitcoin fell 3.26% to $23,027.05

-Gold rose above $1,770

-Oil prices have fallen sharply

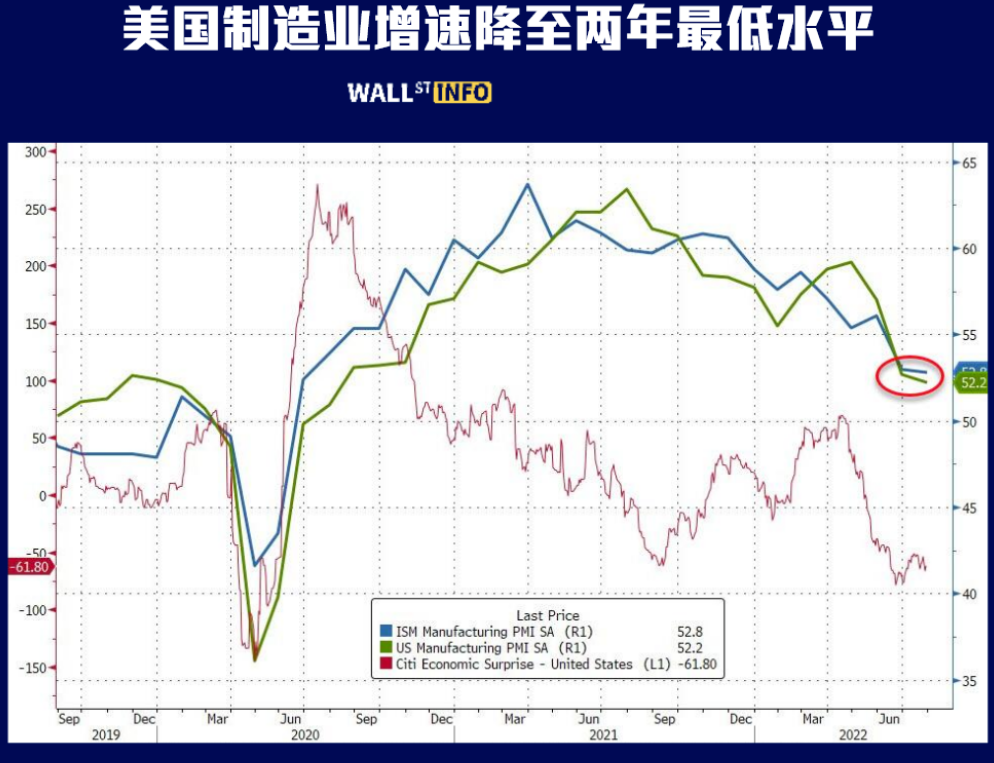

For Wall Street traders, yesterday's most interesting news was the ISM manufacturing data of the United States in July.

Data show that the ISM manufacturing PMI of the United States dropped to 52.8 in July from 53 in the previous month (reading above 50 indicates expansion), which is the lowest level since June 2020.

Meanwhile, the index of new orders is in a shrinking area for the second consecutive month. The ISM Manufacturing Inventory Index rose to 57.3, the highest level since 1984, indicating that more manufacturers have increased inventories (shrinking orders and increased inventories have led to more factories cutting production).

Experts are now worried about a weaker economy as new indices fall again and supply chain inventories show signs of excess.

After the data was released, the Atlanta Fed sharply lowered its GDP growth in the third quarter (from 2.1% to 1.3%).

