After getting pummeled in 2021 and early 2022, there are some great reasons to invest in NFLX this month.

Dropping a whopping 42% in 2022, Netflix has disappointed many investors as of late. And NFLX’s problems stretch farther back than the YTD - indeed, the company's current share price (about $345) sits well below its price this time last year (about $500). Much of Netflix’s dramatic tumble can be attributed to the company's failure to meet market expectations for subscriber growth and profit.

Even so, Netflix remains a company that many on Wall Street like, with some investors believing the stock is downright cheap at today’s prices. Here, we’ll take a look at some factors that might justify investing in NFLX in the coming months.

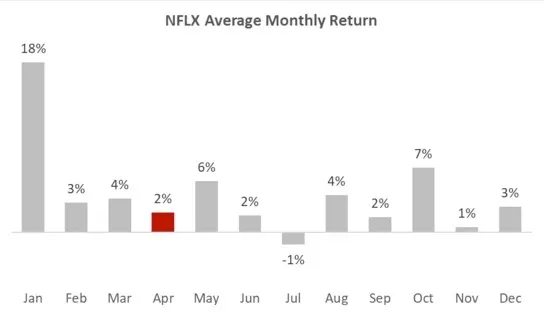

Past returns show May is a strong month for NFLX

Looking at the historical data, April has usually been a poor month for NFLX. May, on the other hand, has historically been solid - with an average growth of 6%, May has the third-highest average monthly return for NFLX.

Of course, patterns can change, and plenty of NFLX’s historical returns can be attributed to noise. But given Netflix’s steep decline over the past several months, a turnaround in May - a historically strong month for the company anyway - doesn’t seem out of the question.

Price close to pre-pandemic value, yet business is much more robust

In January 2020, just before the onset of the Covid pandemic, NFLX was trading at $325 per share. That’s only 6% below the price it’s trading at today (approximately $345, at the time of writing).

But Netflix’s streaming business has changed significantly since early-2020. Segment trends have accelerated, and the company has improved its leverage and growth metrics. Given these drastic improvements, it doesn’t make much sense for NFLX to be pegged at the valuation it had nearly two years ago.

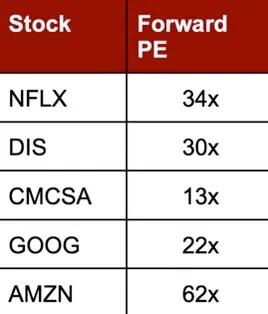

Valuation in line with technology peers

Although plenty of investors still consider Netflix’s valuation to be rich, the company is trading at much lower multiples than it saw in 2021 and 2020. Currently, the NFLX has a forward PE that’s close to the PE off some of its key competitors, such as Disney - and its PE is well below those of other players in the tech sector, such as Amazon.

The confluence of these three factors - historically positive movement in May, a depressed valuation compared to 2020, and a reasonable PE compared to peer companies - means Netflix may be presenting a solid buying opportunity at current prices.