Summary

- Apple stock received a lot of interest recently as it surged in early December and has maintained its market outperformance.

- We discuss the critical drivers for investors to watch moving into 2022.

- We also discuss whether Apple stock is likely to reach $200 moving forward.

Investment Thesis

Apple Inc. (AAPL) has recently drawn significant interest among investors as the stock has continued to outperform the market since early December. It's notable since AAPL stock has lagged the market for almost the whole year. However, investors' interests spiked following the series of successful new product launches, including its pivotal iPhone 13.

Supply chain checks from numerous sell-side analysts have also demonstrated that the delays over its iPhones have improved markedly. In addition, Goldman Sachs also highlighted that lead times were down significantly in mid-December as Apple continues to leverage strong iPhone demand in its most crucial calendar quarter.

AAPL stock continues to hold its price steadily, briefly topped a $3T market cap milestone. However, there shouldn't be any doubt that AAPL stock has had an unmistakable long-term uptrend over the years. Moreover, given that the company has multiple long-term secular drivers driving its business model, we are confident that the stock can reach $200 in 2022.

We discuss these critical drivers for AAPL stock as we head into 2022 with the $3T market cap looking over the horizon.

Services Revenue Growth Could Have Been Significantly Understated

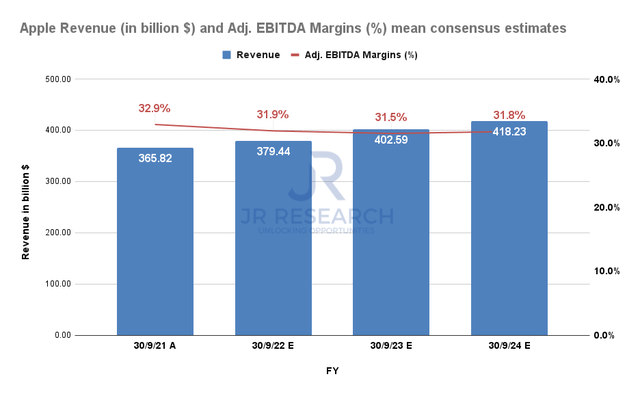

Apple bears have often pointed out the deceleration in the company's topline growth as proof of a stock that is massively overvalued. It's easy to understand what they mean. Readers can refer to the chart above, where Apple's revenue growth is estimated to decelerate over the next three years. Consensus estimates point to a revenue CAGR of just 4.6% through FY24. Moreover, its adjusted EBITDA margins are likely to remain consistent. But, AAPL is not projected to gain leverage towards its profitability. Hence, bearish investors claim they don't understand how the Cupertino company can continue to justify its current valuation.

But, we think investors need to step back and consider the critical growth drivers for AAPL moving forward. So let us present our analysis.

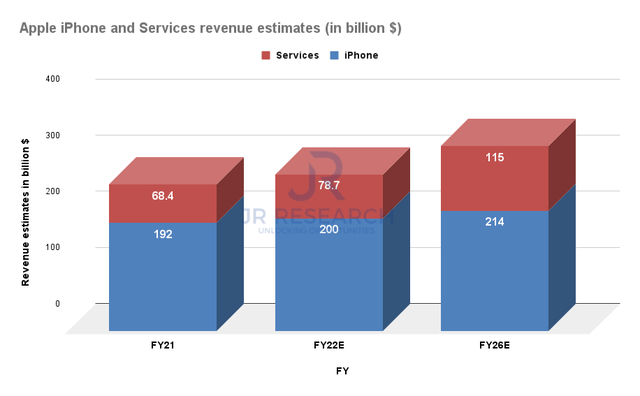

Readers can refer to the above model, where iPhone's revenue is estimated to increase at a CAGR of just 2.2% over the next five years. However, Apple's services segment (including App Store's revenue) is projected to increase its revenue at a CAGR of 11% through FY26, reaching $115B. We think these estimates are relatively conservative. Based on these estimates, a SOTP implied fair value of $159 was reached for AAPL stock. It also includes other segments but was mainly driven by the two critical segments above. iPhone and services accounted for 43% and 25% of its SOTP valuation.

But, we believe that these estimates may not have captured the multiple growth drivers underpinning the App Store. Why?

Based on recent estimates by Sensor Tower, App Store's revenue is estimated to increase at a CAGR of 20.7% through CY25, reaching $185B. Notably, it's way ahead of the estimate of $115B that we discussed earlier for the entire services segment. Importantly, we have not even included revenue from the other services other than App Store's contribution. Therefore, we think that readers need to consider that the Street consensus may have significantly underestimated the prowess of Apple's highly profitable (estimated operating margin > 70%) App Store.

We are not saying that Sensor Tower's estimate is the source of truth. But, we wanted to highlight that investors should pay more attention to Apple's key services segment. Sensor Tower presented a region by region breakdown, which we thought seemed credible, and we encourage investors to monitor closely.