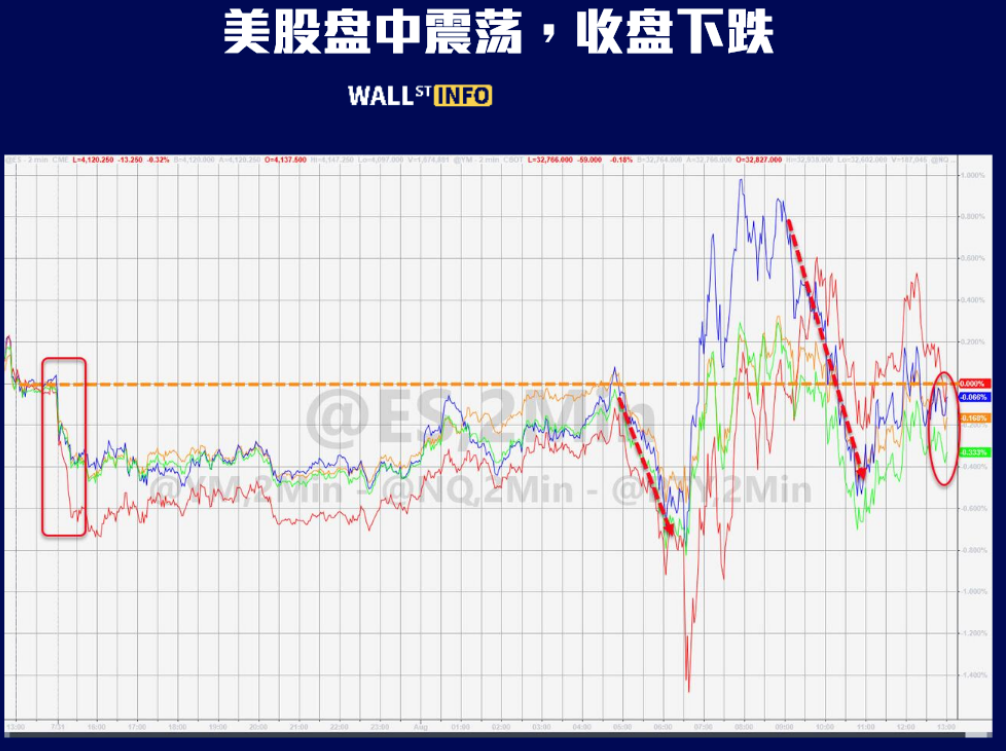

This is not a very good data, which frustrated the opening of US stocks.

However, from the comparison of the opening and closing data of US stocks, some of the declines were recovered at the close, and there must be a game:

-US stocks opened: Dow Jones index opened down 0.44%; The S&P 500 index opened down 0.68%; The Nasdaq index opened down 0.60%

-US stocks closed: the Dow Jones index closed down 0.14%, and the S&P 500 index closed down 0.29%; The Nasdaq closed down 0.18%

Long before this data was released, there was a debate that the market's view on the path of raising interest rates was completely different from that of the Federal Reserve.

Market view: Raise interest rates by about 90 basis points this year, and then cut interest rates next year.

September 22: Raise interest rates by 50 basis points (the first interest rate hike slowed down and exceeded the neutral level of interest rates)

Nov. 3: Raise interest rates by 25 basis points

December 15: May stop raising interest rates, or raise interest rates by 25 basis points (reaching the peak of interest rates)

Markets appear to be betting that the Fed has done most of its job on inflation and will accept slowing economic data.

Fed's view (about 50 basis points more than the market expected):

September 22: Raise interest rate by 50 basis points (the first rate increase slowed down and exceeded the neutral level of interest rate)-the interest rate reaches 3.00%-3.25%

November 3rd: Raise interest rates by 25 basis points (reaching the level predicted by the Federal Reserve at the end of the year)-the interest rate reaches 3.25%-3.5%

December 15: Raise interest rate by 25 basis points-the interest rate reaches 3.5%-3.75%

January next year: Raise interest rates by 25 basis points (reaching the peak of interest rates)

The Federal Reserve has repeatedly stressed the need to control inflation, and unless there are obvious signs of improvement, the Fed may not deviate from its position.

However, the current financial market trend is priced by "market view". Once the Fed's view occupies the peak, the financial market will have a revised trend.

Traders are more inclined to take the actual data as a guide to the debate between the two-in order to reason about the consensus level of economic recession.

Last night, US stocks did not rise after the ISM manufacturing PMI was released in July, and the signal sent was huge:

1. Last week's situation was that worse-than-expected economic data caused the stock market to rise instead, because the worse the data, the more investors bet that the Fed would end the interest rate hike cycle ahead of schedule.

2. After the poor data was released last night, US stocks fell, which was a small change in market sentiment, indicating that some prescient people began to consider that "the market misunderstood the Fed's interest rate hike".

3. However, US stocks only fell slightly, and the decline did not match the importance of the data, indicating that "the market's expectation of raising interest rates" still occupied the mainstream.

To a large extent, lightThe loose rising stage is over. Now it is at the crossroads of changing the disk, and several key data in the future will be set for this purpose.

The biggest focus this week will be Friday's US non-farm payrolls report. Before that, Chicago Fed Chairman Evans and St. Louis Fed Chairman Brad will speak at different events on Tuesday, and Cleveland Fed Chairman Meister will speak on Thursday.

$E-mini Nasdaq 100 - main 2209(NQmain)$ $E-mini Dow Jones - main 2209(YMmain)$ $E-mini S&P 500 - main 2209(ESmain)$ $Gold - main 2212(GCmain)$ $Light Crude Oil - main 2208(CLmain)$

Comments