Don't Ignore Apple's Metaverse Ambitions

Renowned TF International Securities analyst Ming-Chi Kuo estimated that Apple's AR/VR device would be released sometime in Q4'22. We believe this is significant as it augurs well for Apple's ambitions into the metaverse. There's little doubt that Meta Platforms (FB) and Microsoft(MSFT) are strengthening their lead in the consumer and commercial AR/VR space.According to TrendForce, global AR/VR device shipment is estimated to reach 12.02M units, up 26.4% YoY in 2022. Moreover, the market is estimated to grow rapidly through 2025, reaching 25.76M units at a CAGR of 38.8%. Notably, it expects Meta's Oculus devices to maintain a 66% consumer market share. But, TrendForce also noted that (edited):

AR/VR device suppliers may look to expand their user base and increase their market penetration via low-priced yet high-spec devices,while compensating for their reduced hardware profitability through software sales. (TrendForce)

Software sales indeed. Apple runs the largest mobile ecosystem globally, which dwarfs Google Play's (GOOG) (GOOGL) revenue. Therefore, we believe the entry of Apple into the metaverse game could significantly raise the company's monetization opportunities. Theories that Meta Platform has ambitions to displace Apple as the next-gen computing platform abound. However, we have also discussed thatMeta Platforms' eventual metaverse will unlikely be the only virtual world we will ever experience. Instead, the metaverse will likely be a series of interconnected virtual worlds that will be interoperable. So, Apple could still be the critical ecosystem owner as creators build their virtual worlds to be monetized through the App Store, reaching out to Apple's more than 1B (and growing) installed base.

TrendForce also added that global VR content revenue is estimated to grow at a rapid 40% CAGR through 2025, reaching $8.3B. The content will be varied but primarily consisting of "gaming/entertainment, videos, and social interactions." Therefore, Apple can continue to leverage such opportunities through its massive ecosystem. We think these opportunities are so novel that it hasn't even been written into Apple's consensus estimates just yet. But, once Apple's AR/VR devices are launched, we believe that the revenue runway could become even more apparent. However, we must still caution that we are still very early into Apple's metaverse ambitions. But, we believe that Apple will be a critical player in defining the metaverse through its ecosystem. It won't be very smart to consider that Apple doesn't have a clearly-defined metaverse strategy.

So, is AAPL Stock a Buy Now?

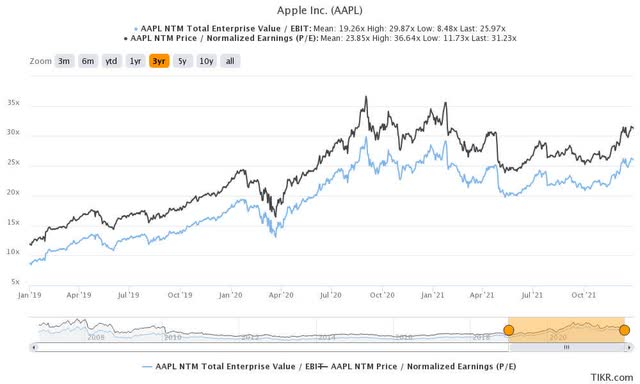

If you consider AAPL stock's relative valuation against its 3Y mean, there's little doubt that AAPL stock seems expensive. It's trading at an EV/NTM EBIT of 26x, way above its 3Y mean of 19.3x. In addition, its normalized P/E (NTM) also read 31.2x, significantly ahead of its 3Y mean of 23.9x. Therefore, we wouldn't blame bearish investors who think that AAPL stock seems well overvalued now.

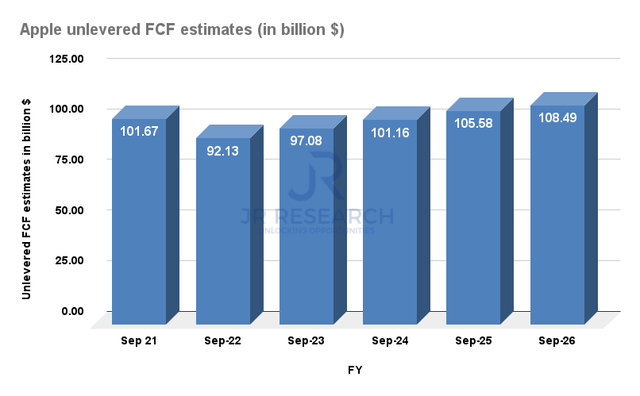

However, we also estimated that AAPL stock would continue to generate robust FCF growth over time. Moreover, our model is even more conservative than the consensus estimates. In addition, we have also not considered Sensor Tower's estimates or Apple's metaverse opportunities that we discussed earlier. Nevertheless, it led us towards a DCF implied fair value estimate of $153, which we highlighted in our previous article. It's also quite close to our SOTP implied fair value of $159 that we showed earlier. Therefore, it's clear that these estimates have not factored for the robust services growth and the potential metaverse opportunities that could accrue to Apple over the next five to ten years.

Nevertheless, we think that AAPL stock looks extended, as seen above. But, as mentioned, it wouldn't be very smart for investors to bet against CEO Tim Cook & Co. The stock's long-term uptrend is clear for all to observe.

So, we are clear that the stock would likely break the $200 level in 2022 as the excitement surrounding its AR/VR launch gets closers, coupled with its services segment revenue growth in its earnings releases. As a result, we believe that AAPL's stock price could be re-rated to reflect its potential over the next year.

Nevertheless, due to its over-extended price action, we encourage some patience with AAPL stock. But, if you have no AAPL stock, we think you can consider adding at this price if you are a long-term investor. We don't believe it's significantly overvalued, as discussed earlier. But, if you already have considerable exposure relative to your portfolio, we think you can wait for a potentially better entry point with some patience.

Therefore, we reiterate our Neutral rating on AAPL stock for now.

This article was written by JR Research.